The S&P 500 has risen for seven consecutive weeks—should you chase the rally or take profits?

Analysis of the Rotation among 11 Major Sectors in the US Stock Market (April 20): Defensive Themes Remain Dominant, Technology Shows Short-Term Recovery

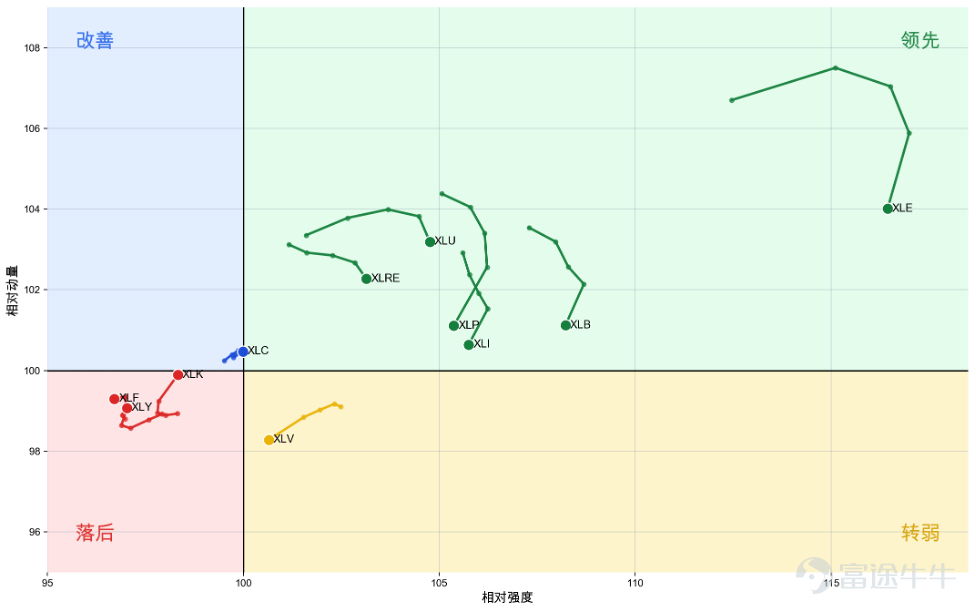

Summary: As of the close of the US stock market on April 17, at the weekly level, the leading sectors in the rotation among the 11 major sectors were still dominated by Energy XLE, Materials XLB, Industrials XLI, Utilities XLU, Real Estate XLRE, and Consumer Staples XLP, indicating that the medium-term trend remains biased towards defense and resources. At the daily level, Technology XLK has already returned to the leading zone, while Consumer Discretionary XLY and Industrials XLI have entered the improvement zone, showing a marginal recovery in risk appetite. However, Energy XLE has weakened rapidly on a daily basis, suggesting that the previously strongest sector is undergoing short-term consolidation. The current market is closer to a transitional phase characterized by an 'unbroken defensive theme with growth recovery initiating.'

1. Weekly Rotation: Medium-Term Trend Remains Biased Towards Defense and Resources

The leading area on a weekly basis is still occupied by Energy XLE, Materials XLB, Industrials XLI, Utilities XLU, Real Estate XLRE, and Consumer Staples XLP. Among them, Energy XLE's relative strength reached 116.44, and its relative momentum was 104.01, making it the strongest sector in the medium term. Materials XLB and Industrials XLI remain on the right side of the leading area, indicating that the resource chain and pro-cyclical manufacturing chains still hold advantages over SPY. Meanwhile, Utilities XLU, Real Estate XLRE, and Consumer Staples XLP are also within the leading area, showing that capital has not completely shifted towards high-elasticity offense but continues to allocate towards low-volatility and more defensively oriented areas.

On the other end, Healthcare XLV has fallen into the weakening zone, while Communication Services XLC has entered the improvement zone and is approaching the boundary between strength and weakness. Although Technology XLK and Consumer Discretionary XLY are still in the lagging zone, their relative momentum rebounded significantly over the past week, with Technology XLK showing an especially steeper recovery slope. Financials XLF remain in the lagging zone and have marginally weakened further over the past week, indicating that the current mid-term structure has not yet evolved into a full return of risk appetite but is instead starting with exploratory recovery in specific growth sectors.

Second, daily rotation: Technology XLK strengthens, while Consumer Discretionary XLY follows with recovery

The daily structure has already signaled a style rotation earlier than the weekly chart. Technology XLK has returned to the leading area, with its relative strength and relative momentum continuously rising over the past five trading days, making it the clearest short-term offensive direction currently. Consumer Discretionary XLY has entered the improvement zone, while Industrials XLI is also near the upper edge of the improvement region, indicating that market risk appetite is undergoing a tentative recovery. Communication Services XLC is still consolidating sideways within the lagging region; if it subsequently crosses above the strength boundary, the recovery in growth sectors would be more complete.

Meanwhile, Energy XLE has quickly plunged deep into the lagging region on the daily chart, with its relative strength dropping to 95.63, showing that the previously strongest mid-term sector has significantly cooled in the short term. Materials XLB and Financials XLF are in weakening zones, while Utilities XLU, Healthcare XLV, and Consumer Staples XLP have retreated back into the lagging region. In other words, short-term recovery has begun, but it remains concentrated primarily in the localized rebound driven by Technology XLK, without yet expanding into synchronized strength across the entire market.

Third, trading strategy

In determining the current main trend, medium-term allocation should still anchor on the defensive and resource chains that maintain leadership on the weekly chart, focusing on Energy XLE, Industrials XLI, Materials XLB, Utilities XLU, and Real Estate XLRE. Among them, although Energy XLE remains the strongest sector on the weekly chart, its daily performance has clearly pulled back. The cost-effectiveness of chasing highs in the short term has diminished, making it more suitable to wait for consolidation before confirming again.

For short-term recovery, Technology XLK is the primary observation target, while Consumer Discretionary XLY is the second tier. If the market continues to recover, we should first see Technology XLK continue advancing in the leading region on the daily chart, driving Communication Services XLC back above the strength dividing line. If this round of recovery holds, growth-style sectors' outperformance relative to SPY is expected to expand further.

The key verification points going forward are threefold: First, whether Technology XLK can maintain its daily lead over the next several trading sessions and further push the weekly chart out of the lagging region. Second, whether the weekly leadership of Energy XLE, Materials XLB, and Industrials XLI can regain momentum after their daily pullbacks. Third, whether Financials XLF and Healthcare XLV can stabilize and reverse their declines; otherwise, the market will remain more like a structural rotation rather than a broad-based increase in risk appetite. Until these three conditions are met simultaneously, the strategy should retain a defensive base while using the short-term recovery in Technology XLK and Consumer Discretionary XLY as flexible supplements.

$S&P 500 Index (.SPX.US)$ $SPDR S&P 500 ETF (SPY.US)$ $NASDAQ 100 Index (.NDX.US)$ $Invesco QQQ Trust (QQQ.US)$ $Dow Jones Industrial Average (.DJI.US)$ $State Street® SPDR® Dow Jones Industrial Average® ETF Trust (DIA.US)$ $Russell 2000 Index (.RUT.US)$ $iShares Russell 2000 ETF (IWM.US)$ $USD (USDindex.FX)$ $U.S. 10-Year Treasury Notes Yield (US10Y.BD)$ $XAU/USD (XAUUSD.CFD)$ $Real Estate Select Sector Spdr Fund (The) (XLRE.US)$ $The Technology Select Sector SPDR® Fund (XLK.US)$ $The Communication Services Select Sector SPDR® Fund (XLC.US)$ $Consumer Discretionary Select Sector SPDR Fund (XLY.US)$ $Consumer Staples Select Sector SPDR Fund (XLP.US)$ $Materials Select Sector SPDR ETF (XLB.US)$ $Industrial Select Sector SPDR Fund (XLI.US)$ $Energy Select Sector SPDR Fund (XLE.US)$ $Financial Select Sector SPDR Fund (XLF.US)$ $The Health Care Select Sector SPDR® Fund (XLV.US)$ $Utilities Select Sector SPDR Fund (XLU.US)$

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

4

2