Become a fan of Pop Mart's Wang Ning, and Duan Yongping's 14.5 billion 'slap in his own face'

(This article was written by Radar Finance and authorized for publication by Titanium Media)

Text | Radar Finance, Author | Peng Cheng, Editor | Meng Shuai

From stating 'I won’t invest' to 'I am indeed a fan of Wang Ning now,' Duan Yongping, known as the 'Chinese Buffett,' made a complete turnaround in his attitude towards Pop Mart.

Recently, Duan Yongping posted on the Xueqiu platform confirming that he is positioning himself in Pop Mart by selling put options.

Just months ago, Duan Yongping was skeptical about Pop Mart, openly stating, 'I can't understand why people would need this thing.'

As Duan Yongping officially began his investment strategy, Pop Mart recently delivered an impressive earnings report. Last year, the company achieved revenue of 37.12 billion yuan, a year-on-year increase of 184.71%, with a net profit attributable to shareholders of 12.776 billion yuan, surging 308.76% year-on-year.

However, beneath the seemingly dazzling performance, Pop Mart faces concerns such as increasing reliance on LABUBU from THE MONSTERS IP for revenue and a significant year-on-year rise in inventory.

During the 2025 annual earnings conference, Pop Mart’s Chairman of the Board and CEO Wang Ning stated that the company aims for growth of no less than 20% in 2026, but this guidance represents a sharp decline compared to last year's 184.71% revenue growth.

Moreover, as of the close on April 16, Pop Mart's latest share price had fallen by half compared to its historical high set last year.

Notably, according to the '2026 Hurun Global Rich List' released in March, Duan Yongping's net worth stood at 14.5 billion yuan.

Since the beginning of the year, renowned investor Duan Yongping has frequently mentioned Pop Mart on the Xueqiu platform.

On the morning of April 14, Duan Yongping posted to confirm that he is positioning himself in this leading trendy toy company by selling put options.

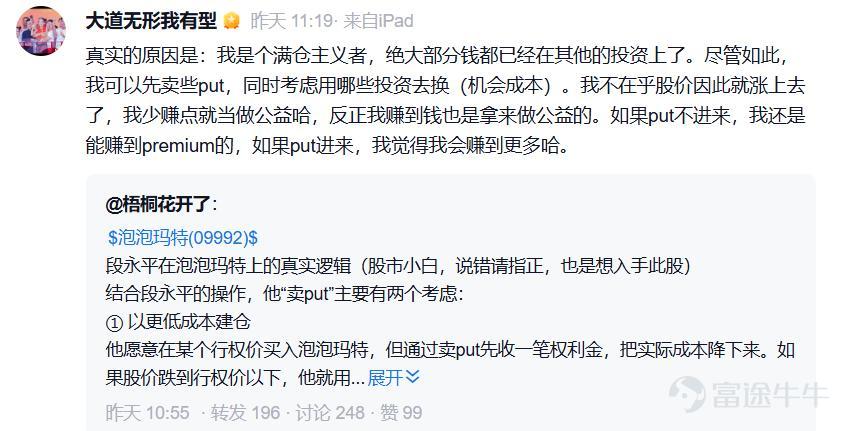

Duan Yongping explained: 'I am a full position investor, and most of my money is already tied up in other investments. Nevertheless, I can start by selling some puts while considering which investments to swap out (opportunity cost).'

Duan Yongping stated, 'I don’t care if the stock price rises as a result; if I earn less, I’ll consider it a charitable contribution, since any profits I make are ultimately for charity anyway. If the put option isn't exercised, I'll still earn the premium; if it is exercised, I think I'll make even more.'

In fact, Duan Yongping's move was not sudden. Prior to this, his attitude towards Pop Mart evolved from 'not understanding it' to officially taking a position.

At the beginning of the year, when discussing his view on Pop Mart, Duan Yongping said, 'I took a general look at Pop Mart and found them quite impressive. However, I still can’t understand why people would want these things—if everyone stops wanting them in a couple of years?'

The turning point came in late March this year when Pop Mart released its 2025 annual report, showing a record revenue of 37.12 billion yuan, surpassing the 30 billion yuan mark for the first time, with a year-on-year surge of 184.71%; net profit attributable to shareholders reached 12.776 billion yuan, soaring 308.76% year-on-year; gross margin increased from 66.8% in 2024 to 72.1%.

On March 30, Duan Yongping posted on Xueqiu: 'After spending time reviewing Pop Mart again over the past two days, I’ve decided to retract my earlier statement to Chairman Fang Sanwen (founder and chairman of Xueqiu) that I wouldn’t invest in Pop Mart.'

In the following days, Duan Yongping spent several days studying the company and frankly admitted, 'I haven't felt this excited in a long time.'

According to Duan Yongping, he reviewed an interview transcript with Wang Ning, founder of Pop Mart, titled 'Because of Uniqueness,' and also visited a Pop Mart store at Westfield in London.

This store, with an area of only about 60 square meters, left a deep impression on Duan Yongping: 'The business is indeed very good, the vast majority are adults, and the proportion of middle-aged and elderly people is very small, probably around 10%.'

Based on this observation, Duan Yongping reached a striking conclusion – 'I can't help but feel that Pop Mart is actually the pioneer of Chinese products going global. Other companies don’t seem to be at this level yet.'

On April 9, Duan Yongping posted on social media saying, 'My Pop Mart insurance company has officially opened,' formally confirming his investment in Pop Mart.

What he meant by 'opening an insurance company' is a metaphor for selling put options, a strategy he has applied multiple times before on stocks like Tencent and Apple.

The specific rule of this strategy is as follows: if the stock price does not fall below the strike price, the option seller earns the full premium; if the stock price falls below the strike price, the seller must buy the underlying stock at the agreed strike price.

In August 2024, when sharing his operation of selling put options on Tencent shares, Duan Yongping clearly stated, 'It’s just another insurance company opening up, earning some premiums.'

Duan Yongping admitted that he had a good impression of Wang Ning before but always felt that this business was too far removed from him, difficult to understand, and uncertain about its sustainability.

He also compared it to many once-popular toys like Tamagotchi, hula hoops, and Rubik's cubes, adding, 'I'm curious whether my understanding of gaming will pay off again with Pop Mart.'

In Duan Yongping’s view, Pop Mart’s competitive barriers are much stronger than imagined, including its established user attention (brand), artist signing barriers, stores worldwide, and Wang Ning and his team. 'As long as the trend toy market remains sustainable, Pop Mart is a fantastic business.'

On April 10, Duan Yongping further commented on his investment in Pop Mart: 'Slowly mobilize funds; otherwise, just collect some premiums for now.'

On April 11, while responding to a netizen's question, he added that he would gradually accumulate 'the desired shares' in the future.

This recent earnings report is quite impressive, showing such strong profitability,' remarked Duan Yongping, expressing his surprise at Pop Mart's latest annual financial results.

According to Tianyancha, Pop Mart went public on the Hong Kong Stock Exchange in 2020. However, beneath its seemingly stellar performance, concerns linger.

LABUBU, part of THE MONSTERS IP, has been contributing more revenue to Pop Mart, but the company's reliance on this IP has also been deepening.

The financial report shows that in 2025, THE MONSTERS contributed 14.16 billion yuan in revenue to Pop Mart, marking a year-over-year increase of 365.7%. Its revenue share also surged from 23.3% in 2024 to 38.1%.

Although Pop Mart claims to have 17 artist IPs generating over 100 million yuan in revenue each, there remains a significant gap between these second-tier IPs and THE MONSTERS.

For instance, SKULLPANDA, which ranks second in revenue contribution, generated 3.54 billion yuan last year, a mere fraction compared to THE MONSTERS, with a revenue share of just 9.5%. Meanwhile, MOLLY, once Pop Mart’s top performer, saw its revenue share drop from 16.1% to 7.8%.

This reliance on a single blockbuster IP has heightened market concerns about the sustainability of Pop Mart's performance.

In a recent report, HSBC Global Research analyst Lina Yan pointed out, 'The hyper-growth driven by LABUBU will fade,' and defined 2026 as the year for Pop Mart to 'reset its foundation.'

Moreover, as of the end of 2025, Pop Mart's inventory scale reached 5.473 billion yuan, a surge of 259% compared to 1.525 billion yuan at the end of 2024. The inventory turnover days also extended from 102 days to 123 days.

In response, Pop Mart explained that this was mainly due to an increase in the proportion of overseas revenue and long cargo transportation times on one hand, and on the other hand, a net increase of 109 global stores, which led to increased inventory to meet sales demand.

However, the significant growth in inventory scale and inventory turnover days suggests that Pop Mart may face the risk of inventory overstock.

Notably, during the 2025 earnings conference, Wang Ning officially announced that Pop Mart will launch derivative small home appliances centered around IPs such as MOLLY and LABUBU, available for sale through mainstream e-commerce platforms like JD.com.

Meanwhile, Pop Mart also clarified that the small home appliance business is a key component of the company’s IP group strategy, alongside desserts, films, and theme parks as core extensions of its IP ecosystem.

However, this cross-industry move has raised some investor concerns about the company's focus on its core business.

Some opinions suggest that Pop Mart’s new ventures, such as small home appliances, are still in the exploratory stage and may not contribute significant performance in the short term. Additionally, they could increase cost expenditures, dilute net profit margins, and impact the company's profitability.

At the critical juncture when Duan Yongping stepped in to invest in Pop Mart, market sentiment towards this trendy toy company was experiencing significant fluctuations.

According to iFinD data, as of the end of the first half of 2025, 288 funds held shares of Pop Mart, with a total market value of approximately 15.74 billion yuan.

However, as of the end of the third quarter and fourth quarter of last year, the number of funds holding Pop Mart dropped to 180 and 123 respectively, with the total market value of shares held dropping to approximately 11.29 billion yuan and 6.37 billion yuan.

On March 24, a research report released by Morgan Stanley pointed out that due to highly divergent market views, Pop Mart's stock price is expected to remain volatile after the earnings release, before entering a new round of range-bound fluctuations.

On March 25, the day of the release of the 2025 financial report, Pop Mart's stock price suffered a heavy blow, plummeting 22.51%. The next day, the company’s share price continued to fall, dropping another 10.46%, resulting in a cumulative decline of over 30% in just two trading days.

As of the close on April 16, Pop Mart was trading at HKD 164.8 per share, with its stock price having fallen by more than half from the high of HKD 339.8 per share (adjusted) reached last year.

The main reason for this sharp drop in Pop Mart may be a significant downward revision in the company’s growth expectations.

At the 2025 annual earnings conference, Pop Mart's Chairman of the Board and CEO Wang Ning stated: 'In 2026, we will strive to achieve a growth rate of no less than 20%.' This guidance represents a substantial retreat from the revenue growth rate of 184.71% recorded in 2025.

In response to stock price volatility, Pop Mart took swift action. Data from iFinD shows that between March 26 and April 2, Pop Mart conducted six share buybacks, totaling approximately 1.4 billion Hong Kong dollars.

A research report from Bocom International noted that the market previously assigned Pop Mart a PE ratio of over 40 times, based on the pricing of a growth stock with over 50% growth; when growth slows to the 20% range, valuations must shift to mature IP company standards, making a decline in valuation inevitable.

A research report from Zhongtai Securities suggested that due to the high uncertainty of hit IPs, simply 'adding more' is unlikely to result in higher valuations.

However, Duan Yongping stated, 'I no longer need to think about whether this business model can work or not, and I’ve also figured out the issue of sustainability. Of course, there will always be ups and downs in the process of growth. I will gradually, or perhaps not so gradually, accumulate the shares I want, unless I change my mind.'

But Duan Yongping also emphasized, 'The debate over sustainability will continue for a long time, so they may need to keep proving themselves (though they don't actually need to prove anything; they just need to keep doing what they are supposed to do). Everyone can wait and see for five or ten years.'

Some analysts believe that Duan Yongping's countercyclical investment in Pop Mart essentially reflects a value-driven contrarian response to the market’s 'excessive short-term emotional reaction.' He is betting on Pop Mart’s long-term core competitive advantages and eventual return to intrinsic value.

Whether the 'investment legend' written by Duan Yongping can be extended to Pop Mart remains to be seen. Radar Finance will continue to monitor the situation.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

1