A 15-fold surge in one year! How long can the new A-share stock king last?

![On April 17, Yuanjie Technology rose another 10%, closing at 1445 yuan, officially surpassing Kweichow Maotai to become the new A-share stock king. Its share price surged 1472% within a year, which is extremely rare even in global stock markets. After 2015, the 'Maotai curse' was summarized by the market - every company whose stock price exceeded that of Maotai would suffer misfortune. So, as the new challenger, can Yuanjie Technology break this 'curse'? [The Mystery of the 15-Fold Surge] Over the past year, Yuanjie Technology has surged nearly 15 times, ranking second on the A-share gainers list (only behind Shangwei New Materials), thanks to a significant improvement in performance. In 2025, the company’s revenue reached 600 million yuan, a year-on-year increase of 138.5%, with net profit attributable to shareholders reaching 191 million yuan, reversing losses into profits and recording the largest annual profit in its history. Breaking it down, the traditional telecom market business shipped 2.5G, 10G and other mid-to-low speed optical chips, but growth had stagnated over the past few years. In 2025, revenue only reached 206 million yuan, declining by more than 30 million yuan from its peak in 2022. The reasons include the global 5G construction entering a stable phase, slower capital expenditure by operators, combined with high localization rates and fierce market competition, causing gross margins to fall from 60% to around 30%. Another key segment is data communication business. The company, relying on products like CW silicon photonic light sources and other optical chips, seized the market dividend from the AI computing power explosion. Revenue contribution has risen to over 65%, making it the backbone of the business and a new growth engine. This segment boasts a gross margin of over 70%, boosting the company’s overall profitability...](https://nnqimage.futunn.com/sns_client_feed/18891453/20260417/web-1776419988498-3zhLkwKLT0.jpeg/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

On April 17, Yuanjie Technology rose another 10%, closing at 1445 yuan, officially surpassing Kweichow Maotai to become the new A-share stock king. Its share price surged 1472% within a year, which is extremely rare even in global stock markets.

After 2015, the market summarized the 'Maotai Curse' — every company whose stock price surpasses Maotai will face misfortune. So, as a new challenger, can Yuanjie Technology break this 'curse'?

▲Source: LatePost Data

[The Mystery of the 15-Fold Surge]

Over the past year, Yuanjie Technology surged nearly 15 times, ranking second on the A-share gainers list (only behind Shangwei New Materials), thanks to significant improvement in performance.

In 2025, the company’s revenue reached 600 million yuan, a year-on-year increase of 138.5%, with net profit attributable to shareholders reaching 191 million yuan, reversing losses into profits and recording the largest annual profit in its history.

▲Source: Wind

Breaking it down, the traditional telecom market business shipped 2.5G, 10G and other mid-to-low speed optical chips, but growth had stagnated over the past few years. In 2025, revenue only reached 206 million yuan, declining by more than 30 million yuan from its peak in 2022. The reasons include the global 5G construction entering a stable phase, slower capital expenditure by operators, combined with high localization rates and fierce market competition, causing gross margins to fall from 60% to around 30%.

The other segment is the data communication business, where the company, relying on optical chip products like CW silicon photonics light sources, seized the market dividend from the AI computing power explosion. Revenue contribution rose to over 65%, making it the backbone of the business and a new engine for growth. This business boasts a gross margin of over 70%, significantly boosting the company's overall profitability to near 2022 levels.

In addition, the valuation premium brought by abundant liquidity is also a core reason for the stock price surge.

Over the past year, the overall A-share market has been on an upward trend, with valuations of leading tech stocks in the AI supply chain rising significantly. The most typical example is 'Yi Zhongtian,' which saw its maximum increase reach between 860% and 1190%. Even 'contract manufacturers' like Foxconn Industrial Internet, with weak profitability, soared about 400% during this period, briefly surpassing the market value of its parent company, Hon Hai Precision, by more than 50%.

The same is true for overseas markets. Excessive dollar liquidity drove optical chip companies like Lumentum to soar 17-fold, with the latest valuation reaching 250 times earnings.

The broader A-share market rallied, investors flocked to AI-related stocks, and operating performance improved.—Under favorable circumstances in terms of timing, location, and people, it is no surprise that Yuanjie Technology, as a relatively scarce leader in the optical chip market, created a 'tenfold investment miracle' within just one year of its emergence.

[Another AI Enabler]

Computing power represents a vast industrial chain, with the upstream comprising 'hardware cornerstones' such as core chips, servers, and components.

Among these, optical modules are responsible for photoelectric signal conversion, akin to building an information 'highway' network that allows tens of thousands of GPUs to work together. Their performance parameters directly constrain the efficiency and scale of the entire computing power system.

Further breaking down the optical module sector, upstream are optical chips, which handle signal transmission or reception, with companies like Yuanjie Technology as key players. Midstream are optical components, whose main functions include assembly testing, filtering, coupling, and modulation, with companies such as TFC Communications being representative. Downstream are integration and terminal shipment, represented by companies like InnoLight Technology and NeoPhotonics.

It can be said that the greater the demand for computing power, such as large model training, the larger the shipment volume of optical modules, and the higher the prosperity level of optical chips will be.

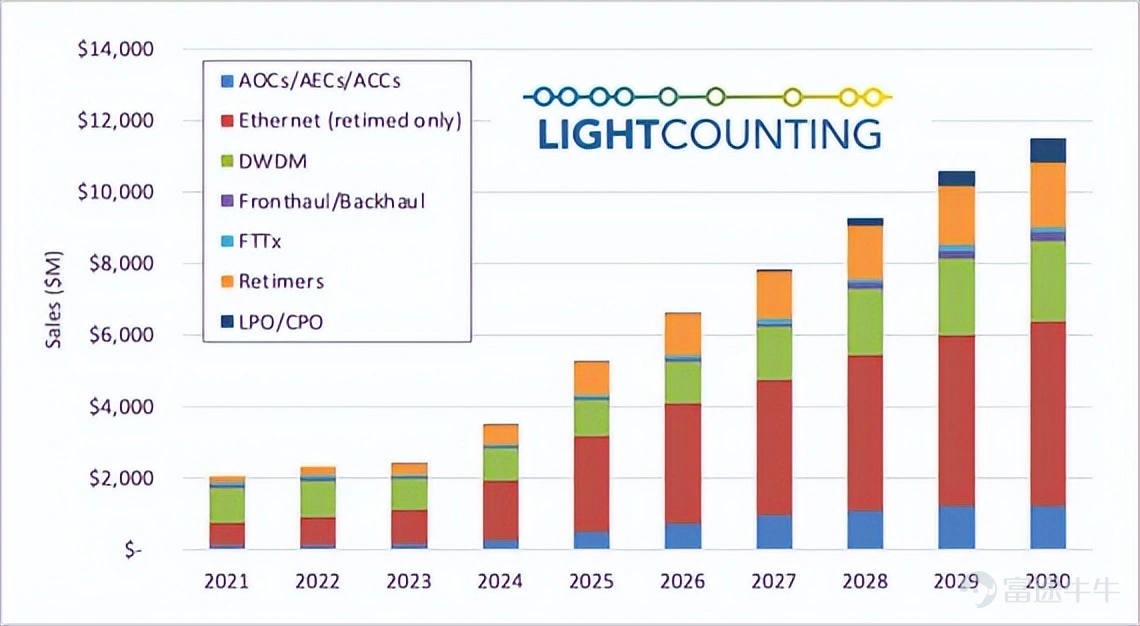

According to LightCounting data, the global optical chip market size in 2024 is $3.5 billion, expected to reach $11 billion by 2030, with an annual compound growth rate as high as 17%. According to China Business Industry Research Institute, the domestic market size has exceeded 15 billion yuan in 2024, compared to just 9.35 billion yuan in 2020.

▲Global optical chip market size, source: LightCounting

In the future, the expansion of the optical chip market will be driven mainly by two major growth factors.

The first is the increase in the number of optical chips brought about by the explosive growth of AI computing power. In recent years, capital expenditures of downstream cloud computing vendors have been continuously rising. The combined capital expenditure of Microsoft, Google, Amazon, and Meta in the fiscal year 2025 is projected to reach $350 billion, a year-on-year increase of approximately 60%, aiding in the expansion of AI data centers, and also boosting the shipment volume of optical chips.

Moreover, the evolution of optical module rates has progressed from 100G, 400G, to the current mainstream 800G in AI clusters, and now moving toward 1.6T. Higher rate requirements lead to a greater number and higher value of optical chips required for each optical module.

The second factor is the generational upgrade of optical chips themselves, transitioning from single-channel rates of 25G to 100G and 200G.

Higher rates impose more stringent demands on chip material design, process technology, and packaging testing, raising operational barriers. A high-end optical chip with a rate of 100G or above commands significantly higher prices and profit margins compared to traditional 10G and 25G chips.

From a global perspective, in mid-to-low-end markets such as 2.5G and below, 10G, and 25G, domestically produced optical chips have achieved a monopolistic position globally, with shares exceeding 90%, 80%, and 60%, respectively. In contrast, the higher-end market has long been dominated by US and Japanese giants, including Lumentum, Broadcom, Sumitomo Electric, and Mitsubishi Electric. These giants accounted for over 95% of the global market share in 2020.

In recent years, domestic optical module companies have begun to emerge and rise.Companies such as InnoLight Technology, NeoPhotonics, Huawei, Accelink Technologies, Hisense Broadband, HG Genuine, and Source Photonics have entered LightCounting's 2024 list of the top ten global optical module companies. In contrast, back in 2018, only three Chinese companies were among the top ten global players.

The global optical communications industry chain is showing a major trend of shifting towards China. Domestic optical chip manufacturers are expected to benefit from this process of domestic substitution. As a leading domestic optical chip company, Source Photonics has formed deep partnerships with mainstream domestic optical module enterprises like InnoLight Technology and NeoPhotonics, and has also obtained certification from NVIDIA’s supply chain.

Clearly, Source Photonics stands at the forefront of transformative changes in the AI era, benefiting from the explosive growth in the computing power supply chain while also capitalizing on the broader trend of 'domestic substitution.' It has become one of the core AI leaders pursued in the A-share market, seemingly predestined to do so.

[Beware of the Music Stopping?]

Under such strong investor抱团 (group support), the capital market has given Source Photonics a very high valuation premium.

As of April 17, Yuanjie Technology's latest PE ratio was 650 times, far higher than the optical chip index at 156 times and the artificial intelligence index at 73 times. Meanwhile, other AI giants favored by the market—Xinyi Sheng, Zhongji Xuchuang, and Tianfu Communications—are valued at 78 times, 63 times, and 146 times, respectively.

The significant valuation premium given to Source Photonics compared to its industry or competitors implicitly reflects the market's expectation that the company will sustain high earnings growth amid an explosion in AI-driven computing demand. However, this optimistic assumption may face considerable challenges.

Currently, the demand for large model training and inference continues to expand among global tech giants.But how long the high capital expenditure can be sustained depends on whether these players can successfully achieve commercial monetization.

▲ Changes in capital expenditures by tech giants, Source: Pacific

Currently, AI application implementation is still in the exploration phase, and no large-scale profitable scenarios have emerged. Although general tools like ChatGPT are widely used in text-based office work, enterprise-level AI applications face difficulties, with penetration rates in key industries such as consumer retail and manufacturing almost at zero.

This has also led to AI giants like OpenAI facing a 'bottomless pit' on the cost side - due to the extremely high proportion of free users (95%), and every AI inference having a cost, the company essentially uses revenue from a small number of paying users to subsidize usage by the vast majority of free users. The more users there are, the scale effect does not bring down costs; instead, losses expand simultaneously.

Thus, OpenAI's long-term infrastructure investment commitment, initially claimed to be $1.4 trillion, was slashed to $600 billion within just a few months. This figure may still be overly ambitious, and further substantial cuts cannot be ruled out in the future. Moreover, OpenAI recently shut down Sora, an application previously hailed by the market as another revolution.

These signs indicate that AI commercialization is not as easy and rapid as market expectations suggest, and it will become one of the core factors constraining the high capital expenditures of technology giants in the future.

In addition, the expansion of computing power infrastructure by tech giants has heavily relied on bond financing and bank loans in recent years, with extremely low interest rates being a basic condition.

Today, amid fluctuating geopolitical tensions, Brent crude oil remains close to $100 per barrel, rebounding more than 50% from its recent low. The impact on US inflation will gradually manifest in April and May, making planned interest rate cuts increasingly unlikely and potentially raising the possibility of rate hikes instead. Such changes in the interest rate environment could add new uncertainties to high capital expenditures.

In fact, around early 2026, several major US banks stopped lending to tech giants like Oracle, and investment banks downgraded their debt ratings, questioning whether AI-related capital expenditures had exceeded the support range of free cash flow. Additionally, the price of the company’s five-year credit default swaps (CDS) surged significantly, sharply increasing the risk of bond defaults.

Oracle’s situation is not an isolated case, reflecting growing concerns from banks and the capital market about the aggressive AI investments by tech giants.

This shows that the future of AI computing power experiencing sustained rapid growth is facing certain vulnerabilities. Once expectations change, the foundation for SourceTech's continued high growth may also face reevaluation.

In addition, potential shifts in market style and tightening liquidity could also put pressure on the valuation of global AI leaders.

In the A-share market, valuations of major asset categories such as technology, cyclical, and finance have undergone a trend of continuous increase over two years, with overall levels at a relatively high position compared to previous years. Meanwhile, major asset categories like consumption and dividend are at relatively low levels in recent years. Looking ahead, the dominant market style might shift from growth to value.

Moreover, the liquidity of overseas currencies is likely to evolve towards a marginally tighter direction, which is not favorable for leading AI companies that have significantly benefited from previous loose liquidity. Once the overall valuation center of global AI shifts downward, Yuanjie Technology may also struggle to remain unscathed.

In summary, the surge in Yuanjie Technology's stock price is the result of both high performance growth driven by the AI wave and the loose liquidity environment. However, a valuation of 650 times may already reflect several years of sustained high prosperity in advance. The sustainability of high capital expenditure by downstream giants and the potential shift in macro liquidity are variables that loom overhead.

Breaking the 'Maotai curse' ultimately requires consistent high growth to resolve. $Yuanjie Semiconductor Technology (688498.SH)$$Kweichow Moutai (600519.SH)$

By Little Flying Dagger

Disclaimer

This article contains content related to listed companies, reflecting the author's personal analysis and judgment based on information disclosed by these companies in accordance with their legal obligations (including but not limited to interim announcements, annual reports, and official interactive platforms). The information or opinions presented in this article do not constitute any form of investment or other business advice. Market Value Observer assumes no responsibility for any actions taken as a result of adopting the content of this article.

——END——

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comment (1)

to post a comment

3