Bank of Tianjin reports mixed earnings: total assets nearing one trillion, non-performing loan ratio at a record high

In April 2026, coinciding with the tenth anniversary of its listing, Bank of Tianjin delivered a mixed 'report card' for 2025.

Total assets are approaching the trillion-dollar mark, with revenue and net profit achieving 'double growth' for three consecutive years, and net interest margin rebounding against the trend. However, alongside the growth in asset scale, the non-performing loan rate for personal loans has hit a new high since the bank's listing, showing significant structural differentiation in asset quality. For this long-established city commercial bank rooted in Tianjin for 40 years, how to properly address potential risks while moving towards the 'trillion club' has become a pressing real-world challenge.

The trillion-dollar target is within reach, cost reduction and efficiency improvement sustain growth

In 2025, Tianjin Bank’s most notable performance lies in its steady expansion of scale.

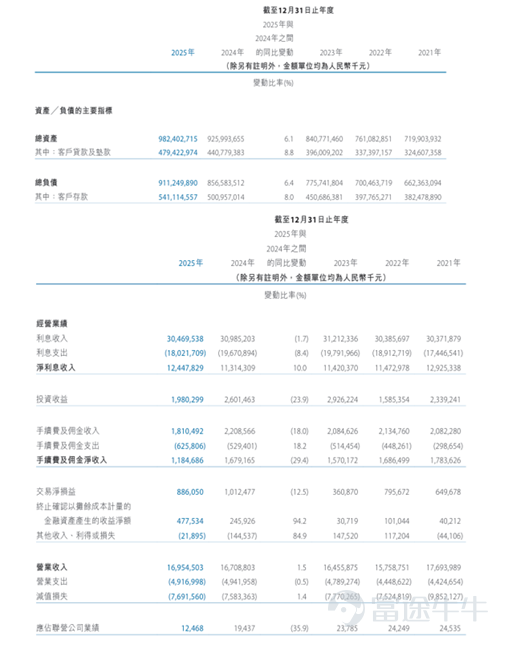

Annual report data shows that as of the end of 2025, Tianjin Bank's total assets reached 982.403 billion yuan, an increase of 6.1% from the beginning of the year. It is only one step away from joining the trillion-dollar asset club.

In terms of performance, the bank achieved annual operating income of 16.955 billion yuan, a year-on-year increase of 1.5%; net profit attributable to shareholders was 3.866 billion yuan, a year-on-year increase of 1.7%. Although the absolute value of growth is not particularly impressive in the banking industry, maintaining positive growth for three consecutive years under the current backdrop of narrowing interest margins is no small feat. Additionally, the capital market also responded positively, with the stock price rising cumulatively by 36.8% for the whole year.

However, breaking down the revenue structure reveals that Tianjin Bank’s growth in 2025 features 'obstructed revenue sources but effective cost-cutting.'

On one hand, non-interest income suffered a 'debacle.' Affected by a decline in investment scale and market volatility, the bank’s annual investment income was 1.98 billion yuan, a year-on-year decrease of 23.9%; fee and commission net income plummeted by 29.4% to 1.185 billion yuan, mainly due to the contraction of agency commissions and underwriting fees.

On the other hand, net interest income supported the entire year's profits. Financial reports show that in 2025, the bank's net interest income was 12.448 billion yuan, a year-on-year increase of 10%, which is particularly remarkable in an environment where yields on interest-earning assets generally declined. This also benefited from the bank’s liability cost control. The annual report disclosed that through full efforts in advancing the 'cost battle' and 'deposit battle,' the average interest rate on interest-bearing liabilities decreased by 35 basis points year-on-year to 2.13%. Annual interest expenses decreased by 1.65 billion yuan year-on-year, a drop of 8.4%, effectively offsetting the pressure of a 1.7% slight decline in interest income. Furthermore, the total remuneration of key management personnel was cut by nearly 3.47 million yuan, reflecting the bank’s firm determination to reduce costs and increase efficiency.

Structural Differentiation: Corporate Expansion Accelerates, Retail Loan Risks Highlighted

If fluctuations at the revenue level are still considered normal, structural risks on the asset side deserve more attention. In 2025, Tianjin Bank’s credit business showed a striking 'two extremes' situation.

Corporate banking operations are expanding rapidly. Backed by the coordinated development of the Beijing-Tianjin-Hebei region and Tianjin's 'Ten Actions' plan, Tianjin Bank's corporate loans reached 391.603 billion yuan, marking a year-on-year growth of 17.2%. Among this, loans to leasing and business services amounted to 160.3 billion yuan, up 31% year-on-year, becoming the main driving force behind the scale expansion.

In stark contrast is the retail business. By the end of the year, the balance of personal loans stood at 80.015 billion yuan, down 17.8% year-on-year. More concerning is the asset quality: the balance of non-performing personal loans surged to 3.71 billion yuan, with the non-performing rate soaring to 4.64%, hitting an all-time high since the bank went public.

The reasons for this are twofold: on one hand, the macroeconomic environment has led to a decline in the debt repayment ability of some clients; on the other hand, it is the result of the bank's proactive efforts to address past issues. The repercussions from its earlier rapid expansion through internet-assisted lending are still being worked through, and in 2025, the bank continued to reduce the scale of internet partnership loans, causing personal business loans and consumer loans to drop significantly by 24.1% and 14.7%, respectively.

Asset Quality: High Levels of Overdue Loans

Although Tianjin Bank managed to keep its overall non-performing loan ratio at 1.7% as of the end of 2025, unchanged from the end of the previous year, certain structural issues deserve attention.

First, there is a dual increase in the volume and amount of non-performing loans. As of the end of 2025, Tianjin Bank's total non-performing loans exceeded 8 billion yuan, reaching 8.276 billion yuan, an increase of 667 million yuan from the beginning of the year.

Secondly, loan classifications have shown a clear downward migration. As of the end of 2025, the bank's special-mention loans totaled 17.15 billion yuan, an increase of 1.98 billion yuan from the end of the previous year, with the proportion of total loans rising to 3.47%. Additionally, loss category loans within non-performing loans surged from 1.736 billion yuan at the end of 2024 to 5.202 billion yuan, representing an increase of 199.69%, indicating that a significant portion of loans have transitioned from 'potential losses' to 'confirmed losses,' posing a direct challenge to the bank’s provision coverage capacity.

Moreover, the issue of overdue loans remains a focus of market attention. As of the end of 2025, the balance of loans overdue for more than 90 days was still higher than the balance of non-performing loans, reflecting that risk identification and classification in earlier periods remain insufficiently prudent.

"Not competing on scale but on quality"—this is the strategic determination repeatedly emphasized by Tianjin Bank Chairman Yu Jianzhong in the annual report message.

In 2025, Tianjin Bank delivered a performance report with assets approaching one trillion yuan and a modest profit increase, demonstrating its control capabilities in corporate banking and liability management. However, the personal loan non-performing rate of 4.64% and the growing level of non-performing loans serve as a warning signal for potential risks.

For Tianjin Bank, which is about to cross the trillion-yuan threshold, the real challenge may just be beginning: how to fully resolve the historical baggage of internet loans and how to rebuild its risk control system while scaling back its retail loan portfolio.

(Article Serial Number: 2044700351411654656/JW)

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment