Star Health Insurer on the IPO Fast Track: Annual Revenue Exceeds 1 Billion, Sequoia Bets Big!

(This article was authored by Medical Insight, and Titanium Media has been authorized to publish it)

By Medical Frontline Insight, Author: Zhang Xiaoman

After eight years of establishment, the health insurance star company has initiated its IPO push at the Hong Kong Stock Exchange.

On April 13, Nuwa Insight Technology Co., Ltd. (referred to as 'Nuwa Technology') officially submitted its prospectus, with JPMorgan and HSBC serving as joint sponsors.

In the prospectus, Nuwa Technology showcased an impressive track record.

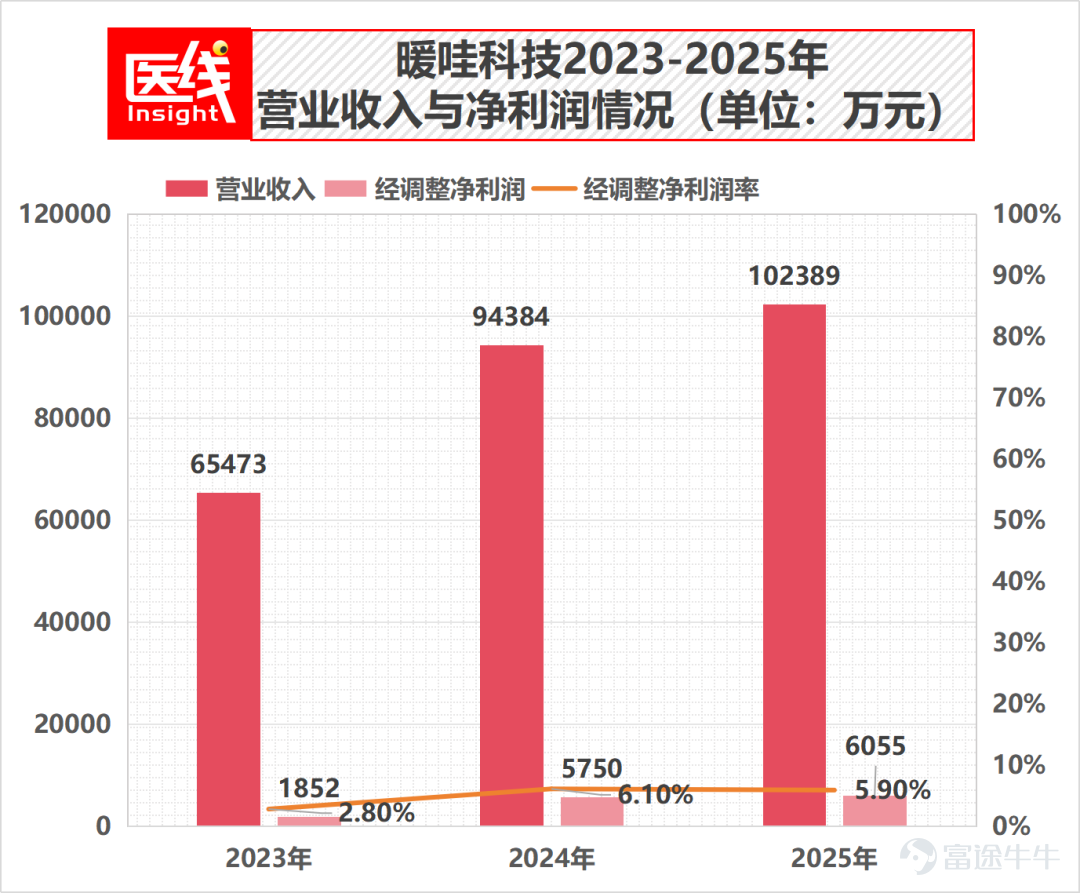

RevenueIn terms of revenue, total revenue for 2025 reached10.239billion RMB, with a compound annual growth rate of 25.1% from 2023 to 2025.

profitabilityIn terms of non-IFRS measures, excluding non-cash items such as changes in the fair value of preferred shares, NuonTech achieved adjusted net profits of 18.51 million yuan, 57.5 million yuan, and 60.55 million yuan for 2023, 2024, and 2025 respectively, demonstrating the viability of its AI business model.This has enabled sustainable self-generated revenue.

Data source: NuonTech prospectus

industry penetration rateAs of December 31, 2025, NuonTech'sAI solutions have been adopted by a cumulative total of 115 insurance companies nationwide.Based on premium scale in 2025, nine out of the top ten insurance companies in China are key collaborative clients of NuonTech.

According to Frost & Sullivan, in terms of the number of insurance claims processed in 2024,NuonTech is the largest independent AI-driven technology company in China's insurance industry.

More critically, it is the first and only AI-driven technology company in China’s health insurance sector with 'full-stack risk analysis capabilities,' offering services throughout the entire lifecycle of insurance transactions from product design, underwriting risk control, claims management, to policy servicing.

Image source: NuonTech prospectus

How did Nuonova Technology achieve its current success step by step? What are the market opportunities and challenges for its core business model? The following article will provide a detailed analysis.

The birth of every star company is the result of deep resonance between era dividends, top-level strategy, and industrial capital.

Looking back at Nuonova Technology's entrepreneurial journey, it is a typical case of 'internal incubation by an industry giant + independent team operations + strategic acquisitions to address weaknesses' in corporate evolution.

Let’s go back to October 2018. At that time, China’s health insurance market was on the verge of explosive growth, but underlying pain points in the industry were becoming increasingly prominent.

Specifically, in the niche track of health insurance, insurers have long been trapped in the 'impossible triangle' of 'large premium scale, extremely high claims ratio, and razor-thin or even negative profit margins.'

Faced with massive, fragmented, and unstructured medical data, traditional underwriting and claims models relying on manual labor and static rules proved inadequate. Manual claims review typically takes 3 to 7 days, which is inefficient and highly prone to fraud and incorrect payouts.

Against this industry backdrop, Nuonova Wuxi (the main operational entity of Nuonova Technology in China) officially launched in Shanghai and quickly carved out a niche in the insurtech field.

This achievement would not have been possible without the deep industry background of its core management team.

First,Founder, Chairman and CEO Lu Min has over 20 years of hands-on experience in the insurtech industry. Prior to founding Nuonova, he held key positions at Alibaba (China) Network Technology Co., Ltd. and multinational insurance software provider EbaoTech Corporation (Shanghai), as well as serving as General Manager of the Executive Committee Member and InsurTech Business Unit at the Shanghai Insurance Exchange.

These experiences have given him a keen sense for core insurance systems, business expansion, and digital platform innovation.

Nuonova's Co-CEO Cai Jianweialso has over 20 years of experience in insurtech and TMT, having worked at Ant Financial responsible for local wallet and platform products, and also overseeing e-commerce operations at AIA.

In addition,Chief Marketing Officer Shen Helingled insurance digital transformation initiatives at SAP and Deloitte;Chief Data Officer Chen Honghas more than 15 years of experience in AI and data science and was previously a senior algorithm expert at Ant Fortune;Finance and Operations Head Yang JianyingAlso has a background in investment and financing as well as strategic consulting.

Source: Nuova Technology's IPO prospectus and official website

An executive team that brings together cross-disciplinary experience from 'actuarial insurance + cutting-edge technology + leading internet companies' allows the company to quickly gain momentum.

At the same time, being spun off from a giant often means potentially being constrained by that giant.

To ensure Nuova’s neutrality as an independent technology company so it can provide services to other large insurance companies in the market,Lu Min and ZhongAn Online initially maintained a delicate balance,with both parties holding equal ultimate voting rights.

As of before the IPO, Lu Min and ZhongAn Online each held 31.65% of the company’s shares. This structure, which combines 'backing by a giant while maintaining independence,' laid an important foundation of trust for Nuova to subsequently secure nine of the top ten insurance companies in China.

With industrial DNA and a proven business model, Nuova registered an offshore holding company in the Cayman Islands in March 2019, officially beginning its rapid expansion in the private market.

In July 2019, Sequoia China partnered with ZhongAn to complete the angel round, raising 100 million yuan at a cost of 0.32 US dollars per share. Sequoia’s significant investment not only brought capital but also served as a crucial endorsement for Nuova’s AI-powered health insurance track.

Six months later, Longfor Group led the Series A round, Sequoia increased its investment, raising 16 million US dollars with the per-share cost rising to 0.52 US dollars.

From 2021 to 2024, institutions such as Lenovo joined, and the Series A+ round raised 29 million US dollars, doubling the per-share cost to 1.08 US dollars. Afterward, Woori Financial Group also made a significant entry in January 2025 by acquiring existing shares.

From September 2024 to November 2025, Liangxi Sci-Tech, backed by Wuxi local state-owned capital, led the Series B round, with existing shareholder ZhongAn following up on the investment, pushing the per-share cost to 2.18 US dollars.

Looking at its financing history, every step has been quite solid, outlining a steep valuation growth curve: in just a few years, the capital market's valuation of Nuonova surged nearly sevenfold.

Data source: Nuonova Technology prospectus

Of course, relying solely on primary market funding does not make a company an industry star.

The key to Nuonova Technology’s advancement lies in its deep understanding of the compliance requirements and offline characteristics of the insurance industry.

To this end, itThrough a series of strategic acquisitions, it transformed from a single software service provider into a full-stack platform encompassing 'online + offline' and 'marketing + appraisal'.

In January 2020, it acquired 'Aibang' and 'Yadun', securing core compliance licenses, enabling it to legally and compliantly intervene directly in user operations, distribution conversion, and offline claims verification processes for insurers.

In October 2023, the acquisition of 'Jiangsu Daotai,' a company specializing in user operations via AI voice outbound calls and SMS services, completed its front-end customer acquisition and conversion capabilities.

In September 2025, the acquisition of 'Guangzhou Tianxin' integrated the company’s nationwide offline investigation service network, providing Nuwa with an offline execution tool for handling high-risk suspected fraud cases. This created a closed loop of 'online AI smart review + offline appraisal investigation.'

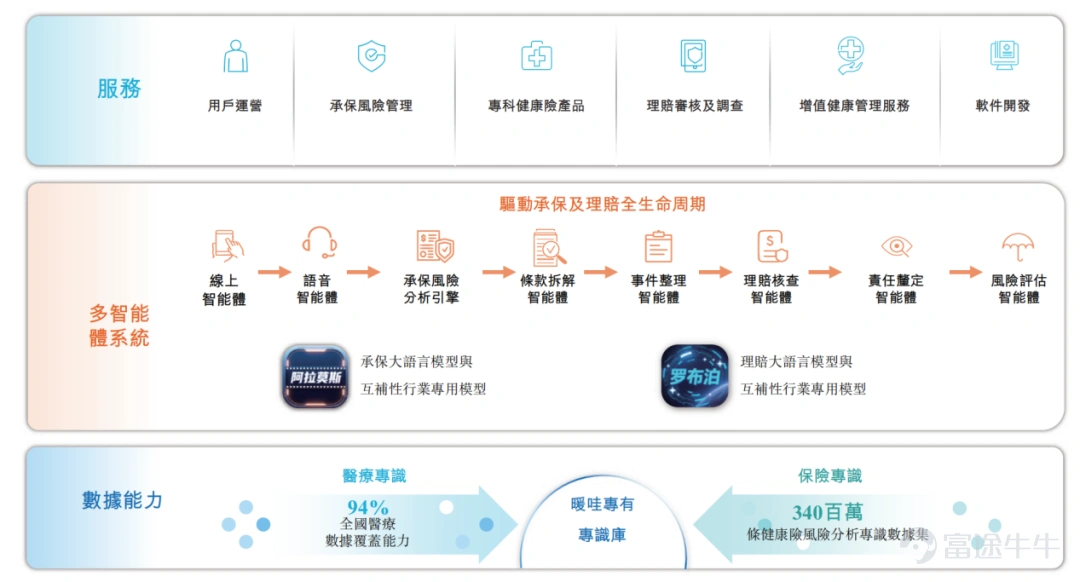

Nuwa Technology Core Technology Illustration

Image source: prospectus

From its startup in 2018, to launching underwriting solutions in 2019, to rolling out a multi-agent AI system in 2024, complemented by precise M&A strategies, Nuwa has gradually assembled a full-chain landscape from front-end customer acquisition marketing, mid-tier underwriting risk control, to back-end claims review and offline appraisal investigations, firmly securing its place among China's top health insurance companies.

Under the spotlight of the capital markets, no matter how compelling the technology story is, it ultimately comes down to whether the company can generate real profits.

By breaking down Nuwa Technology’s financial data, we see a company in a rapid growth phase, with a proven business model and self-sustaining capabilities, but also undergoing cost restructuring and growing pains while expanding its scale.

According to the prospectus, its total revenue in 2023, 2024, and 2025 was 654.7 million yuan, 943.8 million yuan, and 1.0239 billion yuan, respectively.

Within just three years, revenue successfully surpassed the one-billion-yuan mark, achieving a compound annual growth rate of 25.1% between 2023 and 2025.

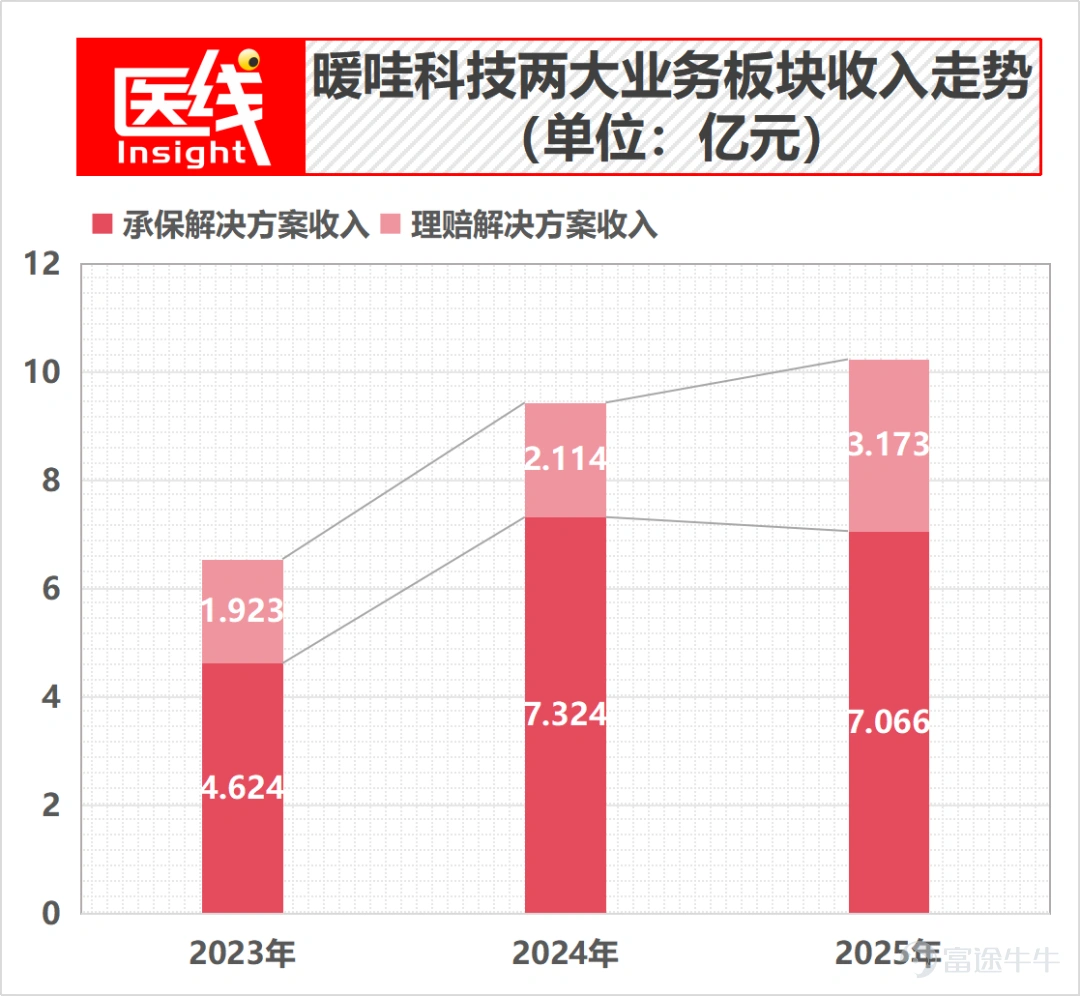

To break it down further, this billion-dollar revenue is mainly driven by two major business engines.

The first engine: Underwriting solutions.

This segment is the backbone of NuWa, contributing 462.4 million yuan, 732.4 million yuan, and 706.6 million yuan in 2023, 2024, and 2025 respectively, accounting for 70.6%, 77.6%, and 69.0% of total revenue.

Among these, 'User Operations' is the strongest monetization node, leveraging AI voice and online intelligent agents to help insurers with precision marketing, cross-selling, and renewals.

In 2024, thanks to the acquisition and consolidation of Jiangsu Daotai, user operations revenue increased from 209.9 million yuan in 2023 to 483.6 million yuan.

Additionally, 'Underwriting Risk Management,' included within the underwriting segment, also saw steady growth, reaching 235.4 million yuan in 2025.

The second engine: Claims solutions.

This segment has shown promising late-stage potential, with revenue growing from 192.3 million yuan in 2023 to 317.3 million yuan in 2025.

Data source: NuWa Technology's prospectus

Among the services, the "claims review and investigation" business contributed 218.7 million yuan in 2025, a significant increase from 139.2 million yuan the previous year. This growth was mainly driven by upselling strategies and enhanced appraisal capabilities following the acquisition of Guangzhou Tianxin in September 2025.

In addition, Nuowah also launched "value-added health management services" by connecting pharmaceutical companies with medical institutions, such as physical exams, medical consultations, and expedited green channels for critical illnesses. Revenue surged from 12.69 million yuan in 2023 to 66.4 million yuan in 2025, becoming an important source of incremental income.

One noteworthy detail is that Nuowah's fee model is quite confident—"Pay-for-performance”。

For example, user operations charge a certain percentage of the first-year premium facilitated; underwriting risk management charges an additional variable fee of 20% to 50%, based on the decrease in insurers' claims ratios, on top of basic service fees. If the number of inaccurate claims cases exceeds the limit, Nuowah could even face penalties.

This model, deeply aligned with customer interests, directly demonstrates Nuowah's confidence in its AI risk control capabilities. It is also the core reason behind its ability to maintain an extremely high revenue retention rate (160.2% in 2023 and 134.0% in 2024).

Given the two main business engines driving continuous revenue growth, what about profitability?

According to the prospectus, Nuowah Technology's net losses for the periods ending 2023, 2024, and 2025 were 239.9 million yuan, 155.2 million yuan, and 269.8 million yuan, respectively.

On the balance sheet, as of the end of 2025, the company even recorded net debt of 1.108 billion yuan and net current liabilities of 1.175 billion yuan.

Does this mean that Nuwa is a company that 'burns money for scale' or 'goes public while bleeding capital'?

But that's not true.

The prospectus clearly states that the core reasons for the huge losses and insolvency are'losses from changes in the fair value of financial liabilities measured at fair value through profit or loss'.

In short, due to Nuwa issuing a large number of convertible redeemable preferred shares and convertible instruments to investors during its historical financing rounds, as Nuwa's valuation continued to rise during its IPO preparation period, the fair value of these liabilities also increased. Under International Financial Reporting Standards, this premium in valuation must be recorded as the company’s 'book loss'.

From 2023 to 2025, this non-cash loss reached as high as 256.7 million yuan, 205.5 million yuan, and 303.6 million yuan respectively.

This is a typical accounting phenomenon of a star company showing 'apparent losses but actual profits'.

Once the company completes its IPO, these preferred shares will automatically convert into common shares, reclassifying from liabilities to equity, and the substantial book loss will instantly vanish, restoring the company's net asset position to positive.

If we look beyond this facade and exclude factors such as changes in the fair value of financial liabilities, share-based payment expenses settled in equity (employee stock option incentives), and one-time non-cash items like listing expenses, Nuwa Technology's genuine business cash-generating ability is quite impressive.

Under non-International Financial Reporting Standards, Nuwa Technology's 'adjusted net profit' was 18.51 million yuan, 57.5 million yuan, and 60.55 million yuan in 2023, 2024, and 2025 respectively.

Its adjusted net profit margin also surged from 2.8% in 2023 to stabilize at 6.1% in 2024 and 5.9% in 2025.

More crucially, the cash flow data. As economies of scale became evident, the net cash generated from Nuonva's operating activities increased significantly from 4.64 million yuan in 2023 and 7.04 million yuan in 2024 to 51.72 million yuan in 2025.

By the end of 2025, the company had 247 million yuan in cash and cash equivalents on its books.

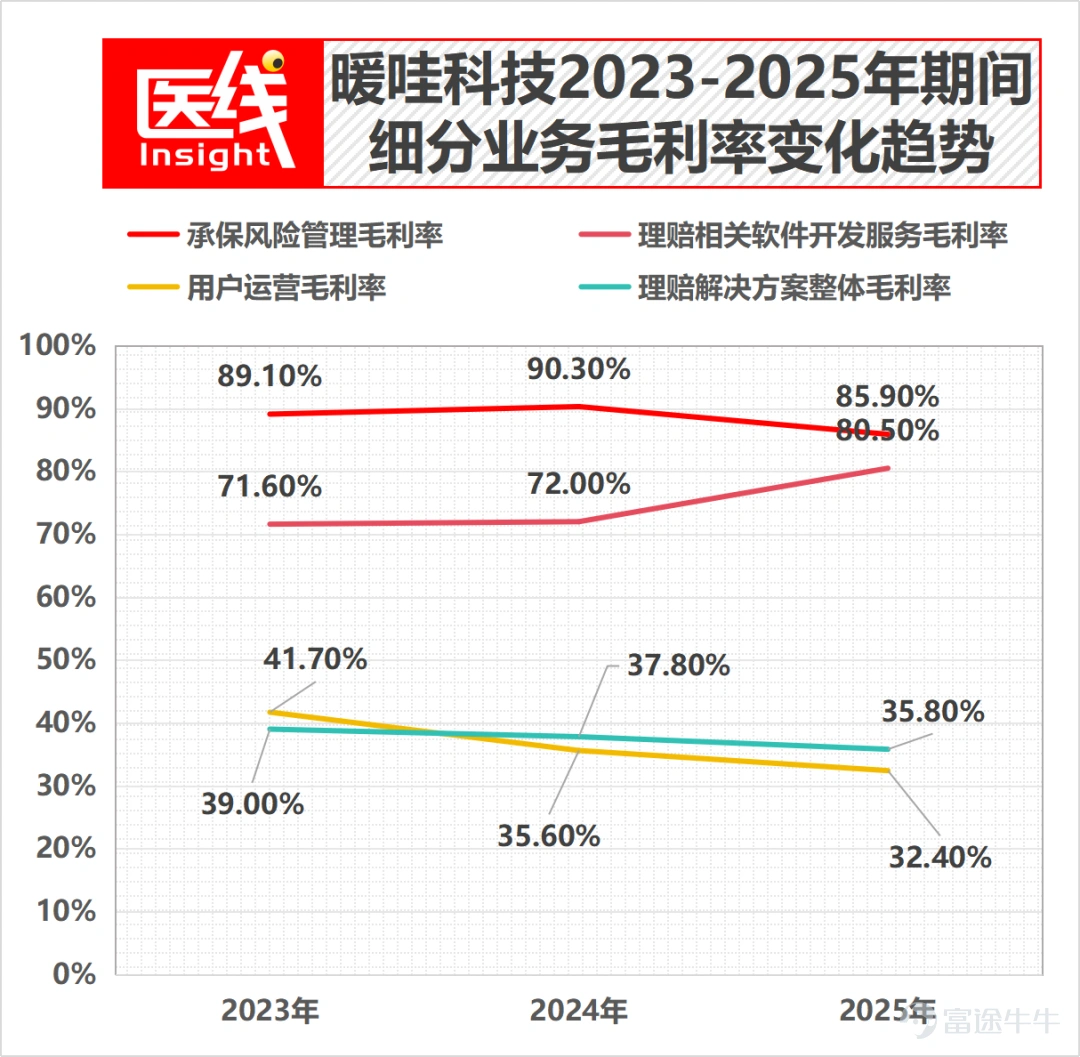

Despite the dual growth in revenue and adjusted net profit, Nuonva'sgross profit margin showed a clear structural decline during the reporting period: dropping from 58.3% in 2023 to 49.8% in 2024, and further to 47.2% in 2025.

The main culprit behind the continuous decline in gross margin was the acquisition of 'Jiangsu Daotai,' which boosted revenue but concealed high telecommunications costs.

The prospectus details show that Nuonva's cost of services skyrocketed from 273.1 million yuan in 2023 to 473.4 million yuan in 2024. Among this, 'telecommunications expenses' surged from 27.02 million yuan in 2023 to 203.9 million yuan in 2024, accounting for service costs rising from 9.9% to 43.1%.

This is because Jiangsu Daotai mainly relies on AI outbound calls and SMS services for user operations.

After consolidation, although it brought substantial revenue, its business model incurred heavy telecom channel fees. This directly caused the gross margin of Nuonva’s 'user operations' sub-business to fall from 41.7% in 2023 to 35.6% in 2024.

In other words, while Nuonva was expanding its revenue base, it bore heavier channel costs and suffered from cost backlash.

To make matters worse, in 2025, due to months-long telecom service capacity control implemented across the industry, Jiangsu Daotai's AI-driven outbound call efficiency was temporarily reduced, limiting service capacity.

This sudden policy disruption directly led to a drop in user operation revenue to 436.5 million yuan in 2025, with the segment’s gross margin further falling to 32.4%. This also served as a wake-up call for Nuonva:Over-reliance on a single telecom outbound channel for AI marketing exhibits significant vulnerability in the face of regulatory policies.

Additionally, the gross margin of claims solutions fell from 37.8% in 2024 to 35.8% in 2025. The main reason was that after consolidating Guangzhou Tianxin in September 2025, there were changes in the business mix of claims review and investigation services (increased offline labor and channel procurement costs), coupled with relatively lower gross margins for health management services.

Data source: Nuonva Technology prospectus

However, the pure technology-enabled business of 'underwriting risk management,' which represents Nuonva's core AI technology barrier, still maintains a high gross margin of 85.9% to 90.3%; the gross margin for 'claims-related software development services' is also as high as 80.5%.

After calculating all operations comprehensively, Nuonva Technology has managed to maintain a relatively high overall profit margin for the company.

Stepping back from the individual perspective of Nuwo Technology and situating ourselves at the intersection of China's health insurance and AI technology, we can truly gauge the industry significance of this star company, the real-world challenges it faces, and the future vision it seeks to outline.

China’s insurance market is the second-largest insurance market globally, with an overall premium scale reaching 5.7 trillion yuan in 2024.

However, at the same time,The insurance penetration rate in China is only 4.4%, far below the 12.5% seen in the United States.with per capita premium expenditure standing at just 578 US dollars.

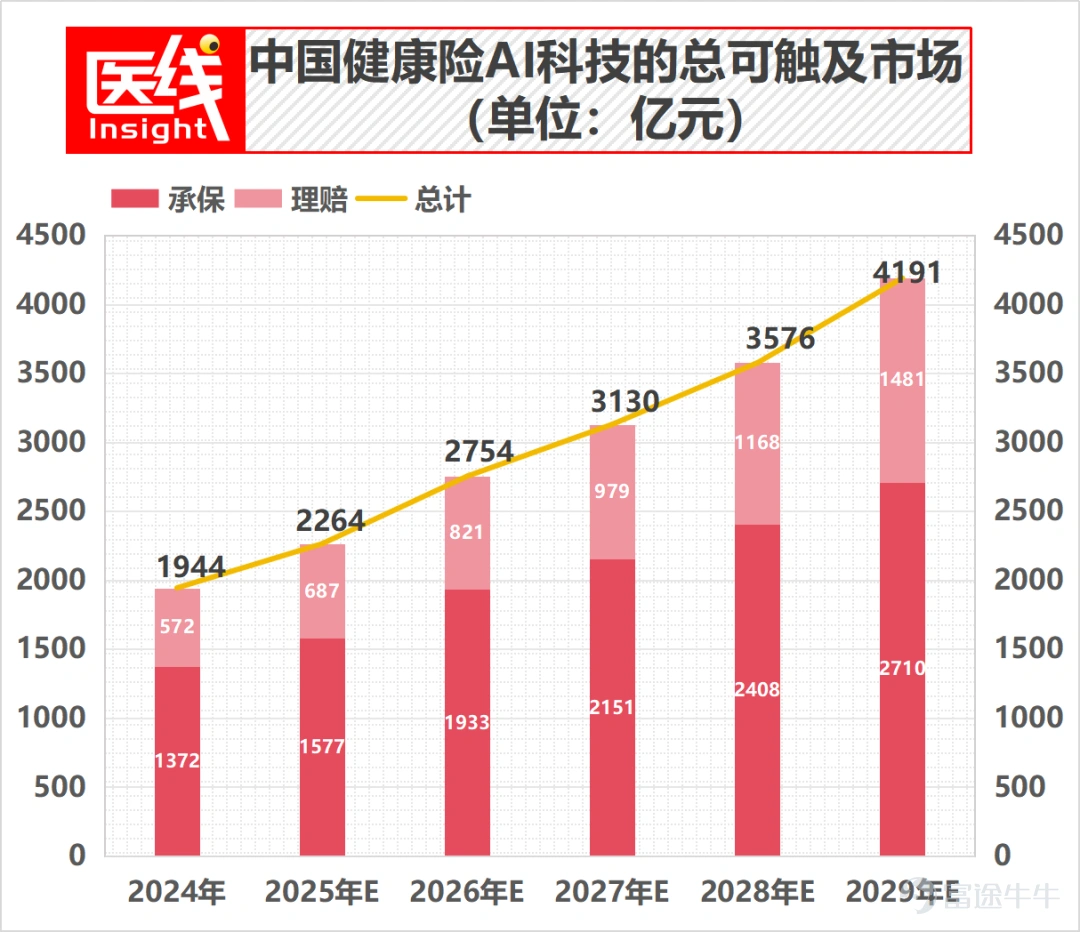

This is the 'vast ocean' that Nuwo Technology is targeting. According to a Frost & Sullivan report, the total addressable market size for AI technology in China’s health insurance sector is projected to grow from 194.4 billion yuan in 2024 to 419.1 billion yuan by 2029.

Source of data: Nuowa Technology's prospectus

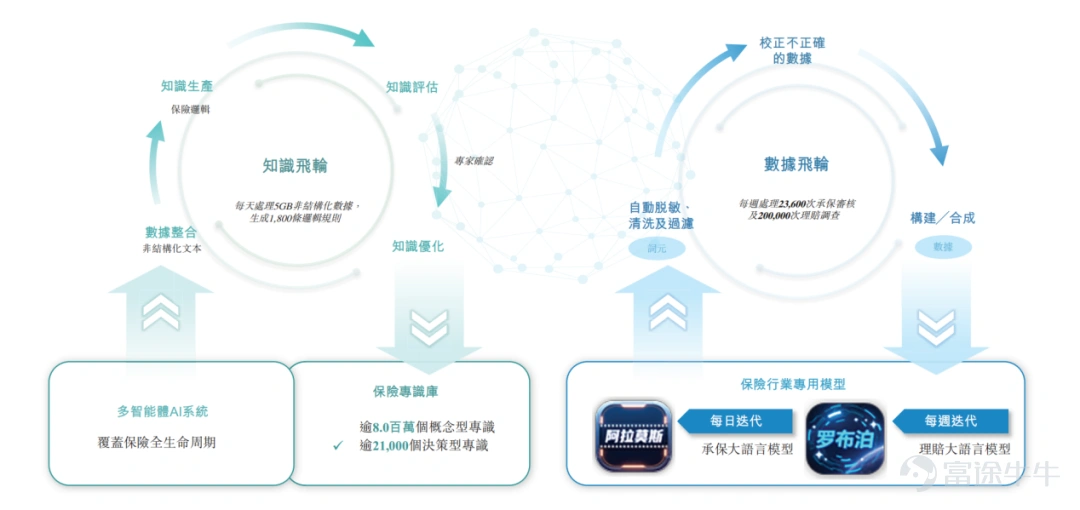

Within this billion-dollar incremental blue ocean, Nuwo has not simply adopted generic large models like many SaaS companies do for straightforward API calls; instead, it has pursued a unique approach characterized by‘Data + Expertise + Multi-Agent’.

The intelligence quotient of a large model depends on the data fed into it.Nuonova possesses one of the largest health insurance knowledge bases in China, with the capability to cover 94% of the nation's medical data, reaching more than 160,000 medical institutions across 32 provinces.

Meanwhile, the knowledge base has accumulated 340 million health insurance risk analysis data points, including over 8 million conceptual knowledge points (such as diseases, medicines, treatment plans, etc.) and more than 21,000 decision-making knowledge points (practical claims rules and standard operating procedures).

On top of this massive knowledge flywheel and data flywheel, Nuonovahas incubated two major multi-agent systems.

Image source: prospectus

One is called Alamos — the 'super brain' for underwriting.

This is a multi-agent system specifically designed for underwriting and user operations. It directly engages with customers through voice and online agents, analyzing emotions and purchase intent in real-time and dynamically generating personalized marketing scripts.

The prospectus mentions that in a case involving an internet insurance company, after deploying Alamos, its cross-selling rate increased from 23.0% at the start of the collaboration to 59.9%, facilitating cumulative premiums exceeding 3.3 billion yuan.

In terms of risk control, it can infer potential medical conditions even without direct diagnostic results, helping insurance companies accurately filter out 3.0% to 10.0% of high-risk individuals from all applicants in 2025. In a specific application case involving a state-owned insurance company, the identification rate of high-risk individuals surged from 0% to 2.0% before the collaboration to 3.0% to 10.0%.

The other is called Lop Nor — the 'AI detective' for claims processing.

This is a claims system integrating e-invoice processing, OCR, large language models, and vast amounts of medical rules.

When claims occur, the 'Smart Entry System' automatically parses medical records; subsequently, the 'Clause Decomposition Agent', 'Event Organization Agent', 'Claims Assessment Agent', 'Liability Determination Agent', and 'Risk Evaluation Agent' seamlessly collaborate to automatically compare clauses, calculate payouts, and detect fraud.

In 2025, Nuwa Tech assisted in reviewing 5.3 million claims cases, with an average automatic review rate of 74.1% (the highest automatic review rate reaching 85.0%), and large language model review accuracy reaching 98.0%.

In a case involving a state-owned insurance company's branch in Tianjin, after deploying Lobop, the efficiency of claim closure, measured by the number of days for claim settlement, increased fourfold.

In another case involving a state-owned insurer using its 'Comprehensive AI Underwriting and Claims Full-stack Solution', Nuwa Tech helped reduce the client’s loss ratio to 17.4% through dual empowerment at both underwriting and claims ends—significantly below the industry average of 43.5%.

It can be said that Nuwa Tech has, to a certain extent, solved the Achilles' heel of the health insurance industry: 'difficult claims, slow claims processing, and high fraud'.

However, the capital market always remains rational. In navigating deeper waters, as a star company operating at the intersection of financial insurance and data technology, Nuwa Tech constantly faces the Sword of Damocles hanging over its head.

For example, Nuwa’soperations heavily rely on massive amounts of patients’ health, medical, and claims data.Regulations such as the 'Cybersecurity Law of the People's Republic of China', the 'Data Security Law of the People's Republic of China', the 'Personal Information Protection Law of the People's Republic of China', and the 'Network Data Security Management Regulations', which came into effect in January 2025, are becoming increasingly stringent.

Although Nuwa emphasizes implementing strict desensitization and cleaning protocols before training large models to ensure personal information is never used for large model training, in highly regulated fields, any actual or alleged data breaches or unauthorized use could result in devastating regulatory penalties and reputational damage to the company.

At the same time, overseas regulatory risks are escalating. For instance, the recently issued 'Foreign Investment Rules' by the US Treasury Department impose a ban on investments involving China's AI systems and other related fields, adding uncertainty to Nuonova’s future international capital market financing.

Therefore, standing at the gateway to an IPO sprint, Nuonova Technology needs to demonstrate to the secondary market that this flywheel driven by data and algorithms can seize market opportunities under compliance conditions and navigate toward the vast trillion-dollar blue ocean.

From this perspective, the “second half” battle for Nuonova Technology and China’s health insurance sector has just begun.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

2