Emotional Explosion in the Silicon Predicament: Polysilicon's Journey from Halving to Limit-Up Amid Anti-Internal Competition

(This article was authored by Duo Kong Xiangxian and published by Titanium Media with permission)

By Duo Kong Xiangxian

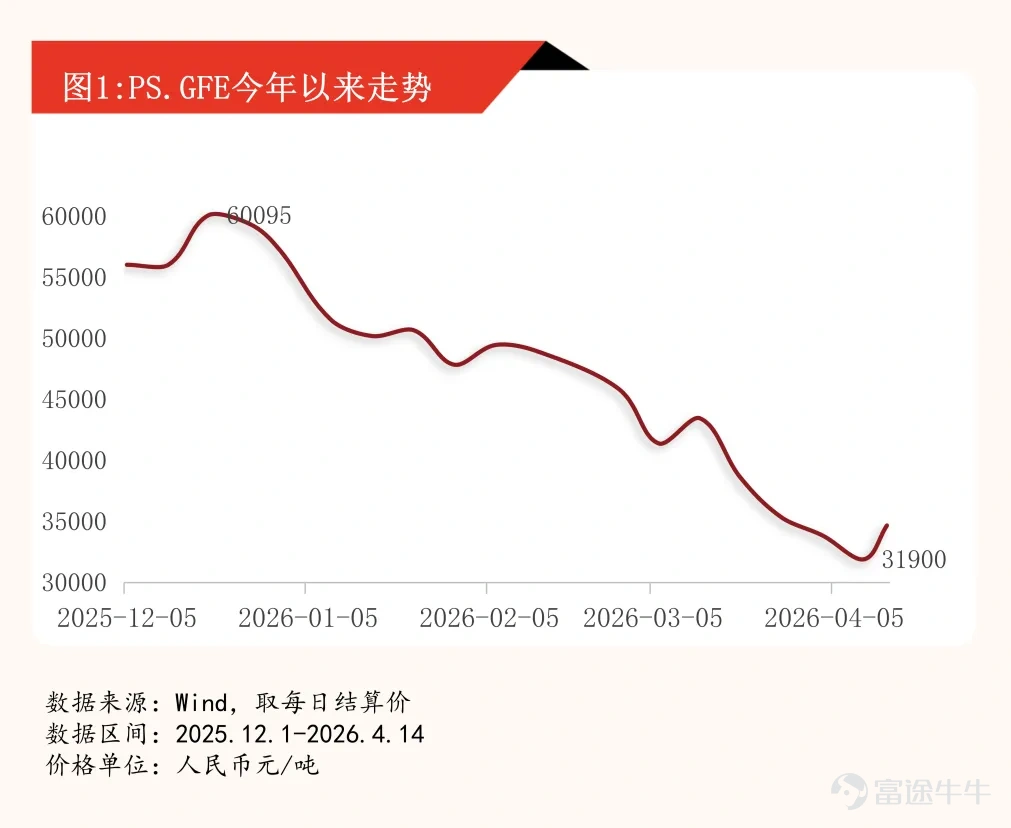

On the afternoon of April 13, 2026, the main polysilicon contract 2605 on the Guangzhou Futures Exchange surged and remained locked at the daily limit-up price, closing at 34,770 yuan per ton, with a gain of 9%. The trading volume exceeded 60,000 lots. The A-share photovoltaic sector followed with a strong rally, as Daqo New Energy once rose over 12%, and Tongwei Co., Ltd. saw significant gains.

However, the trigger for this 'limit-up feast' was not an improvement in fundamentals but an unverified 'rumor.' It was rumored that several leading photovoltaic companies held a closed-door meeting in Chengdu at the beginning of April to discuss mandatory production control, setting a 'firm bottom' for silicon material prices and establishing a penalty mechanism for breaches. After the market closed, companies like GCL Technology, TCL Zhonghuan, and LONGi Green Energy successively denied the rumors, which were proven false.

In the afternoon of April 13, the main futures contract for polysilicon suddenly surged in volume and eventually closed at a 9% limit-up, with prices settling at 34,770 yuan per ton. Multiple contracts hit their limit-up simultaneously that day, showing typical characteristics of 'news-driven + short interest squeeze.' The open interest of the main contract reached 33,169 lots, with a trading volume of 59,236 lots, and the turnover significantly expanded. On the morning of April 14, polysilicon continued its upward momentum, surging more than 6% at one point during the morning session but retreated in the afternoon to close with a 0.61% gain, with trading volume increasing to 110,000 lots.

This is the first time polysilicon futures have hit the limit-up this year,Since the beginning of this year, the price of polysilicon futures has been continuously declining. Last Friday’s lowest price fell by 48.39% compared to the highest price at the beginning of the year, nearly halving. The main continuous contract fell by 18.61% in January, 1.37% in February, plummeted by 24.29% in March, and dropped by 8.74% in April (as of the close on April 10). The lowest price on April 10 was 31,070 yuan per ton, almost halving from 61,985 yuan per ton in December last year.

Following the sharp rise on April 13, photovoltaic concept stocks in the A-share market responded strongly. Daqo New Energy once surged by 12.16%, finally closing with a 7.93% increase; Tongwei Co., Ltd. and Hongyuan Green Energy also saw significant gains, with the sector's total market value soaring by over 10 billion yuan in a single day.

On the morning of April 13, a message about polysilicon 'anti-internal competition' spread in the market, mentioning that polysilicon would cut production and raise prices to 50,000 yuan per ton. Several leading photovoltaic companies held a closed-door meeting in Chengdu at the beginning of April to discuss mandatory production control and price stabilization. This rumor quickly spread, triggering a sharp rebound in the futures market.

After the market closed, the Futures Daily verified with multiple related companies and learned that the above meeting summary was false news. Regarding the statement that relevant meetings would be held this week or by the end of this month, several companies said they had not yet received any meeting notices, and the authenticity of the related information remains to be verified. GCL Technology and TCL Zhonghuan clearly responded that the news was untrue, while LONGi Green Energy stated that the company, being downstream in the industrial chain, was unaware of any related meetings.

Industry insiders reminded that market participants should rationally discern unverified news.

The direct driving factor behind the limit-up of polysilicon was the market rumor about production control, price stabilization, and profit recovery. GF Futures indicated that the rise in polysilicon futures prices was mainly influenced by news of production cuts and price control. Although the news has not been confirmed, some companies do indeed have plans for maintenance and production cuts based on their strategic decisions and the low price levels.

Xinhu Futures pointed out that the main drivers of the polysilicon futures rally are disturbances from news and support from cost pressures.On one hand, as the opening price was close to historical lows, some shorts took profits and exited; on the other hand, there were market rumors about an industry conference involving discussions on coordinated self-discipline against 'internal competition' in early April.

Guosen Futures believes that the rebound in polysilicon futures prices reflects a recovery in market sentiment, noting that 'after consecutive sharp declines, pessimism has been fully released, and coupled with the boost from anti-internal competition news, prices have stabilized and started to recover.'

From a capital perspective, some market participants noted that when the industry is extremely pessimistic, any news of production cuts could ignite market sentiment and strengthen expectations for policy support. Shorts who had accumulated significant gains began exiting as longs, fueled by prolonged accumulation, saw news-driven triggers becoming the last straw breaking short interest.

Even setting aside rumor factors, polysilicon prices have entered the cost-supported zone. Some listed companies previously disclosed polysilicon cost data: for example, Daqo New Energy reported cash costs at 33.95 yuan per kilogram. Last week, the main polysilicon futures contract fell to a low of 31,070 yuan per ton (or 31.07 yuan per kilogram), breaching this cost line, which to some extent reversed the downward trend of polysilicon futures.

Due to oversupply in the market, polysilicon futures prices previously broke below 31,000 yuan per ton, nearing the cash cost line of 27,000–30,000 yuan per ton for leading firms such as Tongwei Co. and GCL Technology. As losses expanded across the industry, some short positions chose to take profits and exit.

Additionally, the main polysilicon futures contract had been trading at over 2,000 yuan per ton below spot prices, increasing procurement activity among downstream enterprises, potentially including hedging participants. The continued drop in polysilicon prices toward the cost line further stimulated downstream firms' hedging demand.

From the supply side, current polysilicon production is showing signs of marginal contraction. Several companies plan maintenance shutdowns and production cuts in late April, with industry output expected to decrease month-over-month, easing supply pressure. Coupled with刚需 restocking in the downstream wafer sector and traders taking positions at lower levels, futures prices stabilized and rebounded.

According to GF Futures data, weekly polysilicon production stabilized at 19,300 tons. Earlier reports indicated that multiple companies planned maintenance shutdowns in April, potentially affecting around 10,000 tons of output, but reductions are expected later in the month, so April's production will not significantly decline. With the arrival of the rainy season, Southwest capacity may face further delays, though startups remain possible. At current prices, the willingness to resume production remains low, and some companies might even reduce output further.

Domestic demand remains weak, with downstream production decreasing month-over-month. Wafer production for April slightly declined to 48.73 GW, cell production edged down to 44.3 GW, and module production fell back to 32.15 GW, creating an inverted pyramid structure in downstream production. However, overseas demand has steadily grown, with FOB prices for modules exported through Chinese ports rising by 1.7–2.5%.

The Silicon Industry Branch Association predicts that, against the backdrop of falling costs and insufficient demand support, the wafer market is expected to remain weak in the short term. However, after recent consecutive declines, the room for further price drops in wafers is relatively limited, and if subsequent demand improves, the wafer market is expected to stabilize.

The core contradiction in the current market remains the imbalance between supply and demand. According to data from the Silicon Industry Branch of the China Nonferrous Metals Industry Association, the average transaction price of N-type multicrystalline silicon re-feed material from April 2 to April 8 was 36,000 yuan per ton, down 1.37% from the previous week; the average transaction price of N-type granular silicon was 35,000 yuan per ton, down 4.11% from the previous week.

In response, the Silicon Industry Branch believes that despite the reduction in production by polycrystalline silicon companies in February lowering industry operating rates to 35.5%, inventories continue to accumulate, indicating that the contraction in supply still falls short of offsetting the speed of weakening demand. A research report by NanHua Futures also points out that the fundamental aspects of the polycrystalline silicon sector currently exhibit a “weakness on both supply and demand” characteristic. On the supply side, the polycrystalline silicon market is under pressure from inventory and the resumption of operations by large factories, leading to strong selling intentions from manufacturers, even resulting in prices below cash cost lines. On the demand side, operating rates in downstream wafer, cell, and module segments remain low.

From the perspective of inventory levels, according to SMM statistics, the latest polysilicon manufacturer's inventory stands at 335,000 tons, up 1.50% from the previous period, while wafer inventory reached 27.45 GW, increasing by 1.48%. Data from GF Futures also shows a slight increase in weekly inventory by 5,000 tons to 335,000 tons, with warehouse receipts rising by 390 contracts to 11,970 contracts.

Looking at longer-term trends, since 2026, polysilicon inventories in China have continued to rise: initial January stockpiles were approximately 302,000 tons, increasing to 341,000 tons by early February, and slightly rising to 348,000 tons by early March. Domestic polysilicon production in March amounted to 92,600 tons, up 9.7% month-on-month, further exacerbating inventory pressures.

On the demand side, the accelerated decline in market prices has exacerbated the downstream “buying on rallies but not on declines” wait-and-see mentality. According to SMM statistics, N-type material prices range between 34.00-36.50 yuan/kg, and N-type granular silicon between 34.00-36.00 yuan/kg, with spot prices remaining stable. However, overall market trading sentiment remains subdued, with downstream participants showing low acceptance of high-priced sources, only purchasing for urgent needs.

The drop in polysilicon spot prices is related to excessively high industry inventory levels, weaker year-on-year photovoltaic installations, and weaker module output. Additionally, the cancellation of export tax rebates effective April 1 further impacted expectations for overseas demand.

By the end of the first quarter, polysilicon prices had fallen below the cost level of leading enterprises, leaving the entire industry in widespread losses. The main reason behind this year’s sharp drop in polysilicon prices lies in oversupply and persistently high inventory. Furthermore, while other segments of the photovoltaic industry are still struggling around break-even points, the polysilicon segment enjoyed higher profits due to last year's price surge, which also created significant downward pressure.

Some research suggests that the event in early January 2026, where the State Administration for Market Regulation held talks with the Photovoltaic Association and major companies to communicate monopoly risks, changed the operational landscape of polysilicon. Following the meeting, divisions emerged within the polysilicon alliance, with some companies selling large volumes at low prices, bringing the industry back to fundamental logic. Although spot prices fell to about 35 yuan/kg, buyers continued to test the price floor, further depressing prices. Market data also shows that polysilicon futures began this round of sharp declines on January 7.

The industry generally expects that polysilicon prices are still in the bottom-probing phase, and the sector needs to go through a difficult 'grinding bottom' period. The first sign is the continued low operating rate of the industry, which dropped to 35.5% in February, with no short-term recovery momentum. The second sign is that cash flow pressure has become the core variable for industry consolidation, with some companies starting to passively cut production through maintenance shutdowns or production halts. The third sign is that the appearance of an inventory turning point is a leading signal of prices truly bottoming out, but this signal has not yet appeared.

Experts from the China Photovoltaic Industry Association believe that the second quarter could see prices rebound to a reasonable range through further production cuts and inventory reduction. The industry load is already at a low level, but terminal demand recovery is slow, and inventory digestion will take time, requiring continued reduction in load, especially for leading companies with high production capacity shares.

The policy of VAT export tax rebates for photovoltaic products was officially canceled on April 1, significantly impacting the demand side of the industry. Overseas market demand weakened further, causing photovoltaic module companies' operating rates to gradually decline and progressively affect upstream sectors. GCL Technology's earnings briefing stated,The first quarter is the off-season for the photovoltaic industry, compounded by the impact of policies such as export tax rebates, which is the main reason for the recent decline in polysilicon prices.

Operating rates in downstream silicon wafer, cell, and module segments remain low, with the entire upstream and downstream sectors primarily focused on inventory consumption, spreading market pessimism.

On April 1, the Guangzhou Futures Exchange released a notice optimizing polysilicon futures rules, simultaneously adjusting trading thresholds, fees, and margin requirements, with the changes officially taking effect on April 3, significantly improving liquidity in the polysilicon futures market.

From a policy perspective, the anti-internal competition orientation in the downstream photovoltaic industry has become increasingly clear in recent years. As early as November 2024, the Ministry of Industry and Information Technology revised the 'Photovoltaic Manufacturing Industry Standard Conditions' and the 'Interim Measures for the Management of Photovoltaic Manufacturing Industry Standards.' In December 2025, the long-awaited 'Polysilicon Production Capacity Consolidation and Acquisition Platform' was implemented. In April this year, the MIIT held a meeting emphasizing the need to resolutely eliminate internal competition in the photovoltaic industry and enhance the resilience and security of key industrial chains and supply chains. This policy background provides 'reasonable' room for market speculation.

The涨停行情 observed yesterday was essentially driven by rumors rather than fundamental improvements, but it reflected the market's strong expectation for a 'turnaround from difficulties' in the polysilicon segment. Although leading manufacturers benefited from the rise in stock prices, the trading atmosphere in the spot market did not fundamentally improve.

From the perspective of corporate costs, Daqo New Energy's announcement shows that the unit cash cost of polysilicon is 33.95 yuan per kilogram, while futures prices have fallen below 31 yuan per kilogram, placing it in a deep loss-making zone.

The expected rise in polysilicon prices will directly increase raw material costs for the wafer segment. Currently, the wafer segment itself faces profitability pressure and persistently low operating rates; an increase in upstream costs will exacerbate its operational pressures. According to SMM data, domestic N-type 18Xmm wafers are priced at 0.94 yuan per piece, while N-type 210mm wafers are priced at 1.23 yuan per piece, with prices continuing to operate at low levels. Wafer production reached 10.82GW, down 1.55% from the previous period.

Profit margins in downstream segments are further squeezed. In terms of cells, high-efficiency PERC182 cell prices stand at 0.27 yuan per watt, while Topcon M10 cell prices are 0.35 yuan per watt. For modules, mainstream transaction prices for N-type 182mm modules range from 0.74 to 0.76 yuan per watt, and for N-type 210mm modules, prices range from 0.75 to 0.78 yuan per watt, with both remaining at low levels.

The composite price index for the photovoltaic industry indicates that as of April 7, SPI (polysilicon) has dropped by 32.74% year-to-date, SPI (wafers) has decreased by 19.82%, but SPI (cells) has risen by 3.05%, and SPI (modules) has increased by 7.73%, showing a clear divergence between upstream and downstream sectors.

In the short term, after sentiment recedes, focus will return to fundamentals. Huatai Futures predicts that polysilicon prices are expected to remain weak and volatile, with industrial silicon prices also staying subdued, making polysilicon cost support fragile, compounded by high inventory levels and difficult demand transmission across the supply chain.

In the medium term, the pace of production cuts and capacity clearance, the rate of hidden inventory reduction, whether there will be substantial policy measures, and the subsequent impact of the cancellation of export tax rebates are the four key factors.

In the medium to long term, energy security and power demand growth driven by AI development are expected to boost demand for polysilicon. Institutions predict that global new photovoltaic installations in 2026 will range from 500 to 667 GW, with domestic new installations projected at 180 to 240 GW. As emerging market demand rises in India, the Middle East, and North Africa, global new photovoltaic installations during the 'Fifteenth Five-Year Plan' period are expected to return to a stable upward trajectory, with average annual new installations forecasted at 725 to 870 GW. However, these medium- to long-term factors are unlikely to release significant incremental demand in the short term.

Reference materials

[1] Polysilicon spot quotes and inventory data, Shanghai Nonferrous Metals Network

[2] Silicon Branch of the China Nonferrous Metals Industry Association: Weekly Polysilicon Market Report

[3] Polysilicon Daily: With Inventory at High Levels, Expected Price Rebound Is Limited, Huatai Futures

[4] Polysilicon: Expectations of production cuts and price increases drive polysilicon futures to limit-up, GF Futures

[5] Multiple contracts hit limit-up! A 'message' ignites the polysilicon market, Futures Daily

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comment (1)

to post a comment