After trending on hot search, looking at CMB: Is that highlighted moat still solid?

By Dong Xuan

Source: Node Finance

On Weibo's trending topics list, banks are rarely seen, but they do make appearances.

At the end of March, due to a statement made by Chairman Miao Jianmin at the earnings conference, China Merchants Bank was pushed onto the trending list.

Tracing back to the origin of the incident, it started when a media outlet asked, 'In the past, when people talked about China Merchants Bank’s moat, they might think of retail, service, cost of liabilities, etc. Now, entering the low-interest-rate era, what is China Merchants Bank’s moat?'

Miao Jianmin replied that China Merchants Bank's real moat lies in internalizing the concept of 'customer-centricity' as part of its corporate culture and transforming it into employees' daily actions.

He further elaborated with examples: employees at China Merchants Bank seldom leave work on time, and the board office staff completed extensive investor communication materials within two days. This core competitiveness, built on cultural cohesion and professionalism, supports China Merchants Bank's superior performance compared to its peers.

Unexpectedly, the phrase 'employees at China Merchants Bank seldom leave work on time' caused a storm of reactions, sparking heated discussions among netizens. Some questioned the bank's 996 work culture, while others suggested notifying the labor inspection department…

Image source: Weibo

After the commotion died down, reviewing China Merchants Bank’s 2025 report card, although it has consistently outperformed the industry, signs of strain on its 'moat' have emerged.

The 'top student’s' report card

If the keyword for CMB in 2024 was 'under pressure,' then the keyword for 2025 is 'recovery.'

The financial report shows that in 2025, China Merchants Bank achieved revenue of 337.532 billion yuan, a year-on-year increase of 0.01%; net profit attributable to shareholders reached 150.181 billion yuan, a year-on-year increase of 1.21%, equivalent to earning 411 million yuan per day.

The '0.01%' may seem negligible, but this is a signal that China Merchants Bank has returned to an upward trajectory after experiencing two consecutive years of negative revenue growth in 2023 and 2024.

Image source: East Money

As Wang Liang of the industry mentioned during the earnings briefing, '(Revenue) declined for two years, and finally achieved positive growth. This result is a slight increase, but it was hard-earned.'

Over the past year, facing multiple pressures such as the continued decline in LPR (Loan Prime Rate), adjustments to existing mortgage interest rates, and weak credit demand, China Merchants Bank's ability to stabilize its revenue base has already demonstrated the resilience of its operations.

Supporting this stability are the marginal improvements in China Merchants Bank's net interest margin, leading capital strength, and extremely low non-performing loan ratio.

In recent years, the continuous drop in net interest margin has sent chills through the industry, and China Merchants Bank was no exception. However, in the fourth quarter of 2025, there was a turning point for China Merchants Bank's net interest margin, which increased by 3 basis points quarter-on-quarter (group口径), eventually settling at 1.87% for the full year.

Although this is still 11 basis points lower than the previous year, the slight rebound in the fourth quarter was significant. Vice President Peng Jia Wen revealed at the earnings conference that this was due to active management on both sides of the balance sheet, such as reducing low-yield bills and increasing the proportion of high-yield assets.

Within the industry, China Merchants Bank's net interest income remains at the forefront. According to data disclosed by the National Financial Regulatory Authority, as of the end of 2025, the net interest margin of commercial banks was 1.42%.

While most peers were struggling with their non-performing loan ratios, as of the end of 2025, China Merchants Bank’s indicator remained controlled at an extremely low level of 0.94%, a decrease of one basis point from the previous year.

It is not easy to keep the non-performing loan ratio below 1% amid economic cycle fluctuations. More importantly, its provision coverage ratio is as high as 391.79%, a figure that is not only three times the regulatory standard but also about twice the industry average.

This means that CMB is well-prepared to weather the winter with substantial risk resistance barriers and profit reserves.

Secondly, formidable capital strength.

As of 2025, CMB's total assets have broken through the 13 trillion yuan mark for the first time, further strengthening its scale effect.

Ranked by Tier 1 capital, CMB ranks 8th among the top 1000 global banks, advancing two places from 2024; its total capital adequacy ratio at the end of the period was 18.24%, maintaining a leading level in the industry.

However, during the deep adjustment phase of the industry, CMB could not remain immune, with collective declines in capital adequacy ratio indicators.

Overall, whether considering size, safety buffers, or profitability, CMB’s foundation remains solid, making it an undisputed 'top student' in the industry.

Retail business encounters 'offensive and defensive battles'.

However, behind this robust report card, the trending question 'What is the moat?' is striking a nerve with CMB.

As Chairman Miao Jianmin stated: CMB's true moat lies in internalizing the concept of 'customer-centricity' as corporate culture and translating it into employees’ daily actions. Professionalism, dedication, and quality service have long been the chips that earned CMB the title of 'King of Retail,' and its retail business remains a key benchmark for capital markets when assigning valuation premiums to CMB.

However, over the past year, the retail business fortified by this 'moat' has faced an unprecedented 'tug-of-war,' becoming a pressing issue that China Merchants Bank's management needs to address urgently.

According to the financial report, in 2025, China Merchants Bank's retail business generated revenue of 191.017 billion yuan, a decrease of 5.818 billion yuan from 196.835 billion yuan in the same period in 2024, representing a 2.96% decline; pre-tax profit reached 90.676 billion yuan, up 0.32 billion yuan from 90.644 billion yuan in the same period in 2024, reflecting a 0.04% increase.

Meanwhile, the share of pre-tax profit from the retail business dropped to 50.66%, further shrinking from 50.74% in the same period in 2024.

Source: China Merchants Bank's financial report

Specifically, China Merchants Bank's retail business is currently facing multiple challenges such as credit slowdown, asset quality volatility, and weakness in the credit card segment.

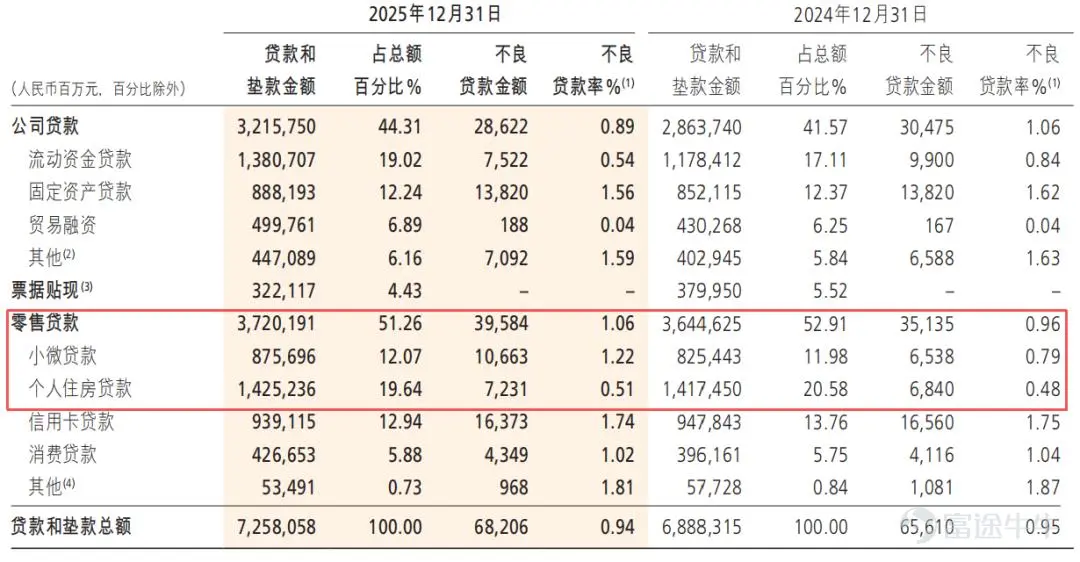

By the end of 2025, China Merchants Bank's retail loan balance stood at 3.72 trillion yuan. Despite its still significant size, the year-on-year growth rate slowed significantly to only 2.07%.

More concerning is the risk. In 2025, the non-performing loan ratio of China Merchants Bank's retail loans increased from 0.96% to 1.06%, rising by 10 basis points. Among them, the non-performing loan ratio for small and micro-enterprise loans, once considered high-quality assets, surged from 0.79% to 1.22%; the non-performing loan ratio for individual housing loans also slightly rose from 0.48% to 0.51%.

Source: China Merchants Bank's financial report

In response, Executive Vice President and Chief Risk Officer Xu Mingjie acknowledged that risks across the entire retail credit market are still on the rise. The real estate market continues to adjust in the short term, and whether residents' employment and income can improve rapidly has also placed certain pressures on the asset quality of small and micro-loans and consumer loans.

Adding to the concerns, credit card transaction volumes are still contracting.

As the retail spearhead of China Merchants Bank, the credit card business showed mixed performance in 2025. Node Finance observed that while the number of cards in circulation rebounded from previous declines, credit card transaction volume fell by 7.62% year-over-year to 4.08 trillion yuan. This reflects to some extent that users holding China Merchants Bank credit cards are reducing their use of consumer credit.

In response, China Merchants Bank has chosen a path of 'sacrificing scale for quality.' President Wang Liang stated: 'We are willing to bear this decline in revenue share to ensure proper control over asset quality.'

This represents a typical defensive posture. Before the macroeconomic fog clears, China Merchants Bank prefers to let its credit card business 'slow down' rather than loosen risk controls in pursuit of boosting performance.

On the positive side, China Merchants Bank’s wealth management business has shown strong signs of recovery.

In 2025, China Merchants Bank’s wealth management revenue reached 44.013 billion yuan, a year-over-year increase of 16.91%. Revenue from fund distribution surged 40.36%, and revenue from wealth product distribution grew by 18.98%. This provides significant support for stabilizing its retail business.

A report by Donghai Securities noted that fee-based income is the core representation of China Merchants Bank’s retail strategy. Its strong customer base, product system, channel reach, and professional services form an almost insurmountable competitive barrier. The company’s client foundation and specialized systems in wealth management remain unshaken. With non-interest income elasticity far exceeding industry peers, wealth management is expected to return as a core driver of earnings contributions.

Conclusion

Looking ahead, Chairman Miao Jianmin proposed a new strategy of balanced development across 'four major segments,' relaunching retail efforts, surpassing corporate banking, and building a smart bank… This effectively acknowledges a fact: for the foreseeable future, China Merchants Bank can no longer rely solely on retail as the single growth engine but needs four wheels—retail, corporate banking, investment banking, and asset management—to drive forward simultaneously.

But transitioning from a single engine to four-wheel drive raises the question: can China Merchants Bank’s 'moat' sustain the weight of these 'four major segments'? The answer remains on the journey ahead.

*The cover image is generated by AI.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment