Following the failed launch of the ASTS satellite, where do space-related stocks go from here?

SpaceX, Amazon and other giants are competing! Morgan Stanley launches Space Race 2.0 investment guide: This 'Space 60' list is worth watching!

The news of SpaceX's upcoming public listing is triggering a funding frenzy across space-related stocks.

According to Bloomberg citing sources familiar with the matter, SpaceX has confidentially filed for an IPO, with its target valuation now raised to over $2 trillion, and it may go public as early as June this year.

Meanwhile, Amazon is in acquisition talks with satellite operator GlobalStar, with an announcement expected as early as April 14 local time; if successful, GlobalStar will help Amazon strengthen its satellite business to compete with SpaceX's 'Starlink.'

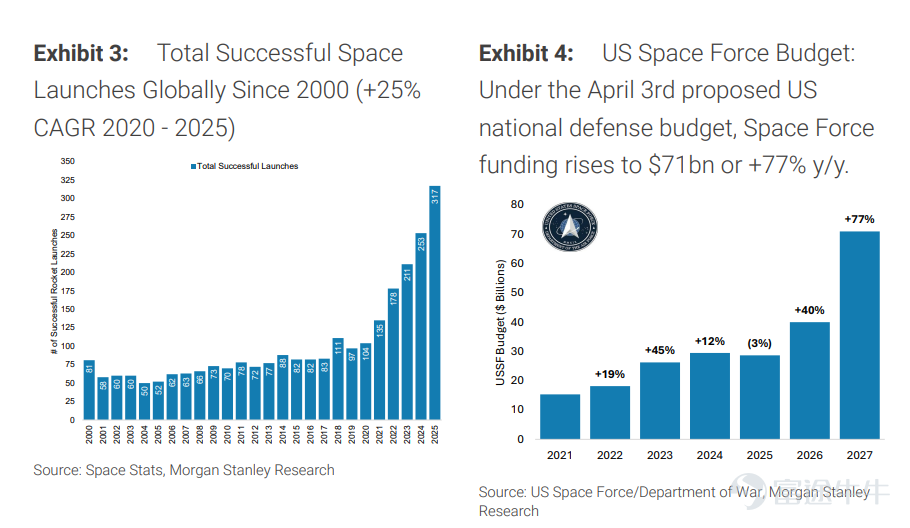

This series of market-shaking news confirms optimistic expectations for the space economy. Notably, according to Morgan Stanley’s latest research report, from 2020 to 2025, the cumulative number of objects launched into space grew at a compound annual growth rate (CAGR) of about 20%, while the CAGR for successful launches was approximately25%. Additionally, the US government’s budget proposal also calls for a significant increase in the US Space Force's budget compared to 2026,77%reaching $71 billion.

Source: Morgan Stanley

Amidst the heated market sentiment, investors are actively seeking reasonably valued derivative investments. Just like the California Gold Rush of the 19th century, the safest bet often lies with those providing infrastructure and equipment — the 'picks and shovels.'

To this end,Morgan Stanley has launched the 'Space 60' list,a comprehensive list of publicly traded space-enabling companies covering the entire value chain, including raw material producers, component manufacturers, and operators themselves. The report divides the industry into seven core areas:

Specifically:

Raw materials and mining: The structure, power, and communication systems of a single satellite may require the use of dozens of specialty metals.

$MP Materials (MP.US)$ : A U.S.-based rare earth magnet producer operating the Mountain Pass facility in California. This is the only large-scale rare earth mining and processing plant in North America. The company's facility in Fort Worth, Texas, manufactures rare earth magnets, which are crucial for aerospace and defense supply chains, including satellites and guidance systems.

$Almonty Industries (ALM.US)$: A leading non-China tungsten producer operating the Sangdong mine in South Korea. Commercial operations at this mine began in December 2025, with full production capacity expected to supply over 80% of the world’s non-China tungsten output. Tungsten, known for its extremely high density and melting point, is used in extreme high-temperature environments such as rocket engine nozzles and heat shields.

$Freeport-McMoRan (FCX.US)$: One of the largest publicly traded copper producers globally, accounting for approximately 5% of global copper production in 2025, ranking among the top three worldwide. As a major global copper supplier, the company is well-positioned to benefit from the growing demand for copper and other metals driven by satellite manufacturing and space infrastructure development.

$Alcoa (AA.US)$: A leader in bauxite, alumina, and aluminum products. In October 2025, Alcoa announced a joint venture in Western Australia to produce 100 tons of gallium annually (about 10% of global demand), reducing reliance on China, which currently accounts for 99% of gallium production. Gallium is critical for semiconductors used in satellite power systems and communication equipment.

$Teck Resources (TECK.US)$ : A major producer of copper and zinc, as well as the largest germanium producer in North America and fourth-largest globally.

Special materials and alloys: Provide engineering superalloys and composite materials capable of withstanding extreme temperature fluctuations and high mechanical stress in deep space.

$Carpenter Technology (CRS.US)$ : Primarily produces specialty titanium and nickel alloys for the aerospace and defense markets, which accounted for over 60% of its FY2025 revenue.

$ATI Inc (ATI.US)$ : A leading brand in specialty alloys, with aerospace and defense accounting for 68% of its FY2025 sales. The company is one of the few U.S. manufacturers of C-103 (a niobium-based alloy designed for high-temperature applications in engines and thrusters).

$Materion (MTRN.US)$ : A major supplier of advanced materials and composites in the U.S. The company owns the world's largest source of beryllium in Utah (historically representing 85% of global supply). Beryllium has an extremely high stiffness-to-weight ratio and thermal stability, making it ideal for precision optical systems in space.

$Hexcel (HXL.US)$ : A leading manufacturer of advanced composites (such as carbon composite structures, heat shields). Its 'Defense, Space & Others' segment accounted for 39% of FY2025 revenue ($747 million), with sales in the space sector (including launchers, rocket engines, and satellites) continuing to grow.

$Corning (GLW.US)$ : A top supplier of glass aerospace optics (including telescope lenses, satellite windows),having provided products for multiple NASA missions such as Hubble and Gemini.

$Park Aerospace (PKE.US)$ : Specializes in advanced composites and metal components for aerospace. The military market accounted for 42% of its $62 million total sales in FY2025, with rocket nozzles representing the largest portion (44%) of military sales.

Propulsion systems and fuel: A single launch may require hundreds of tons of propellant, with propellant typically accounting for over 85-90% of the total launch mass.

$Linde (LIN.US)$ : A leading industrial gas company supplying more than four-fifths of U.S. launches. Space propulsion accounts for approximately 2% of its early 2026 sales, with space customers expected to become its largest commercial clients by 2027.

$Air Products & Chemicals (APD.US)$ : A major industrial gas supplier, with space propulsion making up over 2% of its F1Q26 total sales. The company has supplied NASA with liquid hydrogen since the 1960s and is estimated to hold about 40-50% market share in the U.S. space propulsion market.

$Air Liquide SA Unsponsored ADR (AIQUY.US)$ : Provides propulsion gases at every U.S. launch pad and maintains a long-term partnership with NASA. Its technology spans from hydrogen to krypton and xenon used in satellites, serving over 180 clients within the U.S. space ecosystem.

$NewMarket (NEU.US)$ : Its specialty materials division (including AMPAC, which provides solid rocket propellants, and Calca, a supplier of high-purity hydrazine for liquid fuels) accounted for approximately 7% of total revenue in fiscal year 2025.

Electronics and semiconductors: Satellites rely on radiation-hardened chips and sensors to operate in space.

$Analog Devices (ADI.US)$ : Supplies radiation-hardened semiconductors to commercial space operators. Its aerospace and defense business generates annual revenues exceeding $1 billion, accounting for over 10% of total revenue.

$STMicroelectronics (STM.US)$ : Has provided over 5 billion RF antenna chips for LEO satellite terminals since 2015; its RF and optical communications division grew 23% year-over-year in Q4 2025.

$INFINEON TECHNOLOG (IFNNY.US)$ : Supplies radiation-tolerant power semiconductors and microelectronics (including sensors and MOSFETs) for satellites and space-grade systems.

$Microchip Technology (MCHP.US)$ : Offers radiation-hardened FPGA products for satellites. With 60 years of flight heritage applied across more than 90 missions, its aerospace and defense business accounted for 18% of total revenue in fiscal year 2025.

$Qorvo (QRVO.US)$ Actively expanding into the space and satellite communications market, developing Ka-band antennas and RF solutions for high-throughput satellites.

$Mercury Systems (MRCY.US)$ Provides radiation-hardened processing subsystems. Space business revenue for the 2025 fiscal year was $56 million, accounting for 6.1% of total revenue.

$TTM Technologies (TTMI.US)$ Offers printed circuit boards (PCBs) and RF components for satellite communications. Aerospace and defense accounted for 44% of total revenue in 2025, with approximately 4% coming from the space sector.

$Broadcom (AVGO.US)$ Entering the space market through RF components, optical/laser components, and custom chips; its micro-optical components have already been used in satellites.

$Coherent (COHR.US)$ A supplier of LEO satellite laser communication links, with the potential to become a driver of orbital AI infrastructure.

$Lumentum (LITE.US)$ Could drive the space market by providing photonic components such as lasers and transceivers suitable for optical communication architectures.

$NVIDIA (NVDA.US)$ : Announced at the 2026 GTC Conference the entry into the space market through the 'Space-1 Vera Rubin' module, an AI computing platform designed for orbital data centers, supporting real-time processing of satellite data in orbit and even running large language models.

Components and subsystems: Space systems rely on thousands of individual parts; the failure of a single component could jeopardize the entire mission.

$Teledyne Technologies (TDY.US)$ Provides commercial and defense imaging technology, integrating its space business in April 2026 to establish 'Teledyne Space.' The aerospace and defense electronics division accounted for 17% of FY25 total sales.

$RBC Bearings (RBC.US)$ Offers bearings and engineering solutions for rocket and satellite structures. In 2025, acquired valve and subsystem supplier VACCO Industries to further expand its space footprint.

$Parker Hannifin (PH.US)$ : Designs and manufactures valves, hydraulic, and thermal solutions for spacecraft. The aerospace division accounts for 31% of total revenue in fiscal year 2025.

$AMETEK (AME.US)$ : Provides precision instruments and specialty alloys used in Atlas V rockets, Artemis missions, and more.

$Amphenol (APH.US)$ : A leader in satellite and communication data network cabling products. Defense (including space) market accounts for 9% of FY25 sales.

$Aptiv PLC (APTV.US)$ : Offers space-grade solutions through its subsidiary's wiring harnesses and software.

$Moog-A (MOG.A.US)$ : Primarily designs and manufactures drive components for commercial and government spacecraft. Space and defense segment sales reached $1.1 billion in 2025.

$Graham (GHM.US)$ : Supplies propulsion, cryogenic, and thermal management equipment to the space industry. The space sector, while accounting for only 7% of FY25 revenue, has achieved a compound annual growth rate of 37% since 2022.

$Karman Holdings (KRMN.US)$ : Specializes in propulsion subsystems and payload protection. Space and launch account for 36.9% of 2025 revenue.

$Honeywell (HON.US)$ : Its technology is deployed on over 950 satellites and all NASA manned missions over the past nearly 60 years. The aerospace technology division generated $17.5 billion in revenue in 2025, with plans to spin off this division in Q3 2026.

Spacecraft and Launch Systems: Includes companies responsible for designing satellites and rockets, and providing orbital launch services.

$Redwire (RDW.US)$ : Provides solar arrays, avionics, and in-orbit manufacturing technologies. The space division accounts for 62% of total revenue ($335 million) in 2025.

$Rocket Lab (RKLB.US)$ : Provides Electron and Neutron launch vehicles and satellite manufacturing services.

$Boeing (BA.US)$ : Its Defense, Space & Security (BDS) division handles missions such as the X-37B, SLS rocket, and Starliner spacecraft. Revenue reached $27.2 billion in 2025 (30% of total revenue).

$Northrop Grumman (NOC.US)$ : Provides satellites, sensors, and launch vehicles (e.g., GEM 63 boosters). The Space Systems segment achieved sales of $10.7 billion in 2025.

$MDA Space (MDA.US)$ : Provides satellite systems and robotic technologies (e.g., Canadarm3). Recorded a record revenue of $1.6 billion in fiscal year 2025.

$York Space Systems (YSS.US)$ : Offers standardized satellite platforms with an annual production capacity exceeding 1,000 satellites. FY25 revenue was $386 million.

$Lockheed Martin (LMT.US)$ : Develops satellites and strategic defense systems (e.g., Orion spacecraft). The space division reported sales of approximately $13 billion in 2025 (17% of total revenue).

$Kratos Defense & Security Solutions (KTOS.US)$ : Provides virtualized satellite ground systems (OpenSpace platform) and a global space domain awareness sensor network.

$Firefly Aerospace (FLY.US)$ : Offers the Alpha rocket and Blue Ghost lunar lander (the only commercially successful lunar landing vehicle).

$Voyager Technologies (VOYG.US)$ : Involved in space infrastructure and the planned Starlab commercial space station. Net sales in 2025 reached $166 million.

$Intuitive Machines (LUNR.US)$ : Provides Nova-C and Nova-D lunar landers. Revenue in 2025 was $210 million, with expectations to grow nearly fivefold to nearly $1 billion by 2026.

$RTX Corp (RTX.US)$ : Raytheon division provides integrated defense systems including space-based systems, with sales reaching $28.04 billion in 2025.

Satellite operations and services: Generates revenue by providing communication, Earth observation, navigation, and data services; Amazon and Globalstar fall under this segment.

$Amazon (AMZN.US)$ : Promoting Amazon Leo (Project Kuiper), a low-orbit broadband satellite constellation, with plans to deploy over 3,200 satellites, of which more than 200 are already in orbit.

$Gilat Satellite Networks (GILT.US)$ : A provider of global ground satellite communication equipment and services (e.g., VSATs, antennas).

$Viasat (VSAT.US)$ : Operates a fleet of 23 satellites, providing satellite internet, in-flight connectivity, and defense communications, along with a significant ground infrastructure business.

$AST SpaceMobile (ASTS.US)$ : Building a space-based mobile broadband network that can be accessed directly by standard smartphones. Full-year revenue for 2025 reached 70.9 million US dollars.

$Iridium Communications (IRDM.US)$ : The only commercial provider offering truly global coverage communication services via a constellation of 66 low-orbit L-band satellites. Total 2025 revenue was $871 million.

$Globalstar (GSAT.US)$ : Providing mobile satellite services through an LEO satellite constellation, with 85% of its network capacity dedicated to Apple’s SOS emergency service. Revenue for 2025 was $273 million.

$Planet Labs PBC (PL.US)$ : Operating one of the largest fleets of Earth observation satellites globally (e.g., Doves and SkySat). Fiscal year 2026 revenue amounted to $307 million; the company is also collaborating with Google on Project Suncatcher, which aims to deploy orbital data centers equipped with Google TPUs by early 2027.

$BlackSky Technology (BKSY.US)$ : Provides real-time imagery and AI analysis through high-resolution LEO satellites. 2025 revenue was $106 million.

$Spire Global (SPIR.US)$Operates approximately 100 nano-satellites, collecting radio frequency data and providing space intelligence and weather forecasting services.

$Telesat (TSAT.US)$Provides GEO mission-critical satellite communication services and is developing the Telesat Lightspeed LEO satellite constellation with 198 satellites.

EutelsatCombined with OneWeb resources, Eutelsat has become the first operator to fully integrate GEO (34 satellites) and LEO (over 600 satellites). Total revenue for the 2024-25 fiscal year reached 1.24 billion euros.

SESAcquired Intelsat in July 2025, owning a fleet of about 120 GEO and MEO satellites. Revenue for 2025 was 2.627 billion euros.

Summary

SpaceX's potential IPO and Amazon's acquisition strategy are undoubtedly catalysts igniting the explosion of the space economy. However, from the perspective of the capital markets, beyond the star companies directly involved in launch and satellite operations, the 'picks and shovels' hidden deep within the supply chain—those providing critical metals, radiation-resistant semiconductors, and precision components—are perhaps the indispensable cornerstones supporting this interstellar expansion.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (11)

to post a comment

315

1037