"AI Bottleneck Trade" Ignites Upstream Sector—Who’s Raking in the Profits?

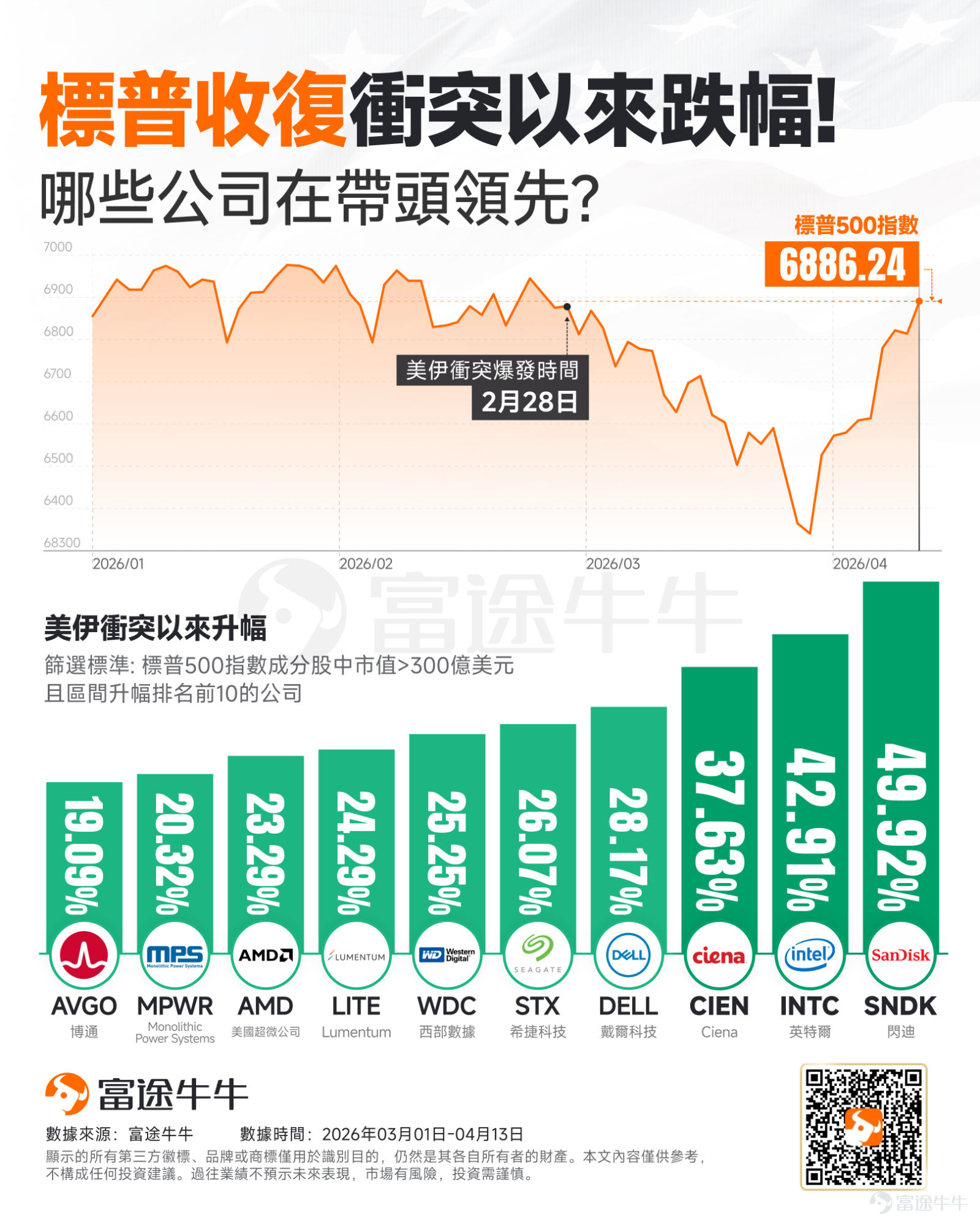

S&P recovers losses since the conflict! Which companies are leading the way?

Despite many issues remaining unresolved since the outbreak of the US-Iran conflict, with the stability of the temporary ceasefire agreement being highly tested, the risk-off sentiment in the capital markets has reached a significant turning point following President Trump's optimistic announcement today at the White House that Iran had proactively called to seek a reconciliation agreement.

The three major U.S. stock indexes surged overnight, with the S&P 500 closing up 1% and the Nasdaq closing up 1.2%, fully recovering all losses since the outbreak of the US-Iran conflict.

In this round of recovery, the capital markets have demonstrated extremely strong resilience. The sectors that took the lead not only stabilized the market but also clearly outlined the most critical investment themes of the year:With tech hardware and semiconductor giants as the anchor, the infrastructure for storage, communication, and optical networks driven by the deep wave of AI is leading a comprehensive recovery in the tech industry, becoming the core force cutting through geopolitical uncertainty.

These leading stocks are not speculative plays but precisely correspond to the four core components of the AI industry chain transitioning from 'logical imagination' to 'earnings realization,' with funds drawing a clear map of AI infrastructure construction using real investments.

1. Anchor: Revaluation of the value of computing power and IT terminals

During periods of market turbulence, tech giants with core competitive barriers become the preferred choice for capital. The camp represented by...$Advanced Micro Devices (AMD.US)$ 、 $Intel (INTC.US)$ 、 $Broadcom (AVGO.US)$ and $Dell Technologies (DELL.US)$ has built a solid foundation for this rebound.

Dual engines of computing power and networking:

◦ $Advanced Micro Devices (AMD.US)$ As a pioneer in high-performance computing chips, AMD is continuously capturing and reshaping the competitive landscape of AI accelerator cards. According to Bloomberg, South Korean AI startup Upstage plans to purchase 10,000 of AMD’s latest MI355 chips, a significant order that opens a new breakthrough for AMD in expanding its AI computing power market in the Asia-Pacific region.

◦ $Intel (INTC.US)$ It has strongly defended its position in the CPU and wafer foundry sectors. Driven by a 10% price increase for server CPUs, collaboration with Musk's Terafab, and progress on the 14A advanced process node, it achieved a historic nine-day consecutive stock price rise, surging 58% cumulatively in 58 days.

◦ On the data center backend,$Broadcom (AVGO.US)$ With absolute dominance in customized AI chips (holding over 80% of the ASIC market share) and Ethernet switch chips, it has become an indispensable 'leader' in the data center backend network.

Recovery on the device side and hardware upgrades:

◦ $Dell Technologies (DELL.US)$ The strong follow-up rise confirms that AI capabilities are accelerating from the cloud to the device side. With breakthroughs in the AI PC ecosystem and large-scale deployment of enterprise-level AI servers, traditional IT hardware is experiencing a new wave of replacement and value reassessment.

II. Reservoir: The AI data flood triggers a 'storage supercycle' reversal

Training and inference of large models fundamentally involve processing massive amounts of data. Without a vast data 'reservoir,' even the strongest computing power would be useless.$SanDisk (SNDK.US)$Having risen nearly 50% cumulatively since the conflict began, repeatedly hitting new highs, $Seagate Technology (STX.US)$、$Western Digital (WDC.US)$rose more than 25%,which is the best footnote to this logic.

The rise of large AI language models has not only driven the demand for HBM (High Bandwidth Memory), but also led to an explosive increase in demand for high-capacity mechanical hard drives (HDD) and high-performance enterprise solid-state drives (SSD) in data centers. With the end of the previous industry inventory reduction cycle, these three major storage giantsare now experiencing a 'surge in demand' and 'price recovery,' creating a Davis Double Play, positioning them as high-elasticity leaders of this recovery phase.

Third, The Major Arteries: The 'Water-Seller' Logic of Optical Communications and Network Transmission

The scale of computing clusters is expanding exponentially. However, if data transmission between nodes cannot keep up, expensive GPUs will face a computational bottleneck of 'idle spinning.' In this context, optical communication stands out, with main representatives $Ciena (CIEN.US)$and$Lumentum (LITE.US)$ having risen over 37% and 24%, respectively, since the conflict began.

As leading providers of optical communication components and telecom-grade network transmission equipment, they are truly the 'water sellers' of the AI era. From upgrading optical modules to 800G or even 1.6T, to the expansion of Data Center Interconnect (DCI) architectures,optical network infrastructure has become one of the most certain and fastest-performing sub-tracks in the AI supply chain.

Fourth, The Breakthrough Point: The 'Invisible Winners' of the High-Power Consumption Era

Finally, hidden behind this computational boom is the imminent 'energy and power consumption crisis.' The power consumption of single AI server racks is doubling, making $Monolithic Power Systems (MPWR.US)$ this range of advanced power management chip (PMIC) leaders stand out with a 20% increase.

As a high-growth niche in the semiconductor sector, high-performance analog chips and power management solutions play a crucial 'behind-the-scenes' role in ensuring stable operation and heat control of AI computing components. The market's enthusiasm for $Monolithic Power Systems (MPWR.US)$ demonstrates that exploration of the AI hardware supply chain has moved beyond surface-level computing chips to precision components that address engineering pain points.

Summary:

Looking at the strong recovery following this sharp decline, the market has provided a clear answer:abandon pure speculative hype and return to underlying infrastructure supported by solid performance.

Whether it’s the semiconductor and hardware giants acting as ballast or the storage and optical communication equipment leaders paving the way, these four key areas confirm an indisputable fact—the focus of the global technology industry is irreversibly tilting towards AI infrastructure development. In future investment strategies, adhering to this 'enabler' theme will be key to navigating macroeconomic uncertainty and achieving long-term excess returns.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (18)

to post a comment

90

264