The chip industry has fully entered a price hike cycle, with analog and digital chips leading the rise

Text by Li Zhuang, Edited by Chengcheng

A comprehensive price hike trend in the chip industry chain is being established, especially as recent leaders in analog and digital chips have joined the queue for price hikes. Institutional perspectives are optimistic about leaders in analog chips such as Saint邦 Semiconductor and Naxun Microelectronics.

Since the first quarter of 2026, the global chip industry has officially entered a new round of price hike cycles. Since March, many leading domestic and foreign manufacturers have announced price increases, covering key areas such as wafer foundries, analog chips, memory chips, and CPUs.From Vanguard International Semiconductor Corporation to Texas Instruments and Naxun Microelectronics, the price hike range is generally over 10%. Behind this are rising raw material costs and continued capacity constraints, along with strong demand from downstream sectors like AI servers and automotive electronics driving the surge.

At the same time, profitability in the industry has significantly improved - in 2025, the net profits of the top 10 companies in the semiconductor sector all exceeded 1 billion yuan and achieved year-on-year growth. Gross margins remained high overall, indicating that the chip industry has fully transitioned from the 'inventory reduction' phase into an upward channel of both volume and price increases.

The chip industry enters a price hike cycle

Currently, the chip industry has fully entered a price hike cycle. According to incomplete statistics, since March, over 20 well-known domestic and international chip industry chain companies have announced product price increases. For instance, in the wafer foundry sector, UMC and VIS, among other mature process wafer foundries, reportedly have plans for price increases on some products. VIS intends to raise the processing fees for certain products starting April, with an increase of 15%.

Regarding international firms, Texas Instruments (TI) initiated its second full-scale global price increase starting April 1, with a range of 15%-85%, affecting all customers and core product lines. Analog chip manufacturer MPS issued a price increase notice on March 17, adjusting prices for certain power management and analog chips, with the new pricing effective May 1, 2026. Additionally, according to overseas media reports on March 25, Intel and AMD informed clients of CPU price hikes scheduled for March and April.

In the A-share market, Novosense, a leading company in the semiconductor industry's niche markets, issued a price adjustment notice on March 23,Given the ongoing fluctuations in the global semiconductor market and the significant rise in the costs of core raw materials such as wafers and packaging materials, to ensure stable product quality and continuous supply, and to maintain long-term investment in R&D and services, the company has decided, after careful evaluation, to make appropriate adjustments to the prices of some products soon.

In fact, as early as the beginning of March, Bright Power Semiconductor and ChipSea Technology had already raised their product prices.Products related to SMIC Hai Technology have increased in price by 10% to 20%.The reason for the price increase of these companies' products is consistently attributed to the continuous rise in upstream raw material costs.

Looking at the memory chip industry, which was the first to raise prices and has maintained the trend, data released by the National Development and Reform Commission's Price Monitoring Center on February 28 shows that, as of January this year, the prices of the two main memory chip products, DRAM (memory) and NAND flash, have reached their highest levels since data was available in 2016. Taking mainstream models as an example, the average contract price of DRAM (DDR4 8Gb 1G*8) in January was $11.5, an increase of about 24% from the previous month and approximately 83% higher than September 2025; the average contract price of NAND flash (128Gb 16G*8 MLC) was $9.5, up about 65% from the previous month and nearly 1.5 times higher than September 2025. The rise in memory chip prices is mainly driven by explosive demand growth, a cliff-like shortage of capacity, and panic buying downstream.

The National Development and Reform Commission’s Price Monitoring Center pointed out that, due to the impact of rising memory chip prices and its transmission to downstream sectors, the PPI (Producer Price Index) for computers, communications, and other electronic equipment manufacturing may stabilize after a period of decline, reducing its drag on the overall PPI.

Regarding the price increases of analog chip companies such as Novosense and Bright Power Semiconductor, a recent research report by Open Source Securities noted, 'The core driver behind the current surge in the analog segment, aside from rising costs, includes incremental demand for high-end analog products from AI servers and optical modules. Additionally, tightening foundry capacities may prompt downstream customers to adjust their ordering patterns. Cost pressures coupled with improving demand are expected to strengthen the likelihood of broad-based price increases across the analog sector.'

As for the price hikes in digital chip products, Shenwan Hongyuan recently stated, 'Tight advanced process capacity, stricter yield requirements for packaging, and rising material and logistics costs have driven up the cost structure of high-end CPUs. Meanwhile, leading cloud providers locking in capacity early and allocating resources towards higher profit-density accelerators have constrained short-term supply elasticity for server CPUs. The combined effect of supply and demand fundamentals makes price increases almost an inevitable outcome of industrial adjustment.'

Industry profitability continues to improve.

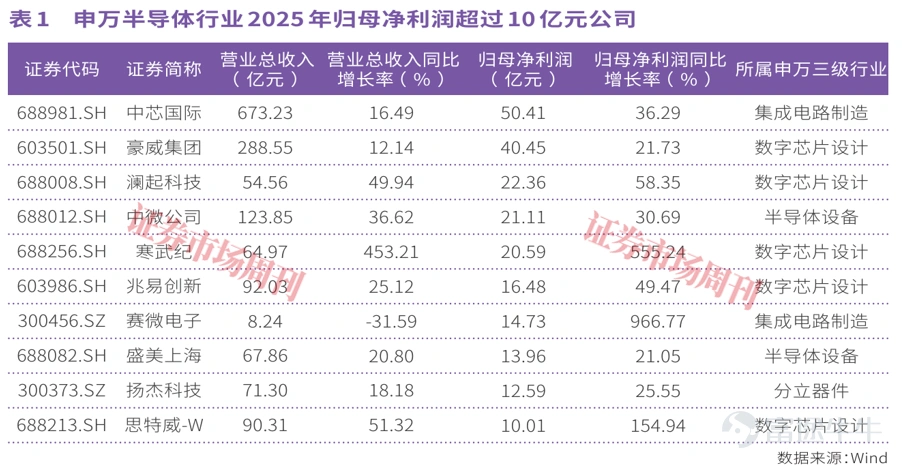

As the entire chip industry enters a price hike cycle, profitability continues to improve. For instance, among companies in the Shenwan Semiconductor sector projected to exceed 1 billion yuan in profits in 2025, there are currently 10 companies expected to surpass 1 billion yuan in net profit attributable to shareholders, all showing year-on-year growth (see Table 1).

Among companies with leading profitability, there are both leading foundries like SMIC and Saiwei Electronics, digital chip design leaders like OmniVision Group, Montage Technology, and Cambricon, as well as semiconductor equipment leaders like Advanced Micro-Fabrication Equipment.For example, OmniVision Group, one of the top ten global fabless semiconductor companies and a Fabless chip design company, achieved operating revenue of 28.855 billion yuan in 2025, growing 12.14% year-on-year, and net profit attributable to shareholders of 4.045 billion yuan, increasing 21.73% year-on-year. Its return on equity (weighted ROE) was 15.39%, up 0.56 percentage points year-on-year. The company is the world's third-largest provider of digital imaging solutions, with products widely covering automotive, smartphones, home security, medical, industrial/machine vision, and emerging markets. It is also one of the few domestic enterprises with both semiconductor R&D design and semiconductor distribution capabilities.

For instance, Montage Technology achieved revenue of 5.456 billion yuan in 2025, representing a year-on-year increase of 49.94%; net profit attributable to shareholders reached 2.236 billion yuan, up 58.35% year-on-year. The company noted that due to the AI industry trend and strong demand in the sector, the shipment volume of its interconnect chips significantly increased, driving a substantial rise in related product sales revenue compared to the previous year.

The rapid growth in performance of the chip industry aligns with robust market demand; however, there are certain differences in gross margin among leading companies in terms of profitability (see Table 2).

Companies like SMIC, OmniVision Group, and Montage Technology have maintained a stable and slightly upward trend in sales gross margin, while companies such as AMEC and Cambricon have experienced some decline. For example, Cambricon’s gross margin in 2025 slightly decreased by 1.56 percentage points to 55.15% compared to 2024.

It is worth noting that the current gross margin levels of leading companies in terms of profitability remain generally high.

Looking at the recent performance of companies that announced product price hikes, such as Fortiori Technology, Novosense Microelectronics, and ChipSea Tech, Fortiori Technology's performance in 2025 declined by 1.54% year-on-year, while Novosense Microelectronics and ChipSea Tech narrowed their losses. In terms of sales gross margin, Fortiori Technology's gross margin in 2025 dropped by 0.67 percentage points to 52.57%, whereas Novosense Microelectronics and ChipSea Tech increased by 2.26 percentage points and 1.05 percentage points respectively, reaching 34.95% and 35.20% (see Table 3).

Novosense Microelectronics noted in its financial report that its operating revenue grew by 71.80% year-on-year, primarily driven by steady growth in demand from the downstream automotive electronics sector, where the company’s related products continued to gain traction; the overall recovery in the broader energy sector, particularly in photovoltaic, energy storage, and industrial automation, where most customers resumed normal demand, and server power customers saw rapid growth driven by AI; the consolidation of Magotan further enriched the company’s product portfolio, contributing positively to this period’s revenue growth and pushing the company’s quarterly operating revenue to continuously climb. The main reasons for the company’s reduced losses were: on the revenue side, the recovery of downstream market demand, new product traction, and the consolidation of Magotan led to significant growth in shipment volume and revenue; on the cost side, the company deepened lean management and organizational efficiency, reducing overall expenses as a proportion of operating revenue, which improved profitability.

Companies like Novosense Microelectronics and SG Micro significantly benefited.

According to TrendForce data, in the fourth quarter of 2025, the average capacity utilization rate of major global wafer fabs rebounded to 90%, with 8-inch processes remaining fully loaded. Open Source Securities believes that the ongoing contraction of 8-inch capacity, relatively stable demand from automotive and industrial control sectors, and the accelerated expansion of the AI industry are driving the analog chip sector towards structural shortages, with comprehensive price hikes expected to follow. Open Source Securities holds a positive outlook for companies such as Novosense Microelectronics, SG Micro, Sino-foreign Joint Venture, Jiehua Technology, and Bright Power Semiconductor.

As one of the leading analog chip design companies, Novosense Microelectronics focuses on three major product categories: sensors, signal chains, and power management, offering a wide range of semiconductor products and solutions widely used in automotive, broader energy, and consumer electronics fields, currently providing over 3,900 saleable product models. In terms of quarterly revenue, as of the fourth quarter of 2025, the company has achieved continuous revenue growth quarter-over-quarter for 11 consecutive quarters, with overall business performance in a rapid growth trend.

In terms of R&D investment, Novosense Microelectronics' R&D expenses in 2025 amounted to 794.6027 million yuan, increasing by 47.15% year-on-year. As of the end of December 2025, the company had 655 R&D personnel, growing by 16.96% year-on-year.

SG Micro, as a leading company in the analog chip sector, also benefits from the industry's upward cycle. According to financial reports, in 2025, SG Micro achieved revenue of 3.898 billion yuan, a year-on-year increase of 16.46%; net profit attributable to shareholders reached 547 million yuan, a year-on-year increase of 9.36%. On a quarterly basis, the company achieved revenue of 1.097 billion yuan in Q4 2025, a year-on-year increase of 21.65% and a quarter-on-quarter increase of 11.78%; net profit attributable to shareholders was 204 million yuan, a year-on-year decrease of 5.35%, but a quarter-on-quarter increase of 43.14%; the gross margin for Q4 2025 was 52.28%, an increase of 2.72 percentage points year-on-year and 1.39 percentage points quarter-on-quarter. This shows that the company has seen a quarter-on-quarter improvement in revenue, profit, and gross margin.

SG Micro is a leading company in China’s analog integrated circuit design industry, with a comprehensive portfolio of analog signal and mixed-signal integrated circuit products covering signal chains, power management, sensors, and memory, among others. The company currently offers nearly 7,000 products across 38 categories, widely used in industrial and energy, automotive, networking and computing, and consumer electronics sectors.

At the same time, SG Micro continues to expand its R&D investment. In 2025, the company's R&D expenses amounted to 1.045 billion yuan, representing an R&D expense ratio of 26.81%. In 2025, the company launched nearly 900 new products with full independent intellectual property rights, covering all major product categories and sub-application areas. The company continuously tracks market developments, actively making relevant technology, intellectual property, and product layouts and reserves. It has already achieved good sales performance in electric vehicles, industrial control, 5G communications, IoT, smart home, wearable devices, drones, and intelligent manufacturing, expanding its customer base.

Everbright Securities believes that SG Micro, as a leading company in the analog chip field, boasts a comprehensive product portfolio and is continually expanding its application areas.As the analog chip industry enters an upturn cycle, the company’s performance is expected to grow rapidly. We are optimistic about the development potential of SG Micro as a platform-based analog chip company and maintain a 'Buy' rating.

In terms of institutional research, from the beginning of this year until April 7, Nasdaq-listed companies Novosense Microelectronics and SG Micro received institutional visits once and twice respectively. Among the 67 sector companies that officially released their 2025 annual reports, a total of 45 companies have received institutional research so far.

(This article was published in the April 11 issue of Securities Market Weekly. The mentioned stocks are for illustrative analysis only and should not be considered investment advice.)

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment