The reevaluation of innovative drug stocks is happening right now—did you get in on this wave?

Outperforming Hang Seng Index by 7%! Southbound capital sweeps HKD 20 billion, is the innovative drug sector entering a 'value reassessment' golden period? | In-depth analysis | Research report | Potential stocks | Pharmaceutical stocks

The innovative drug sector in Hong Kong's stock market has recently performed remarkably, $WUXI APPTEC (02359.HK)$ 、 $WUXI BIO (02269.HK)$ 、 $JOINN (06127.HK)$The performance of key targets in the industrial chain, especially in the innovative drug sector, has been particularly outstanding. Behind the sector's rally is the continuous increase in policy support for the innovative drug field: at the top-level design level, the 2026 government work report, for the first time, listed biomedicine as an 'emerging pillar industry,' marking a historic leap in industrial strategic positioning; on the industry side, the National Medical Products Administration launched a three-year 'Spring Rain Action' aimed at accelerating clinical innovation and commercialization of medical devices, thereby empowering the entire pharmaceutical innovation ecosystem; on the payment side, the 2026 updated National Reimbursement Drug List underwent significant expansion, adding 114 new drugs, with record-high inclusion of Class 1 new drugs both in quantity and proportion, laying a solid payment foundation for the commercial scaling of innovative drugs. The continuous implementation of favorable policies provides strong support, coupled with high global enthusiasm for innovative drug business development (BD) cooperation, which could accelerate the revaluation of Hong Kong-listed innovative drug companies. In this context, which core targets within the innovative drug sector should investors focus on?

Domestic Policy Support and BD Overseas Resonance: Value Reassessment and Investment Opportunities in Innovative Drugs

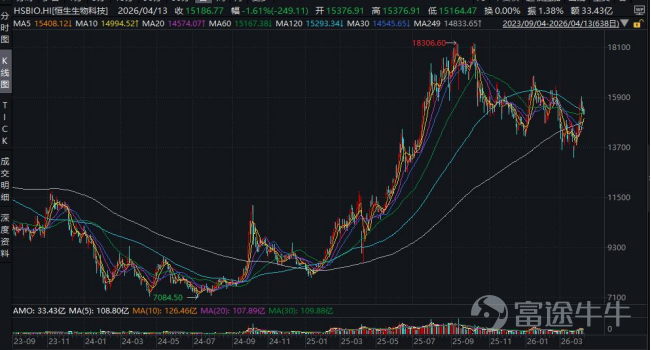

Since the first quarter of 2026, the Hong Kong-listed innovative drug sector has charted an independent upward trend, becoming one of the core themes in the Hong Kong stock market.As of April 10, 2026, the Hang Seng Hong Kong-listed Biotech Index (HSHKBIO) has recorded a cumulative gain of 8.6% since the beginning of the year, outperforming the Hang Seng Index by about 7 percentage points, with significant profit effects in the sector.

Among them, the performance of leading core targets in the industrial chain has been particularly prominent:$WUXI APPTEC (02359.HK)$with a cumulative gain of 29.7% during the period,$WUXI BIO (02269.HK)$and a cumulative gain of 14.1%, both significantly outperforming the sector and the broader market. On the capital front, the sector has seen increased investment from southbound capital: since 2026, southbound capital has cumulatively flowed into the Hong Kong-listed innovative drug sector with over 20 billion Hong Kong dollars,$WUXI APPTEC (02359.HK)$ 、 $WUXI BIO (02269.HK)$ 、 $INNOVENT BIO (01801.HK)$with certain targets consistently ranking high on the list of southbound capital increases; meanwhile, as major Hong Kong-listed biotech companies have shown significant improvement in financial performance, smooth progress in international business, and continued domestic policy support, the sector has delivered relatively strong performance.

Figure 1: Cumulative Year-to-Date Gain of the Hang Seng Hong Kong Biotechnology Index (HSHKBIO)

Source: Wind

Two Sessions Set Tone for Emerging Pillar Industry, Innovative Drugs Enter New Cycle of High-Quality Development

The 2026 government work report, for the first time, listed biopharmaceuticals as an "emerging pillar industry," marking a significant leap in strategic positioning from its previous classification as a "strategic emerging industry." This designation underscores the core role of the biopharmaceutical sector within the national economy and implies that a series of cross-departmental, multi-cycle supporting policies—such as fiscal subsidies, tax incentives, financing support, and industrial park development—will be implemented. The policy certainty for the long-term growth of the industry has significantly improved, effectively removing the ceiling on the domestic innovative drug industry's growth.According to data from the National Medical Products Administration, the number of approved innovative drugs in China reached 76 in 2025, setting a new historical record. Domestically produced innovative drugs accounted for 80.85% of approved chemical drugs and 91.30% of biological products, firmly establishing themselves as the primary drivers of innovative drug listings in China. The field of out-licensing (BD) for innovative drugs also performed exceptionally well, with total licensing amounts exceeding $130 billion USD in 2025. In just the first quarter of 2026, this figure surpassed $60 billion USD, reflecting strong growth momentum. These impressive figures confirm that the high-quality development of China's pharmaceutical innovation industry has entered a phase of full realization.

Figure 2: Out-licensing transaction amounts for innovative drugs in China in 2025

Source: CCTV News

In terms of measures, on March 24, 2026, the General Office of the National Medical Products Administration issued the 'Notice on Launching the "Spring Rain Initiative" for the Transformation of Clinical Innovation Achievements in Medical Devices' (hereinafter referred to as the 'Notice').The Notice emphasizes advancing source innovation in medical devices guided by clinical value, focusing on deep integration between medical engineering and promoting the transformation of more clinical innovations into medical device products. The National Medical Products Administration has decided to implement a three-year "Spring Rain Initiative" nationwide. This policy directly addresses core pain points in innovative drug R&D: on one hand, it significantly shortens the cycle from clinical application to market launch, reducing the time and capital costs for drug companies and increasing R&D returns; on the other hand, it strongly encourages first-in-class (globally pioneering), best-in-class (best in their category) drugs, and innovation in areas such as rare diseases, oncology, and autoimmune diseases with unmet clinical needs, driving the industry to transition from homogeneous competition to "source innovation." This benefits leading companies with genuine R&D capabilities. On the payment side, there is also positive news: the 2026 National Health Insurance Catalog will officially take effect on April 1, adding 114 new drugs (including 50 Class 1 innovative drugs and 36 anti-cancer drugs), bringing the total number of cancer treatments to over 230. Additionally, outpatient reimbursement rates for cancer treatments have been significantly increased, with employee health insurance covering no less than 90% and resident health insurance no less than 80%. Most regions have eliminated deductibles and streamlined dual-channel reimbursements, greatly alleviating the challenges of hospital entry, reimbursement, and payment for innovative drugs, which will directly boost sales of related company products in the short term. This policy reverses the market's pessimistic expectations about "health insurance negotiations drastically compressing the profit margins of innovative drugs": firstly, the health insurance catalog's acceptance of truly clinically valuable innovative drugs has notably increased, achieving "full inclusion," providing payment guarantees for rapid scaling of innovative drugs, and substantially shortening the commercialization period. Secondly, price reductions have slowed, achieving a "volume-price balance," balancing the affordability of the health insurance fund with drug companies' R&D returns, ensuring cash flow and sustained R&D investment capacity for innovative drug companies, creating a virtuous business cycle of "R&D-launch-health insurance scale-up-research again."

Figure 3: 'Notice on Launching the "Spring Rain Initiative" for the Transformation of Clinical Innovation Achievements in Medical Devices'

Source: General Office of the National Medical Products Administration

BD collaborations continue to recover, accelerating value reevaluation of innovative drug companies

Beyond policy benefits, the global recovery in BD (business collaboration) transactions is the core industry logic driving the value reevaluation of Hong Kong-listed innovative drug sectors. From 2025 to the first quarter of 2026, the number of overseas license-out (out-licensing) transactions, total transaction amounts, and upfront payment sizes for domestic innovative drug companies all reached new historical highs, becoming the key catalyst for sector performance.Data shows that by 2025, the number of outbound BD projects for innovative drugs in our country reached 166, with upfront payments growing by over 199% year-on-year. Among these, ADC has become the second-largest transaction type after chemical drugs, emerging as a core driver for our innovative drug exports.

Figure 4: Status of Outbound Licensing Amounts for China's Innovative Drugs

Source: China Pharmaceutical Industry Information Center

From an industry perspective, BD collaborations hold dual significance for the value reassessment of innovative pharmaceutical companies:First, direct cash flow realization to improve corporate fundamentals.Large upfront payments and milestone payments can directly bolster pharmaceutical companies' cash reserves, alleviate R&D funding pressures, reduce operational risks, and minimize equity financing's dilution of shareholder rights while optimizing financial statements.Second, validating global innovation value and reconstructing the valuation system.Licensing partnerships with overseas large pharmaceutical firms essentially serve as authoritative endorsements of the clinical value and global commercial potential of domestically produced innovative drugs, breaking previous market biases against them as being 'homogeneous and lacking global competitiveness.' As license-out deals become routine, the valuation framework for innovative drug companies listed on the Hong Kong Stock Exchange will shift from the traditional PEG valuation model to a universal global biotech valuation approach based on 'pipeline value DCF + commercial cash flows,' leading to a systemic uplift in valuations.

Since 2026, BD collaborations among Hong Kong-listed innovative drug companies have expanded from popular fields like ADC and bispecific antibodies to cutting-edge technologies such as gene therapy, cell therapy, and RNA therapeutics. The counterparties have broadened from small and medium-sized overseas biotech firms to the world’s top 20 large pharmaceutical companies, demonstrating a qualitative leap in the global competitiveness of domestically produced innovative drugs and providing ongoing industrial catalysts for sector value reassessment.Looking ahead to Q2 2026, key events disclosed at industry conferences—such as clinical data progress, major outbound licensing (BD) deals, and breakthroughs in critical technologies—will continue to positively catalyze the pharmaceutical innovation sector. Two of the world’s top oncology academic conferences, the 2026 American Association for Cancer Research (AACR) Annual Meeting and the American Society of Clinical Oncology (ASCO) Annual Meeting, are expected to take place from April 17-22 and May 29-June 3, respectively. Significant clinical results presented during these meetings are likely to act as primary catalysts driving sector momentum.

Which companies should be focused on in the innovative drug sector?

Currently, China's innovative drug sector is in a golden layout period driven by multiple positive cycles including earnings realization, valuation recovery, academic conference catalysts, and industrial policy support. The industry’s prosperity remains on a clear upward trajectory. From a fundamental perspective, the sector has completed the previous phases of valuation bubbles and over-competition, with leading Biotech companies first entering a turning point of profitability and recovery. The trend of major R&D achievements transitioning into commercial value is becoming increasingly evident.In addition, the continuous high growth of overseas licensing deals for innovative drugs brings incremental performance gains, further solidifying the underlying profitability fundamentals of the industry.

From the perspective of market catalysts, a series of top-tier global pharmaceutical academic conferences throughout the year will provide ongoing positive momentum. In addition to the upcoming AACR annual meeting, subsequent key oncology conferences such as ASCO and ESMO will also take place, where cutting-edge clinical progress and breakthrough technological achievements of domestically produced innovative drugs will be unveiled, continuously offering opportunities for sector revaluation and driving momentum. On the payment side, the normalization, refinement, and continuous optimization of National Reimbursement Drug List (NRDL) renewal rules have created a clear and predictable path for commercial scaling of innovative drugs, significantly shortening their market penetration cycle. The rapid expansion of commercial health insurance and the improvement of a diversified payment system have further broadened the payment boundaries for innovative drugs, opening up long-term growth potential for high-value innovations. Meanwhile, supportive industrial policies encouraging pharmaceutical innovation are being implemented, and the efficiency of regulatory review and approval processes for innovative drugs continues to improve. Coupled with the sector’s current relatively low historical valuation levels, there is ample room and certainty for valuation recovery. Multiple positive factors are strongly resonating.Together, these factors are driving China’s innovative drug industry into a comprehensive high-quality development phase, with the sector’s long-term investment value continuing to stand out.

In terms of investment strategy, investors can screen targets based on two main themes:First, CXO leaders with strong global competitiveness and high earnings certainty, which directly benefit from the recovery of domestic innovative drug R&D and global industrial transfer; second, leading innovative drug companies with strong commercial capabilities and clear pipeline monetization, possessing sustained cash flow and R&D investment capacity.:

The absolute global leader in biologics CDMO, with a global market share firmly ranked second and a domestic market share exceeding 60%.The company owns world-leading bispecific antibody, ADC, gene therapy, and cell therapy CDMO technology platforms, with production capacity spanning China, Ireland, the United States, and Germany, providing end-to-end services from drug discovery to commercial production. Benefiting from the recovery of R&D demand driven by favorable domestic innovative drug policies and the long-term trend of global biologics CDMO industries shifting to China,The company has abundant order reserves and extremely strong earnings growth certainty.At the same time, the company continues to expand its overseas client base, with a steadily increasing share of business from emerging technology platforms.Its profitability has been steadily improving, making it a core investment target in the Hong Kong-listed innovative drug sector.。

As a global leader in integrated pharmaceutical R&D CRDMO/CTDMO services, the company covers the entire industry chain from drug discovery, preclinical research, clinical trials to commercial production. It has extremely high client barriers.All of the top 20 global pharmaceutical companies are the company’s core clients.The domestic business benefits from supportive policies for innovative drugs, maintaining rapid growth; overseas operations demonstrate strong resilience, with continuous optimization of order structure and a steady increase in high value-added commercial production.The company boasts excellent cash flow and stable dividends, with highly predictable earnings growth at the forefront of the industry. It also consistently benefits from southbound capital inflows, serving as a key stabilizing asset within the sector.

A leader in China's bispecific antibody market, the company owns a world-leading bispecific antibody technology platform. Its core product, Cadonilimab (PD-1/CTLA-4 bispecific antibody), is the world’s first approved dual immune checkpoint bispecific antibody for cancer treatment, showing stronger-than-expected commercial adoption. After inclusion in national medical insurance, revenue is expected to grow significantly. Several first-in-class bispecific antibody pipelines have entered late-stage clinical trials.Overseas business development and licensing progress has been smooth, demonstrating global commercialization potential.。The company has achieved profitability, with continuously improving cash flow.Entering a positive cycle of 'commercial scaling – R&D investment – pipeline realization.'It is a benchmark enterprise for domestic innovation in the pharmaceutical industry, with significant potential for value revaluation.

The leading company in the domestic ADC sector, its core product HER2 ADC Disitamab Vedotin is the first domestically self-developed ADC drug. Its commercial rollout in the domestic market is proceeding steadily, while overseas rights have been licensed to global ADC leader Seagen.Secured substantial upfront and milestone payments, validating the product's global competitiveness.The company owns an independent intellectual property rights platform for ADC technology, with a pipeline covering multiple popular targets. Multiple products have entered clinical stages, demonstrating continuous pipeline realization capabilities. As the core product benefits from inclusion in national medical insurance and achieves overseas BD milestones,The company’s earnings inflection point is clear, with ample room for valuation recovery.。

Disclaimer: The information provided in this report, or any investment or potential transaction related thereto, is subject to the applicable laws and regulatory requirements of your jurisdiction, and you are solely responsible for compliance with such laws and regulations. The content of this report is for reference only and does not constitute any investment advice. Our company has made every effort to ensure the accuracy of the financial information provided, but assumes no responsibility or provides any form of guarantee for the accuracy, completeness, or effectiveness of all or part of the content. We will not be liable for any errors or omissions. Please also note that securities and virtual asset prices can fluctuate, especially given the extremely high risks associated with virtual assets, and investors should exercise caution and assume investment risks on their own.

———————————————————————

About the author:

Victory Securities - Hong Kong's Leading Virtual Asset Broker

Victory Securities (08540.HK), with over 50 years of history in Hong Kong, is a comprehensive full-service licensed brokerage offering four main business services to retail investors, institutional investors, high-net-worth clients, and enterprises: wealth management, asset management, virtual assets, and capital markets. It has received numerous accolades and essential qualifications in the Asia-Pacific region. In 2023, Victory Securities became the first licensed brokerage in Hong Kong to hold licenses issued by the Securities and Futures Commission for virtual asset trading, advisory, and asset management services. It was also approved by the SFC to provide virtual asset trading and advisory services to retail investors, offering one-stop compliant and legal Bitcoin and Ethereum trading, exchange, and deposit/withdrawal services.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

1

1