Major data releases ahead! Could GDP and PCE trigger market volatility?

[Weekly Market Insights] Collapse of US-Iran talks triggers ongoing market volatility, global capital accelerates repricing

Guide to this week's strategies for the US and Hong Kong markets:

Amid geopolitical tensions, how will the 'reflation' game unfold?

Live Broadcast Alert: At 19:00 tonight, Futu's Chief Investment Research Expert will join you to review this week's market and unlock wealth strategies!

[I. Macroeconomic Observations]

1.1 International Macroeconomics:

US Core CPI unexpectedly cools; when will energy inflation truly be under control?

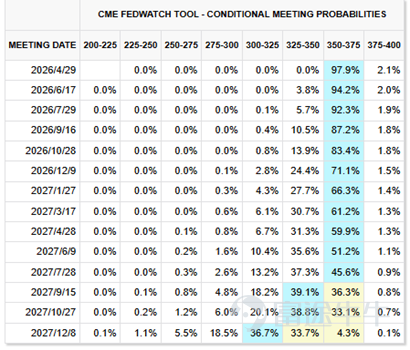

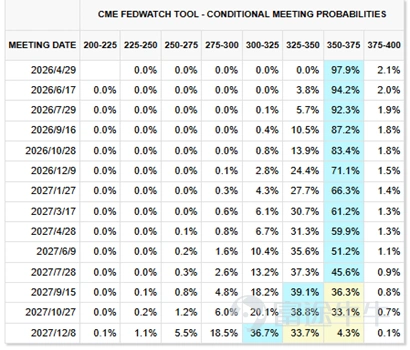

In March, the US CPI rebounded year-over-year to 3.3%, up 0.9% month-over-month, but core CPI fell year-over-year to 2.6%, with a month-over-month increase of 0.2%, below expectations.The inflation structure indicates that energy is the single core driver, with transportation services contributing to an increase of 0.26 percentage points in overall CPI.The substantial easing of inflationary pressures in core services and goods has led to a renewed expectation of interest rate cuts by the Federal Reserve this year.

Figure 1: Fed Watch Implied Rate Cut Pace

The US-Iran negotiations collapsed, with the ceasefire deadline set for April 22. The core issues regarding passage rights in the Strait of Hormuz and enriched uranium remain unresolved,$Brent Last Day Financial JUN6 (BZ2606.US)$High-level volatility. Due to unresolved core geopolitical conflicts,The market is expected to remain volatile until the ceasefire deadline.。

Figure 2: Brent Crude Oil Price (2026/04/12)

1.2 Domestic Macro:

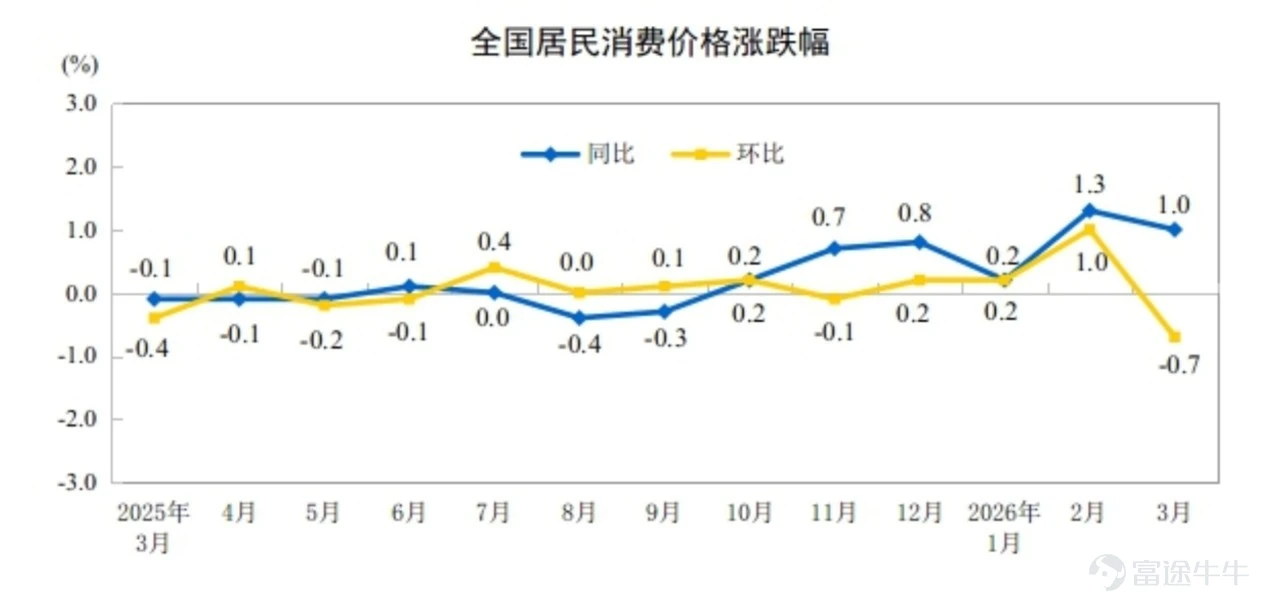

Both China's CPI and PPI have rebounded. Is deflation coming to an end?

In March, PPI increased by 1.0% year-on-year and 0.5% month-on-month, mainly driven by energy; CPI rose by 1.0% year-on-year but fell by 0.7% month-on-month. Deflation expectations have eased somewhat,To further convert this into a benign re-inflation, it still depends on additional policy measures to boost domestic demand,We believe that as uncertainties around the energy impact gradually fade, the likelihood of further policy easing to counteract the economic slowdown is increasing.

The Purchasing Price Index for Raw Materials (PPIRM) surged from 54.8 to 63.9, while the ex-factory price only increased from 50.6 to 55.4,resulting in a gap of 8.5 percentage points between the two.A sharp rise in upstream costs coupled with weak downstream demand suggests that enterprises are facing cost pressures far greater than their ability to pass on such costs.

Figure 3 National consumer price index changes

Figure 4 Producer price index changes for industrial products

[Section Two: Market Views]

2.1 US Stock Market

The Nasdaq rose nearly 5% in a week. Is the worst-case scenario over?

$S&P 500 Index (.SPX.US)$Gains for the entire week.3.56%,$NASDAQ 100 Index (.NDX.US)$Up 4.68%. The expectation of a ceasefire has reduced the probability of the worst-case scenario, oil prices have retreated, but spot gold remains at a high of $4,749 per ounce – the market has not fully exited its geopolitical hedging as the underlying risks have yet to be resolved. Capital has flowed back into technology and risk assets, with divergence occurring after the inflow, favoring leading tech firms with strong earnings visibility, stable balance sheets, and robust cash flow.The Federal Reserve's expectation of maintaining high interest rates throughout the year remains unchanged, with an overall cautious bias toward more hikes.。

The US added 178,000 non-farm jobs in March, with an unemployment rate of 4.3%.The fundamentals of the US have not significantly deteriorated, with earnings still supporting the US stock market, particularly large-cap tech stocks.Moreover, the market maintained stable overall valuation for the S&P 500, with Q1 2026 EPS expected at around $72; while the tech sector's profit margin is expected to grow by approximately 25%, significantly higher than the non-tech sectors.

Figure 5 S&P 500 forward 12-month P/E ratio 20.86 (2026/04/09)

Focus Stocks -$Intel (INTC.US)$: 18A has entered mass production ramp-up. Advanced packaging EMIB/EMIB-T is expected to begin ramping up in the second half of 2026. Market bulls believe external order opportunities may materialize before foundry volume picks up.If investors value the scarcity of advanced manufacturing in the US, Intel remains worth following and holding, anticipating that the valuation narrative will be substantiated and further expand.

The direct catalyst for this round of stock price increase: The Terafab project aims for 1TW annual computing power output, an extremely large scale. Moreover, Intel's management previously mentioned that advanced packaging opportunities at the single-customer level could exceed $1 billion, significantly boosting market confidence in Intel's foundry services monetization path.

Figure 6 INTC forward one-year P/E ratio

Figure 7 INTC forward one-year EV/EBITDA

2.2 Hong Kong Stock Market

The Hang Seng Index rose 3%. Where are the opportunities in Hong Kong stocks?

The Hang Seng Index rose 3.09% for the week, with an average daily turnover of HKD 288 billion (an increase of HKD 18.9 billion compared to last week), and southbound funds accumulated net inflows of HKD 17.1 billion. However, since the outbreak of the war, foreign capital outflows have exceeded HKD 20 billion, with ETFs seeing cumulative net sales of RMB 17.1 billion from March to early April — this rebound was event-driven, not a trend reversal.The forward P/E of Hang Seng Index is only 11.55 times, which is attractive in terms of valuation. However, the conditions for a major uptrend are not yet in place due to continuous foreign capital outflows. Maintain a neutral-to-bullish stance.

If repeated negotiations lead to oil prices rising again above $95-100 per barrel, market preferences will shift towards: pharmaceuticals, banking/finance, high-dividend consumer goods, raw materials/gold, and utilities; technology and aviation will come under renewed pressure. Current recommendations prioritize sectors with high earnings certainty and fully downgraded expectations: healthcare, raw materials, finance.

Figure 8 Hang Seng Index forward 12-month P/E ratio 11.55 (2026/04/10)

Focus Stocks -$INSILICO (03696.HK)$The marginal improvement stems from a significant acceleration in BD activities since 2026. The disclosed collaborations have notably enhanced revenue visibility and reinforced the market's perception of the Pharma.AI platform as commercially viable, replicable, and globally exportable.

Basis for opinion: 1) Rentosertib (ISM001-055) isthe world’s first drug candidate discovered by generative AI and validated through Phase IIa clinical trials; 2) The upfront payment from Eli Lilly and Co is $115 million, with a total deal value of $2.75 billion. BD (Business Development) activities will accelerate comprehensively by 2026, with partners including Eli Lilly and Co, Servier, Qilu Pharmaceutical, and other domestic and international pharmaceutical companies. 3) The target for 2026 is to add 8-10 PCCs annually. Further observation will focus on the pace of BD activities and the progress of Phase III clinical trials.

Figure 9 Insilico Medicine HK Stock Connect holdings percentage and cumulative fund flows

[III. Focus for This Week]

What are the key events investors should focus on this week?

- April 14th / GPT-6 rumored to be released:Code-named Potato, it is rumored to have a 40% performance improvement over GPT-5.4,Supports a context length of up to 2 million tokensinternally positioned as the final 20% push towards AGI. If released and performance meets expectations,it will directly benefit the AI infrastructure chain(computing power, storage, communication services), potentially acting as a short-term catalyst for the Nasdaq index; if delayed, interest in the topic will quickly wane.

- April 16 / China's Q1 GDP and March social retail data:Market expectations for retail sales growth are around 3.5%, and GDP growth is expected to be about 5.0%. Benefiting from strong exports, industrial production is expected to rebound; if the data falls short of expectations, it will strengthen expectations for a policy easing window.favoring the bond market and defensive assets; if it exceeds expectations, it will help restore risk appetite in Hong Kong stock consumption and industrial sectors.

[4. Major bank views]

US Stock Market Summary: Market expectations for S&P 500 1Q26 EPS remain stable. The profit margin for the technology sector is expected to increase from 26.6% in 1Q25 to 29% in 1Q26, with profit growth of approximately 25%, significantly higher than non-tech sectors. The solid earnings base continues to support the US stock market, especially large-cap tech stocks. There is consensus that the technology sector remains the growth engine.Earnings growth will also significantly outperform the broader market.。

Hong Kong stock market summary: If US-Iran negotiations fail, market preference will return to pharmaceuticals, banking/finance, high-dividend consumer stocks, raw materials/gold, utilities, and foreign institutional investors will adopt a barbell allocation strategy: one side beingEnergy security, AI, roboticsHigh-quality growth targets, and the other side beingThe energy sector and high-dividend defensive assets.In the Chinese market,Overweight raw materials, industrials, healthcare, and energy;Underweight discretionary consumption and real estate.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

5