Major data releases ahead! Could GDP and PCE trigger market volatility?

Q1 2026 Review and Q2 Outlook: Market Dynamics and China Opportunities Amid Geopolitical Conflicts

Report Date: April 7, 2026

The first quarter of 2026 has officially concluded. Looking back at the first trading quarter of the year, global capital markets completed pricing amid ongoing tug-of-war between expectations and reality. Since the start of the year, macro trading themes have frequently shifted: expectations for the Federal Reserve’s interest rate cuts have been continuously adjusted; the Bank of Japan ended eight years of negative interest rate policy, completing a historic shift; within the AI sector, profit divergence and logic differentiation emerged while gold prices hit new highs, reflecting declining trust in the global dominant monetary system. Asia-Pacific markets showed valuation recovery supported by policy measures, whereas emerging markets experienced extreme divergence internally. Behind each wave of volatility in Q1 lay the reconstruction of macro logic; within every market trend hid the reshaping of global capital pricing power.

Part One: Q1 2026 Review — Asset Performance Amid Macro Battles

1. Macro Theme: The 'Last Mile' of Inflation and Expectations for a 'Soft Landing' in Growth

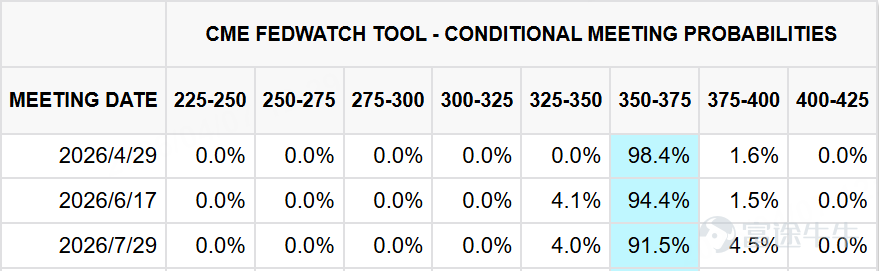

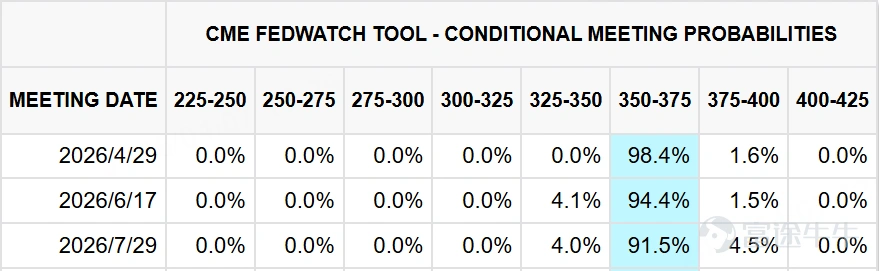

In the first quarter, the core logic of market trading revolved around the pace of global inflation's retreat and whether the economy could achieve a 'soft landing.' Taking the U.S. as an example, although the year-over-year growth rate of CPI has significantly declined from its peak, the stickiness of service sector inflation and wage growth exceeded expectations, leading to continuous postponement of market expectations regarding the timing of the Federal Reserve’s first rate cut. According to the CME FedWatch Tool, as of April 7, the probability of the Federal Reserve raising interest rates by 25 basis points in April was 1.6%, while the probability of maintaining unchanged rates was 98.4%. The probability of the Federal Reserve cutting rates cumulatively by 25 basis points by June stood at 4.1%, maintaining unchanged rates at 94.4%, and cumulatively raising rates by 25 basis points at 1.5%. The U.S. economy overall showed resilience, while risk events in the Middle East triggered concerns about medium- to long-term inflation, collectively influencing rate-cut expectations in the U.S.

[1] Data Source: CME FedWatch Tool (CME Group FedWatch Tool), as of April 7, 2026.

2. Major Asset Performance: Strong Dollar, Divergence in Equity Markets

Against this macroeconomic backdrop, the performance of major assets is as follows:

Equity Market:Significant divergence occurred within global equity markets. In the U.S. market, value stocks and small-cap stocks made a comeback—Russell 2000 Index rose 7.89% in Q1, led by gains in energy and materials sectors; whereas technology growth stocks came under pressure, with Nasdaq falling approximately 7.11% during the quarter and the Mag 7 index dropping 1%. The Hong Kong market exhibited a 'V-shaped' fluctuation, with the Hang Seng Index declining 3.29% in Q1, but the Hang Seng Tech Index plummeting 15.70%. Market logic shifted towards HALO (heavy asset, low depreciation) defensive strategies.

The bond marketGlobal government bond yields moved higher overall due to the delayed rate-cut expectations. For instance, the yield on the 10-year U.S. Treasury bond, which started the year at around 3.8%, continued to climb, reaching 4.32%-4.37% by the end of Q1 2026, putting pressure on bond prices.

Foreign Exchange Market:The US Dollar Index strengthened due to the relative advantage of the US economy and safe-haven demand, with a quarterly increase of approximately 1.43% in Q1 2026, closing near 99.7, putting valuation pressure on non-US assets.

CommoditiesGold remained strong due to geopolitical uncertainties and central bank purchase demands, with Q1 prices oscillating upwards between $4,500-$4,800 per ounce; crude oil prices fluctuated within a range amid supply-demand dynamics, with Brent crude averaging around $58 per barrel.

*Data source: Bloomberg Terminal, as of March 31, 2026. Index performance data sourced from S&P Dow Jones Indices, Nasdaq, and Hang Seng Indexes Company Limited.

Part Two: Focus on China-themed opportunities, highlighting 'resilience' and 'potential' in a turbulent world.

Against the backdrop of global energy shocks triggered by the current Middle East conflict, China has demonstrated stronger macroeconomic resilience compared to most economies. China's economy reflects relative advantages in its energy mix, growth expectation adjustments, and capital market performance.

1. Strong economic growth resilience, with relatively limited impact from the energy shock:

The oil price shock caused by the Middle East conflict has led to downward revisions in growth forecasts for major global economies. However, China’s economy has been less affected due to its diversified energy structure and lower dependence on oil and natural gas. Meanwhile, alternative and renewable energy sources such as nuclear, wind, solar, and hydroelectric power now account for 40% of China's electricity generation, up significantly from 26% a decade ago [2]. Additionally, China's strategic and commercial oil reserves total approximately 1.2 billion barrels, sufficient to support over 110 days of consumption needs in extreme scenarios [2]. These factors collectively enhance China's ability to withstand energy supply disruptions, resulting in a relatively mild impact and bolstering its macroeconomic resilience against external shocks.

2. Attractive valuations for Chinese equity assets, with considerable expected return potential

According to Goldman Sachs report data, some institutions have lowered their 12-month target price for the MSCI China Index by 5% and the CSI 300 Index by 4%, implying potential price returns of approximately 24% and 12%, respectively [2]. Although global stagflation risks have not yet been fully priced in by the market, there is consensus among analysts to maintain an 'overweight' rating on A-shares and H-shares within the Asia-Pacific (ex-Japan) region, considering their risk-return profile remains attractive.

3. A-shares and H-shares demonstrate strong diversification value

Since the outbreak of the Middle East conflict on February 28, 2026, the CSI 300 Index and MSCI China Index have fallen by approximately 4% and 7%, respectively, performing in line with the MSCI Global Index and slightly better than emerging markets excluding China. More importantly, after adjusting for volatility, A-shares and H-shares have significantly outperformed their peers: the Sharpe Ratios over the past month were -0.7 and -0.6, respectively, and their correlation with the S&P 500’s 52-week rolling return was only 0.2 and 0.3 [2]. This low-correlation characteristic gives Chinese assets significant risk diversification value in global portfolios.

4. Favorable liquidity environment in Hong Kong stocks; southbound funds will continue to flow in

The Hong Kong Interbank Offered Rate (HIBOR) has dropped to a seven-month low, and trading volume on the Hong Kong Exchange remains active even after the outbreak of the conflict. The market expects that the inflow of southbound funds will maintain its momentum in 2026, while allocations to Chinese equities by global mutual funds and hedge funds remain at conservative levels. This liquidity landscape provides potential capital support for the Hong Kong stock market and offers ETF investors a good window for allocation.

Against the backdrop of the current global energy shock and rising geopolitical uncertainty, Chinese assets demonstrate stronger macro resilience, more attractive valuations, excellent risk diversification capabilities, and a favorable liquidity environment. For investors in Hong Kong stock ETFs, these factors collectively provide important reference points for focusing on and allocating Chinese equity assets at this stage.

According to the Investment Department of China AMC (HK), generally speaking, during market downturns or periods of turbulence, A-shares tend to outperform Hong Kong stocks.The core reason lies in the fact that the A-share market is predominantly driven by domestic capital, with a relatively stable liquidity environment, making it less susceptible to external market sentiment and capital outflows, thus exhibiting stronger defensive capabilities. However, once the market bottoms out and enters a rebound phase, Hong Kong stocks often show higher elasticity and outperform A-shares. This is mainly because Hong Kong stocks are more sensitive to changes in external liquidity and had previously been more affected by external market pressures, resulting in greater downward adjustments and valuations being pushed to historical lows. Once risk appetite recovers and foreign capital flows back, Hong Kong stocks exhibit stronger rebound momentum. Therefore, in terms of investment timing, A-shares' relative defensive value can be prioritized during turbulent periods, and once bottoming signals become clear, allocations to high-elasticity Hong Kong stocks can be moderately increased.

Source: Morgan Stanley, China AMC (HK), as of December 2025.

Part Four: How to position? Utilize broad-based ETFs for one-click allocation of China's core assets

For investors looking to capture China’s long-term development opportunities while avoiding individual stock risks and the complexities of sector rotation, broad-based index ETFs are an efficient, transparent, and cost-effective tool. China AMC (HK), an asset manager specializing in overseas Chinese investments, offers a series of ETF products covering China’s core assets:

China AMC CSI 300 Index ETF (3188.HK): The China AMC CSI 300 Index ETF (3188.HK) provides investors with a convenient way to allocate core A-share assets via the Hong Kong market. This ETF tracks the CSI 300 Index using a physical replication strategy, directly investing in the 300 largest and most liquid A-share companies listed on the Shanghai and Shenzhen exchanges, representing a broad-based index of the A-share market. The CSI 300 Index covers multiple core industries, including industrials, finance, information technology, and consumption, broadly reflecting the overall performance of China’s mainland economy, making it one of the best options for positioning in the A-share market.

China AMC MSCI China A50 Connect ETF (2839.HK): The China AMC MSCI China A50 Connect ETF (2839.HK) provides investors with a convenient option to allocate core assets of China A-shares via the Hong Kong stock market. This ETF tracks the MSCI China A50 Connect Index, using an innovative industry-neutral approach to select 50 leading stocks from the Shanghai and Shenzhen markets that meet the Connect criteria. It broadly represents the China A-share market, effectively avoiding sector concentration while comprehensively tracking China's economic performance.

The MSCI China A50 Connect Index covers 11 sectors including energy, materials, industrials, consumer, finance, and information technology, making it one of the most representative indices in the A-share market.

China AMC Hang Seng ESG ETF (3403.HK): The China AMC Hang Seng ESG ETF (3403.HK) offers a tool for investors focused on sustainable investing to allocate core assets in the Hong Kong market. The ETF tracks the Hang Seng ESG Enhanced Index, which applies triple screening based on ESG risk ratings, UN Global Compact principles, and involvement in controversial products to exclude companies with high ESG risks or those linked to controversial products. The Hang Seng ESG Enhanced Index covers leading companies across various industries such as finance, technology, consumer, and real estate in Hong Kong, making it an excellent choice for gaining exposure to Hong Kong’s overall economy with an ESG investment philosophy.

The current market faces both short-term disruptions caused by geopolitical conflicts and structural opportunities arising from China’s long-term economic transformation. Through diversified allocation in broad-based ETFs, investors can:

– Diversify risk: Allocate across markets (A-shares, Hong Kong shares) and styles (value, growth) to smooth out volatility in a single market or sector.

– Capture key themes: Fully cover both the “traditional pillars” and “innovative future” of China’s economy, ensuring no missed opportunities for recovery or growth.

– Address uncertainty: When macroeconomic prospects are unclear, holding an index representing the best collection of Chinese companies is a more prudent way to participate in the long term than betting on a single sector.

Conclusion:

In Q2 2026, the market may not be smooth sailing, but the most severe phase of macro shocks might be passing. For investors, rather than trying to predict every short-term fluctuation, it is better to return to the essence of investing: deploying low-cost, transparent broad-based ETFs to position in core assets tied to long-term economic growth where valuations appear attractive.

Report Date: April 7, 2026.

References

1. CME Group. (April 7, 2026).CME FedWatch Tool - Interest Rate Probability for 2026. Retrieved from https://www.cmegroup.com/trading/interest-rates/countdown-to-fomc.html

2. Goldman Sachs Global Investment Research. (March 2026). 10 reflections so far on the Mideast oil shock (China Musings Series).

3. The market data, case studies, and industry observations mentioned in this article are for illustrative purposes only. They are sourced from public media reports and industry research and do not constitute investment advice.

$HSTECH (LIST91332.HK)$$XIAOMI-W (01810.HK)$$Hang Seng Index (800000.HK)$$S&P 500 Index (.SPX.US)$$CBOE Volatility S&P 500 Index (.VIX.US)$$Hang Seng TECH Index (800700.HK)$$Contemporary Amperex Technology (300750.SZ)$$Hang Seng China Enterprises Index (800100.HK)$$SSE Composite Index (000001.SH)$$CSI 300 Index (000300.SH)$$NVIDIA (NVDA.US)$$Amazon (AMZN.US)$$Alphabet-C (GOOG.US)$$Meta Platforms (META.US)$$Tesla (TSLA.US)$$Hang Seng Index (800000.HK)$$SSE 50 Index (000016.SH)$$CSI 300 Index (000300.SH)$$CSI 1000 Index (000852.SH)$$SSE Science and Technology Innovation Board 50 Index (000688.SH)$$ChinaAMC CSI 300 Index ETF (03188.HK)$$SSE Composite Index (000001.SH)$$JD.com (JD.US)$$TENCENT (00700.HK)$$Shenzhen Component Index (399001.SZ)$$Kweichow Moutai (600519.SH)$$PING AN (02318.HK)$$Alibaba (BABA.US)$$ICBC (01398.HK)$$CHINA MOBILE (00941.HK)$$ABC (01288.HK)$$Midea Group Co., Ltd (000333.SZ)$

Investing involves risks, including the loss of principal. Past performance is not indicative of future results. Before investing in the China AMC CSI 300 Index ETF (the "Fund"), investors should read the fund prospectus, paying particular attention to the risk factors. You should not rely solely on this material to make investment decisions. Please note:

• The Fund aims to provide investment returns that closely track the performance of the CSI 300 Index ("the Index") (before fees and expenses). The Fund invests in the China domestic securities market through the fund manager’s RQFII and Stock Connect programs.

• Since the Fund tracks the performance of a single region (China), it faces concentration risk, and its volatility is likely to exceed that of funds with broader regional coverage.

• The Fund is exposed to risks associated with the RQFII system, such as changes in rules and regulations, default by Chinese brokers or the Chinese custodian in executing or settling trades, and restrictions on repatriation of funds.

• The Fund faces risks related to Stock Connect, such as changes in rules and regulations, quota limits, and suspension of the Stock Connect mechanism.

• Investing in China involves higher political, tax, economic, foreign exchange, liquidity, legal, and regulatory risks.

• The market prices of fund units traded on the Hong Kong Exchange in different currencies may vary significantly due to various factors. Therefore, the amount investors pay when purchasing or selling fund units in HKD or USD on the Hong Kong Exchange may exceed what they would pay or receive for units traded in RMB, and vice versa.

• When the Shanghai and Shenzhen stock exchanges are open for trading, the Fund's units may not yet be priced, so the value of securities within the Fund's portfolio could change on days when investors cannot trade the Fund's units. Differences in trading hours between the Shanghai, Shenzhen, and Hong Kong Exchanges, along with trading restrictions on A-shares, may widen the premium/discount level of the unit price relative to its net asset value.

• The Fund is denominated in RMB. The RMB is currently not freely convertible and is subject to foreign exchange controls and restrictions. Investors whose base currency is not RMB are exposed to foreign exchange risk.

• This fund involves securities lending transaction risks, including the possibility that borrowers may not return the securities on time or even at all.

• Dividend distributions paid out of capital or effectively out of capital are equivalent to returning or withdrawing part of an investor's original investment amount or the capital gains attributable to that amount. Any such distribution may result in an immediate reduction of the fund's net asset value per unit.

• The Fund may be exposed to tracking error risk.

• This Fund is not 'actively managed', and therefore, the value of the Fund may decrease as the index declines.

• Generally, retail investors can only buy and sell the fund units of this fund on the Hong Kong Stock Exchange, and the trading price of the fund units on the Hong Kong Stock Exchange is influenced by market factors such as supply and demand for the fund units. Therefore, the trading price of the fund units may trade at a significant premium or discount to the fund’s net asset value.

Investment involves risks, including the potential loss of principal. Past performance is not indicative of future results. Before investing in the China AMC MSCI China A50 Connect ETF (the "Fund"), investors should refer to the fund prospectus and carefully review the risk factors. You should not solely rely on this material for making investment decisions. Please note:

• The Fund’s investment objective is to provide investment returns that closely track the performance of the MSCI China A50 Connect Index (the "Index") (before fees and expenses).

• The Fund is passively managed. A decline in the Index is expected to result in a corresponding decline in the value of the Fund.

• The Fund invests in equity securities and is subject to general market risks. Its value may fluctuate due to various factors.

• Since the index is a new index, this fund may face higher risks compared to other exchange-traded funds that track indices with longer operational histories.

• The Fund faces concentration risk in a single region (Mainland China), which may likely experience greater volatility than broader funds.

• The Fund is subject to risks associated with the Shanghai-Hong Kong Stock Connect, such as changes in rules and regulations, quota limits, or suspension of the Stock Connect mechanism.

• This fund involves securities lending transaction risks, including the possibility that borrowers may not return the securities on time or even at all.

• The Fund is denominated in Renminbi (RMB). RMB is currently not freely convertible and is subject to exchange controls and restrictions. Investors in fund units whose base currency is not RMB are exposed to foreign exchange risk.

• Since the units of the Fund listed on the Hong Kong Exchange may not yet be priced when the Shanghai and Shenzhen stock exchanges open, the value of securities within the Fund’s portfolio may fluctuate on days when investors cannot buy or sell Fund units. Time zone differences between the Shanghai, Shenzhen, and Hong Kong Exchanges, along with trading restrictions on A-shares, could widen the premium/discount level of the Fund’s listed units relative to its net asset value.

• Listed and unlisted classes follow different pricing and trading arrangements. Due to varying fees and costs, the net asset value per unit of each class may differ. The trading hours for listed classes on the secondary market as set by the Hong Kong Exchange differ from the trading cut-off times for listed or unlisted classes in the primary market.

• Units of the listed class are traded at the current market price on the secondary market, while units of the non-listed class are sold through intermediaries based on the end-of-day net asset value. Non-listed class investors can redeem their units at net asset value, whereas secondary market investors of the listed class can only sell at the prevailing market price and may have to exit the Fund at a significant discount. Investors in the non-listed class may have advantages or disadvantages compared to those in the listed class.

• The trading price of listed classes is influenced by market factors such as the supply and demand for fund units. Therefore, the trading price of fund units may be at a significant premium or discount to the net asset value of the fund.

• This fund involves tracking error risk.

• If cross-counter transfers of listed fund units between two counters are suspended, and/or due to any restrictions on the services provided by securities brokers and Central Clearing System participants, unit holders will only be able to trade their fund units on one counter. There may be significant deviations in the market prices of listed fund units traded on different counters.

• Fund unit holders will only receive distributions in Renminbi. Fund unit holders without a Renminbi account may incur fees and expenses associated with foreign exchange conversion.

• The Fund may, at its discretion, pay dividends out of its capital or effectively out of capital. Paying distributions out of capital or effectively out of capital amounts to returning or withdrawing part of an investor's original investment or any capital gains attributable to that original investment. Any such distribution may result in an immediate reduction in the Fund’s net asset value per unit.

Investing involves risks, including the loss of principal. Past performance is not indicative of future results. Before investing in the China AMC Hang Seng ESG ETF (the "Fund"), investors should refer to the fund prospectus, paying particular attention to the risk factors. You should not rely solely on this material to make investment decisions. Please note:

• The Fund's investment objective is to provide investment returns that closely track the performance of the Hang Seng ESG Enhanced Index (the "Index") (before fees and expenses).

• The Fund is passively managed. A decline in the Index is expected to result in a corresponding decline in the value of the Fund.

• Investing in equity securities exposes the Fund to general market risks. Its value may fluctuate due to various factors.

• As the Index is a new index, the Fund may face higher risks compared to other exchange-traded funds that track indices with longer operating histories.

• The Fund is exposed to concentration risk in a single region (Greater China), and its volatility is likely to exceed that of more broadly diversified funds.

• This fund is exposed to risks related to ESG, such as the impact of ESG screening criteria on investment performance, ESG concentration, incomplete, inaccurate, or lack of ESG data and assessments, and the absence of standardized ESG classification.

• This fund involves securities lending transaction risks, including the possibility that borrowers may fail to return the securities on time or even at all.

• Listed and unlisted classes follow different pricing and trading arrangements. Due to varying fees and costs, the net asset value per unit of each class may differ. The trading cut-off times for listed and unlisted classes differ. The trading hours for listed classes on the secondary market as set by the Hong Kong Exchange also differ from the trading cut-off times for listed or unlisted classes in the primary market.

• Listed class fund units are traded on the secondary market at the current market price, while unlisted class fund units are sold through intermediaries based on the end-of-day net asset value on the trading day. Investors in the unlisted class can redeem their units at net asset value, whereas investors in the listed class on the secondary market can only sell at the prevailing market price and may have to exit the Fund at a significant discount. Investors in the unlisted class may have advantages or disadvantages compared to investors in the listed class.

• The trading price of listed fund units is influenced by market factors such as the supply and demand for fund units. Therefore, the trading price of listed fund units may be at a significant premium or discount to the net asset value of the Fund.

• This fund involves tracking error risk.

• If cross-counter transfers of listed fund units between various counters are suspended, and/or due to any restrictions on the services provided by securities brokers and Central Clearing System participants, unit holders will only be able to trade their fund units on one counter. There may be significant deviations in the market prices of listed fund units traded on different counters.

Unit holders will only receive distributions in Hong Kong dollars. Unit holders without a Hong Kong dollar account may have to bear the costs and expenses associated with foreign exchange conversion.

• This fund may, at its discretion, pay dividends from the capital of the fund or actually from the capital. Paying distributions from the capital or effectively from the capital amounts to returning or withdrawing part of the fund unit holder’s original investment or any capital gains attributable to that original investment. Any such distribution may result in an immediate reduction in the net asset value per unit of the fund.

Risk Warning:

Investment involves risks, including possible loss of principal. Past performance is not indicative of future fund returns. This document is for your reference only and does not constitute an offer or solicitation for the purchase or sale of any securities or funds, nor does it constitute any investment advice, nor is it prepared for any such offer. The publisher of this material is China AMC (HK) Limited. This material has not been reviewed by the Securities and Futures Commission of Hong Kong.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

1

2