"AI Bottleneck Trade" Ignites Upstream Sector—Who’s Raking in the Profits?

The Next Frontier in the Computing Power Boom: Tech Giants Ramp Up DCI Deployments—Key Players on Hong Kong and U.S. Stock Markets Deserve Close Attention!

While the market's attention remains fixed on GPU iterations, a "transmission" revolution driven by "computing power" has already begun to unfold quietly.

As the global AI large-model race enters a white-hot phase, the bottleneck in infrastructure is shifting. Dongwu Securities points out that,DCI (Data Center Interconnect) represents post-cycle demand for AI computing power infrastructure.As multiple data centers seek to achieve interconnection across campuses, regions, and even continents, the demand for long-distance connectivity is expected to gradually emerge.

So what exactly is DCI, and why has it emerged as one of the most certain investment themes for 2026? Which key players in the Hong Kong and U.S. stock markets are worth watching? This article will break it all down for you.

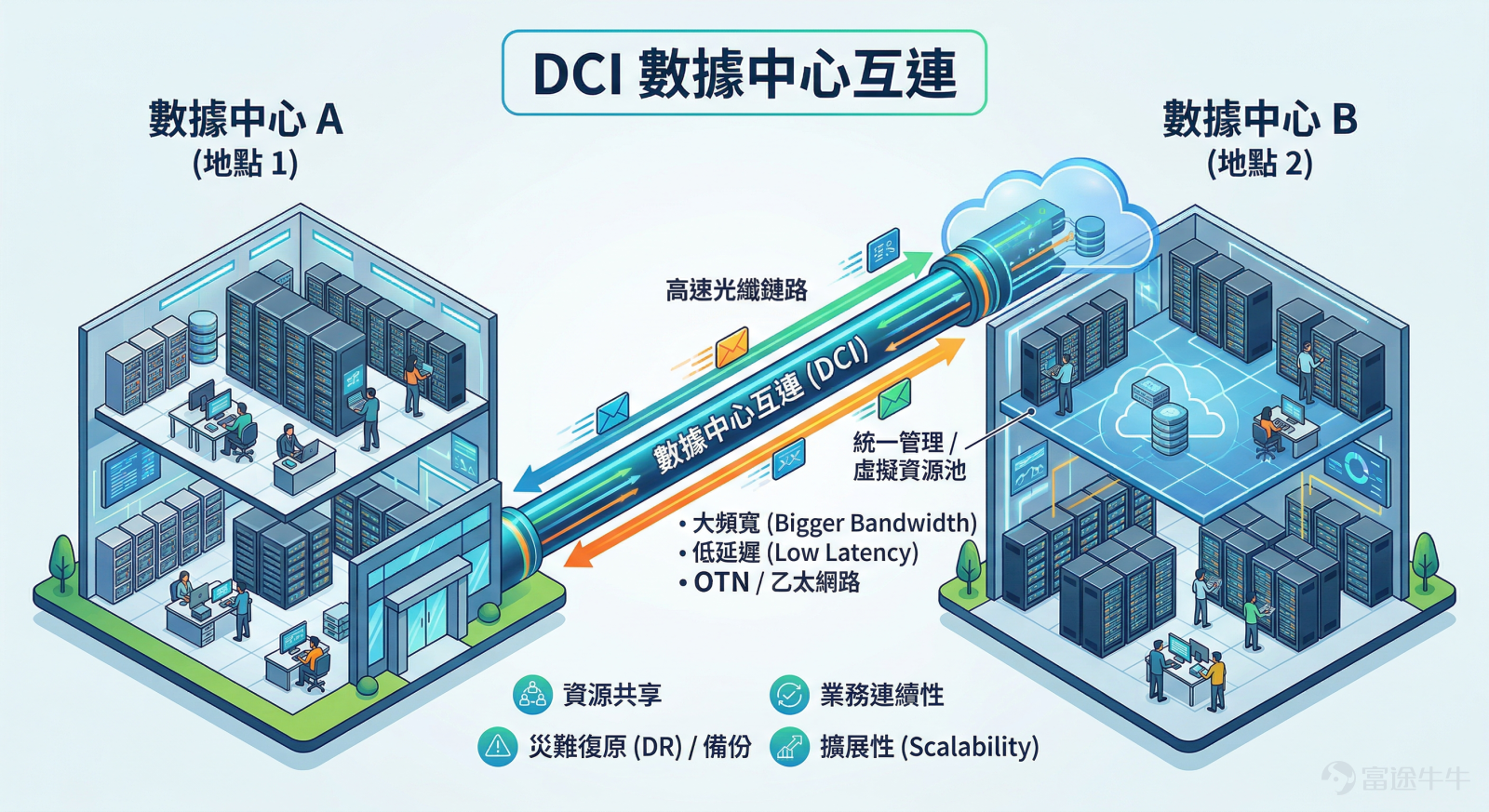

What exactly is DCI?

Data Center Interconnect (DCI) is a networking solution that enables interconnection and communication across data centers, primarily to support data exchange, disaster recovery and redundancy, and content delivery among geographically dispersed data centers.

If we compare a single data center to aThe "superbrain" is packed with GPUs and servers, while DCI (Data Center Interconnect) serves as the "neural network" or "high-speed railway" that connects these brains.。

It is a networking technology solution specifically designed to connect two or more physically separate data centers—whether they are just across the street from each other or located on opposite sides of the Pacific—enabling them to operate in concert as a single, unified resource pool.

Why is DCI now entering a supercycle? The core reason is that AI computing power has hit a wall:

1. Single-point computing power has reached its limit: Training large models today often requires clusters of tens of thousands—or even hundreds of thousands—of GPUs. No single data center can possibly support such a massive heat-generating behemoth, given the constraints on power supply, physical space, and cooling capacity.

2. From "Centralization" to "Decentralization": Since it's impractical to cram 100,000 cards into a single data center, tech giants adopt the following approach: they build several data centers in different locations, and thenConnect them using DCI to enable "distributed training."。

To enable instantaneous, lag-free transfer of massive amounts of data among GPUs in different data centers, DCI must possessUltra-wide bandwidth(DWDM Dense Wavelength Division Multiplexing technology) andUltra-long-distance transmission with extremely low latency(Coherent Optical Technology).

In other words,Without DCI, the computational scale of large AI models cannot continue to expand. It has evolved from a mere "backup option" in the past to an "essential enabler" for scaling today.

Why will DCI become one of the main investment themes for 2026?

If, over the past two years, the AI arms race among tech giants was still mired in a numbers game centered on vying for GPU computing power and model parameters, then with the arrival of 2026, the battle has now escalated to the more fundamental physical infrastructure—building the "information superhighway" that connects isolated data-center computing silos. According to the latest industry data, major players have already committed significant capital, making 2026 a landmark year for large-scale DCI equipment procurement.

According to market reports, the total tender volume for DCI in North America in 2026 is expected to reachUS$15 billion to US$16 billion, representing a substantial increase of approximately 50% compared with 2025.

$Alphabet-C (GOOG.US)$: The DCI equipment tender was completed in Q1 2026, with a contract value of approximately USD 6 billion, to be executed over 2–3 years; centralized deliveries are expected to commence in H2 2026 and continue for another 2–3 years.

$Microsoft (MSFT.US)$: The DCI tender is scheduled to launch in Q2 2026, with a total value of approximately USD 6 billion, and is expected to be completed over two years; deliveries will begin in H2 2026, and 2027 will mark the peak of deployment.

$Meta Platforms (META.US)$: The DCI tender is scheduled to be launched in H2 2026, with a contract value of approximately USD 2–3 billion; delivery is expected to commence by the end of 2026, followed by a centralized deployment phase in 2027.

$Amazon (AMZN.US)$: The DCI tender is scheduled to launch in H2 2026, with a contract value of approximately USD 2.5–3.0 billion, and full delivery and deployment are expected to be completed over a two-year period.

With a budget exceeding US$10 billion gradually being implemented, 2026 is expected to drive a comprehensive scaling-up of the entire DCI industry chain.

Which core players in the Hong Kong and U.S. stock markets are worth watching?

The DCI industry chain features extremely high technological barriers, and multi-billion-dollar orders from industry giants will cascade up the value chain from downstream to upstream. The following are key Hong Kong- and U.S.-listed players that warrant close attention:

Among them,Most importantly, the downstream segment—DCI transmission and switching equipment—is the ultimate winner, reaping tens of billions in orders.

This is the most profitable segment in the entire DCI industry chain. The multi-billion-dollar capital expenditure expansions by tech giants are first and most directly reflected in the order books of these equipment vendors. Currently, the North American market is highly concentrated.Oligopolistic structure (Ciena, Nokia, and Cisco account for 80%-90% of the market share), and is currently alongTwo Major Technological ApproachesEngage in fierce competition:

Camp One: Proprietary DCI Transmission Systems (the core business of traditional optical transmission giants)

Primarily serves long-distance data center interconnections that require ultra-high stability and dedicated, direct connections.

$Ciena (CIEN.US)$— Absolute leader:It consistently holds the top market share in North America (about 40%-45%). As a giant in the pure optical communication network industry, CIEN is the unshakable first choice when major companies such as Meta and Amazon need to establish dedicated lines to connect data centers, with an extremely stable core business.

$Nokia Oyj (NOK.US)$—The strongest dark horse in the revaluation of value:Following its acquisition of leading optical communications vendor Infinera, the company's market share has surged to 20%–30%, closing in on Ciena. Notably, the market expects Nokia to have secured a massive 50%–60% share of Google's Q1 2026 procurement tender, making it the core stock with the greatest earnings elasticity in this round of bidding activity.

$ZTE (00763.HK)$— Domestic computing power foundation:A giant in China's telecommunications equipment and transmission network sector, it is a key player in shaping the country's domestic computing power network infrastructure.

Camp Two: IP over DWDM (a disruptive, high-growth new force that is upending tradition)

Core trends:By abandoning traditional, bulky DCI transmission boxes and instead "plugging" coherent optical modules directly into network switches, data center physical space and power consumption are dramatically reduced—making this a hot trend in the AI era.

$Arista Networks (ANET.US)$—The King of Cloud Switches:It is the undisputed core driver of IP over DWDM. Leveraging its technological advantages, the company has secured a substantial number of AI backend network orders—such as GPU cluster interconnects—making it the standout AI networking stock in recent years.

$Cisco (CSCO.US)$—The giants' defensive counterattack:It holds a 10%–20% share of the North American DCI market. To fend off disruptors, Cisco made a hefty acquisition of optical coherence giant Acacia, and now it offers a complete IP over DWDM solution spanning "chip → module → router."

$Hewlett Packard Enterprise (HPE.US)$—Enterprise-level market predator:A traditional IT infrastructure giant has recently made a bold entry into the fray by acquiring Juniper Networks, a long-established networking powerhouse, with the aim of capturing a share of the enterprise AI connectivity market.

Meanwhile, the upstream segment—optoelectronic core chips and underlying foundational hardware—acts as the "water seller" with deep competitive barriers, representing the link with the highest technological hurdles and the most substantial profit margins.Specifically:

1. Core Chip for Computing Power Optoelectronics

$Broadcom (AVGO.US)$It is the undisputed leader in network chips.In AI networks, its Tomahawk and Jericho series of switching chips are indispensable. At the same time, the company has made extensive investments in silicon photonics, making it the most certain beneficiary of the expansion of AI computing power networks.

$Marvell Technology (MRVL.US)$It has formed a duopoly with Broadcom.It is the leading provider of electro-optical conversion DSP (digital signal processor) chips; whenever DCI requires high-speed, long-distance electro-optical signal conversion, MRVL's chips are virtually indispensable. Within Marvell's extensive technology portfolio, data center interconnect modules play a critical role, primarily used for data transmission across regional fiber-optic networks.During the earnings call, Matt Murphy, Chairman and CEO of Marvell, outlined the company's progress, noting that it is securing new customers and expects to supply DCI modules to all five of the largest hyperscale cloud service providers in the U.S. this year.

$POET Technologies (POET.US)$This is a relatively cutting-edge player. Its core technology is the "optical interposer," which enables seamless integration of electronic and photonic components. With a smaller market capitalization, it is a high-potential, high-volatility stock offering attractive upside potential.

2. Core Optical Components and Passive Network Elements

$Coherent (COHR.US)$& $Lumentum (LITE.US)$These two companies are global leaders in laser and optical-component supply. DCI transmission requires light emission, and they are the leading providers of core light sources, such as VCSELs and EML laser chips. They also boast end-to-end vertical integration and manufacture midstream modules.

3. Physical Layer Testing and Network Monitoring

$Keysight Technologies (KEYS.US)$& $Viavi Solutions (VIAV.US)$:The "quality inspectors" and "toll booths" of the digital world. Before cloud giants invest billions of dollars in building DCI networks, these networks must undergo rigorous testing and validation. Keysight's business spans a broad range of electronic testing, while Viavi specializes more in fiber-optic networking and communications testing. This year, the stock prices of these two companies have risen by 50% and 116%, respectively.

4. Fiber Optic Cables (Physical Transmission Medium)

$Corning (GLW.US)$YesA century-old materials giant and the founder of global fiber-optic technology. DCI networking essentially requires the deployment of massive fiber-optic networks, and Corning is the leading infrastructure player that directly benefits from this trend. Its share price has risen by 70% so far this year.

$YOFC (06869.HK)$It is the leading domestic fiber-optic cable manufacturer, and its share price has surged by as much as 330% this year. Not only is it firmly benefiting from the infrastructure dividends brought about by major players' expansion and the "East Data, West Computing" initiative; more noteworthy is its forward-looking deployment in the next-generation"Hollow Fiber"Advanced technologies can bring optical signal transmission close to the speed of light in a vacuum, reducing latency by more than 30%. Hollow-core fiber, as a key technological solution for DCI networks, boasts significant technical advantages and substantial market potential, with its commercialization expected to accelerate markedly in the coming years.

5. Specialty Foundry Services for Bottom-Level Wafers

$Tower Semiconductor (TSEM.US)$It is the hidden champion in the optical communication field. DCI transmission requires analog signal conversion at extremely high frequencies, which depends on semiconductor materials such as SiGe and BiCMOS processes. Tower is one of the world's leading foundries specializing in these advanced analog processes. Many networking chip design giants, such as Broadcom and Marvell, rely on such specialized process fabs to manufacture their optoelectronic conversion chips.

The midstream—high-speed coherent optical modules and advanced manufacturing—functions as an "assembly plant" that sells the tools of the trade. The core technology underpinning DCI inter-region transmission is "coherent optics," which ensures that optical signals can travel thousands of kilometers without distortion.Specifically,

1. High-Speed Coherent Optical Module

$Coherent (COHR.US)$ & $Lumentum (LITE.US)$:Leveraging their advantages in upstream components, they also hold a significant position in the high-end coherent optical module market.

$Applied Optoelectronics (AAOI.US)$:In the past few years, its stock price has been highly volatile. Recently, it has been actively transforming into high-speed modules such as 400G/800G and entering the supply chains of major manufacturers such as Microsoft. It is a stock with great elasticity, but risks should also be noted.

$FIT HON TENG (06088.HK)$: The company's core competitive advantage in the DCI field lies in "its vertical integration and dominant precision mass-production capabilities, backed by the Hon Hai Group."It not only boasts mass-production capabilities for high-speed optical modules ranging from 800G to even 1.6T, coupled with advanced copper interconnect technologies, but also benefits directly from its parent company's leading global market share in AI server and networking equipment ODM manufacturing. This enables rapid internal validation and bundled shipments of optoelectronic modules, creating an ecosystem moat that is hard for other independent module manufacturers to match in translating cutting-edge technology into large-scale, low-cost, and predictable revenue performance.

2. Advanced Optoelectronics Foundry

$Fabrinet (FN.US)$:Taiwan Semiconductor in the optical communications field. The packaging and manufacturing of optical modules are extremely complex and yield-dependent, so many major European and American optical manufacturers (such as Cisco/Acacia) outsource their manufacturing to FN. Its performance visibility is very high, and it has a deep competitive moat.

Summary

Global AI infrastructure is undergoing a paradigm shift from "single-point computing power expansion" to "a global transmission revolution." 2026 is expected to be the "first year of performance realization" when DCI orders are fully implemented. While capitalizing on the sector's highly certain growth, fellow investors are advised to remain rational and continuously monitor potential variables such as reductions in major players' capital expenditures, disruptive effects of new technologies, geopolitical competition, and high valuation premiums.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (5)

to post a comment

107

386