Tesla may double down on affordable SUVs! Can a strategic shift save its stock price?

Option Sir Breaks Down Hot Topics | JPMorgan Reiterates Bearish Stance, Negative Factors, Rebound and Long-Term Narrative: How to Evaluate Tesla Before Earnings?

Yesterday, due to a notably bearish report from JPMorgan and the uncertain situation between the US and Iran, $Tesla (TSLA.US)$ the market once dropped over 4% during trading hours, but recovered much of the losses by the close, ending at -1.75%; after-hours, it rebounded more than 4% as tensions between the US and Iran eased, boosting market risk appetite.

In fact, JPMorgan has largely remained on the cautious, bearish side in recent years, merely adjusting its target price and revising down earnings forecasts at different stages.This time, it simply reinforced its cautious stance based on the latest developments.

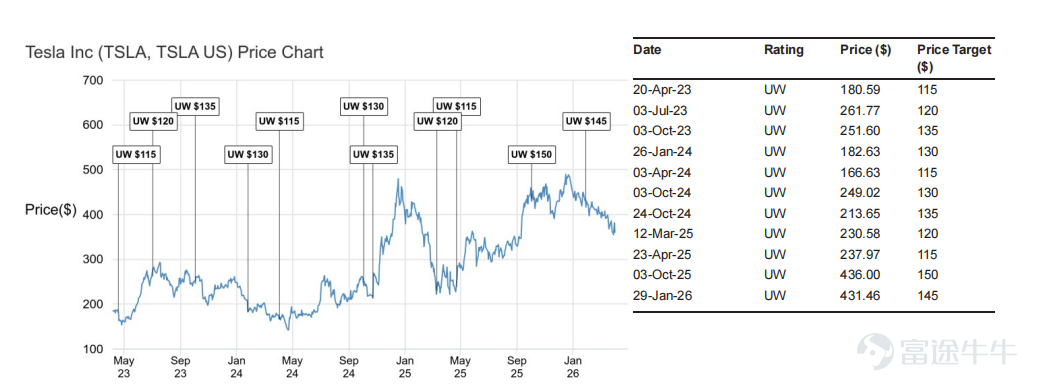

Since the beginning of the year, Tesla’s shares have fallen 22%, weighed down by both geopolitical risks and fundamental pressures, showing weak performance. Analyst ratings from major banks show target prices ranging from $125 to $600, reflecting the pricing tug-of-war between short-term results and long-term strategy. Tesla is being repeatedly reassessed amidst high volatility.With the earnings report scheduled for release on April 22, this article will provide background information for investors by synthesizing recent key bullish and bearish perspectives from major banks regarding Tesla.

What did JPMorgan get right in this report, and where might they be too harsh?

The report indeed pointed out some of Tesla's current challenges:

First, near-term fundamentals are indeed weak, with the automotive core business yet to truly stop the bleeding.

Tesla Delivered 358,000 units in Q1 2026, lower than Bloomberg consensus expectations of 372,000 units;

In addition to the vehicle business, the previously high-growth energy storage segment also underperformed expectations. Energy storage installations in Q1 were only 8.8GWh, down 15% year-over-year, marking the first YoY decline since 2022 and nearly 40% below market consensus.

Second, inventory and cash flow pressures are mounting.

The company produced 408,000 vehicles in Q1, delivered 358,000, adding over 50,000 to inventory. By the end of Q1, total unsold vehicle inventory reached 164,000 units, up 80% from the same period last year. Excess inventory will further exacerbate the company’s free cash flow pressure. Coupled with plans to double capital expenditures to over $20 billion this year, short-term cash flow stress is becoming evident. Moreover, Tesla’s CFO noted during the Q4 2025 earnings call thatThe capital expenditure guidance for 2026, which exceeds 20 billion US dollars, does not include investments in Terafab or solar cell manufacturing;Free cash flow for 2026 is expected to be negative。

Third, the valuation has decreased, but it is still not considered cheap

Tesla's stock price has indeed retreated from its peak, but according to HSBC's calculationsOver the past four years, only 9% of trading volume occurred at a higher valuation than the current level, in other words, Tesla remains relatively expensive even after the pullback; on Tuesday Eastern Time, Goldman Sachs made a rare statement pointing out that the relative performance of tech stocks against the broader market hit its worst level in 50 years. However, their earnings resilience remains intact while valuations have rapidly retreated, creating a 'generational buying opportunity,' and suggested$NVIDIA (NVDA.US)$ 、 $Taiwan Semiconductor (TSM.US)$ 、 $Advanced Micro Devices (AMD.US)$ 、 $Broadcom (AVGO.US)$ the 'AI computing power supergroup' consisting of。However, for Tesla, as of now, Tesla's forward PE for 2026 still stands at 168x, significantly higher than most large-cap tech stocks.

Amid significant downward revisions in market expectations for Tesla’s revenue, EBIT, EPS, and FCF over the next few years, the stock price has not declined proportionally. This indicates that the market is placing higher value on businesses such as robotaxis, robots, and AI anticipated a decade from now

It is indeed a fact that progress on several long-term development goals previously proposed by the company has been slower than expected: for example, the goal of deploying a million-level Robotaxi fleet announced in 2020 has so far only resulted in the deployment of hundreds of supervised test vehicles; similarly, the target of achieving 20 million annual vehicle sales by 2030 currently has a market consensus of just 2.8 million units. Therefore, there is some execution risk associated with the market’s current pricing of new businesses like Robotaxis and Optimus robots

However, J.P. Morgan's assessment has not been universally accepted by all institutions.

First, the deceleration of energy storage business in the first quarter was extrapolated too quickly.Regarding the decline in the energy storage sector, Morgan Stanley explicitly pointed out that fluctuations in a single quarter should not be inferred as a long-term demand trend. The figure of 8.8GWh is significantly below expectations, but it was also emphasized that large-scale grid-side energy storage projects inherently experience strong quarterly volatility due to factors such as approvals, labor, and grid connection. Thus, "it is too early to define this as a trend". Although the forecast for energy storage deployment in 2026 has been revised down to 59GWh, the long-term outlook remains largely unchanged. In other words, while the poor performance of the energy storage sector in the first quarter is factual, one cannot simply conclude that 'the second growth curve has failed.'

Second, it may have underestimated Tesla's resilience in terms of its market share in electric vehicles.Global electric vehicle data from February showed that in February 2026, Tesla regained the top spot with 101,826 BEV sales and a 14% global market share., surpassing BYD's 11%; in the US market, Tesla's BEV share in February was 45.8%, and it was mentioned that the US share rose to in March 49.2%, higher than the same period last year's 40.1%。

This shows that Tesla's automotive business has not collapsed; it has simply shifted from a 'high-growth unilateral narrative' to a 'strong market share but not fast enough growth' mature divergence asset.Although brand sentiment is relatively weak, it is not unilaterally deteriorating.In terms of regional sales data, the US and China were relatively weak as of February, but European registrations through February were roughly flat to slightly growing year-over-year, with stronger performance within the month for European countries with available March data.

What should we look at next? How should Terafab be evaluated?

Therefore, regarding Morgan Stanley’s report, if you're only looking at the next two quarters, its logic holds up. If you’re looking at the next three to five years, its model may not fully capture what the market truly trades on with Tesla.Going forward, four key points still need attention:

First,Earnings report on April 22,especially regarding energy storage, inventory, gross margin, price incentives, and cash flow.The earnings day is the next key moment. What the market most wants to confirm is whether the 50,000-unit inventory pile-up in Q1 was a one-time fluctuation or indicative of deeper demand issues.Whether the energy business is experiencing temporary fluctuations or also starting to face pressure,if energy storage cannot recover in Q2, the market will reassess Tesla's logic of 'weak auto sales offset by strong energy storage'.

Second, the speed at which robotaxi transitions from concept to verifiable operations.One of the most important catalysts for the market at this stage is the expansion of the unsupervised robotaxi fleet in Austin,as well as progress on launching in additional cities by the end of June. The core logic is that every mile driven by an autonomous vehicle will enhance the learning efficiency of the personal version of FSD, increase FSD adoption rates, and ultimately improve auto demand and free cash flow. The market may not fully believe in this closed loop yet, but it will first trade on whether 'it has started to run.'

Third, new models and model mix.The role of Model Y L and potential new models in improving deliveries in the second half of the year.The biggest issue for Tesla on the automotive side right now is not a lack of market share, but rather the absence of a strong enough new product driver.

As for Terafab: the direction is ambitious, but it remains far from realization at this stage.The direction is correct, and the imagination is vast, but at this point, it resembles more of a long-term option than a near-term performance variable.

On one hand, it does align with Tesla's strategic path in recent years. Chips have become the pillar of Tesla's growth logic for the next decade or more and are at the center of its physical AI narrative. According to Musk, the goal of Terafab is an annual computational power production capacity of 1TW, including logic, storage, and packaging, which is approximately equivalent to50 times the current global AI computing power output.From a strategic intent perspective, the essence of this initiative is not about 'making money by producing chips,' but rather gaining control over FSD, Optimus, the robotics network, and even broader computational power supply.

But on the other hand, it's still very far from realization.Terafab did not provide a specific production start date; if viewed in the traditional way, advanced 2nm logic capacity capex for every 10,000 wafer starts per month is approximately USD 5.5 billion, corresponding toand for 100,000 wafer starts per month, it would be USD 55 billion. The potential scale Musk mentioned even includes 160,000 wafer starts per month , though the scope and the proportion Tesla will bear remain unclear.

Barclays was more straightforward, describing Terafab as a "show-me story", drawing an analogy with the progress made after Tesla's 2020 Battery Day. At that time, the company set a goal of 3TWh battery production capacity by 2030, but currently less than 1% has been achieved. The company needs to demonstrate tangible progress rather than just停留在规划层面.

Another important but easily overlooked detail is:A significant portion of Terafab’s output is actually intended for space-related applications, not all directly serving the terrestrial automotive business. Musk mentioned that about 80% of the chips will be sent to space for massive solar-powered AI data centers (launched by Starship). The remaining 20% will stay on Earth for Optimus robots, robotaxis, and autonomous driving systems.。This means that even if the project moves forward, its near-term impact on the automotive business over the next two quarters will be almost negligible. Therefore,Terafab can be seen as Tesla’s attempt to upgrade itself from being a 'car company + software' to becoming an 'infrastructure company for physical AI.' If this path succeeds, its valuation will be rewritten; however, at this current point in time, it is more suitable to view it as a strategic declaration rather than a reflection of next year’s income statement.

Lastly, how should investors approach Tesla right now?

Tesla resembles an asset being traded in three parts: its automotive core business, energy operations, and long-term options like AI, robotaxis, and Optimus. Currently, the pressure on the stock price comes from the first part, while the latter two are supporting the overall valuation. The issue is that the former is weakening, and the latter remains far off. Consequently, the divergence between bulls and bears will widen, leading to greater volatility.

Based on the latest data as of April 8, 2026,Tesla (TSLA.US) shows initial signs of stabilization following severe overselling in its technical indicators.The current stock price rebounded to $364.6 during after-hours trading, still below all major moving averages, with a bearish moving average alignment and weak technical patterns; however, numerous oscillators have entered the oversold zone, suggesting that short-term downward momentum may be waning. After experiencing a deep correction, there is potential for a short-term technical rebound, but a reversal of the medium-term trend remains to be seen.

Meanwhile, signals from the options market reflect strong risk-hedging demand from institutional investors as well as bets on short-term volatility.The implied volatility (IV) stands at 53.36%, with the put-call ratio below 1 but close to 1, indicating fierce competition between bulls and bears at the current price level. Yesterday's large purchases of put options in the options market show that big money is actively managing downside risks. In the short term, attention can be paid to the support effectiveness at $345; if it holds steady, an oversold rebound could occur. Additionally, whether it breaks through and stabilizes above the 5-day and 10-day moving averages (in the $362-$367 range) with increased volume will be crucial.

(1) If you are a conservative investor, now is not the time to chase Tesla just because of a day or two of geopolitical easing rebounds.

Short-term market risk appetite has significantly improved, with investors eager to seize the rebound window brought by geopolitical easing.However, medium-term uncertainties remain. If negotiations collapse, oil prices may spike again, and risk assets could continue to face pressure.What truly weighs on it is not only the Middle East situation but also factors such as the lack of proof for a turning point in the automotive fundamentals, high inventory, cash flow pressure, and still expensive valuations, among others.

(2) If you already hold Tesla and don't want to sell, but are concerned about uncertainties around earnings reports,

If catalysts and key data on earnings day begin to materialize, the stock price has a chance to recover towards the optimistic scenario. Conversely, if the automotive segment continues to rely on price cuts and incentives, inventory doesn’t clear, and energy storage remains stagnant, the market will increasingly converge towards a pessimistic framework.

If investors are optimistic about Tesla’s long-term plans and short-term rebound but are worried about uncertainties surrounding the earnings report,a long collar strategy could be considered. The benefit is that it provides downside protection via a Put while selling a Call to recoup some premium, reducing hedging costs. The trade-off is giving up some upside potential, which aligns with the goals of defensive clients. This strategy is suitable for heavily invested shareholders who already have profits or are deeply underwater but are concerned about earnings risk. The strike price of the Put should be chosen based on where you want to set your floor, while the strike price of the Call depends on where you're willing to cap your upside gains. For example, with Tesla currently at $362 pre-market:

(The figure below illustrates the simulated profit and loss scenario of this strategy on the expiration date. The design image displayed on the screen is for demonstration purposes only and does not constitute any investment advice or guarantee; market conditions fluctuate frequently, and the prices shown do not represent actual values.)

(3) If you wish to participate in the short-term rebound following a geopolitical easing, you are an investor with a relatively high risk appetite.

Suitable for those who acknowledge the restoration of risk appetite after the easing of Middle Eastern tensions and also recognize Tesla’s strong upside potential but do not want to take excessive risks by placing large bets.One may consider a Bull Call Spread. Both bearish logic and bullish imagination are strong, leading to significant divergence and thus substantial volatility, making it suitable for participating in a 'rebound with limited cost.' The choice of strike price for the long leg determines your starting point for participating in the upside, while the selection of strike price for the short leg needs to be at what you consider a reasonable short-term target range.

(The figure below illustrates the simulated profit and loss scenario of this strategy on the expiration date. The design image displayed on the screen is for demonstration purposes only and does not constitute any investment advice or guarantee; market conditions fluctuate frequently, and the prices shown do not represent actual values.)

Finally, Option Sir brings a small perk for fellow investors, welcome to claim it.Options Beginner Pack

This event is exclusively for invited HK users, click to learn moreDetailed event rules >>

Market conditions are complex and volatile,Options strategyOverwhelmed by choices? Futubull helps you build a portfolio in three steps.Options strategymaking investing simple and efficient from now on!

Option Risk Warning:An option is a contract that grants the holder the right, but not the obligation, to buy or sell an asset at a fixed price on a specific date or at any time before that date. The price of an option is influenced by various factors, including the current price of the underlying asset, the strike price, time to expiration, and implied volatility. Implied volatility reflects the market’s expectations for the level of volatility in the option over a future period. It is a data point derived inversely from the Black-Scholes option pricing model and is generally regarded as an indicator of market sentiment. When investors anticipate greater volatility, they may be more willing to pay a higher price for options to hedge risks, resulting in higher implied volatility. Traders and investors use implied volatility to assess the attractiveness of option prices, identify potential mispricings, and manage risk exposure.

Disclaimer:This content does not constitute any offer, solicitation, recommendation, opinion, or guarantee for any securities, financial products, or tools. The risk of loss in trading options can be substantial. In some cases, losses may exceed the initial margin deposited. Even if you set contingent orders such as 'stop-loss' or 'limit' orders, these may not prevent losses. Market conditions may prevent these orders from being executed. You might be required to deposit additional margin within a short period. If you fail to provide the required amount within the specified time, your open positions may be liquidated. However, you will still be responsible for any shortfall in your account. Therefore, before trading, you should study and understand options and carefully consider whether such trading is suitable for you based on your financial situation and investment objectives. If you trade options, you should be familiar with the procedures for exercising options and the rights and obligations upon exercise and expiration. Option trading involves extremely high risks and is not suitable for all investors. Investors should read carefully before engaging in any options trading strategy.Characteristics and Risks of Standardized Options。

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (21)

to post a comment

78

109