"AI Bottleneck Trade" Ignites Upstream Sector—Who’s Raking in the Profits?

Token Economy Explodes! China's Daily Average Token Usage Breaks 1.4 Quadrillion | In-Depth Analysis | Research Report | Potential Stocks | AI

Recently, NVIDIA CEO Jensen Huang clearly stated in a recent in-depth interview that Token has become a new commodity, AI computers are factories producing Tokens, and the proportion of AI computing in GDP will achieve a hundredfold increase in the future. Since 2026, the global AI industry has entered a new phase of scaled commercial use, with Token evolving from the basic technical unit of large models to a carrier of commercial value that can be measured, priced, and traded, marking an inflection point for the explosion of the Token economy. In March 2026, China's daily average Token usage exceeded 1.4 quadrillion, growing over a thousand times in two years; global weekly Token usage annual growth exceeds 800%. The Token economy addresses the long-standing pain point of vague commercialization within the AI industry, driving large model vendors to shift from a customized 'selling capabilities' model to a standardized 'selling usage' monetization model, restructuring the entire AI industry chain’s business logic. Presently, tech giants like NVIDIA and Alibaba have completed their core strategic positioning; investors should consider which investment opportunities within the domestic market?

The Rise of the Token Economy: A New Cycle for the AI Industry – How Can Investors Seize the Opportunities of the Times?

Since 2026, as the global AI industry has transitioned from technological R&D to scaled commercial application, Token (officially named 'Ciyuan' in Chinese) has evolved from being the smallest technical unit for processing information in large AI models to becoming a new commercial value carrier that can be measured, priced, and traded. The Token economy is now at an explosive turning point. Data from the National Data Bureau shows thatAs of March 2026, the average daily Token usage in our country has exceeded 140 trillion, achieving over a thousand-fold increase in just two years since early 2024; globally, weekly Token usage surged from 2.03 trillion in March 2025 to 20.4 trillion by March 2026, growing more than eightfold within a year.。

The core value of the Token economy lies in resolving the long-standing pain points of commercial ambiguity within the AI industry, shifting large model enterprises from a customized service model of 'selling capabilities' to a standardized, scalable revenue model of 'selling usage,' thereby restructuring the entire commercial logic of the AI industry chain. Global tech giants have taken the lead in strategic positioning: NVIDIA CEO Jensen Huang explicitly stated that 'Token is a new commodity, and AI computers have become factories producing Tokens,' asserting that the share of AI computing in GDP will increase a hundredfold; $BABA-W (09988.HK)$ Formally establishing the ATH business group with the core objective of 'creating Tokens, distributing Tokens, and applying Tokens,' completing the full industrial chain layout. As global demand for Tokens in the AI industry rapidly grows, what investment opportunities will this bring to domestic market investors?

Figure 1: Growth in Token usage among major global models

Data source: OpenRouter platform data

AI-driven rise of the Token economy with significant future growth potential

On March 25, 2026, the National Committee for the Review of Scientific and Technical Terminology officially announced that the Chinese term for Token in the field of artificial intelligence would be 'Ciyuan,' clearly defining it as 'the basic symbolic unit with certain semantics used for information storage, processing, and exchange in smart devices, and the smallest unit for large models to process and exchange information.' The National Data Bureau further clarified that Token possesses three core characteristics: measurability, pricability, and tradability, making it a value anchor in the intelligent era and the key settlement unit connecting technical supply with commercial demand. From an industry perspective, the Token economy is a new economic form in the AI industry based on Token as the value scale and medium of circulation, encompassing its entire lifecycle of 'production-scheduling-consumption-pricing-trading.' Its underlying logic can be summarized as 'Token = computing power = energy = value,' essentially transforming AI capabilities into standardized tradable commodities.

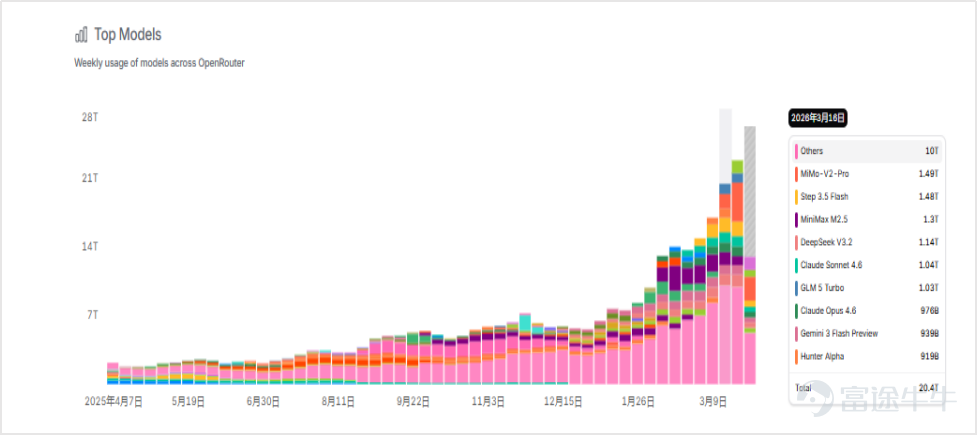

The rise of the Token economy is primarily driven by the exponential surge in AI inference demands, with this growth momentum reflected in three core dimensions: invocation scale, application scenarios, and commercialization models. In terms of invocation scale, the average daily Token usage in China's AI sector soared from 100 billion at the beginning of 2024 to 100 trillion by the end of 2025, further breaking through 140 trillion by March 2026, representing over a 1,400-fold increase in just two years; the global market also maintains high levels of growth.Data from the OpenRouter platform shows that by mid-March 2026, the global weekly model token usage has reached 20.4 trillion tokens, with a week-on-week growth rate exceeding 20%. Notably, China’s weekly model token usage has surpassed that of the United States for several consecutive weeks, achieving a historic milestone.

Figure 2: Weekly Token Usage Comparison Among Major Global Models

Source: OpenRouter platform data

In terms of application scenarios, the use of tokens has achieved full-dimensional penetration across all areas. Large-scale deployment of AI agents, enterprise-level intelligent systems operating 24/7, and explosive growth in multimodal content generation have driven per-user token consumption to increase 10-50 times compared to traditional dialogue scenarios. Beyond core text-based applications, demand for multimodal tokens in vision, audio, and video is rapidly expanding. A single high-definition image of 1024×1024 consumes approximately 85 visual tokens, while one minute of high-definition video can consume thousands to tens of thousands of tokens, continuously pushing the industry’s growth ceiling higher.Some domestic model companies have even seen '20-day revenues surpassing the entire year of 2025,' fully demonstrating the commercial feasibility and long-term growth potential of the token economy.

Figure 3: Characteristics of AI Agents at Different Application Levels

Source: NVIDIA GTC Conference, Wind

The value proposition of tokens is not static; it has undergone three core evolutionary stages, ultimately completing a fundamental leap from being a basic technical unit to becoming a core value carrier in the digital economy. In its initial stage as a technical unit, tokens represented the smallest processing unit for models to perform text tokenization, semantic understanding, and reasoning generation—serving as the foundational layer for stable operation of AI technology systems. As the industry's commercialization accelerated, tokens entered the billing standard phase, becoming the key measurement unit for AI service commercialization. The standardized 'pay-as-you-go' model based on token consumption, analogous to utility billing such as water, electricity, and gas, significantly lowered the threshold for using AI services, driving widespread adoption at scale. Now, amid an explosion in AI inference demands, tokens have advanced to become a value carrier, gradually emerging as a core tool for value transfer in the digital economy. They successfully bridge the full conversion chain of 'electricity-computing power-intelligence-value,' evolving into a globally tradable, tiered-priced new commodity in the AI era.

How does the token economy reshape the business logic of the AI industry?

The rise of the token economy is not merely an innovation in billing models but represents a fundamental reconstruction of the entire value chain of the AI industry. This transformation manifests in three core dimensions: iterative business models, reshaped competitive dynamics, and the rebuilding of end-to-end value distribution systems. Before the maturity of the token economy, commercialization of large AI model companies primarily relied on customized solutions, private deployments, and fixed subscription models—all essentially 'selling capabilities.' These approaches faced key challenges: difficulty quantifying technical abilities, lack of unified pricing standards, high complexity in scaling replication, and clear profitability ceilings. The token economy has triggered a fundamental shift in AI industry business models. The core revenue source for AI companies has transitioned from one-time capability delivery to ongoing token consumption. This model eliminates service pricing discrepancies across different scenarios and customers by adopting tokens as a universal measurement standard, enabling industrialized and scalable AI service delivery. It also converts project-based one-time income into recurring usage-driven revenue streams, creating a stable cash flow loop and significantly reducing operational fluctuations for businesses. Furthermore, this approach expands the reach of AI services from serving only top-tier clients to a more inclusive model covering small and medium-sized enterprises and individual developers, greatly expanding market potential. It directly ties companies’ computing power investment, electricity costs, and token output, binding revenue scale directly to token consumption, thereby forming a clear 'input-output-profit' business cycle.

The token economy has fundamentally transformed the competitive logic of the AI industry. The core metric of competition has shifted from comparing model parameter sizes and leaderboard scores to optimizing the production cost per token and increasing the token output rate per watt. Whoever can produce tokens at a lower cost and with higher energy efficiency gains control over industry pricing and core competitiveness. This shift has given rise to two clear industry trends. First, energy resources have become a core competitive barrier for AI companies, with electricity costs accounting for 70% of token production costs. Electricity prices directly determine the floor price of tokens. In Western China, new energy electricity prices are as low as 0.3 yuan/kWh, only 1/3 to 1/5 of those in Europe and America, making domestic token production costs only 1/6 to 1/10 of overseas prices, creating a crushing cost advantage that is driving 'token exports' as a new growth curve for China’s AI industry. Second, efficiency optimization has become the core direction of industry R&D, shifting the focus from 'building larger models' to 'building efficient models.' The iteration of technologies like MoE sparse architecture, KV Cache caching technology, liquid cooling, and the energy efficiency optimization of domestic chips all aim to improve token production efficiency. Just as NVIDIA's AI systems lead competitors by an order of magnitude on the 'tokens per watt' metric, it directly determines their core influence in the token production process.

In addition, the token economy has built a brand-new industrial value loop for the AI industry, completely reconstructing the value distribution system across the entire chain. In this closed loop, electricity is the core raw material, AI chips are the production engine, intelligent computing centers are token factories, large models are the token refining process, cloud services are the distribution channels, and AI applications are the final consumption scenarios. Tokens have become the core measure of value distribution throughout the entire industry chain. The value contribution of each link can be quantified by its contribution to token production, circulation, and appreciation, breaking the previous imbalance where 'computing power vendors take most of the profits, while application vendors struggle to make a profit.' Meanwhile,The token economy is also driving the AI industry from 'technology-driven' to 'demand-driven.' Model development and computing power deployment no longer blindly pursue parameter scale but instead precisely match downstream token demand, achieving a positive cycle of 'demand-production-supply,' propelling the AI industry from the technology exploration stage into the mature phase of industrialization and commercialization.

AI Token: The 'New Oil' War Between Computing Power and Model Giants

AI Tokens have evolved from being the smallest semantic and computational unit for processing large model texts to becoming 'digital hard currency' with triple core attributes in the AI era: means of production, valuation standard, and business model carrier. By 2026, the industry will officially complete the historic transition from 'training-driven' to 'inference-driven,' with inference computing power accounting for 70% of total AI computing power investment. The global competition has fully shifted from contests over model parameter size to a systematic war over productivity, pricing power, and ecosystem control across the entire token industry chain. Token production efficiency, cost control, and scenario penetration capabilities will directly determine a company’s core competitiveness and industry influence.

The competition in the underlying computing power layer is the foundation of the AI token economy, focusing on three core metrics: single-token production cost, energy efficiency, and throughput. The essence of this competition is to gain rule-making authority over token production and hardware barriers. NVIDIA is the absolute leader in this space. At the 2026 GTC conference, NVIDIA officially introduced the concept of 'Token Factory Economics,' defining data centers as 'token factories' for the first time and establishing a five-tier token value hierarchy ranging from free tiers to $150 per million tokens, redefining the industry’s value assessment standards. On the hardware side, NVIDIA launched two generations of core architectures, Blackwell and Vera Rubin, integrating Groq’s LPU language processing units (acquired for $20 billion) to form a hybrid inference architecture where 'GPUs handle high throughput, and LPUs manage low latency.' They claim this reduces the cost per token to one-tenth of the previous Hopper platform, increases inference performance per watt tenfold, and maintains a monopoly over more than 90% of global high-end AI training and inference computing power through the CUDA ecosystem, firmly controlling the core hardware standards of token production. Competitors such as AMD, Intel, and Huawei Ascend are respectively targeting mid-to-low-end markets and domestic alternatives, while major cloud providers are accelerating the deployment of self-developed chips. Leveraging its green energy supply chain advantages, China has constructed a systemic cost barrier for token production from the energy end.AMD, Intel, and Huawei Ascend are competing for the mid-to-low-end market and domestic replacement tracks. Major cloud providers are also speeding up the deployment of proprietary chips. China, leveraging its green energy supply chain advantages, has established a systemic cost barrier for token production from the energy end.

Figure 4: AI Factory Tokens Become Standardized Output

Data Source: GTC Conference

The model layer and pricing power represent the core profit battle within the industry chain. A clear hierarchical competitive landscape has formed. Leading US-based firms firmly control the pricing话语权 of the high-end token market. OpenAI, through its tiered capabilities in GPT-4o and GPT-5, has established industry-standard token price anchors, with high-end model token pricing reaching up to $150 per million tokens, promoting a premium logic of 'paying for results.' Anthropic’s Claude 3 series focuses on long-context window advantages, offering differentiated pricing in professional long-text scenarios. Google, through its Turbo Quant lossless compression technology, compresses KV Cache to 3-3.5 bits, achieving over six times memory compression and eight times attention calculation acceleration, optimizing token costs to the extreme in multimodal scenarios, forming direct competition against OpenAI.

Chinese manufacturers have achieved a clustered rise and the reconstruction of pricing systems. Data from OpenRouter, a global AI model API aggregation platform, in March 2026 shows that the weekly token usage of China's large AI models reached 7.36 trillion tokens, surpassing the US for three consecutive weeks. Four out of the top five global AI models are Chinese, completely breaking the long-term monopoly of American vendors. Domestic models have achieved a dramatic reduction in per-token costs through engineering innovations like MoE (Mixture of Experts) architecture, FP8 mixed-precision quantization, and KV cache optimization. The token consumption of MiniMax M2.5 in standard tests is only 36% of Claude Opus, with operating costs being just 1/40th of leading overseas models. The mainstream domestic model APIs have entered an era where input prices are fully below 0.5 yuan per million tokens, which is only 1/10 to 1/20 of overseas models with similar performance. Notably, industry competition has shifted from pure price wars to value stratification. Leading domestic companies such as Zhipu AI, with its GLM-5 model making breakthroughs in specialized scenarios like programming, raised token prices twice in Q1 2026, with cumulative increases reaching 83%, yet API usage continued to rise instead of falling, confirming the core industry logic that 'upper limits of model intelligence determine pricing power, and token consumption scale determines value volume.'Vendors have increasingly used price hikes to filter out non-essential testing demands, focusing on high-value enterprise clients to complete the commercial transition from 'traffic subsidies' to 'value screening.'

What opportunities should investors pay attention to?

In the AI era, the rise of tokens has driven a fundamental leap in the nature of computing — evolving from a 'storage system,' where humans pre-input data and computers retrieve matches, into a 'generative system' with contextual awareness and autonomous generation capabilities. Computers' role in the real economy has also been fundamentally restructured. NVIDIA founder Jensen Huang provided an accurate definition of this transformation: he likened traditional computers, which focused on file storage, to 'warehouses' incapable of directly creating substantial revenue. Today’s AI computers have evolved into 'Token factories' directly tied to enterprise income creation. Tokens produced by AI foundries have become a new digital commodity that can be finely stratified and standardized in pricing. Huang further pointed out that tokens offer differentiated core values for different audiences, forming a tiered product system akin to the iPhone’s free, mid-range, and premium levels. 'Market applications willing to pay $1,000 per million tokens are already on the horizon; it’s a matter of when, not if,' he stated. Based on the new 'Token factory' business model, computing devices have completed the shift from traditional cost centers to profit centers. Huang confidently predicted the macro trend: 'The surge in productivity will accelerate global GDP growth. I’m absolutely certain that future computing’s share of global GDP will reach 100 times its previous level.' Against this backdrop, the explosive growth in Token consumption has spurred deep market exploration of the underlying core investment opportunities.

Investors should first focus on the mainline of the AI computing power industry chain, which represents the most deterministic 'pick-and-shovel' track within the Token economy and serves as the foundational layer for AI industry explosions. The essence of tokens lies in their transformation from computing power and energy, with computing power supply directly determining token production capacity, showing extremely strong demand rigidity. Key attention should be given to leading domestic general-purpose AI computing power players, which directly influence the efficiency and cost of token production, deeply benefiting from the surge in inferential computing power demand. Examples include Montage Technology (6809.HK), a leader in configurable memory interface chips, and core optoelectronic communication targets. $CIG (06166.HK)$ and $YOFC (06869.HK)$ , as well as leading wafer manufacturers $SMIC (00981.HK)$ , and computing infrastructure operators $GDS-SW (09698.HK)$. These entities are directly tied to the rigid demand for expanding token production capacity, offering high certainty in earnings realization and serving as the core holdings for stable allocation.

Mid-term growth should focus on AI software and large models, the pricing core and value distribution hub of the Token economy, where the Matthew Effect is highly pronounced. Large models act as the core 'issuers' of tokens, with leading firms setting the industry's token pricing standards. They can leverage economies of scale to form a positive feedback loop of 'cost reduction driving market share gains.' In the general large model space, key focus should be placed on vendors who have achieved scalable API commercialization via token-based billing, with clear logic of simultaneous volume and price increases. For vertical AI tracks, investors may allocate towards companies specializing in high-value scenarios like office automation, enterprise ERP, and intelligent agents, which are tightly integrated into core enterprise workflows, securing long-term stable token consumption needs and offering robust growth potential. $MINIMAX-W (00100.HK)$ 、 $SENSETIME-W (00020.HK)$ , these companies have realized scalable API commercialization based on token billing, with clear growth logic of rising volume and pricing; $KINGSOFT (03888.HK)$ 、 $KINGDEE INT'L (00268.HK)$ , these enterprises specialize in high-value scenarios such as office solutions, enterprise ERP, and intelligent systems, deeply binding themselves to corporate core business processes and locking in long-term stable token consumption demand, providing ample growth elasticity.

For stable allocation, prioritize leading internet giants with a full industry chain layout. These stocks offer both steady cash flow and strong AI growth potential, serving as the cornerstone for AI-focused Hong Kong stock investments. Key focus areas include $TENCENT (00700.HK)$ 、 $BABA-W (09988.HK)$ , which respectively leverage large-scale models like HunYuan and the ATH business group’s Token full-chain ecosystem to complete a closed-loop for Token 'creation-distribution-application.' They possess irreplaceable competitive barriers across pricing, supply capacity, and real-world application scenarios; simultaneously, consider $KUAISHOU-W (01024.HK)$ 、 $MEITUAN-W (03690.HK)$ platform enterprises with rich application scenarios. Their C-end and B-end ecosystems can continuously unlock scalable Token consumption potential.

Disclaimer: Any information provided in this report regarding or related to any investment or potential transaction is subject to the applicable laws and regulatory requirements of your jurisdiction, and you are solely responsible for ensuring compliance with such laws and regulations. The content of this report is for reference purposes only and does not constitute investment advice. Our company has made every effort to ensure the accuracy of the financial information provided, but we assume no responsibility or provide any form of guarantee regarding the accuracy, completeness, or effectiveness of all or any part of the content. We will not be held liable for any errors or omissions. Please also note that securities and virtual asset prices can fluctuate, particularly with very high risks associated with virtual assets, and investors should exercise caution and bear investment risks on their own.

———————————————————————

About the author:

Victory Securities - Hong Kong's Leading Virtual Asset Broker

Victory Securities (08540.HK), with over 50 years of history in Hong Kong, is a comprehensive full-service licensed brokerage offering four main business services to retail investors, institutional investors, high-net-worth clients, and enterprises: wealth management, asset management, virtual assets, and capital markets. It has received numerous accolades and essential qualifications in the Asia-Pacific region. In 2023, Victory Securities became the first licensed brokerage in Hong Kong to hold licenses issued by the Securities and Futures Commission for virtual asset trading, advisory, and asset management services. It was also approved by the SFC to provide virtual asset trading and advisory services to retail investors, offering one-stop compliant and legal Bitcoin and Ethereum trading, exchange, and deposit/withdrawal services.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comment (1)

to post a comment

5

4