SICC Advanced: The market may be underestimating a true silicon carbide substrate leader

In the third-generation semiconductor sector, SICC Advanced is a typical example of 'strong industry presence but weak pricing power'.

If we only look at the secondary market, it doesn't enjoy high valuations as early as some popular stocks. However, when we return to the industrial chain, we find that SICC Advanced is not positioned in an ordinary material segment, but rather in the most fundamental and critical base material segment of the silicon carbide supply chain—the substrate.

This means that the market's understanding of it may not yet be fully mature.

1. Why should we reassess SICC Advanced?

To start with the conclusion: SICC Advanced $SICC (02631.HK)$ is not a thematically weak company in terms of fundamentals; on the contrary, it increasingly resembles a silicon carbide substrate company with characteristics of a global leader.

In the past, market attention on such companies often focused on industry conditions, price fluctuations, and short-term profitability. However, if we only use this framework to evaluate SICC Advanced, we risk overlooking a more important fact: its position in the supply chain determines that it is not just a 'material company tied to cyclical trends.'

Based on publicly available information and industry logic, SICC Advanced already exhibits several strong attributes:

※ Ranks first globally in market share for 6-inch conductive SiC substrates

※ Ranks first globally in market share for 8-inch conductive SiC substrates (with over 50%), which represents the mainstream direction of the future

※ The first to advance mass production and delivery of 12-inch SiC substrates

※ Gradual production ramp-up at three major bases in Lingang (Shanghai), Jinan, and Jining, with capacity now entering the release phase

Looking at these points together, the core feature of SICC Advanced becomes clear: it is not playing catch-up but rather securing strategic positions.

However, the capital markets have not fully priced the company based on this logic. Compared to some third-generation semiconductor companies, SICC Advanced does not appear aggressive in metrics like PB or PS, and at certain times, it even seems undervalued. In other words, the market has already given significant growth premiums to some peers, but it still underestimates the value of SICC Advanced as a 'leading materials company.'

The real contradiction here is not whether the company has value, but that the market’s understanding of its value remains incomplete.

Second, the market has not fully reflected the expectation gap: Tianyue is not an ordinary 'materials stock'.

Many people’s understanding of Tianyue Advanced stays at one sentence: it is a materials company in the SiC industrial chain.

This statement is correct, but not comprehensive enough.

Because there are significant differences within 'materials companies.' Some materials are midstream, while others are upstream; some materials resemble processing steps, whereas others serve as the most crucial foundation of the entire industrial chain. Silicon carbide substrates clearly belong to the latter category.

Why do I say that?

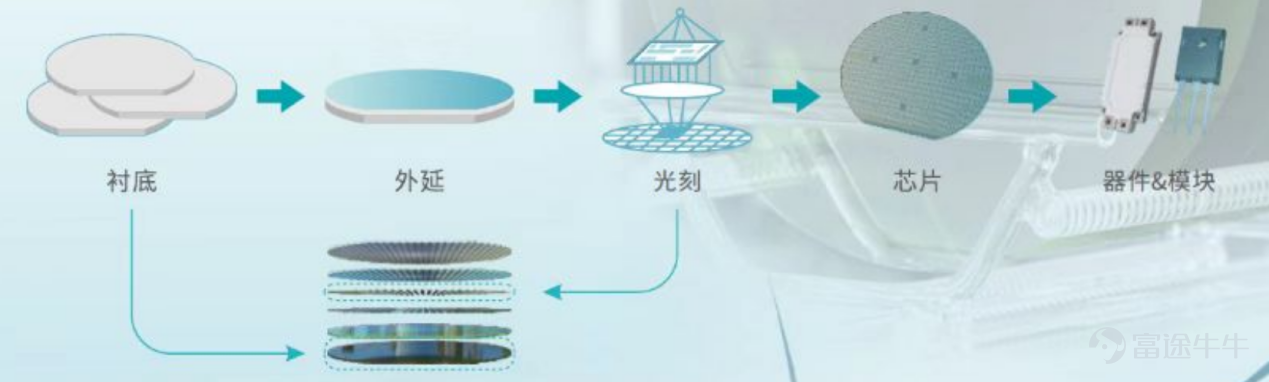

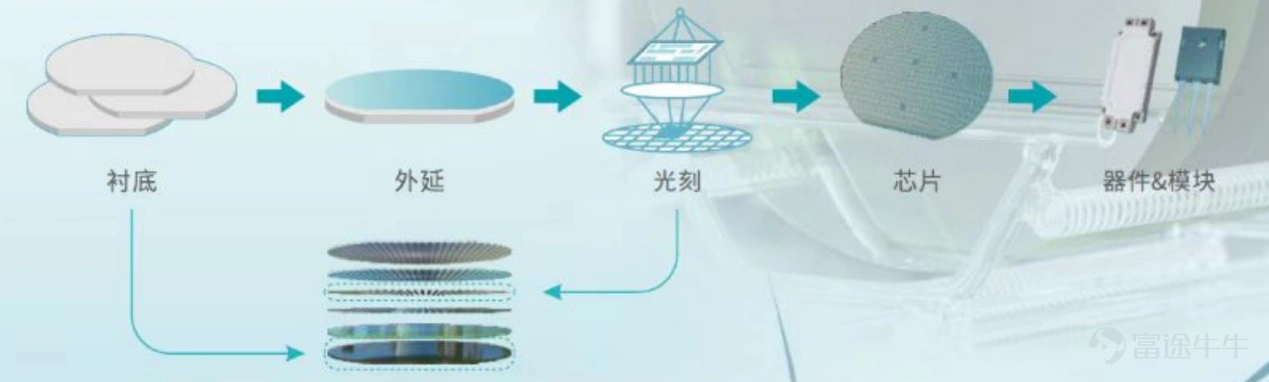

This is because the substrate determines not only costs but also the upper limit of the industry.

Simply put, the substrate is the 'foundation' of chips, and silicon carbide substrates grow slowly, making it more difficult to control microscopic defects compared to silicon substrates. The production process of substrates ranges from crystal growth to microfabrication of substrates at the atomic level, coveringcrystal quality, defect control, size upgrades, and final yield,which makes it the core part of the entire silicon carbide industrial chain that first determines the performance and manufacturing difficulty of the final product.

In comparison, epitaxy, although a necessary step, is essentially a process based on the substrate, mainly responsible for forming functional layers, adjusting doping, and improving device voltage resistance.

Whether epitaxy is done well or not fundamentally depends on the quality of the substrate. The substrate is the most fundamental layer in the entire silicon carbide device system and the hardest part to breakthrough.

Especially as the silicon carbide industry transitions from 6-inch to 8-inch, and then upgrades to even larger sizes, the first element to be tested is not actually downstream devices, but whether upstream substrates can stably increase in size, suppress defects, and ensure yield.

Therefore, if the market only views Sinopower Advanced Materials as a 'material stock that fluctuates with the SiC cycle,' this judgment would be overly simplistic.More accurately, Sinopower Advanced Materials is closer to being a leading foundational material company with platform-like characteristics.

The value of such companies does not just depend on how good the market conditions are, but also on whether they occupy an irreplaceable position in the industrial chain.

And what makes Sinopower Advanced Materials most noteworthy is precisely this point.

Third, why can't we simply compare Sinopower Advanced Materials with Innoscience and Hanchen Tiancheng as direct substitutes?

When discussing third-generation semiconductors, the market often compares several companies side by side.

But the issue is that different companies operate in different parts of the industry, serve different application boundaries, and have varying business models; direct comparisons can easily lead to biased conclusions.

1. Compared with Innoscience: GaN and SiC do not share the same market space.

Innoscience is undoubtedly the leader in gallium nitride (GaN), which is not in question.

Gallium nitride is also an important branch of third-generation semiconductors, and Innoscience operates under the IDM model, making its growth logic easier for the market to understand.

However, gallium nitride and silicon carbide do not belong to exactly the same competitive landscape.

Gallium nitride is mainly used in low-voltage power electronics, such as fast charging and power conversion in medium- and low-voltage scenarios. Silicon carbide, on the other hand, is more suitable for high-power applications such as new energy vehicles, photovoltaic energy storage, power grids, and industrial sectors, which typically represent a larger market with broader applications.

More importantly, SICC Advanced does not focus on devices but on SiC substrates.

The scope of substrates is naturally wider than that of devices. Substrates not only serve the power device supply chain but also have the potential to expand into areas such as RF, optics, AR glasses waveguides, laser chips, computing chip heat dissipation substrates, and advanced packaging.

In other words, Innoscience follows a logic closer to the 'device chain logic,' while SICC Advanced aligns more with the 'basic materials platform logic.'

The two cannot simply be evaluated using the same valuation framework.

[Figure 1: The SiC power device market is projected to grow from approximately $3.4 billion in 2024 to about $10.3 billion by 2030, with automotive and mobility remaining core application scenarios. The vast potential of high-power applications is one of the key factors that makes SiC a more significant industry foundation compared to GaN.]

2. Compared with Hanteck: Epitaxy is a process step, while substrates are the foundation.

If Innoscience represents competition over material systems, then the comparison with Hanteck reflects more of a competition between different segments of the industry chain.

Hanjing Tiancheng is a key company in the silicon carbide epitaxy segment. However, epitaxy and substrates are not at the same level.

As mentioned earlier, epitaxy involves growing functional layers that meet device requirements on the surface of single-crystal SiC substrates. It is important, but essentially it is a process step.

Substrates are different. The substrate is the physical foundation for all subsequent processes, the starting point, and the base plate. From the perspective of the industrial chain, substrates are more upstream than epitaxy. In terms of technical barriers, the process chain for substrates is longer, and the difficulty of crystal growth and defect control is higher. In terms of value, the market size of substrates is also significantly larger than that of epitaxy.

According to third-party industry estimates, by 2030, the market size for SiC epitaxy will be approximately $1.5 billion, while the market size for SiC substrates will be about $4.1 billion. This means that substrates are not only more fundamental but also have a higher value.

There is another point often overlooked:The customers of epitaxy companies are naturally also the customers of substrate companies.Because epitaxy must be built on top of substrates. Part of the revenue from epitaxy sales naturally includes the value of externally purchased substrates. Simply comparing revenue sizes without breaking down raw material costs can easily lead to overestimating the independent value of the epitaxy segment.

For chip manufacturing companies, what they deeply bind with are often substrate suppliers.

Epitaxy can be self-built or outsourced, but high-quality substrates cannot be produced quickly. According to industry experts, substrates need to go through complex crystal growth and be processed into substrate wafers, with extremely high technical thresholds and a capacity expansion cycle of over three years.

This is why, in recent years, several international device manufacturers, including Infineon, have acquired upstream crystal assets to secure substrate supply. Willingness to pay real money for substrates reflects the attitude of the industry chain itself.

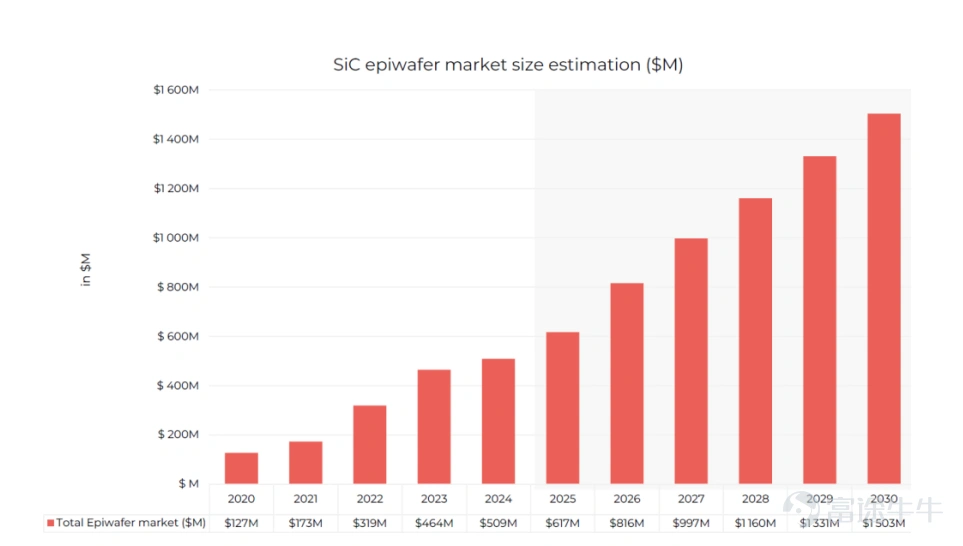

[Figure 2: SiC epitaxy market size forecast. The Yole 2025 annual report shows that by 2030, the global SiC epitaxy market will be approximately USD 1.5 billion. Epitaxy is important but fundamentally remains a process step in device fabrication.]

Fourth, the upgrade to 8-inch and 12-inch may represent the most critical revaluation driver for SICC Advanced.

If 'substrate being more upstream' explains why SICC Advanced should not merely be understood as a cyclical stock, then 'size upgrades' explain why it has potential for revaluation.

The SiC industry is transitioning from 6-inch to 8-inch. This is not just a specification change but more like a redistribution of industry leadership.

Because what an 8-inch upgrade tests first is not downstream device manufacturers but upstream substrate suppliers.

The real challenges are whether larger crystals can be grown stably, whether defects can be controlled, and whether yield rates can be improved.

Epitaxy must also be upgraded, but mostly as an adaptive follow-up. It’s the substrate that holds the true initiative in this round of size upgrades.

This is where SICC Advanced becomes most crucial.

The company is already in a globally leading position with its 8-inch conductive SiC substrates; meanwhile, it is also ahead in the mass production and delivery of 12-inch SiC substrates.

The 8-inch represents the main industrialization focus for the coming years, while the 12-inch represents the long-term technological high ground. Leading on both fronts means that SICC Advanced is positioned not only for capacity expansion but also for future technology premiums and valuation uplift.

Often, the market views 'capacity expansion' as an increase in supply and 'size upgrades' as a natural industry progression.

However, for upstream substrate leaders, size upgrades themselves represent a value reevaluation.

[Figure 3: Global demand for conductive SiC substrates continues to grow, with shipments expected to approach 5 million pieces (6-inch equivalent) by 2030. As a more upstream foundational material segment, substrates directly benefit from the expansion of new energy vehicles, photovoltaic storage charging, and other demands.]

V. The boundary of substrate companies is actually broader than the market perceives.

What substrates determine is not only cost but also the industry's ceiling. The understanding of SiC substrates mainly revolves around power devices, which is clearly insufficient. In fact, the application boundaries of silicon carbide substrates are expanding.

In addition to traditional power electronics scenarios and microwave radio frequency, with the advancement of 8-inch and 12-inch technology, silicon carbide substrates, as a foundational material, are also being eyed by the market for their potential in the following areas:

Acoustic filters

Optics

AR glasses waveguides

Laser Chips

Heat dissipation substrates for computing chips

Advanced packaging and others

These fields are not epitaxial, nor can they be reached by gallium nitride.For example, in the AR field, Meta has already adopted optical-grade SiC waveguide materials in the Orion project, indicating that SiC substrates are extending from traditional power devices to high-end optical applications; in advanced packaging and high-performance computing chip cooling, industry leaders like NVIDIA are continuously exploring the feasibility of using SiC as an interposer or related base material, with a clear timeline, further expanding the market's imagination of the value boundaries for substrates.

These directions share one commonality: what they require are high-performance base materials themselves.

In other words, what truly possesses extensibility is the substrate, not necessarily the epitaxy, and not all material systems can naturally transition into these areas.

This is also why Tianyue Advanced Materials cannot be valued solely as a 'power device supporting material.' If these directions gradually open up in the future, it will more resemble a platform-type basic materials company rather than a subsidiary link in a single growth track.

The valuation of platform-type materials companies often comes not only from current profits but also from their ability to expand future boundaries.

Sixth, why is the undervaluation of Tianyue Advanced Materials essentially due to a lack of understanding of its position in the industrial landscape?

In the short term, Tianyue Advanced Materials is not without pressure. Industry price fluctuations, profit pressures, and demand volatility are all real issues.

However, the problem lies in the fact that the market may be placing too much emphasis on these short-term variables while underestimating the longer-term industrial positioning.

In fact, the decline in prices also has another side: as costs decrease, the replacement rate of silicon carbide devices for silicon-based devices may actually accelerate. Short-term profitability pressures do not necessarily mean a weakening of long-term logic; often, it precisely indicates that the industry penetration rate is entering a phase of faster release.

If we extend the timeline, at least three medium to long-term drivers underpin Tianshan Advanced Materials:

First, its position as the global leader in substrates is strengthening. Advancing simultaneously across 6-inch, 8-inch, and 12-inch dimensions shows that the company isn't just leading in a single area but is building a more comprehensive leadership advantage.

Second, its application scope is clearly broader than what the market currently prices in. It serves not only the SiC power device chain but could also extend into areas like RF, acoustics, optics, AIDC chip cooling, and advanced packaging.

Third, the benefits of size upgrades and supply chain influence have yet to be fully reflected in its valuation. In the 8-inch and 12-inch eras, the true driver of industrial upgrading will be the substrate leader rather than the following links.

Therefore, the core issue for Tianshan Advanced Materials now is not whether the company has room to grow, but when the market will start pricing it as a 'platform-based foundational materials leader.'

Conclusion

The undervaluation of Tianshan Advanced Materials is not just a valuation issue but also a matter of perception.

The market already recognizes that it belongs to the third-generation semiconductor sector, but it may not fully realize yet that it holds the most fundamental, crucial, and potentially value-amplifying position in the industry during the era of size upgrades.

In the short term, it will still be affected by industry pricing pressures and profit volatility; however, in the medium to long term, it benefits from three strong supports: its global leadership in substrates, broader application scope, and the advantages of size upgrades.

Thus, the future recovery of Tianshan Advanced Materials might not just be an earnings recovery. More importantly, it may involve the market's renewed recognition of its position as a 'platform-based foundational materials leader.'

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comment (1)

to post a comment

1

2