"AI Bottleneck Trade" Ignites Upstream Sector—Who’s Raking in the Profits?

Breaking the depreciation curse! GPU leasing fees soar—how far is Neocloud's 'V-shaped' reversal?

Can Neocloud stage a reversal rally?

AI computing power demand has once again exceeded expectations for growth. Since the beginning of the year, leading companies like Anthropic and ByteDance have successively launched blockbuster AI applications. Combined with the 'Lobster' trend igniting an explosion in open-source large model usage, $NVIDIA (NVDA.US)$the H100 chip is experiencing a 'V-shaped' reversal in its value in the leasing market.

Keep in mind that this chip was unveiled by Jensen Huang at the March 2022 GTC and began shipping in the fall of the same year.

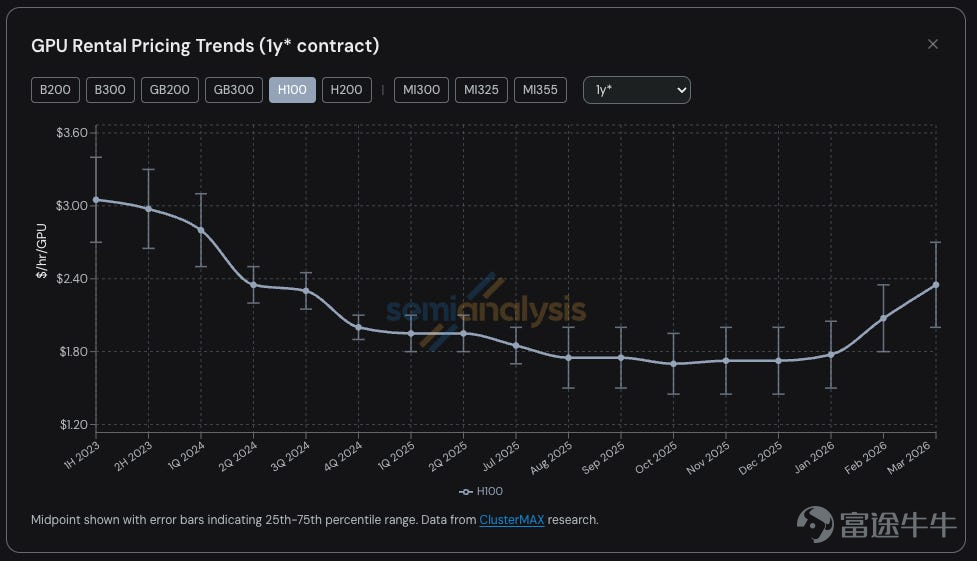

According to the latest data released by semiconductor research firm SemiAnalysis, the one-year lease contract price for the H100 has rebounded strongly from a low of $1.7 per hour in October 2025 to $2.35 in March this year, representing a nearly 40% increase. The GPU computing power market at the start of 2026 is as tight as 'the last flight out'—on-demand rental resources are completely sold out, and locked-in customers are willing to bear price hikes rather than release computing power.

However, there is a severe disconnect between industry reality and market sentiment.Despite the extreme shortage of computing power supply, $CoreWeave (CRWV.US)$ 、 $NEBIUS (NBIS.US)$ 、 $IREN Ltd (IREN.US)$the stock prices of emerging cloud service providers like Neocloud are at their lowest point in nearly a year.

Under aggressive competition in the computing power arms race, this mispricing has created an excellent opportunity for contrarian investment. To understand Neocloud's potential reversal, we need to reassess the three major expectation gaps underlying its business logic.

Three Major Expectation Gaps in Neocloud's Underlying Business Logic

1. Debunking the Myth of 'Commoditized Computing Power': Reassessing Neocloud's Pricing Power

The core logic behind the market's bearish view on Neocloud is that 'computing power will become fully commoditized and陷入a price war.'However, this overlooks the complexity of AI infrastructure. Building clusters with tens of thousands of GPUs to operate efficiently requires a high level of engineering expertise, from network architecture to liquid cooling systems, areas where Neocloud, which focuses exclusively on these aspects, often outperforms traditional cloud giants.

In addition,Despite the accelerated deployment of the Blackwell architecture, demand and rental prices for H100 have remained strong, proving that all types of computing resources are being aggressively snapped up indiscriminately. Neocloud still holds real scarcity and pricing power.

2. Redefining the Business Model: The 'Digital Real Estate Developer' of the AI Era

Investors need to shift their perspective: Neocloud is not a 'middleman' in the traditional sense but rather a highly predictable 'digital real estate developer.'

The true barrier lies in 'power and space': By 2026, chips might be purchasable if you have the money, but data centers with high-density power supply and advanced cooling capabilities will be in short supply. The long-term power contracts and compliant infrastructure that Neocloud holds are its core assets that cannot be easily disrupted.

REIT-like highly predictable cash flow: With non-cancellable lease contracts typically spanning 2-3 years, Neocloud has already secured its future cash flow in advance. This business model, similar to 'infrastructure REITs (Real Estate Investment Trusts),' offers strong financial resilience during macroeconomic shifts or changes in market trends.

III. Pure 'Compute Power Water Seller': Why do large model unicorns favor Neocloud?

Under the monopolistic shadows of AWS, Microsoft Azure, and Google Cloud, how has Neocloud managed to grow aggressively? The answer lies in its 'purity' and 'neutrality.'

Traditional cloud giants are heavily investing in proprietary AI chips (such as AWS Trainium and Google TPU) and directly engaging in the development of large models. This creates significant concerns about 'conflicts of interest' and 'data security' for many independent large model companies (like Anthropic and Cohere), as well as tech giants actively deploying AI (such as ByteDance) when selecting underlying compute power.

In contrast, Neocloud adheres strictly to neutrality. They do not engage in model development, avoid competing with clients for profits, and dedicate 100% of their compute resources to external markets without the risk of internal projects taking priority. This neutral position makes them the most reliable 'safe haven' for top-tier AI players.

Which Neocloud companies are worth paying attention to currently?

Previously‘Mining the New Era of AI! Infrastructure Becomes the Next Main Battlefield—Who Could Become Investors’ New Gold?’I previously compiled a list of Neocloud companies, as follows:

IncludingThe two giants of AI infrastructure $CoreWeave (CRWV.US)$ 、 $NEBIUS (NBIS.US)$ ; emerging AI infrastructure providers $WhiteFiber (WYFI.US)$ ; data center service provider $TSS Inc (TSSI.US)$

Mining transformation company $Applied Digital (APLD.US)$ 、 $IREN Ltd (IREN.US)$ 、 $TeraWulf (WULF.US)$ 、 $Core Scientific (CORZ.US)$ 、 $Hut 8 (HUT.US)$ 、 $HIVE Digital Technologies (HIVE.US)$ 、 $Keel Infrastructure (KEEL.US)$ 、 $Bitdeer Technologies Group (BTDR.US)$ 、 $Galaxy Digital (GLXY.US)$ 、 $Cipher Digital (CIFR.US)$ 、 $Riot Platforms (RIOT.US)$ 、 $MARA Holdings (MARA.US)$ 。

Bernstein recently released an in-depth field guide, breaking down the three most talked-about listed emerging cloud companies in the current market: CoreWeave, IREN, and Nebius.

Although these three companies are all experiencing rapid growth driven by AI computing power and have historical backgrounds in cryptocurrency mining or traditional cloud services, their underlying strategies, asset structures, and business models differ significantly.

1. $CoreWeave (CRWV.US)$: The leading player with both software and hardware capabilities, but facing valuation challenges

CoreWeave is the most mature player among these three enterprises, starting its transformation as early as 2023 and successfully going public in March 2025.

Business Moat:Compared to its peers, CRWV boasts the strongest commercial engine in the industry, along with the most sophisticated software and hardware integration stack. They don't just rent out GPUs; they provide complete AI cluster orchestration and infrastructure services.

Financials and Orders:CRWV has a massive backlog of orders totaling $67 billion and the most diversified customer base. By using large customer contracts as collateral to establish Special Purpose Vehicles (SPVs) for financing, they have successfully reduced their Weighted Average Cost of Capital (WACC) to the lowest among the three, at 8.9%.

Institutional View:Despite strong fundamentals, Bernstein has assigned CRWV an 'Underperform' rating with a target price of $56. The main concern lies in whether CRWV can continue to secure large-scale contracts as data center supply increases post-2028. Additionally, the high net debt/EBITDA leverage ratio of 5.9x is a potential risk.

2. $IREN Ltd (IREN.US)$: A bare-metal computing contractor with 'power assets,' demonstrating explosive growth potential

IREN is still in its transition phase, with over 90% of its revenue in 2025 expected to come from Bitcoin mining operations. However, it holds unique advantages in physical infrastructure.

Core Competitiveness:In an environment of extreme power shortages, IREN’s biggest advantage is its vast portfolio of owned real estate and power pipelines. The company is projected to have up to 4.5GW of grid-connected power capacity.

Business Model:Unlike CRWV, which focuses on software depth, IREN specializes in providing 'bare-metal' GPU hosting services (pure IaaS). Their strategy is straightforward: addressing customers’ pain points around 'time-to-market' by offering pure and reliable power and execution capacity.

Institutional View:Bernstein has given IREN an 'Outperform' rating with a target price as high as $125. Although its $9.7 billion backlog is currently 100% concentrated with Microsoft, its substantial and not fully contracted power reserves provide significant expansion options for future AI stacks (such as Blackwell or even Vera Rubin architectures).

NEBIUS is approximately 18 months behind CoreWeave in terms of development progress, but its strength should not be underestimated.

Historical Legacy and Finances:Thanks to its history as part of Yandex, NBIS retains stakes in assets such as AvRide and ClickHouse, giving it the strongest balance sheet among the three companies.

Flexible Revenue Structure:Compared to the other two companies that almost entirely rely on long-term contracts, NBIS’s cloud background allows it to have a higher proportion of 'on-demand' revenue. However, with large orders from Microsoft and Meta, its contract structure is also changing, with a current backlog of orders reaching $47 billion.

Infrastructure Strategy:In terms of real estate strategy, NBIS adopts a hybrid model, with 25% owned, while actively pushing forward with the construction of its own data centers.

How to Find the ‘Starting Gun’ for a Reversal?

The current Neocloud is in a period of 'extreme divergence,' where industry fundamentals are hot, but the capital market remains cold. This may, however, also represent a golden opportunity for contrarian trading. In the coming quarters, two major catalysts could trigger a market reversal at any time:

1. Earnings Delivery in Financial Reports: When the next quarterly earnings report is released and the market sees that the surging rental prices have genuinely translated into better-than-expected profits and cash flow, the bearish logic will fall apart on its own.

2. Highlighted acquisition value: If Neocloud's market capitalization continues to fall below the replacement cost of its GPU assets and power contracts, it could easily trigger an acquisition by private equity (PE) firms or tech giants seeking to secure independent computing power. This potential acquisition value provides a solid safety net for its stock price.

Summary

In summary, the 'V-shaped' reversal in H100 rental prices is just the tip of the iceberg, reflecting the extreme demand across the entire AI infrastructure market for high-quality, neutral, and sufficiently powered computing resources. Neocloud is at the forefront of this computing power arms race, with underlying business logic far more resilient than traditionally perceived by the market.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (11)

to post a comment

52

161