On Time Mobility (9680.HK): Clear Growth Path After Significant Revenue Increase

It is widely agreed that autonomous driving will reach L4 within a few years, and the number of unmanned vehicles on the road is visibly increasing. The industry's crucial step from zero to one is about to be realized.

Investors in this sector usually focus on companies developing autonomous driving hardware and algorithm models. It is generally believed that once autonomous driving matures, these companies will capture a small portion of the traditional automotive market and a large share of the ride-hailing market. However, an in-depth look at the industrial structure reveals that many participants are still needed for the industry to function effectively.

Ruqi Mobility may be widely recognized as a prominent ride-hailing fleet. However, in the era of autonomous driving, such companies also take on the role of fleet operators, transitioning from managing drivers and vehicles to overseeing vehicles and data. No matter how advanced autonomous driving models become, tasks like supervision, dispatching capacity, refueling or recharging, and asset maintenance will still require human intervention. The company continues to play a crucial role in the future mobility ecosystem.

Today, upon reviewing Ruqi's annual report, it is evident that its revenue has rapidly increased, reflecting its competitive edge in the traditional ride-hailing fleet sector. This also indicates that the company is actively expanding into new business areas. Based on the significant revenue growth, there should be more confidence in the upcoming rapid development of the company’s robotaxi services.

I. Behind the Earnings Growth

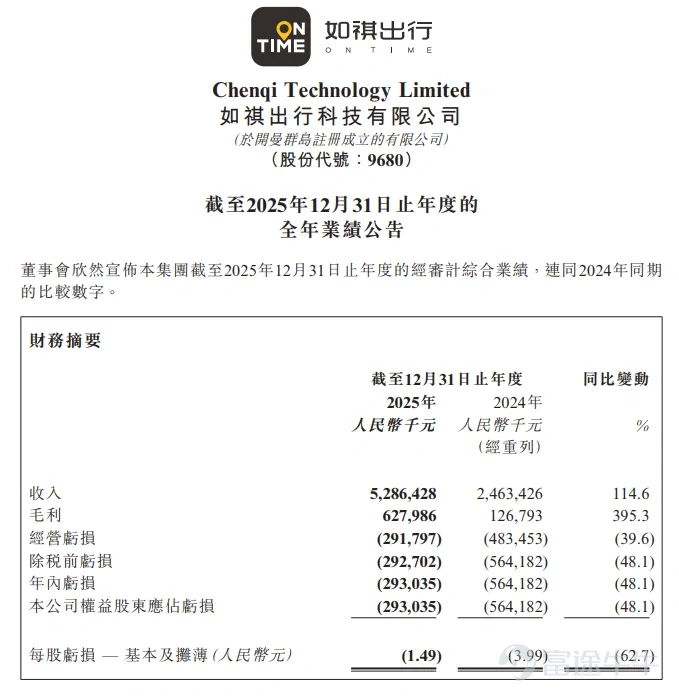

First, looking at the 2025 annual report disclosed by the company, the most notable aspect remains the company's revenue growth. The current expansion can primarily be attributed to the rapid increase in order volume, with both orders and revenue doubling.

By comparison, the revenue growth rate for the ride-hailing industry in 2025 was not particularly high. Didi, as the largest platform, saw an overall order growth rate of around 10%, and the nationwide growth rate was similar to Didi's. Therefore, it's clear that Ruqi’s market share in the ride-hailing sector is quickly increasing. This is largely due to the rapid development of ride-hailing services on aggregation platforms like Amap, which collaborates with Ruqi, boosting its order volume. Essentially, this growth is replacing the market share previously held by self-operated fleets of other platforms. Additionally, this is driven by economies of scale in the company’s management, making drivers more willing to join Ruqi Mobility.

The ride-hailing brands are rapidly consolidating. Compared to self-operated fleets by platforms, Ruqi Mobility's business model appears more dynamic, which is the core trend observed in the financial reports.

Since disclosing data starting in 2021, Ruqi Mobility’s total revenue has continued to grow each year from 2021 to 2024, while net profit margins have also shown continuous improvement.

From the 2025 financial report, it’s clear that the company's growth rate in the second half of the year accelerated significantly. In the first half, the company’s revenue growth rate was only 61%, but in the second half, it surged to 150%, showing strong acceleration. If this trend continues, next year’s revenue growth remains highly promising.

Some sell-side reports project expectations of another doubling in growth for 2026, reaching around 10 billion yuan. Given the current growth trajectory, achieving this goal appears quite reasonable.

Examining the company's financial status, it is evident that profitability metrics are improving in tandem. Gross margin rose from 5.1% to 11.9%. As revenue grows, gross margin is expected to continue trending upward.

Selling expenses increased in tandem with revenue, but the selling expense ratio dropped from 14.5% to 13.4%. Meanwhile, administrative and R&D expenses even declined. From this perspective, as long as the gross margin increases and the selling expense ratio continues to decrease while other expenses remain unchanged, the company's profit model can easily become viable.

Theoretically, with 10 billion in revenue, a 15% gross margin, and a 14% comprehensive expense ratio, the company could achieve a 1% net profit margin. A 1% net profit margin already implies 100 million in profit, which would fully justify the company’s current valuation of 1.6 billion Hong Kong dollars. However, for companies like Xiaoma that focus on autonomous driving solutions, rationalizing their valuation would require them to reach at least hundreds of millions in profit.

Importantly, the company's performance is commendable when compared to its peers. Similarly benefiting from growth driven by platform aggregators such as AutoNavi, Caocao Mobility's growth rate is lower than that of Ruqi Mobility. Caocao’s revenue growth is only 38%, while its gross margin stands at 9.4%, lower than Ruqi’s. Additionally, it has not managed to reduce the selling expense ratio in core cost control, so Caocao Mobility remains unprofitable overall.

In terms of cross-sectional comparison, Ruqi Mobility stands out in both the speed and quality of its growth within the industry.

II. The Impact of Robotaxi Business on the Company

Regarding the development of the robotaxi business, the company began its layout in 2021. As autonomous driving technology iterates and gradually enters L4, the company scales up its robotaxi operations based on industry progress. Currently, several leading domestic robotaxi companies are actually long-term partners of Ruqi.

As of March 2026, the company’s fleet of robotaxis has expanded to 600 vehicles, covering the Greater Bay Area. Compared to the end of last year, capacity has doubled, and over the next five years, the company expects continued expansion to support a robotaxi fleet reaching ten thousand vehicles. This will be roughly equivalent to the current scale of ride-hailing vehicle capacity.

The current hybrid operating model, which involves gradually incorporating robotaxis into the fleet, means that customers occasionally encounter robotaxis when ordering rides through Ruqi, rather than launching a separate new business line. This approach balances technology, costs, and market acceptance. If the passenger experience is indistinguishable and the return on investment exceeds that of human-driven models while order volumes remain stable, the company can utilize robotaxis to further improve profitability.

It is currently difficult to calculate the return on investment for robotaxis within Ruqi’s operational system due to the inherent trade-offs between human-driven benchmarks, vehicle costs, and safety factors. However, if the company accelerates the scaling of its robotaxi fleet, this would indicate that the economics are working.

Given the current business model, the market often worries that in the future, the entire ride-hailing industry might be dominated by robotaxi companies. However, based on collaborations with companies like Xiaoma and WeRide, Ruqi maintains cooperative rather than competitive relationships with them. Developers of robotaxi technology do not wish to handle everything themselves; tasks such as terminal vehicle maintenance and energy replenishment still require substantial manpower, making it more efficient to leave these responsibilities to traditional ride-hailing operators.

Maintaining their own fleet requires significant cash flow for product expansion, and their capabilities are insufficient to complete it. Companies like祺出行 still provide important end-value. In fact, Didi's traditional ride-hailing business has gradually shifted from a self-operated model to a third-party aggregation model, which already provides some reference value.

On the other hand, the company’s robotaxi business is not just a user role but also involves joint development. The company’s technology service business itself uses collected data to charge autonomous driving R&D companies or mapping companies. This segment of the business achieved nearly six times growth last year and is closely related to robotaxis. Therefore, the development of the robotaxi business not only improves the return on investment and lowers costs compared to human-driven vehicles but also generates additional revenue.

In this industrial chain, the company’s role is still in applying AI and executing its industrialization, similar to the model of purchasing computing power and converting it into revenue. Since everyone expects NVIDIA's core business to be selling chips and only selling chips, while downstream there are still multiple layers and various companies thriving together, the autonomous driving industry is no different.

Due to significant uncertainties in the technical path, smart driving R&D companies face competitive-level technological risks, including incorrect choices in technology routes and excessive investment. However, the niche that 如祺 occupies does not carry as much

technological risk. They simply use whatever solution is best and most cost-effective for their fleet. The company can focus on strengthening its existing order volume, operational scale, and brand. Therefore, in terms of the robotaxi industry, the company actually faces fewer uncertainties in R&D.

III. Analysis of the Company's Liquidity Issues

Currently, the company’s liquidity remains insufficient, which is a major concern for investors who worry about buying shares and being unable to sell them. To address this, there are two paths to enhance liquidity: either through undervalued stocks generating substantial dividends to provide real cash returns to investors, thereby injecting liquidity.

Or by demonstrating clear business growth that drives valuation or profit recovery; as the stock price rises, liquidity will naturally improve.

As for 如祺, its recovery path will definitely be driven by earnings growth. There are already initial signs of progress in revenue, and looking ahead to 2026, if high growth continues alongside profitability recovery, the company could achieve an attractive low-valuation state. As mentioned earlier, reaching a profit of 100 million isn’t too difficult for the company’s business model. Once results come out with strong growth rates, liquidity issues will resolve themselves.

The key step still lies in the improvement of the company’s profitability, and at least for now, prospects look good heading into 2026.

The growth of the robotaxi business will also serve as an option for increasing the company's valuation, as the market has yet to fully factor in the long-term prospects of the robotaxi business into the company’s current valuation.

Summary and Core Conclusions

Therefore, after the earnings report, it is evident that Likeqi Mobility has shown outstanding operational performance. Maintaining high revenue growth through 2026 could lead to significant profits. An improvement in profitability, combined with high growth rates, will naturally enhance liquidity, especially since the current market capitalization is relatively small.

More importantly, the company stands to benefit from the development of robotaxis rather than being replaced by them, as autonomous driving companies won't handle everything. The core logic of this industry is that robotaxis must generate positive returns for buyers. Looking ahead, robotaxis are expected to accelerate the company’s profitability improvements, offering greater revenue potential compared to human-driven profit-sharing models.

It is clear that the company has started rapidly expanding its fleet size, and the proportion of robotaxis in the fleet will continue to grow. In the future, it will become a key player that cannot be overlooked in the robotaxi industry. Given that the market’s understanding of the autonomous driving sector is still incomplete, and many investors have yet to notice companies like Likeqi Mobility, this presents an opportune moment for attention, focus, and investment.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment