The reevaluation of innovative drug stocks is happening right now—did you get in on this wave?

A new dawn for the biotech sector: Solid fundamentals combined with a recovery in risk appetite

Report date: April 1, 2026

Summary of Key Insights

After approximately five months of adjustment, the Hang Seng Biotech Index rebounded by 5.6% on March 27, successfully breaking through the 20-day moving average with significant trading volume expansion. The core reasons for this round of adjustment were sector rotation and a decline in risk appetite triggered by Middle Eastern conflicts. However, over the past five months, the fundamentals of the biotech industry have continued to deliver — the majority of companies reported strong 2025 earnings and provided optimistic guidance for 2026, while the amount and number of licensing deals for innovative drugs reached record highs. As geopolitical tensions ease, market risk appetite is expected to bottom out and recover. Accumulated positive fundamental information, combined with less crowded positioning, may drive the biotech sector into an outperformance phase.

I. Two Core Reasons for the Adjustment: Sector Rotation and Geopolitical Risks

The Hang Seng Biotech Index has undergone an adjustment period of about five months since Q4 2025, primarily influenced by two major factors:

First, the effect of sector rotationIn recent months, market funds have significantly flowed into sectors such as non-ferrous metals, energy, and AI supply chains (e.g., storage), leading to noticeable capital outflows from growth sectors like biotechnology. This rotation reflects short-term changes in market preference rather than deterioration in the fundamentals of the biotech industry.

Second, geopolitical conflicts suppressed risk appetiteSince the beginning of the year, tensions in the Middle East have remained high, increasing global risk aversion and putting pressure on the high-beta biotech sector. However, recent developments in the Middle East have shifted to a more 'neutral' scenario — neither ending immediately nor escalating further, with conflict intensity decreasing and the number of vessels passing through the strait rising again. Although the U.S., Israel, and Iran each hold different positions, actual military conflict has eased, and geopolitical risk premiums are gradually dissipating.

II. Continuous Delivery of Fundamentals: Solid Performance, Record Licensing

In sharp contrast to the stock price adjustment, the fundamentals of the biotech industry have continued to improve over the past five months, reflected in three dimensions:

First, steady performance. Recent earnings reports show that the vast majority of biotech companies delivered solid results for 2025 and provided positive guidance for 2026. Take the top two index components as examples:

• Innovent Bio ($INNOVENT BIO (01801.HK)$ ): According to a JPMorgan report, Innovent Bio achieved RMB 13 billion in sales revenue in 2025 (a year-on-year increase of 38%), with product sales reaching RMB 11.9 billion (a year-on-year increase of 45%), meeting expectations. 2025 marked the company’s first year of full-year profitability, with gross margin improving by 2.3 percentage points year-on-year. Management reiterated the target of achieving RMB 20 billion in product sales by 2027 (a compound annual growth rate of about 30% from 2025 to 2027), with contributions from non-oncology drugs (weight loss, ophthalmology) set to surpass those from oncology drugs.

• Akeso Biopharma ( $AKESO (09926.HK)$ ): According to a JPMorgan report, Akeso Biopharma's revenue reached RMB 3.06 billion in 2025 (a year-on-year increase of 44%), with commercial sales growing by 51.5% (after deducting distribution costs). The company has ample cash reserves of RMB 9.17 billion, providing sufficient financial flexibility for R&D investment and pipeline expansion. JPMorgan noted that the company's management expressed increased confidence in the key clinical data for its core product Ivonescimab, with several important data releases expected in 2026, including interim OS data from HARMONi-6 and final OS data from HARMONi-2.

Second, record-high licensing amounts and volumes. The latest data from the National Medical Products Administration shows that the high level of activity in the industry will continue into 2026 —In the first three months of this year, the total value of China’s innovative drug licensing deals has exceeded USD 60 billion, close to half of the total for the whole of 2025.In the same period, the National Medical Products Administration (NMPA) has approved 10 innovative drugs for marketing, eight of which are domestically produced innovative drugs. This strong start fully demonstrates the resilience and sustained potential of China's innovative drug industry.

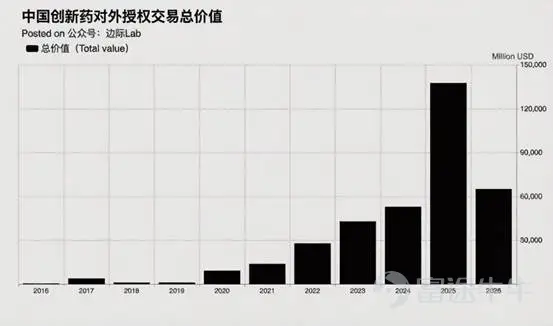

Data source: Marginal Lab x FinGraph, as of April 1, 2026.

Looking at a longer timeframe, the total value of China's innovative drug out-licensing deals in 2025 exceeded $130 billion, with over 150 deals completed—representing a leap from $51.9 billion and 94 deals in 2024. The deeper meaning behind this data is as follows:

– Out-licensing scale achieves exponential growthThe total value of out-licensing deals in 2025 nearly doubled compared to 2024, far surpassing the annual total for 2024. China accounts for about 30% of the global pipeline of new drug candidates under development, ranking second globally, providing ample project reserves for continuous out-licensing.

– Significant increase in overseas recognitionThe NMPA explicitly stated that 'the significant growth in out-licensing reflects international recognition of the value of China’s innovative drugs.' In 2025, China approved 11 first-in-class drugs, four of which were independently developed, marking a shift from catching up to running neck-and-neck, and even leading in some areas within biomedicine.

– Policy benefits continue to be releasedIn 2025, China approved 76 innovative drugs for marketing, significantly surpassing 48 in 2024, setting a new historical high. Of these, domestic chemical drugs accounted for 80.85%, and domestic biologics accounted for 91.30%, reflecting a marked improvement in domestic innovation capabilities. Starting from 2026, the NMPA has announced it will further allocate review resources to clinically urgent products and improve data protection and market exclusivity systems, providing institutional support for long-term industry development.

Third, multinational pharmaceutical companies continue to double down on China’s supply chain.Eli Lilly and Co recently announced a $3 billion investment in China over the next decade to enhance supply chain capabilities, demonstrating that American pharmaceutical companies are not concerned about decoupling from the Chinese supply chain. The long-term strategies of multinational pharmaceutical companies provide a stable external cooperation environment for the development of China’s biotech industry.

III. Portfolio Structure and Risk Appetite: Inflection Point Signals Emerge

After five months of adjustment, the crowdedness of holdings in the biotech sector has significantly decreased, providing room for subsequent rebounds in terms of chip structure. Meanwhile, the following signals indicate that risk appetite is expected to bottom out and recover:

• Technical Aspect: The index rebounded by 5.6% on March 28, successfully breaking above the 20-day line with increased trading volume, showing bottoming characteristics in the technical aspect.

• Geopolitical Aspect: Intensity of Middle East conflicts has eased, with the number of ships passing through the strait recovering; geopolitical risk premiums are gradually dissipating, which is beneficial for capital to flow back into high-Beta growth sectors.

• Capital Aspect: Funds previously flowing into sectors such as non-ferrous metals, energy, and AI storage now have the potential to return to the biotech sector, which has relatively reasonable valuations and solid fundamentals after significant gains in related sectors.

Conclusion: A Resonance Window of Fundamentals and Sentiment

Overall, the Hang Seng Biotech Index, after five months of adjustment, has already factored in negative factors such as sector rotation and geopolitical risks fairly thoroughly. At the same time, the sector's fundamentals continue to improve — with steady performance from leading companies like Innovent Bio and Akeso Inc., record-high outbound licensing deals, and multinational pharmaceutical companies continuing to increase their investments in China’s supply chain. As geopolitical conflict intensity eases, market risk appetite is expected to bottom out and recover, and previously accumulated positive fundamental information combined with a less crowded portfolio structure could translate into outperformance momentum for the biotech sector.

For investors focusing on China’s biotech industry, the current range is worth close attention.

China AMC Hang Seng Biotech ETF (3069.HK) — One-click allocation to leading biotech companies in the Hong Kong stock market

The China AMC Hang Seng Biotech ETF tracks the Hang Seng Biotech Index, which includes a group of globally competitive Chinese biotech companies such as Innovent Bio and Akeso Inc., providing investors with a convenient, efficient, and risk-diversified allocation tool to capture long-term growth opportunities in the biotech industry.

$WUXI BIO (02269.HK)$$BEONE MEDICINES (06160.HK)$$INNOVENT BIO (01801.HK)$$AKESO (09926.HK)$$CSPC PHARMA (01093.HK)$$SBP GROUP (01177.HK)$$HANSOH PHARMA (03692.HK)$$3SBIO (01530.HK)$$WUXI APPTEC CO LTD UNSPON ADS EACH REP 1 ORD SHS (WUXAY.US)$$SSE Composite Index (000001.SH)$$CSI 300 Index (000300.SH)$$NVIDIA (NVDA.US)$$Amazon (AMZN.US)$$Alphabet-C (GOOG.US)$$Meta Platforms (META.US)$$Tesla (TSLA.US)$$HSTECH (LIST91332.HK)$$Hang Seng Index (800000.HK)$$SSE 50 Index (000016.SH)$$CSI 300 Index (000300.SH)$$CSI 1000 Index (000852.SH)$$SSE Science and Technology Innovation Board 50 Index (000688.SH)$$ChinaAMC CSI 300 Index ETF (03188.HK)$$SSE Composite Index (000001.SH)$$XIAOMI-W (01810.HK)$$JD.com (JD.US)$$TENCENT (00700.HK)$$Shenzhen Component Index (399001.SZ)$$Kweichow Moutai (600519.SH)$$Contemporary Amperex Technology (300750.SZ)$$PING AN (02318.HK)$$Alibaba (BABA.US)$$ICBC (01398.HK)$$CHINA MOBILE (00941.HK)$$ABC (01288.HK)$$Midea Group Co., Ltd (000333.SZ)$

Important information about the China AMC Hang Seng Biotech ETF

Investment involves risks, including the loss of principal. Past performance is not indicative of future results. Before investing in the China AMC Hang Seng Biotech ETF (the "Fund"), investors should refer to the fund prospectus, particularly the risk factors. You should not rely solely on this material to make investment decisions. Please note:

• The Fund aims to provide investment performance that closely matches the Bloomberg Asia Pacific Dividend 40 Net Total Return Index (HKD) before fees and expenses.

• The Fund primarily invests in high-yield stocks in Asia. High dividend securities may be affected by risks such as reduction or cancellation of dividends, decline in security value, and lower-than-average price appreciation potential.

• Investments in Asian markets / emerging markets are more susceptible to adverse economic, political, policy, foreign exchange, liquidity, tax, legal, or regulatory events affecting Asian markets, or may face greater losses due to political, tax, economic, foreign exchange, liquidity, and regulatory risks compared to investments in more developed markets.

• The Fund is exposed to industry concentration risk and risks associated with small- and mid-cap companies, which may result in significant fluctuations in the Fund’s value.

• The Fund faces new index risk, rebalancing period risk, and historical performance risk.

• The trading price of the Fund may show significant premiums or discounts relative to the net asset value per unit.

• This fund is exposed to tracking error risk.

• This fund is exposed to risks associated with financial derivative instruments, including counterparty/credit risk, liquidity risk, valuation risk, volatility risk, and over-the-counter trading risk.

• This fund is subject to foreign exchange risk.

• Listed and unlisted classes follow different pricing and trading arrangements. Due to varying fees and costs, the net asset value per unit of each class may differ.

• Units of the listed class are traded on the secondary market at the current market price, while units of the unlisted class are sold through intermediaries based on the end-of-day net asset value on the transaction date. Investors in the unlisted class can redeem their units at net asset value, whereas investors in the listed class on the secondary market can only sell at the prevailing market price and may have to exit the fund at a significant discount. Investors in the unlisted class may be at an advantage or disadvantage compared to investors in the listed class.

• The fund may at its discretion pay dividends from the capital of the fund or actually from the capital. Payment of distributions from the capital or effectively from the capital amounts to returning or withdrawing part of the investor’s original investment or any capital gains attributable to that original investment. Any such distribution may result in an immediate reduction in the fund's net asset value per unit.

JPMorgan, as of March 2026. Innovent Bio (1801.HK) and Akeso Biopharma (9926.HKAnalysis and data sourced from JPMorgan's research reports published on March 27 and March 30, 2026. Performance data of the Hang Seng Biotech Index sourced from Bloomberg, as of March 28, 2026. Out-licensing and innovative drug approval data sourced from the National Medical Products Administration and CCTV News App: Full-year 2025 data (https://mp.weixin.qq.com/s/KoHWE_cdG-vTBIlPABVMwQ), First Quarter 2026 data (https://mp.weixin.qq.com/s/tPh6zCpJgevxt6mK6CU6Cw). Eli Lilly and Co investment information sourced from company public announcements. Market data, case studies, and industry observations mentioned in the article are for illustrative purposes only, derived from public media reports and industry research, and do not constitute investment advice.

Investment involves risks, including possible loss of principal. Any forecasts, outlooks, or opinions contained herein are for your reference only and are not guaranteed. The information contained herein reflects market conditions and our views as of the publication date, and any changes will not be notified separately. This material is issued by China AMC (Hong Kong) Limited. This material has not been reviewed by the Securities and Futures Commission of Hong Kong. For full details and risks related to the funds mentioned, please refer to our official website and prospectus.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

5

1