Everbright Bank 'Explodes with Risk': Quarterly Profit Plummets 44.9%, Real Estate-Related Loans Become Major Source of Bad Debts

Everbright Bank, whose total assets have reached the 7 trillion yuan mark, delivered an annual report in 2025 showing a dual decline in operating income and net profit.

However, what truly shocked the market was the sharp drop in Q4 profitability: the net profit attributable to parent company shareholders for the quarter was only 1.808 billion yuan, plunging 44.91% year-on-year, driven by credit impairment losses amounting to 17.588 billion yuan for the quarter.

The Mystery Behind Everbright Bank's Q4 'Bleeding': Credit Impairment Losses Soar to 17.5 Billion

In 2025, Everbright Bank reported operating revenue of 126.311 billion yuan, a year-on-year decrease of 6.72%. Net profit attributable to shareholders reached 38.826 billion yuan, down 6.88% year-on-year. The data shows that its revenue has fallen into an awkward situation of 'four consecutive declines', while net profit failed to continue the rebound seen in 2024.

However, what surprised the market most was the cliff-like drop in Q4 net profit. In the first three quarters of 2025, Everbright Bank’s quarterly net profit attributable to shareholders exceeded 12 billion yuan each quarter. In contrast, in Q4, the company’s net profit attributable to shareholders for the quarter was only 1.808 billion yuan, plummeting 44.91% year-on-year.

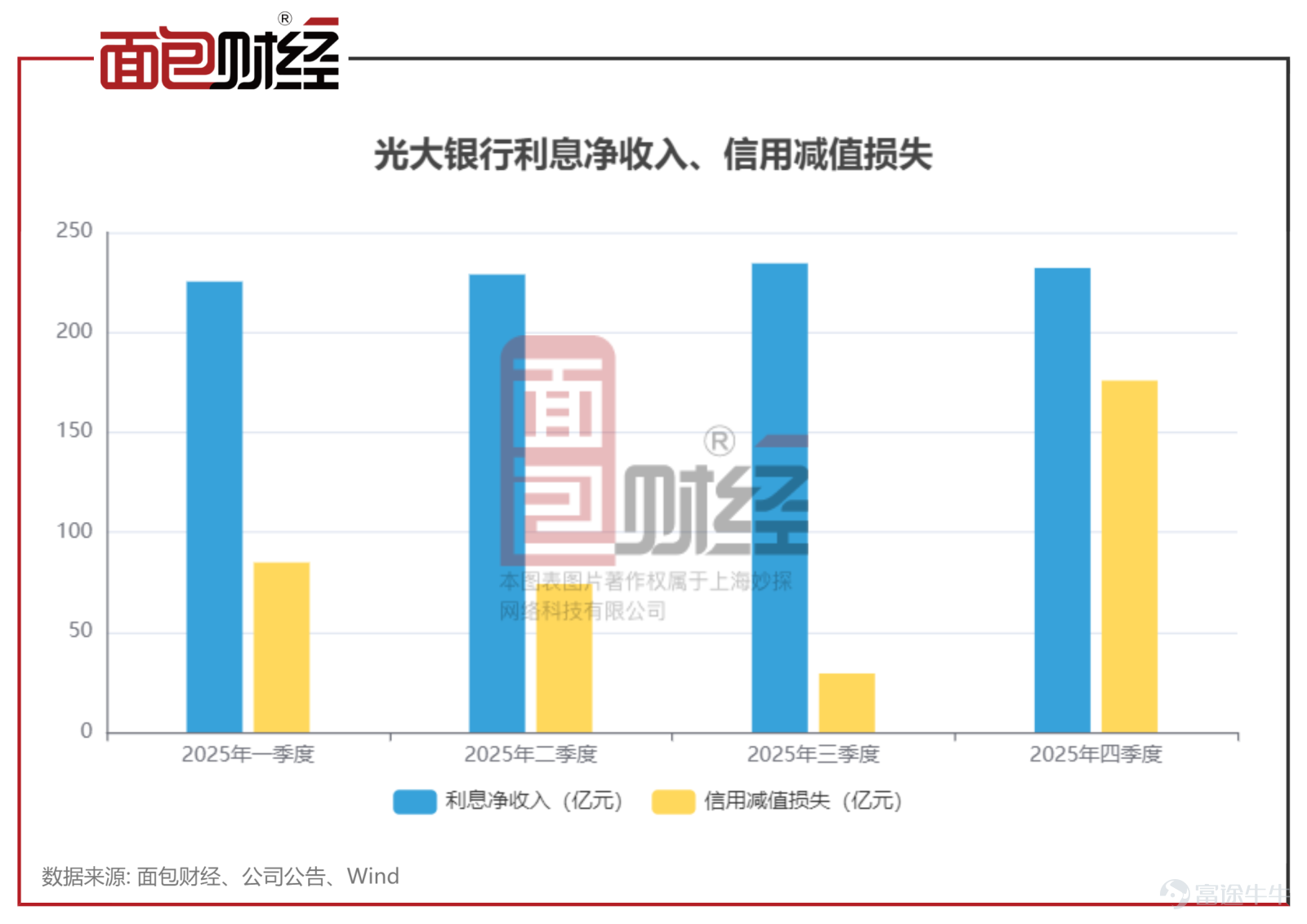

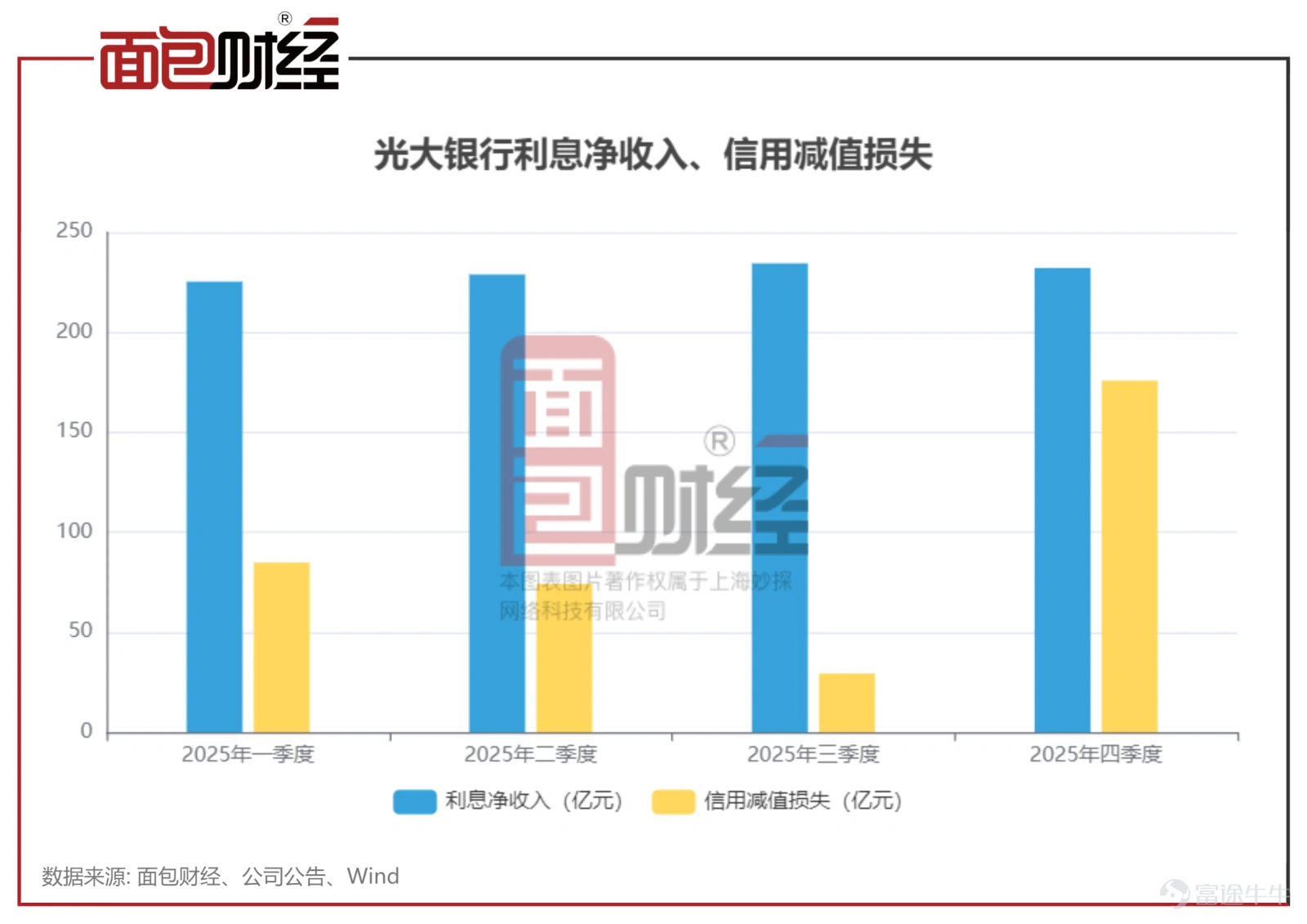

In Q4 2025, Everbright Bank's net interest income remained at over 20 billion yuan, indicating its lending profitability remains intact. However, on the other hand, credit impairment losses surged to 17.588 billion yuan, nearly six times that of Q3 (2.936 billion), accounting for nearly half of the total annual provisions. This massive 'risk reserve' acted like a beast, swallowing up most of the profits that should have belonged to shareholders, causing net profit to drop from over 10 billion yuan to just 1.8 billion—a dramatic plunge.

According to the earnings briefing, Everbright Bank significantly increased its provisioning efforts in Q4 2025, mainly focusing on retail business. The real estate sector continues to face unfavorable market conditions, impacting retail loans, especially those related to real estate, which bear significant risk pressure.

Asset Quality Alert: Provision Coverage Ratio Falls Below 175%

On the flip side of the earnings pressure is the quiet 'deterioration' of asset quality.

By the end of 2025, Everbright Bank's non-performing loan balance surpassed the 50 billion yuan mark, increasing by 1.49 billion yuan from the end of the previous year; the non-performing loan ratio rose slightly to 1.27%, up 0.02 percentage points from the end of the previous year.

Behind the numbers lies a signal of tightening risks across the board: the watch list loan ratio rose to 1.85%, and the overdue loan ratio climbed to 2.13%. Both key risk indicators moved upward simultaneously, indicating growing pressure from future risk exposure.

More alarmingly, the provision coverage ratio, often considered the bank's 'anti-risk ammunition', continued its downward trend since 2023, dropping by 6.45 percentage points to 174.14% by year-end, reflecting a weakening ability to withstand risks.

An analysis of the industry distribution of non-performing loans at Everbright Bank reveals that the real estate and manufacturing sectors, two major industries, have both experienced significant increases in non-performing loan balances. The balance of non-performing retail loans has also risen year-on-year, becoming the primary 'reservoir' of risk. With existing risks yet to be fully addressed, Everbright Bank's campaign to safeguard asset quality remains an uphill battle.

(Article Serial Number: 2039238464704221184/GJ)

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

2