Buffett Holds $370 Billion in Cash on the Sidelines: Are US Stocks Overvalued? Have Tech Giants Dropped Into the 'Sweet Spot'?

Overnight, Buffett's comments during an interview sparked heated market discussions.

Facing the recent pullback in US stocks, this legendary investor, who has weathered both bull and bear markets, stated directly:

The stock market valuation still lacks appeal; if the market crashes, Berkshire will deploy its cash.

Currently, Berkshire is sitting on over $370 billion in cash and Treasury bills. Despite the Dow Jones and Nasdaq indices falling into technical correction territory, and Apple dropping more than 14% from its peak, Buffett remains unmoved.He admitted that Apple is 'still not cheap enough.' While he may buy significantly at a certain sweet spot in the future, it definitely won’t be in the current market.

The Oracle of Omaha’s decision to 'stay put' has left many investors eager to bottom-fish feeling anxious:Are US stocks really too expensive? If we enter now, will we end up buying at a halfway point?

For investors focusing on steady asset growth, while we respect the market, we need to use data to cut through the fog. An analysis of the current valuation structure reveals that the true "money-making effect" has not completely vanished but has undergone a deepstructural fold.

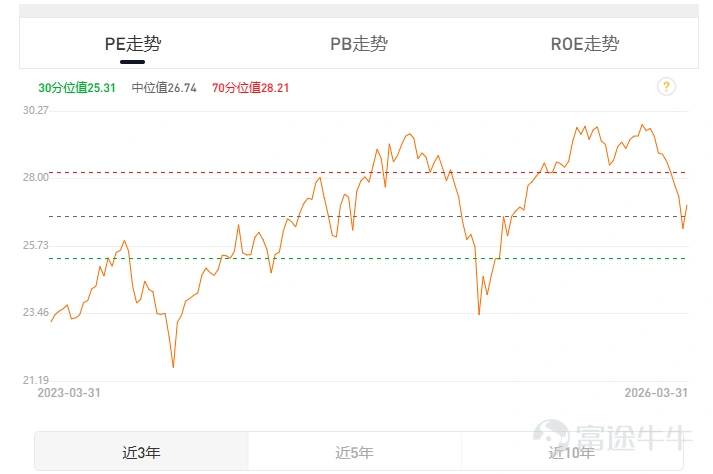

1. Macro Perspective: The index is not overvalued, and is approaching the "sweet spot for investment."

Buffett's belief that the overall market lacks appeal is based on his massive capital base and strict absolute return requirements. However, if we objectively review the market data, the valuation of US stocks has actually returned from "extreme exuberance" to a "relatively reasonable" range. Observing the P/E trend of the broader market over the past three years, we can clearly see:

After the recent pullback, $S&P 500 Index (.SPX.US)$ the P/E level once dropped below the median value (26.74), and the overall valuation has retreated to where it was in May of last year.

What does this mean? It indicates that the systematic risk of "valuation compression" in the broader market has been largely released. For investors with smaller capital bases and higher flexibility,the market has entered a "sweet spot" where investments can be made in batches, rather than a time for blind panic.

2. Micro Dissection: Internal "Valuation Folding" Among Tech Giants and Profitability Effects

Since the broader market already offers certain value for money, why does Buffett still think Apple is expensive?

The answer lies within the internal dynamics of the tech giants'divergence in earnings expectations. The real 'profit effect' always follows those companies that can quickly digest high valuations with strong earnings growth.

By comparing the valuations of core technology stocks, we discover a highly counter-intuitive phenomenon:

giants facing growth bottlenecks still maintain high valuations: $Apple (AAPL.US)$ 's Forward P/E is still as high as 27.28. In the absence of explosive new growth curves, this valuation is indeed unattractive to Buffett-like investors who prioritize a margin of safety. Additionally, $Tesla (TSLA.US)$ is trading at an even higher Forward P/E of 141.

The real AI core assets, on the other hand, are 'the cheapest':In comparison,Among the current U.S. tech giants, the one with the lowest Forward P/E is actually the best performer, $NVIDIA (NVDA.US)$ ,with a Forward P/E of just about 15.69; while $Meta Platforms (META.US)$ The forward P/E ratio is only at 16.51, and additionally, $Broadcom (AVGO.US)$ 、 $Taiwan Semiconductor (TSM.US)$ 、 $Microsoft (MSFT.US)$ the forward P/E ratios are all below the overall level of the S&P 500 index.

This is the most crucial cognitive gap in the current market: high market capitalization does not equal high valuation. The 'money-making effect' of capital is highly concentrated in those AI infrastructure and commercialization leaders with extremely strong earnings certainty and significantly undervalued long-term valuations.

III. Investment Strategy: How to replicate the sage's 'steady pursuit of victory'?

For ordinary investors, Buffett’s wait-and-see approach doesn’t mean we should liquidate our positions and exit; rather, it teaches us how to make more refined asset allocation and risk management during volatility. In the current turbulent market environment, investors can adopt the following strategies:

1. Build a 'cash fortress' to retain strategic initiative

Never go all-in. Follow Berkshire Hathaway’s example by keeping sufficient cash or cash-like assets (e.g., short-term US Treasuries or money market funds) in your account. This serves not only as a shield against extreme tail risks but also gives you the confidence to pick up bargains when a 'once-in-a-century crash' occurs.

2. Avoid blind investments, precisely targeting 'low forward P/E' giants

In the current volatile market, Beta (market-wide) returns are diminishing while Alpha (individual stock) returns are becoming more prominent. Focus your resources on mispriced assets like NVIDIA, which have forward P/E ratios between 15-20x, robust cash flows, and strong earnings certainty.

3. Execute 'pyramid-style' phased position building

Instead of guessing the absolute bottom, focus on the valuation percentile. With the current index approaching the median line, it's appropriate to start building an initial position. If future macro events cause the index to drop further to 20% or even lower historical bottoms, gradually increase the buying proportion.

IV. Conclusion

Buffett might be waiting for a macro-level storm, but we can certainly pick up those mispriced pearls on the beach before the storm arrives. Identify reasonable support levels for the broader market, target undervalued areas within tech giants, remain patient, and enter the market in batches—this is currently the investment approach with the highest probability of success.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (21)

to post a comment

57

197