Double-digit profit growth confirms a fundamental turnaround, with Tiangong International (00826) entering a high-certainty phase of accelerated growth

Tiangong International (00826) $TIANGONG INT'L (00826.HK)$ The 2025 earnings announcement released on March 30 sent a clear positive signal to the market.

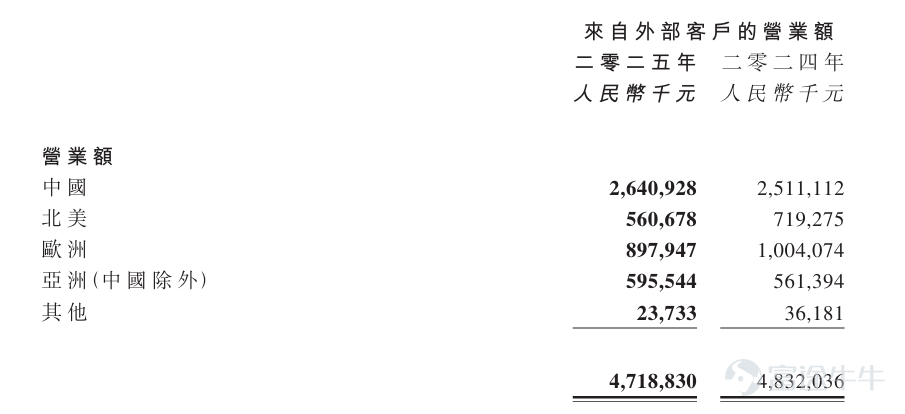

According to the financial report, Tiangong International's revenue in 2025 was approximately 4.719 billion yuan (RMB, hereinafter), with shareholder net profit of about 400 million yuan, representing an increase of 11.5% year-over-year. The double-digit growth in profitability indicates that after three years of phased adjustments, Tiangong International has returned to a growth trajectory.

Focusing on the second half of the year, the recovery trend in Tiangong International’s fundamentals became increasingly evident. Data shows that in the second half of 2025, Tiangong International’s revenue was 2.376 billion yuan, up 2.85% year-over-year, with shareholder net profit at 197 million yuan, up 12.73% year-over-year. The dual growth in revenue and profit reflects stronger growth momentum for Tiangong International in the second half, with overall operations showing an accelerating positive trend.

A deeper analysis of this earnings report reveals that Tiangong International’s long-term commitment to its premium product strategy has entered the harvest phase, with results becoming increasingly apparent. This is not only expected to drive Tiangong International into a new growth cycle, but also gradually gain market recognition, allowing it to benefit from a higher valuation premium brought by premiumization.

The domestic market demonstrated resilience with steady development, as high-speed steel and cutting tools experienced both volume and price increases.

In 2025, the high-end new materials manufacturing industry progressed amidst challenges and opportunities. On one hand, global tariff frictions escalated again, geopolitical tensions continued, uncertainty in trade policies increased, compounded by ongoing volatility in financial markets, collectively exerting pressure on the global economic recovery and significantly disrupting companies’ international strategies.

On the other hand, China made substantial progress in reform and opening-up efforts in key areas and critical sectors, promoting stable yet progressive economic growth, with its growth rate continuing to lead among major global economies. In this context, sustained demand from key industries such as new energy vehicles, consumer electronics, and high-end equipment manufacturing drove robust growth in domestic niche markets such as high-end high-speed steel.

Industry data shows that in 2025, the market size of high-end steel (including high-speed steel, mold steel, and other specialty steels) expanded further, with significant recovery in related sector demand. Notably, the share of steel used in manufacturing rose to 51%, surpassing construction steel for the first time and becoming the core driver of structural upgrades in the steel industry.

As a high-end new materials manufacturer specializing in specialty steel and advanced alloy materials, Tiangong International benefited from strong domestic demand for specialty steel. In 2025, Tiangong International’s revenue from China was approximately 2.641 billion yuan, increasing by 5.17% year-over-year, with its proportion of total revenue rising from about 51.97% to 55.97%, an increase of nearly four percentage points. This was the key reason for Tiangong International’s steady development despite global disruptions. Meanwhile, revenue from Asia (excluding China) was approximately 596 million yuan, growing by 6.08% year-over-year, making Asia a new regional growth point for the company.

In terms of product mix, the domestic sales performance of mold steel, high-speed steel, and cutting tools during the reporting period stood out. Among these, mold steel domestic sales revenue grew by 3.3% year-over-year to 1.041 billion yuan, reflecting a “stable volume and rising price” trend – sales volumes remained stable supported by demand in domestic sectors such as new energy vehicles and integrated die-casting, while average selling prices increased by approximately 4% due to cost pass-through and improved company pricing power.

Domestic sales of high-speed steel grew particularly strongly, with revenue surging 37% year-over-year to 578 million yuan, mainly driven by 'increased volume and higher prices.' Sales volume rose 12% due to growing demand in the domestic cutting tool industry, while the average selling price increased significantly by 23%, propelled by rising raw material costs and a higher proportion of powder metallurgy and premium products.

Domestic sales of cutting tools also performed remarkably, with revenue increasing 19.9% to approximately 400 million yuan, achieving 'volume and price growth.' Sales volume rose 6.8% year-over-year alongside the recovery of downstream industries such as automotive and machinery, while the average selling price increased 12.4% driven by demand for high-end cemented carbide tools.

The titanium alloy business faced some pressure during the reporting period, generating revenue of about 626 million yuan, mainly affected by the iteration pace of key customers in the consumer electronics sector. However, the company still managed to push titanium alloy product sales up 14% year-over-year by continuously expanding into diversified industries, laying the groundwork for future recovery.

Multi-dimensional factors are driving Tiangong International to accelerate into a new growth cycle.

If we say that Tiangong International’s performance in 2025 has bottomed out and started to recover, then entering 2026, driven by strong domestic market demand, effective price transmission, and the rapid scaling-up of premium products, Tiangong International will enter a new growth phase.

In terms of domestic market demand,2026 is expected to maintain strong growth, which will drive Tiangong International's domestic business to continue playing a 'stabilizing' role and demonstrate higher growth elasticity. In 2025, the special steel industry already showed a trend of 'total volume increase, structural upgrade, and accelerating substitution,' with the proportion of premium special steel output rising to 28%. This trend is expected to strengthen further in 2026.

With the government setting an annual GDP growth target of 4.5%-5% and explicitly promoting 'new quality productive forces' and high-quality growth, strategic industries such as high-end manufacturing, new energy, and ultra-high voltage power grids are entering a phase of accelerated development. Against this backdrop, high oil prices will boost global sales of China’s new energy vehicles, thereby driving up demand for mold steel. Additionally, the recovery and upgrading of industries such as automotive, machinery, aerospace, and electronics, along with the benefits of import substitution, will continue to drive demand for high-speed steel and cutting tools. As a leading enterprise in the field of specialty steel and advanced alloy materials, Tiangong International is well-positioned to benefit from this round of structural upgrades in the industry.

In terms of price transmission,By mid-2025, the average selling prices of Tiangong International's mold steel, high-speed steel, and cutting tools have risen to varying degrees, primarily due to the combined effects of continued increases in upstream raw material prices, robust market demand, and a growing proportion of premium products.

Since 2026, geopolitical tensions have continued to escalate, driving up the costs of upstream raw materials rapidly. For instance, tungsten powder, a core raw material for cutting tools, surged over 200% in price throughout 2025, and in the first quarter of 2026, its price increased by more than 118% again. This upward trend is gradually spilling over into other key metal materials. The robust downstream market further reinforces this trend — significant earnings growth reported by industry peers like Okuma Corporation fully demonstrates the strong demand in the CNC tooling sector, also providing a strong reference for the sustained boom in the high-speed steel and cutting tools market.

Tiangong International, as a leading company in the industry, holds significant advantages in business scale and product premiumization, which helps the company smoothly transfer upstream costs to downstream customers, thereby continuously improving profitability. By mid-2025, Tiangong International managed to increase the gross margin of mold steel, whose average selling price saw relatively low growth, to 14.5%, higher than 12.1% in 2024 and 13.8% in the first half of 2025, clearly showing the positive impact of product price increases on profitability. It is foreseeable that with further rises in upstream raw material prices in 2026, all of Tiangong International’s product lines are expected to enter a new cycle of price hikes and profit growth.

In terms of scaling up high-end products,Tiangong International leverages its complete powder metallurgy technology platform to accelerate efforts in three major areas: product upgrades, development of critical 'bottleneck' materials, and raw materials for additive manufacturing (3D printing), pushing the company's product mix towards premiumization.

In product upgrades, Tiangong International continues to enhance the value of its tool and die steel and cutting tools through powder metallurgy technology, thereby steadily raising product prices. Among these, powder steel will begin to scale up in 2026. In July 2025, Tiangong International signed a cooperation agreement with Hengert, under which Hengert will purchase no less than 100 tons of specialized materials for sawing tools annually from Tiangong International over five years, totaling at least 600 tons. The market expects that after establishing a benchmark effect through its collaboration with Hengert, an acceleration in acquiring new customers will drive rapid scaling of powder steel.

In the field of critical 'bottleneck' materials, Tiangong International successfully developed high-nitrogen alloy materials using powder metallurgy technology, achieving commercial breakthroughs especially in the robotics sector. In July 2025, its self-developed high-nitrogen alloy material was delivered to clients and applied in the mass production of planetary roller screws, making it the first domestic supplier to achieve commercial application in this field. Subsequently, the company reached a cooperation agreement with Hengert to further promote the application of high-nitrogen steel in precision screw manufacturing. Going forward, this material is expected to scale up rapidly in the robotics field and continue to penetrate into more high-end industries such as aerospace and medical devices.

Meanwhile, Tiangong International also uses powder metallurgy technology to produce fusion materials. Currently, Tiangong International has made breakthroughs in advanced reduced-activation ferritic/martensitic (RAFM) steel and high-boron steel (304B7) used in nuclear power, with respective demand estimated at 4,000-7,000 tons per fusion reactor and 400-4,000 tons per fusion reactor, indicating a broad market space.

In the area of raw materials for additive manufacturing, Tiangong International owns the largest powder production equipment in the country, with particle sizes ranging from 0 to 500 μm, meeting the requirements of various forming processes. Currently, the company has developed four major categories of metal powder materials, with high-alloy steel powder being its core advantage, boasting an annual production capacity of 8,000 to 10,000 tons.

During the reporting period, Tiangong International quickly entered the titanium alloy 3D printing powder sector by jointly establishing Tiangong Titanium Crystal and acquiring the plasma atomization production line of Pind New Materials. This move built a complete closed-loop industrial chain from titanium alloy base materials to 3D printing powders, allowing the company to obtain bulk production processes and existing capacity while enabling early positioning to capture more than 70% of the domestic titanium alloy powder market, which currently relies heavily on imports. This prepares the company well in terms of capacity and supply chains for incremental demand from high-end sectors like consumer electronics and aerospace.

Notably, while Tiangong International leverages powder metallurgy technology to establish a full titanium alloy industrial chain, its titanium alloy business is set to receive two major catalysts. First, the scaled-up application of titanium alloy hinges in foldable smartphones, with Apple's entry likely to ignite the market. Currently, mainstream brands such as Honor, OPPO, Vivo, Samsung, and Xiaomi have already adopted titanium alloy hinges in their foldable models. Moreover, Apple’s first foldable smartphone, planned for release in the autumn of 2026, will feature a titanium alloy frame.

Industry analysis firm Canalys noted that Apple's entry will become a turning point in the development of the foldable screen industry, with global foldable phone shipments expected to achieve 51% year-on-year growth by 2026. This will significantly accelerate the penetration of high-end titanium alloys in the foldable screen sector.

Secondly, the 3D printing titanium alloy technology has already achieved scaled mass production in Apple products, opening up clear opportunities for upstream material markets. Apple has applied this technology in the casing of its latest Apple Watch and the port of the iPhone Air.

The supply chain further indicated that the hinge key components of Apple’s foldable iPhone, set to launch in 2026, are also expected to adopt 3D-printed titanium alloys. Apple's continued adoption of this technology in core components marks the formal transition of 3D-printed titanium alloys from the prototype stage to mainstream high-end manufacturing, strongly driving demand for high-quality titanium alloy powders.

As a potential core supplier of titanium alloy materials for Apple, Tiangong International is expected to directly benefit from the strong pull of end customers. Industry insiders believe that the low point of Tiangong International's titanium alloy business is now behind it, and by 2026, this segment is expected to return to a rapid growth trajectory.

Ending:

As Tiangong International enters a new growth cycle, the company’s performance is highly certain to accelerate. Multiple brokerage firms hold positive views on its future development. CICC recently released a research report highlighting the company’s high growth potential in 3C titanium materials and powder metallurgy products in 2026 and 2027. The report believes that starting from 2026, Tiangong International’s high-end materials business will continue to scale up, driving the company’s transformation from a leader in tool and die steel to a high-end new materials supplier.

CICC forecasts that Tiangong International’s revenue will reach RMB 6.639 billion and RMB 7.376 billion in 2026 and 2027 respectively, with net profits attributable to shareholders at RMB 697 million and RMB 894 million. Based on these earnings projections and the premium valuation brought about by the company’s transition to high-end new materials, CICC raised Tiangong International’s target price for 2026 to HKD 5.29, representing an over 70% upside from the closing price on March 31.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

2