Both are leaders in the consumer-grade 3D printer market, so why is Bambu Lab making a fortune while Creality is struggling to make money?

Years ago, 3D printing was only the subject of popular science videos.

Now, however, 3D printing is entering the public eye at an unprecedented speed.

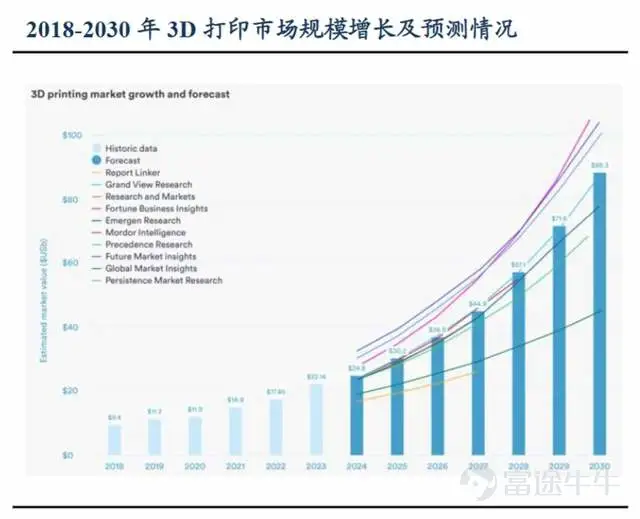

According to data from CIC Consulting, the global market size for consumer-grade 3D printing was $4.1 billion in 2024 and is expected to soar to $16.9 billion by 2029, with an annual compound growth rate as high as 33.0%.

The reaction from the capital markets has been straightforward.

Public data shows that in 2025, 81 domestic 3D printing companies completed 100 rounds of financing, totaling approximately 8.4 billion yuan, setting a new historical record.

Among these numerous companies, Creality was one of the earliest established, and with its cost-effective blockbuster models, it once achieved the highest cumulative shipment volume globally.

However, the path to the capital market has not been smooth. After initiating A-share tutoring at the end of 2023, Creality suddenly terminated the plan in July 2025. In March this year, Creality filed again, starting its push to become the first company in the consumer-grade 3D printing sector on the Hong Kong stock exchange.

Nevertheless, behind all this, the situation remains turbulent.

01 From Industry to Everyday Life

In the consumer-grade 3D printing sector, Creality is a name that cannot be overlooked.

This company, which later achieved the world's largest cumulative shipment volume, actually had a rather 'grassroots' beginning.

In 2014, four strangers met at a 3D printing exhibition and cobbled together the initial prototype of this company in Shenzhen.

Previously, 3D printing was still a typical industrial technology, mainly controlled by overseas manufacturers, and the high equipment costs deterred many consumers.

Therefore, from the very beginning, Creality chose a different path: instead of targeting the industrial market, it directly entered the consumer end.

This approach was soon reflected in its products.

After its establishment, the company mainly focused on 3D printing equipment and consumables, with core products including desktop 3D printers such as the Ender series and CR series.

In 2015, Creality launched its first fully assembled product, the CR-i3, earning its first significant profits. The following year, the CR-10, its first overseas blockbuster product, was born. Priced at 500 USD, it offered print quality comparable to overseas products priced at 1000 USD.

This almost 'disruptive' pricing strategy was no accident.

On one hand, Creality seized the opportunity presented by the rise of the global Maker culture, with rapid growth in demand from overseas DIY users, educational institutions, and others, leading to a continuously expanding market size.

On the other hand, the company greatly benefited from open-source ecosystems like the RepRap Project, quickly iterating its products based on mature technology, thereby achieving scaled replication at a lower cost.

Source: Reprap official website

Since then, Creality rapidly transitioned from being a 'participant' to becoming an 'industry leader.'

Its shipment volume grew from about 17,000 units in 2016 to over 1 million units in 2020, making it one of the representative manufacturers in the consumer-grade 3D printer field.

02 Rapid Growth Hides Concerns

On the surface, Creality 3D continues to develop positively.

From 2023 to 2025, the company’s revenue increased from 1.883 billion yuan to 3.127 billion yuan, nearly doubling in two years, continuing its expansion momentum in the consumer-grade 3D printing market.

At the same time, the second growth curve has started to bear fruit, with the proportion of 3D printer revenue dropping to 57.1%, while businesses such as consumables and scanners have seen continuous growth.

However, on the flip side of this growth, the reality is not so optimistic.

The company's core business, 3D printing, is showing a clear trend of “increasing prices but decreasing volumes.”

According to 36Kr statistics, from 2022 to 2025, the average selling price of the company’s 3D printers increased from 1,306 yuan to 2,404 yuan, but sales fell from 842,000 units to 742,000 units, a drop of 12%.

This means that the growth in Creality 3D’s revenue did not come from expanding demand, but rather relied more on product price hikes.

In an ideal scenario, raising product prices would mean greater profit margins. However, once sales decline, the pressure to allocate fixed costs rises, which could instead shrink overall profitability.

And this trend has already started to show up on the profit side.

In 2025, Creatz3D reported a net loss of 182 million yuan, which the company attributed to non-cash expenses related to pre-IPO dividends and share-based payments. However, even after excluding these factors, the adjusted net profit still declined from 130 million yuan in 2023 to 92 million yuan in 2025, marking two consecutive years of decline.

While profits can be influenced by accounting practices, changes in cash flow more directly reflect the deterioration in the quality of operations.

In 2025, the company's net cash outflow from operating activities reached 64 million yuan, turning negative for the first time. The divergence between reported profits and the lack of cash generation often indicates that a company is maintaining growth through increased investment, or even starting to overdraw its future operational flexibility.

A deeper breakdown reveals that, to address uncertainties in overseas tariffs and logistics, the company opted for large-scale advance inventory purchases, pushing inventory up to 634 million yuan, a year-on-year increase of 44.8%. Meanwhile, accounts receivable grew to 338 million yuan, with an annual increase exceeding 50%.

Overall, growth continues, but the quality of that growth remains far from optimistic. While revenue and product lines are expanding, profits, cash flows, and capital efficiency are all under pressure simultaneously.

In other words, this company is still moving forward, but doing so with increasing difficulty.

03 Intensified Internal and External Challenges

In fact, these pressures are not isolated incidents but rather the result of overlapping internal and external factors.

First, there are changes in the external environment. Creatz3D is highly reliant on overseas markets, with Europe and the US accounting for nearly 60%, and the US market alone representing close to 30%. Fluctuations in tariff policies directly affect product pricing and profit margins.

As of March 1, 2026, its main products exported from China to the US will face high tariffs ranging from 35.0% to 40.8%.

At the same time, stricter regulations in Europe and Southeast Asia have led to a continuous rise in compliance, tax, and product standard costs for businesses.

For example, tighter restrictions by RoHS on heavy metals and flame retardants have directly driven up material and supply chain transformation costs.

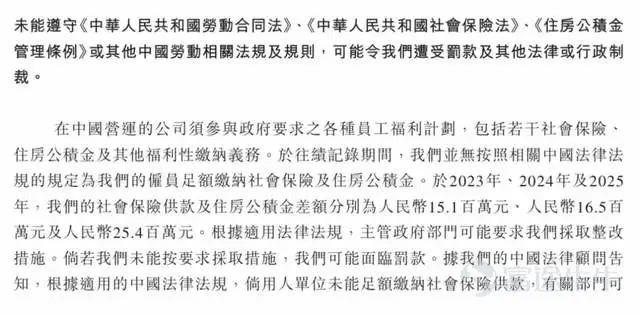

Secondly, there are compliance and legal risks. Issues such as intellectual property-related litigation, as well as historical employment practices and social security contributions, could be magnified during the company’s push to enter the capital market.

In October 2025, Top Bamboo Technology filed a lawsuit against CreateCloud, with key allegations including the mass copying of exclusive paid or contracted models from MakerWorld.

In the same year, the company disclosed a shortfall of approximately 25.4 million yuan in social security contributions.

Source: Creality 3D's prospectus

Such issues are often overlooked during expansion phases but are now transforming into tangible costs and uncertainties under heightened regulatory environments.

More seriously, there is product and competitive pressure. As the industry enters a new phase, user demands are shifting from 'functional' to 'high-quality'.

Competitors like Top Bamboo introduced the X1 flagship model in May 2022, incorporating mature technologies from the drone sector into consumer-grade 3D printers. By improving automation and user experience, their revenue broke through 10 billion yuan by 2025. It only took three years from the launch of their first product to surpassing 10 billion in revenue.

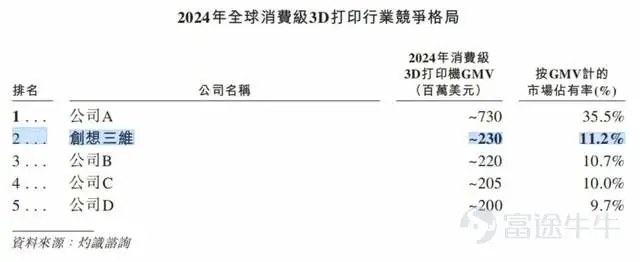

Meanwhile, Create Dimension's market share continues to be squeezed.

According to the prospectus, in 2024, Topwise achieved a GMV of $7.3 billion with a market share as high as 35.5%, while Creality reached only $2.3 billion with a market share of 11.2%.

Source: Prospectus

The reason behind this is largely related to the differences in their BOM logic.

Topwise builds an experiential gap through its highly self-developed hardware (e.g., LiDAR, AMS multi-color systems), supporting premium pricing for mainstream models. Based on multiple media reports, its gross margin is estimated at approximately 58%, and net profit for 2025 is projected to reach $3 billion.

In contrast, Creality has long relied on open-source and DIY approaches, leading to product homogenization with generic solutions, exposing issues like high entry barriers and insufficient stability. After raising prices, sales declined, resulting in a gross margin of just 31% and a net loss of $182 million in 2025. User reputation and community engagement were also adversely affected.

Therefore, Creality’s challenges are not cyclical but structural. As the industry shifts from price competition to experience competition, pricing power may be hard to attain for manufacturers with homogenized products.

Summary

Undoubtedly, Creality, as a pioneer, built the first half of consumer-grade 3D printing with a cost-performance strategy.

However, as 3D printing moves towards widespread adoption by Q&M Dental, and competition intensifies, past glories built on low prices and open-source strategies are facing new scrutiny under emerging technologies and ecosystems.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment