Options Plaza: Earnings Super Week is here! How to use options to capture both bullish and bearish o

Mideast risks roil US stocks; have tech shares bottomed out?

Geopolitical risk premium highlighted in the second half of the week, Wall Street summarizes 'Thursday/Friday effect'

Last night, US stocks opened higher but closed lower, extending the decline from last Friday. In the afternoon, as Trump again issued a strong threat to 'completely destroy' Iran's oil and gas facilities, combined with Iran's parliament's tough response to the Hormuz Strait toll bill, the market's focus shifted unilaterally from 'Fed dovishness' to 'oil shock,' causing indexes to weaken in a one-sided oscillation. From the sector performance, tech stocks were the biggest drag on the overall market throughout the day. $PHLX Semiconductor Index (.SOX.US)$ Plunging more than 4.2%, marking the worst single-month performance in the past three years.

The escalation of the Middle East situation is continuously amplifying volatility in US stocks. Wall Street has even summarized a 'Thursday/Friday effect,' meaning that since the outbreak of the Iran war, declines in US stocks during the second half of the week have been significantly stronger than at other times of the week.The closer to the weekend, the more necessary it is to add a premium for 'geopolitical risk gaps.'Investors are generally worried about the escalation of conflicts over the weekend, disruptions to shipping in the Hormuz Strait, or sudden shifts in White House policy. The selling pressure in the latter part of the week essentially reflects investors 'buying insurance' against geopolitical event risks that cannot be hedged. This logic also synchronously influences the联动走势 between Hong Kong and US stocks.

The 'Magnificent Seven' (Mag7) collectively entered an adjustment phase.

Amid a significant rise in macro uncertainty, the 'Magnificent Seven' (Mag7) collectively entered an adjustment phase. $NVIDIA (NVDA.US)$ , $Microsoft (MSFT.US)$ , $Alphabet-C (GOOG.US)$$Alphabet-A (GOOGL.US)$, $Meta Platforms (META.US)$ and $Tesla (TSLA.US)$ All showed varying degrees of pullback. The renewed escalation of tensions in the Middle East drove up oil prices, while the narrative of 'higher-for-longer interest rates' returned, bringing macro risks back into focus and putting noticeable pressure on highly valued growth stocks.

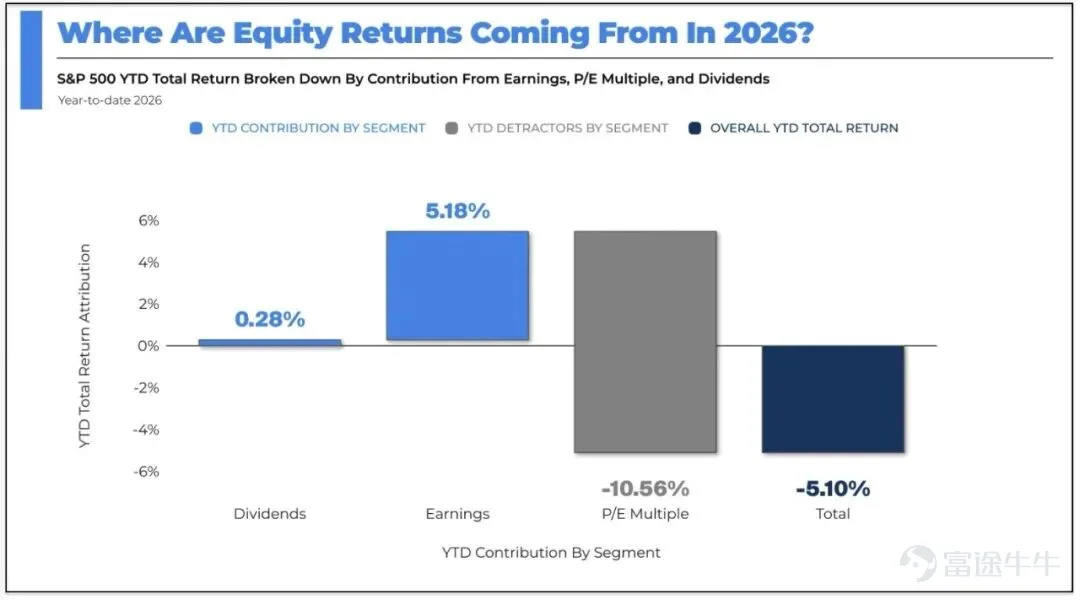

The chart below shows the breakdown of the S&P 500's performance since the beginning of the year (prepared last week), with its year-to-date decline of -5.1% (actually already -7.33% as of last night).The entire decline has been driven by valuation compression(PE Multiple), while earnings growth contributed to a 5.18% increase.

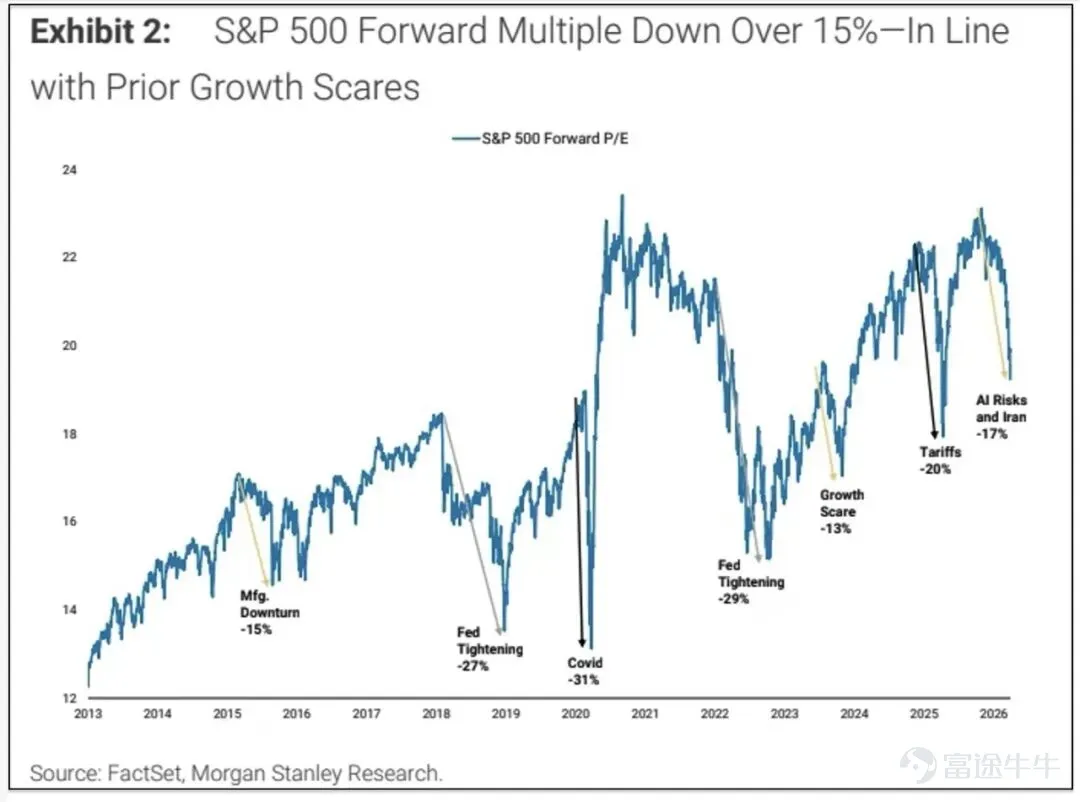

$S&P 500 Index (.SPX.US)$ The forward price-to-earnings ratio has already contracted by 17%, and without a recession or Fed rate hikes, it is already close to the adjustment levels seen during previous periods of panic.

The divergence on Wall Street is also intensifying. Wolfe Research recommends holding defensive positions; Morgan Stanley believes the sell-off is nearing an end, with market concerns about growth being overly exaggerated; the Goldman Sachs team is relatively optimistic, believing that as long as the situation does not spiral out of control, the S&P 500's baseline for 12% earnings growth this year remains solid.

Under the dual pressures of geopolitical tensions and interest rates, the divergence among the 'Magnificent Seven' tech giants is becoming increasingly evident. The core question in the current market has shifted from 'Is it AI-related?' to two points: when will AI investments translate into actual profits, and if profit realization lags, will potential risks erupt first? Despite being leading AI companies, recent stock performances and market tolerance have shown significant differences.

NVIDIA (NVDA): A tug-of-war at the $170 mark, a watershed moment for sentiment and positioning

As of the close on March 30th Eastern Time, $NVIDIA (NVDA.US)$ traded at $165,its 12-month forward price-to-earnings ratio has dropped to approximately 19.6 times, the lowest level since early 2019.It has broken below the psychologically significant $170 mark that the market widely focuses on, and remains within a volatile correction range. This valuation is even lower than the overall P/E ratio of approximately 20 times for the S&P 500 Index.

The core issue is not the breakdown of the industry logic — after the GTC 2026 conference, NVIDIA still emphasized the substantial revenue potential of AI chips and infrastructure. Jensen Huang even predicted that the Blackwell and Vera Rubin generations of AI chips will cumulatively generate at least $1 trillion in revenue by the end of 2027, with no substantial collapse in demand.

However, short-term pressures continue to accumulate: firstly, retail investor sentiment is waning; Vanda data shows that individual investors have recently turned to net selling of single stocks, with NVIDIA being one of the core targets for selling. Secondly, regulatory and legal noise is rising, including new class-action lawsuits related to AI training and U.S. lawmakers calling for an investigation into Jensen Huang’s previous statements about chip flows to China.

For NVIDIA, the $170 level isa watershed for sentiment and positioning, rather than the endpoint of long-term logic.If it can hold this level, then following a easing of Middle East risks, it would remain the most elastic counterattack target in the AI sector. If it breaks below effectively, the market may reprice it from a 'high-growth leader' to a 'high-volatility core asset.'

Meta (META): AI tailwinds suppressed by legal risks

$Meta Platforms (META.US)$ Recently announced an increase in its investment in the AI data center in El Paso, Texas, from $1.5 billion to $10 billion, planning to reach a capacity of 1 gigawatt by 2028. This is clearly positive news for AI infrastructure expansion, but the market reaction was not enthusiastic.

The core reason is:Legal risks have, for the first time, overshadowed the narrative of AI capital expenditure.On one hand, a Los Angeles jury ruled that Meta and Google are responsible for the social media addiction harm caused to a young user, with a combined compensation of 6 million US dollars, of which Meta bears 70%; on the other hand, a New Mexico jury ruled that Meta must pay a civil penalty of 375 million US dollars.

The real concern in the market is not the immediate fines, but rather that these verdicts bypassed the traditional 'user content immunity' clause, directly targeting the platform design itself, opening the door for a large number of similar lawsuits to follow. At the same time, Australia, Indonesia, and other regions have recently been intensifying pressure on Meta regarding minors' use of social media. For Meta, this may not immediately hurt profits, but it will continuously increase institutional costs and product modification pressures. In short, the essence of Meta’s sharp decline is the market sending a signal: the AI investment story continues, but the legal discount on the advertising model may first erode the AI valuation premium.

Tesla (TSLA): A compelling long-term narrative, but profit realization lags behind

$Tesla (TSLA.US)$ Its latest stock price is around $355. Recently, attention on Optimus has increased, with official details revealed on March 25 regarding its reduction gearbox and dexterous hand. Musk disclosed that Optimus 3 is expected to start production this summer and achieve mass production by 2027. He also announced that Tesla and SpaceX will build an advanced chip factory in Texas to strengthen the industrial closed loop of 'chip-model-terminal,' further supporting the long-term narrative.

On the fundamentals side, the pressure is very real. Analysts have already lowered Tesla's 2026 delivery growth forecast from 8.2% at the beginning of the year to 3.8%, and some institutions have even begun predicting that it will see a third consecutive year of declining deliveries. Meanwhile, Tesla’s capital expenditure this year is expected to rise above 20 billion US dollars, raising concerns that free cash flow could turn from seven consecutive years of positive into a net outflow.

The core of Tesla's current valuation hinges on when robotaxis and FSD will truly be implemented. A Reuters report at the end of February showed that Tesla has not completed the key regulatory progress needed for robotaxis in California, and what is currently operating is still just a small-scale pilot in Austin. In January, Musk stated that the initial production ramp-up of Cybercab and Optimus will be 'extremely slow.' This means that while the robotics narrative can drive a stock rebound when risk appetite recovers, in the current high-interest-rate, risk-averse market environment, Tesla leans more towards a high-volatility theme rather than a defensive core asset.

The current task is to distinguish between 'wrongful selloff' and 'overvaluation'

In terms of valuation, a significant portion of the bubble has already been wiped out; in terms of trend, it cannot yet be confirmed that the bottom has been reached. The market bottom often does not appear at the moment when 'the decline is large enough,' but rather when 'depressing factors begin to weaken.' Currently, three layers of pressure are weighing on tech stocks: First, inflation and consumer squeeze brought by high oil prices; second, upward revision of interest rate expectations; third, huge AI investment with slower realization of returns.

If two out of these three issues continue to worsen, it will be difficult for tech stocks to see a sustained reversal. Even though Powell stated that long-term inflation expectations remain largely stable, the market did not immediately restore risk appetite.

But this does not mean that tech stocks have no rebound opportunities. On the contrary,A short-term rebound window could open at any time.The market's current position is already quite sensitive. As long as geopolitical risks marginally ease, tech stocks will show strong recovery elasticity. The issue is that such rebounds currently resemble 'headline rallies,' and their sustainability still depends on whether oil prices can fall consecutively and whether the market regains confidence that policy measures can control inflation and spillover effects from conflicts.

$NVIDIA (NVDA.US)$ The current situation is one ofa 'weak trend' versus 'extreme oversold' conditions in contention. From a technical perspective, the current stock price (USD 166.52) has broken below commonly used moving averages and is approaching the lower Bollinger Band, showing clear bearish alignment and a weak pattern. The stock price is in a downward trend, but multiple oscillation indicators are signaling strong oversold conditions, accumulating momentum for a technical rebound. Investors may focus on the possibility of an oversold rebound, but strict stop-losses should be set. A complete reversal of the mid-term trend still requires clearer trend reversal signals.

Signals from the options market show that the Put/Call Ratio is 0.74, indicating that market sentiment is not entirely bearish. The current implied volatility (IV) is 46.12%, higher than the historical volatility (HV) of 32.13%. The IV percentile is 50%, reflecting moderate volatility.

(1) If you believe NVIDIA's current valuation offers good value and a short-term rebound is likely

Prioritize structures like the Bull Call Spread, which offer 'defined maximum loss and limited cost.' NVIDIA’s fundamentals remain strong, but the short-term market is pricing in 'geopolitical risks + interest rates + AI capital expenditure returns,' leading to valuation compression. Using a Bull Call Spread helps reduce costs, making it more suitable for an environment where the 'mid-term outlook is bullish, but short-term volatility is high.'

(The design images displayed on screen are for illustrative purposes only and do not constitute any investment advice or guarantees; market conditions fluctuate frequently, and the option prices shown do not represent real-world values.)

(2) If you already hold NVIDIA shares and are concerned about a continued downturn but don’t want to sell now

Consider a long collar strategy, which suits those who already own the underlying asset but are concerned about another round of valuation markdowns in the market. With many external variables in the short term, the benefit of a collar is that you don't need to sell your shares immediately, but can lock in downside risk first; the trade-off is that if the stock price rebounds quickly, part of your upside will be sacrificed.

(The design images displayed on screen are for illustrative purposes only and do not constitute any investment advice or guarantees; market conditions fluctuate frequently, and the option prices shown do not represent real-world values.)

Finally, here's a small perk for fellow investors—welcome to claim it!Options Beginner Pack

This event is exclusively for invited HK users, click to learn moreDetailed event rules >>

Futu's simulated trading challenge is now open for registration! Zero cost, zero risk, and you could win stock cash vouchers!For more details, click here

Disclaimer

This content does not constitute any offer, solicitation, recommendation, opinion, or guarantee of any securities, financial products, or tools. The risk of loss in buying and selling options can be substantial. In some cases, your losses may exceed the initial margin amount deposited. Even if you set contingent orders, such as 'stop-loss' or 'limit' orders, these may not necessarily prevent losses. Market conditions may make these orders unexecutable. You might be required to deposit additional margin within a short period. If you fail to provide the required amount within the specified time, your open positions may be liquidated. However, you will still be responsible for any account deficit arising from this. Therefore, before trading, you should study and understand options and carefully consider whether such trading suits you based on your financial situation and investment objectives. If you trade options, you should be familiar with the procedures upon exercising options and at expiration, as well as your rights and obligations when exercising options and at expiration.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comment (1)

to post a comment

13

10