The United States and Iran are sticking to their respective positions—can peace talks proceed smooth

Global Weekly Insights | US March PMI Hits 11-Month Low, China's Real Estate Market Shows Moderate Recovery

On the macroeconomic front

United States: March PMI hit an 11-month low, consumer confidence declined, and stagflation risks rose.

Last week, the US focused on March PMI and consumer confidence data, as economic growth slowed alongside rising inflation, triggering market concerns over stagflation risks.The preliminary S&P Global Composite PMI for March fell to 51.4, hitting an 11-month low, with diverging trends in manufacturing and services.The manufacturing PMI rose to 52.4 (expanding for the eighth consecutive month), while the services PMI dropped to 51.1 (an 11-month low). Price pressures rebounded significantly, with input cost increases being the largest in ten months, and sales prices reaching their highest level since August 2022. Supply chain tensions resurfaced, primarily driven by soaring energy prices amid Middle East conflicts.Employment saw its first decline in more than a year, with businesses adopting a more cautious approach to hiring.Additionally, the final University of Michigan Consumer Sentiment Index for March fell to 53.3, dragged down by rising oil prices and stock market volatility. Consumers' short-term economic outlook deteriorated, with inflation expectations for the next year climbing to 3.8%.This further intensified stagflation concerns and made it harder for the Federal Reserve to balance between cutting interest rates and controlling inflation.

China: Industrial enterprise profits rebounded strongly from January to February, while the real estate market experienced a moderate recovery.

In China, industrial enterprises' profits and the real estate market showed a positive recovery trend from January to February. The total profit of large-scale industrial enterprises increased by 15.2% year-on-year.The growth rate accelerated significantly, with all three major sectors achieving profit growth, among which manufacturing and mining saw notably improved growth rates.Revenue grew in tandem, while unit costs fell year-on-year for the first time since 2022, leading to an improvement in profit margins. Most industries saw a rebound in profits, with high-tech manufacturing and equipment manufacturing making significant contributions, demonstrating clear support from new growth drivers. However, attention should be paid to cost pressures brought by rising crude oil prices in March.In the real estate sector, it has been one month since purchase restrictions were relaxed within Shanghai's Outer Ring Road, with second-hand home transactions continuing to rise; March transactions are expected to reach a new high since April 2021.Second-hand home transactions in Beijing and Shenzhen also show signs of recovery, but listing prices for second-hand homes across cities remain under pressure. At the national level, weekly second-hand home transactions have grown week-on-week for four consecutive weeks, while new home transactions have risen sharply due to strong performance in second- and third-tier cities, indicating a moderate warming trend in the market.

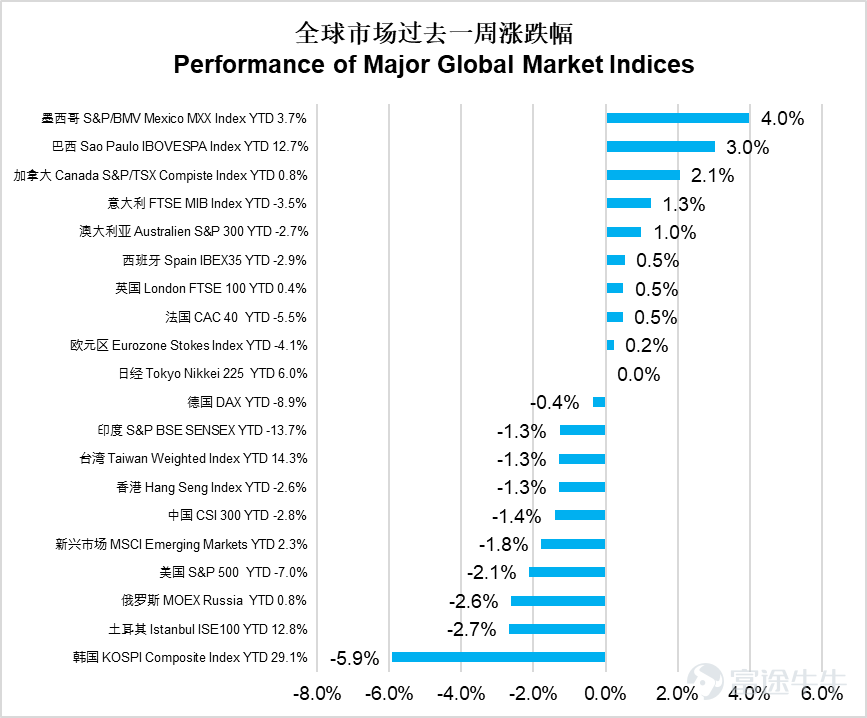

In terms of the equity market

Last week, global markets diverged in performance, with the KOSPI plunging 5.9% to lead declines globally, followed by Turkey's ISE100 down 2.7%, and Russia's MOEX down 2.6%.Emerging markets as a whole fell by 1.8%, the Hang Seng Index dropped 1.3%, and the CSI 300 declined 1.4%. However, Mexico’s MXX surged 4.0%, performing the best, Brazil’s IBOVESPA rose 3.0%, and Canada’s S&P/TSX gained 2.1%. The US S&P 500 fell 2.1%, European markets were mixed, with the UK FTSE 100 up 0.5% and Germany's DAX slightly down 0.4%.Overall, Latin American markets performed strongly, while Asian markets faced notable pressure.

Data source: Wind

The US energy sector soared 6.2%, performing the best, materials rose 4.2%, and utilities climbed 2.9%.Consumer staples rose 1.2%, becoming one of the few sectors to gain. However, communication services plummeted 7.2%, information technology fell 3.5%, financials dropped 2.1%, consumer discretionary fell 1.9%, industrials declined 1.2%, healthcare dipped 1.0%, and real estate slipped 0.7%.The market exhibited an extreme divergence pattern, with energy and materials leading gains while technology and telecommunications led losses.

Data source: Wind

The healthcare sector in Hong Kong stocks performed the best with a 2.9% increase, consumer staples rose by 1.4%, and the materials industry increased by 0.9%.However, the information technology and real estate construction industries both fell by 3.0%, the energy sector dropped by 2.5%, and the industrial sector declined by 2.3%. The Hang Seng Tech Index fell by 1.9%, utilities dropped by 1.7%. Non-essential consumption fell by 1.3%, and the telecommunications sector decreased by 1.2%. Both the financial sector and conglomerates fell by 0.7%.The market displayed a divergent characteristic of healthcare and consumption leading gains while technology and real estate led declines.

Data source: Wind

In the bond market,

Global bond markets continued to retreat overall over the past week.The global composite index fell by 0.49%, the U.S. composite index declined by 0.12%, U.S. investment-grade corporate bonds dropped by 0.23%, and U.S. high-yield corporate bonds fell by 0.47%.The emerging markets USD bond composite index fell by 0.32%, and the Chinese USD credit bond index dropped by 0.14%.

In terms of interest rates, U.S. Treasury yields moved higher overall.The 2-year U.S. Treasury yield rose by 1 basis point to 3.91%, and the 10-year U.S. Treasury yield increased by 5 basis points to 4.43%.

Market Outlook

– Oil prices hit new highs, and the S&P 500 fell significantly, potentially offering a good buying opportunity from a contrarian investment perspective.

The Middle East geopolitical conflict has entered its fifth week.Despite Trump once again displaying a 'TACO' stance (an acronym for 'turning away at the critical moment'), postponing the deadline for Iran from March 27 to April 7, the market did not rebound as it had after similar announcements in the past.This week's media reports can be summarized as follows: both sides are in contact through a third party, while the conflict continues. Based on publicly available information, there remains a significant divergence in their core demands. The market widely interprets this delay as a strategic move by the US to buy time for preparing a ground invasion. As expected, the betting market has lowered expectations for a ceasefire in April, while raising the likelihood of a US ground offensive during the same month.In terms of asset prices, oil prices closed at a new high this week, with the 10-year US Treasury yield moving higher in tandem; the S&P 500 index hit its lowest level since September 2025.On Thursday and Friday, the market declined more than 1% for two consecutive days, showing signs of selling pressure. We previously noted that for most of March, this round of adjustment was relatively restrained, with investors mainly hedging market risks through derivatives; however, starting this week, more investors have shifted to net selling of stocks, actively reducing overall risk exposure. Compared to the panic selling during the tariff conflict in April 2025,the current level of market panic has not reached an extreme. However, if geopolitical tensions further drive the market lower, deteriorating sentiment indicators may provide good buying opportunities from a contrarian investment perspective.Historical data shows that during US midterm election years, the average maximum drawdown for the S&P 500 is close to 15%. This year, the index has already pulled back 9% from its January peak. Moreover, markets tend to perform strongly after drawdowns during midterm election years. Therefore, investors need to guard against downside risks stemming from escalating geopolitical conflicts,but they should also be prepared to seize potential opportunities when market sentiment reaches extreme panic levels, as conflicts could reverse course.

Key economic data and events this week

China will release its official PMI data for March on Tuesday;

The US will release its ISM manufacturing index for March on Wednesday;

The US will release its durable goods orders data for February on Thursday;

The US will release its non-farm payroll-related data for March on Friday.

Disclaimer: The issuer of this report is E Fund Management (Hong Kong) Co., Limited. This report does not constitute an invitation or recommendation to invest in fund units. Fund unit subscriptions can only be made using application forms accompanied by a fund prospectus. Investment involves risks; fund prices may rise or fall, and past performance is not indicative of future results. Before investing, investors should carefully read the investment risks associated with the fund in the fund prospectus (including the “Risk Factors” section). This report may only be distributed within certain jurisdictions. In any jurisdiction where distributing such information or making any invitation or recommendation is prohibited, or if distributing this report or making an invitation or recommendation to any person would be illegal, this report does not constitute such distribution, invitation, or recommendation. This document is exempt from prior review and approval by the Hong Kong Securities and Futures Commission (SFC) and has not been reviewed by the SFC. SFC endorsement does not imply promotion or endorsement of the scheme, nor does it guarantee the commercial merits or performance of the scheme, nor does it represent that the scheme is suitable for all investors, or endorsement that the scheme is suitable for any particular investor or class of investors. All rights reserved ©2026. E Fund Management (Hong Kong) Co., Limited.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

1