The United States and Iran are sticking to their respective positions—can peace talks proceed smooth

Analysis of the Rotation among the 11 Major Sectors of the US Stock Market (March 30): Energy Leads, Defensive Sectors Dominate, Short-term Recovery Yet to Be Confirmed

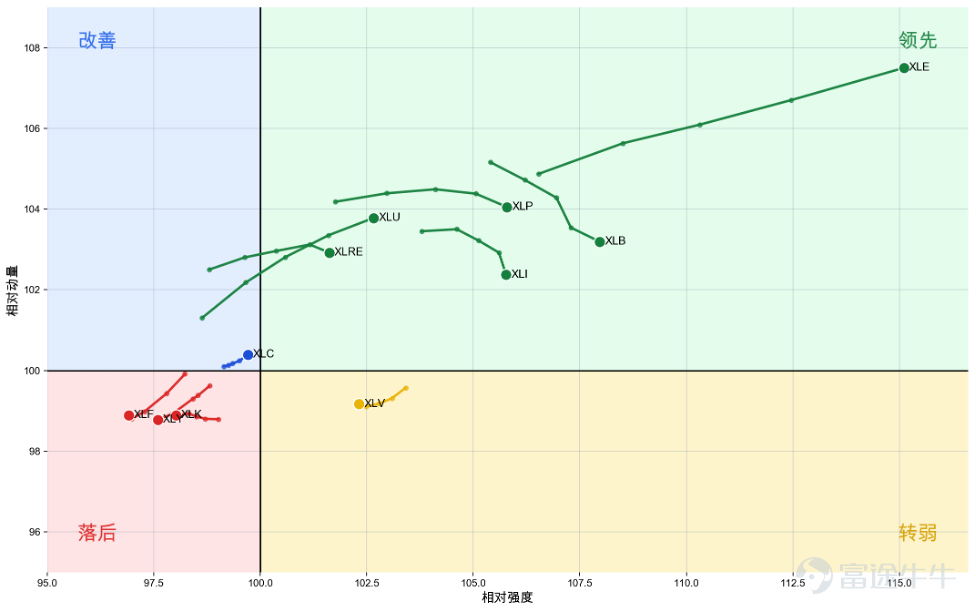

Summary: As of the close on March 27, 2026, Eastern Time, the rotation pattern of the 11 major sectors in the US stock market remains dominated by 'Energy XLE leading and defensive sectors prevailing.' Medium-term capital is mainly concentrated in Energy XLE, Utilities XLU, Consumer Staples XLP, and some old economy sectors, with growth styles yet to regain dominance. Although there has been marginal recovery in Materials XLB, Industrials XLI, and Financials XLF in the short term, Technology XLK has not formed an effective relay, indicating that the diffusion of market risk appetite is still insufficient. Considering the sector structure and macroeconomic cycle mapping, the current market is closer to a late-cycle defensive phase rather than a full rebound in risk appetite.

1. Weekly Rotation: Energy Remains the Main Theme, Defense and Old Economy Dominate

From the perspective of weekly structure, Energy XLE remains the clearest medium-term main theme. Energy XLE is located at the upper right corner of the leading area, and its trajectory continues to extend to the upper right, showing that its relative strength and relative momentum are still rising simultaneously. In addition to Energy XLE, Utilities XLU, Consumer Staples XLP, Materials XLB, Industrials XLI, and Real Estate XLRE are also in the leading area, indicating that the current market advantage lies not in high-elasticity growth but in stronger directions of defense, resources, and old economy attributes.

It should be noted that this leadership does not fully equate to overall strength. Against the backdrop of periodic pressure on the S&P index, the leadership of some sectors is closer to 'relative resilience' rather than 'active leadership.' From this perspective, Energy XLE is one of the few sectors that possess both relative advantage and absolute strength, while Utilities XLU and Consumer Staples XLP more reflect the market's preference for certainty. Meanwhile, Healthcare XLV has fallen into a weakening zone, Communication Services XLC has entered an improvement zone but remains close to the central axis, and Technology XLK, Consumer Discretionary XLY, and Financials XLF are still in lagging zones, indicating that growth and cyclical directions have yet to complete their medium-term recovery.

Second, daily rotation: Materials, Industrials, and Financials show recovery, but Technology fails to take the lead

From the perspective of daily structure, short-term rotation is clearly more active than on the weekly chart. Energy XLE remains in the leading zone, indicating consistent strength in both short- and medium-term trends. Meanwhile, Materials XLB, Industrials XLI, and Financials XLF have entered the improvement zone, suggesting that short-term capital is starting to shift from a purely defensive posture toward some cyclical and financial sectors.

However, this recovery is still a localized phenomenon for now. Technology XLK is near the weakening zone, indicating that short-term momentum has not continued to strengthen but instead slowed down. Communication Services XLC remains weak, while Consumer Discretionary XLY shows marginal improvement, though with limited strength, mostly reflecting passive recovery after overselling. Utilities XLU has also entered the weakening zone, showing that defensive sectors are no longer accelerating in the short term, but this does not mean the market has shifted to a full offensive state. Therefore, what the daily chart reveals is not a signal of 'growth sectors regaining leadership' but rather a sign of 'partial recovery in some cyclical sectors within a defense-led framework.'

Third, macro cycle: Late-cycle defensiveness, short-term recovery yet to alter dominant structure

The macro implications reflected by the current sector composition still lean toward a late-cycle defensive structure. On the weekly chart, Energy XLE continues to maintain its position as the strongest trend leader, while defensive sectors like Utilities XLU and Consumer Staples XLP remain relatively advantageous. At the same time, Technology XLK, Consumer Discretionary XLY, and Financials XLF have yet to complete their medium-term recovery, indicating that the market's dominant structure has not returned to a state where growth and pro-cyclical sectors lead across the board.

On the daily chart, although Materials XLB, Industrials XLI, and Financials XLF show marginal recovery, this improvement reflects short-term rotation rather than a trend-based handover. For this reason, the current macro cycle is better defined as 'late-cycle defensiveness with short-term recovery yet to change the dominant structure.' In other words, the relative strength of energy and defensive sectors supports a defensive outlook amid slowing growth; meanwhile, the recovery in cyclical sectors suggests that the market has not yet entered a one-way recession trade. Overall, the current situation is more akin to 'localized recovery within a late-cycle defensive framework' rather than 'a broad rebound in risk appetite.'

IV. Trading Strategy

In terms of trading strategy, it is currently more appropriate to adopt an approach of 'prioritizing main trends, selecting strong recoveries, and waiting for confirmation.' On a medium-term basis, Energy XLE remains the clearest strong direction, and as long as relative strength and momentum do not show significant reversals, it should be regarded as the most worth tracking trend. For defensive sectors, Utilities XLU and Consumer Staples XLP, although showing signs of cooling in the short term, can still serve as key observation anchors for cautious market sentiment as long as their weekly relative advantages remain intact.

In the short term, Materials XLB, Industrials XLI, and Financials XLF can be prioritized as sectors to observe for recovery, but only under the premise of 'tracking whether the recovery continues,' rather than prematurely upgrading them to new main trends. If these sectors can continue to advance upward and gradually break away from repeated fluctuations around the central axis, then the recovery may have the potential to further escalate. If the recovery stalls again, it should be viewed as a localized bounce within a late-cycle environment rather than a signal of style rotation.

For growth sectors, it is still too early to draw conclusions. Unless Technology XLK can return to the improvement zone and push into the leading zone, it will be difficult for the market to achieve a meaningful broad-based rebound in risk appetite. The key verification point going forward is whether Technology XLK, Communication Services XLC, and Consumer Discretionary XLY can improve simultaneously and form wider synergy with Financials XLF. If these sectors fail to resonate, the market will likely continue to maintain a rotation pattern characterized by 'strong Energy XLE, stable defense, and partial recovery in cyclicals without taking the lead.'

$S&P 500 Index (.SPX.US)$ $SPDR S&P 500 ETF (SPY.US)$ $NASDAQ 100 Index (.NDX.US)$ $Invesco QQQ Trust (QQQ.US)$ $Dow Jones Industrial Average (.DJI.US)$ $State Street® SPDR® Dow Jones Industrial Average® ETF Trust (DIA.US)$ $Russell 2000 Index (.RUT.US)$ $iShares Russell 2000 ETF (IWM.US)$ $USD (USDindex.FX)$ $U.S. 10-Year Treasury Notes Yield (US10Y.BD)$ $XAU/USD (XAUUSD.CFD)$ $Real Estate Select Sector Spdr Fund (The) (XLRE.US)$ $The Technology Select Sector SPDR® Fund (XLK.US)$ $The Communication Services Select Sector SPDR® Fund (XLC.US)$ $Consumer Discretionary Select Sector SPDR Fund (XLY.US)$ $Consumer Staples Select Sector SPDR Fund (XLP.US)$ $Materials Select Sector SPDR ETF (XLB.US)$ $Industrial Select Sector SPDR Fund (XLI.US)$ $Energy Select Sector SPDR Fund (XLE.US)$ $Financial Select Sector SPDR Fund (XLF.US)$ $The Health Care Select Sector SPDR® Fund (XLV.US)$ $Utilities Select Sector SPDR Fund (XLU.US)$

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

4

3