Unisound (09678.HK) 2025 Report Card: Large Model Deployment, Is the Profit Turning Point Approaching?

In 2025, China's AI industry has completely moved away from the 'parameter competition and storytelling' phase of unregulated growth, fully transitioning into the deep waters of commercialization focused on 'implementation and profitability.' In this industry reshuffle, the performance report card submitted by the Hong Kong-listed 'AI voice veteran' $UNISOUND (09678.HK)$ marks a key litmus test for assessing the commercial strength of vertical AI companies.

This AI company, which made it to the 'Most Watched IPO of the Year' list at the 12th 'Hong Kong Stock 100 Strong' awards ceremony, delivered an impressive performance in its 2025 results. Its annual revenue increased by 29% year-on-year, with revenue related to large models surging more than tenfold, while the net loss narrowed by 27.5% year-on-year. This data outlines the company's transition from technology development to commercial monetization and has sparked market discussions: Is Unisound, which has been deeply rooted in the AI sector for 14 years, finally approaching a turning point towards profitability?

The reduction in losses was not achieved through a 'cost-cutting' contraction.

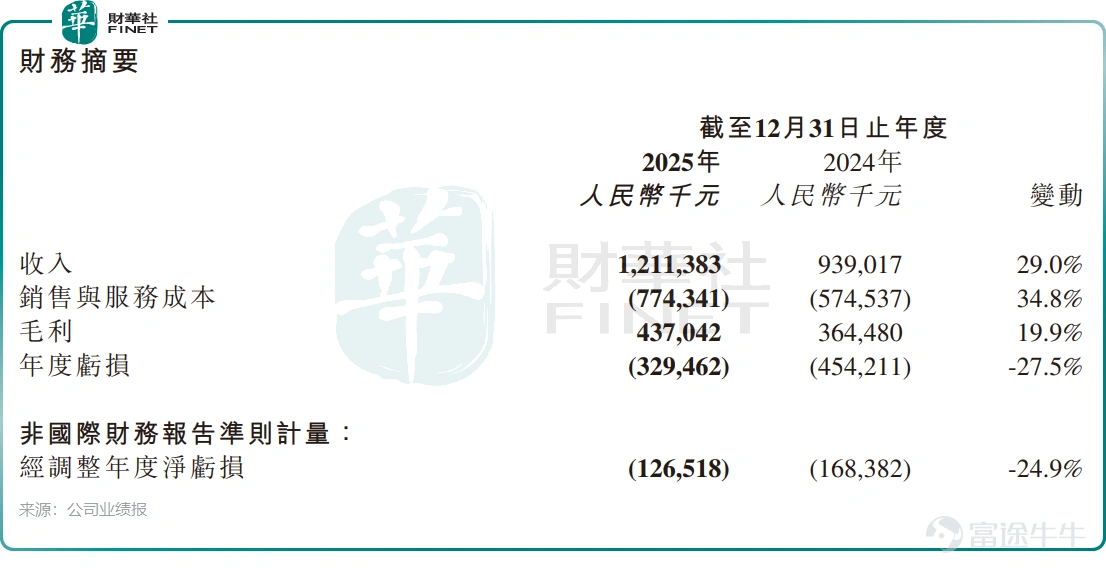

Annual report data shows that in 2025, Unisound achieved total revenue of 1.211 billion yuan (in RMB, unless otherwise specified), representing a year-on-year increase of 29%, setting a new historical high for revenue scale. The improvement on the profitability side was even more remarkable, with the full-year net loss standing at 329 million yuan, narrowing significantly by 27.5% year-on-year. The adjusted annual net loss narrowed to 127 million yuan, decreasing by 24.9% year-on-year.

What is particularly noteworthy is that the pace of the company’s profit improvement showed significant 'acceleration characteristics.' In the second half of 2025, revenue increased by 33% year-on-year, reaching 810 million yuan, while the net loss narrowed by 84% year-on-year. After adjustments, the loss narrowed by 92%, bringing it extremely close to the break-even point, making it the biggest highlight of the year’s performance.

The market has always had a core question about loss reductions in AI companies: Are these paper improvements achieved by cutting R&D investment to save costs?

What makes Unisound's loss-reduction results most commendable is that they have achieved the parallel goals of 'high R&D investment' and 'loss narrowing.' According to the annual report, the company’s R&D expenses in 2025 reached 381 million yuan, maintaining a year-on-year growth of 2.9%. From the business perspective, the iterative multi-modal capabilities of the Mountain-Sea large model, the performance of medical AI in authoritative evaluations, as well as the technical implementation of voice large models and OCR large models, all reflect the actual output of R&D investment.

However, objectively speaking, this parallel state of 'steady R&D investment and loss narrowing' still remains in a stage of balance. On the one hand, the growth rate of R&D investment (2.9%) has fallen below the revenue growth rate (29%), reflecting to some extent that the company is adopting a more prudent approach to R&D investment. On the other hand, the current commercialization of R&D output is still concentrated in a few core scenarios, and has not yet formed comprehensive technical monetization capabilities.

Therefore, although this reduction in losses avoided the short-sighted behavior of 'cutting R&D for short-term profits,' whether R&D investment can continue to be converted into scaled profitability still needs further verification through subsequent business data.

On the expense side, the company’s sales and marketing expenses in 2025 decreased by 7.7% year-on-year, with the sales expense ratio being only 5.4%, achieving a decrease in sales expenses against the backdrop of high revenue growth. Financial expenses fell sharply by 45.2% year-on-year, with the reduction in interest expenses following the redemption of liabilities post-IPO easing the company’s financial pressure.

Additionally, after adjustments, the company’s overall operating expense ratio in 2025 fell by 10 percentage points year-on-year, with per capita output increasing to 2.52 million yuan per person, up 25% year-on-year, reflecting improved operational efficiency.

However, objectively speaking, the acceleration of loss reduction does not equate to having overcome profitability challenges. By the end of 2025, the company's adjusted net loss still stood at 127 million yuan, with a full-year operating cash flow deficit of -213 million yuan. Although this marks a significant narrowing compared to the -319 million yuan outflow in 2024, operating cash flow has yet to turn positive. For Unisound, whether operating cash flow can shift from negative to positive in 2026 will be the benchmark for determining if the true turning point in profitability has arrived.

Large models have evolved from a 'technical concept' into a revenue pillar.

A fundamental change in the revenue structure has become a key highlight in Unisound’s commercial transformation.

The most notable breakthrough in the annual report is that Unisound’s large model business has transitioned from a 'technical testing ground' to a 'revenue anchor.' In 2025, revenue related to the company’s large models reached 610 million yuan, achieving explosive growth of over 10 times year-on-year, accounting for more than 50% of total revenue, officially replacing traditional voice services as the company’s primary growth driver. This data signifies that Unisound’s large models are no longer just a valuation story in the capital markets but have entered the stage of large-scale commercial replication.

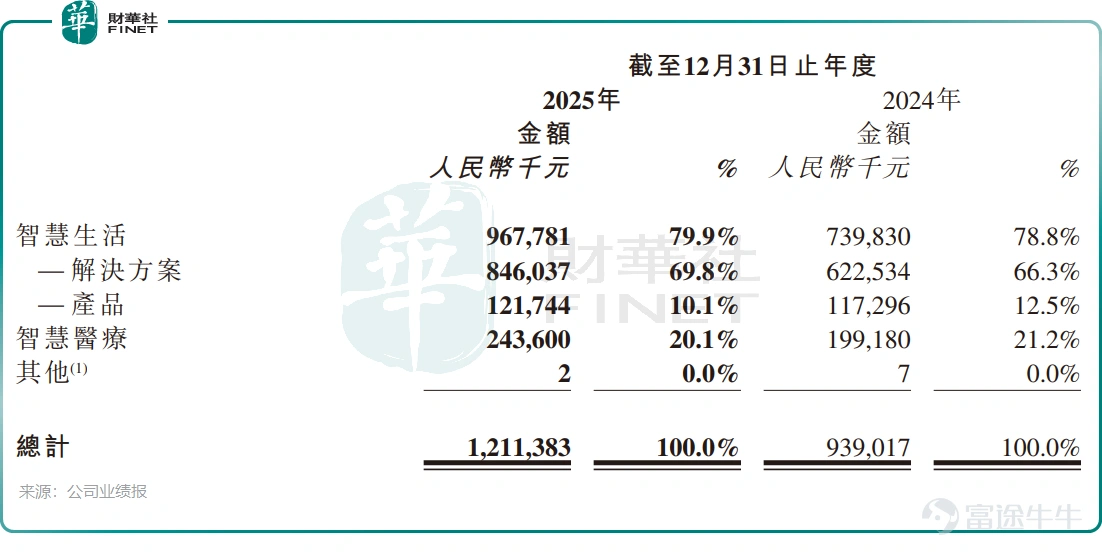

Looking at the two core business segments, the company has formed a structure of 'a stable foundation with new engines gaining momentum,' but it also shows significant imbalances in development.

As the cornerstone of the company’s performance, the smart living business achieved revenue of 968 million yuan in 2025, a year-on-year increase of 30.8%, accounting for 79.9% of total revenue. Among this, revenue from smart transportation grew nearly 40% year-on-year and has been implemented in over 10 cities including Qingdao and Shenzhen; the intelligent cockpit business achieved commercial deployment of large models on the device side and established partnerships with multiple automakers; cumulative shipments of self-developed AI chips exceeded 110 million units.

The highly anticipated smart healthcare business achieved revenue of 244 million yuan in 2025, growing 22.3% year-on-year. Despite a 53.2% year-on-year increase in average revenue per customer and 85% of partner hospitals being tertiary hospitals, the 244 million yuan revenue scale remains relatively small compared to the company’s overall revenue base. Whether it can achieve scaled-up growth through medical large models still requires ongoing validation.

On a deeper level, the company’s business model is transitioning from 'project-based' to 'product + service.' In the past, AI solution providers often struggled with the dilemma of 'too many customized projects and difficulty scaling replication.' However, leveraging its Shanhai large model, Unisound encapsulated complex AI capabilities into standardized intelligent agents, enabling rapid replication across scenarios such as smart transportation, healthcare, and customer service. Although solution revenue still accounts for 69.8% of total revenue, with product revenue making up 10.1%, project-based work remains the primary revenue source. Nevertheless, the enhanced standardization capabilities brought by large models have already given the company a glimpse of breaking free from labor-intensive project models.

From an industry perspective, Unisound’s 2025 annual report reflects the domestic AI industry’s transformation from 'conceptual' to 'practical.' As the industry moves away from its obsession with general large models, the ability to commercialize vertical scenarios has become the core competitiveness of AI companies. Unisound’s tenfold growth in large model revenue demonstrates its technical implementation capabilities, while the narrowing losses under high R&D investment show its potential for development.

But whether the turning point in profitability is truly approaching remains to be seen in 2026. For Unisound, only when the scaled revenue from large models continues to materialize, operating cash flow successfully turns positive, and the company genuinely crosses the breakeven line, will it complete its transformation from an 'AI technology company' to a 'sustainably profitable business.' This annual report gives the market a glimpse of hope, but Unisound still needs to move forward step by step.

Author: Yuan

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment