Looking at Ping An's 'different facets' through the 2025 annual report, which side did you see?

There's an old saying in the capital markets: investing in insurance stocks is essentially investing in the power of compound interest over time.

But in recent years, this statement seems to have been repeatedly questioned by the market. Can the compound interest story of insurance stocks continue amidst falling interest rates, asset scarcity, and agent attrition?

Ping An's A-shares and H-shares rose by 36% and 51% respectively in 2025, showing impressive performance. However, the market has seen a pullback this year, indicating lingering doubts about the valuation system for insurance stocks. The value of a core asset seems to be waiting to be redefined.$Ping An Insurance (601318.SH)$$PING AN (02318.HK)$

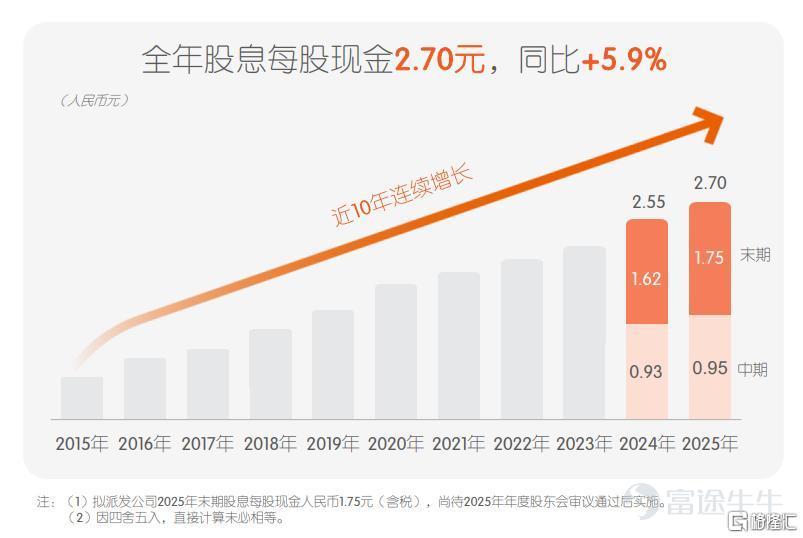

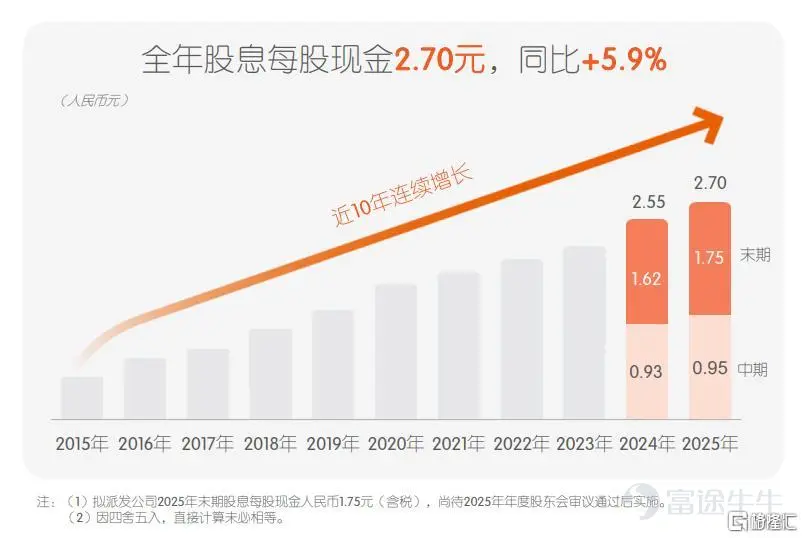

However, Ping An’s annual dividend per share reached 2.70 yuan, up 5.9% year-on-year, marking the 14th consecutive year of increase. The dividend record itself speaks volumes, addressing all questions about whether 'profitability is sustainable' with real cash returns.

After the release of the annual report, Wall Street's top investment banks reached a general consensus – Ping An’s performance met expectations, its main businesses are improving across the board, and its valuation appears attractive. UBS, Goldman Sachs, JPMorgan, and Citi have all maintained their Buy or Overweight ratings on Ping An, while Morgan Stanley explicitly named it as the top pick in the industry.

In my view, the biggest opportunities in the market often lie where the expectation gap is the widest.

Ping An’s 2025 annual report marks the starting point for that 'expectation gap' to materialize. It demonstrates that the company has successfully completed a genetic restructuring from a cyclical stock to a growth stock.

01. The core main business is全面向好, and the value of new business has returned to a high growth channel.

First, let’s examine the most critical life insurance business.

In 2025, Ping An’s life insurance and health insurance new business value reached 36.897 billion yuan, growing by 29.3% year-on-year, achieving double-digit growth for three consecutive years.

More importantly, the new business value margin increased from 22.7% in 2024 to 28.5%, rising by 5.8 percentage points year-on-year.

What does this mean? It means that Ping An’s life insurance business not only sold more but also sold at higher value – the proportion of high-value protection products is increasing, rather than relying on low-value savings products to boost scale.

Behind this turning point lies a qualitative change in channel reform.

In terms of the agent channel, the transformation towards 'three highs' (high quality, high performance, and high standards) continues to deliver results. The value of new business per capita grew by 17.2% year-on-year. Although the monthly average income data was not directly disclosed, we can infer from the increase in per capita productivity that the high-quality transformation is translating into tangible output. More importantly, the value of new business in the agent channel increased by 10.4% year-on-year, which represents significant growth amid an overall industry contraction.

The bancassurance channel also performed impressively. By deepening cooperation with the five major state-owned banks and five nationwide joint-stock banks, the value of new business in bancassurance surged by 138.0% year-on-year, contributing to a 12.1 percentage point increase in its share of the value of new life insurance business. This truly represents a second growth curve.

The property insurance business delivered excellent results as well. The overall combined ratio stood at 96.8%, improving by 1.5 percentage points year-on-year and remaining consistently better than the industry average for multiple years. The auto insurance combined ratio reached 95.8%, improving by 2.3 percentage points year-on-year. Against the backdrop of comprehensive auto insurance reform, maintaining such cost control capabilities relies not on price wars but on precise pricing and risk management abilities.

On the investment side, stability has been demonstrated. The scale of the insurance fund's investment portfolio exceeded RMB 6.49 trillion, with a comprehensive investment return rate of 6.3%, up 0.5 percentage points year-on-year. Over the past decade, the average net investment return rate was 4.8%, and the average comprehensive investment return rate was 4.9%, surpassing long-term investment return assumptions embedded in the intrinsic value. In fact, by 2025, over RMB 90 billion in unrealized equity gains have yet to be included in current profits—these represent values that Ping An can gradually release in the future. In an era of declining interest rates, maintaining such returns does not rely on chasing high-risk assets but on disciplined asset allocation and closely following the direction of national economic development, practicing the investment philosophy of 'seeking certainty amidst uncertainty.'

Therefore, Ping An’s attributable operating profit for 2025 amounted to RMB 134.415 billion, growing by 10.3% year-on-year, while its attributable non-GAAP net profit reached RMB 143.773 billion, increasing by 22.5% year-on-year—not driven by one-time investment gains but by genuine, across-the-board improvement in core operations.

From Zero to One in AI: Technology Investments Enter the Payoff Phase

Is Ping An an insurance company or a technology company?

Five years ago, the answer might have been an insurance company; today, the answer is becoming both. As Guo Xiaotao, Co-CEO of Ping An, stated during the earnings presentation: 'AI is not an optional question for us—it’s a must-answer.'

By the end of 2025, more than 230,000 employees within Ping An had adopted the internal intelligent platform, developing over 70,000 intelligent applications, with models being invoked 3.65 billion times throughout the year. This is not just a 'tech gimmick' but a productivity tool that has already been integrated into daily operations.

What truly transforms AI from a tool into a service is its implementation at the client end. This year, Ping An completed a major upgrade of its technology platform - 'Integrated Finance·All in One'. It consolidated 700 million internet registered users, previously scattered across more than ten apps, into a single unified entry point. This means that no matter which app a user opens, services such as checking policies, buying wealth management products, consulting doctors, or processing claims can all be completed with a single command.

Behind these services lies the support of Ping An’s database. With 33 trillion bytes of data covering 251 million individual customers, it has accumulated over 3.2 trillion high-quality text corpora, 500,000 hours of annotated voice data, and more than 8.5 billion image datasets. This data does not come from publicly available online sources but is native data collected in real business scenarios such as insurance, banking, and healthcare. This means that Ping An’s AI models are not generalists but specialists – in vertical fields like finance and healthcare, their accuracy and practicality far exceed those of general large-scale models.

By 2025, Ping An's AI agent service volume exceeded 1.702 billion instances, covering 80% of the total customer service volume. Through intelligent underwriting and smart claims processing, 94% of life insurance policies achieved near-instantaneous underwriting, with 'flash claims' accounting for 59% of life insurance cases. Intelligent anti-fraud measures for property insurance intercepted losses amounting to 10.51 billion yuan, marking over 10 billion yuan in loss reductions for three consecutive years.

Behind these figures lie tangible cost savings and efficiency improvements.

More importantly, AI has begun to feed back into core business operations. The average new life insurance policy size increased 1.5 times for clients utilizing healthcare benefits, 5.2 times for those using home-based elderly care benefits, and 23.4 times for clients opting for premium elderly care benefits. This indicates that the depth of AI-driven services is translating into significant increases in customer value per transaction.

In my view, this represents the most crucial shift in Ping An’s valuation logic. If a company’s technological capabilities only serve itself, they constitute a cost; if they enhance customer value and operational efficiency in the main business, they become core assets. Ping An is in the process of achieving this transformation.

03, The Battle for Positioning in the Medical and Elderly Care Ecosystem: A Paradigm Shift from Low-Frequency Transactions to High-Frequency Interactions

If life insurance represents Ping An’s present, and AI its future, then the medical and elderly care ecosystem serves as the bridge connecting the present to the future.

By the end of 2025, Ping An had 251 million individual customers, among whom the retention rate for those utilizing the medical and elderly care ecosystem service benefits reached 93%. Customers using these services paid an average first-year premium 2.3 times higher than non-users, with an additional take-up rate 15 percentage points higher.

This set of data reveals a core logic: the medical and elderly care ecosystem serves as Ping An’s secret weapon for enhancing customer stickiness and unlocking customer value.

Why?

Since insurance involves low-frequency transactions, a person may purchase insurance only once a year, or even once every few years. However, medical care and elderly care are high-frequency needs—physical exams, consultations, chronic disease management, rehabilitation, and nursing care are all daily necessities. Through its medical and elderly care ecosystem, Ping An has increased the frequency of customer interactions from yearly to weekly, or even daily.

The shift from low frequency to high frequency, and from transactions to engagement, marks a paradigm shift in the business model.

More importantly, the ceiling for this sector is much higher than insurance itself.

The proportion of China’s population aged over 60 has exceeded 21%, indicating an irreversible trend towards deep aging. However, there is a severe shortage of high-quality medical and elderly care services—top doctors are concentrated in tertiary hospitals, and there is a significant shortage of beds in elderly care facilities. Ping An's medical and elderly care ecosystem precisely addresses this supply-demand bottleneck.

By the end of 2025, Ping An will have a team of approximately 50,000 internal and external doctors, with over 3,500 contracted expert doctors, and cooperation with more than 37,000 domestic hospitals for claims services. Coverage of top 100 hospitals and tertiary hospitals in China reaches 100%. In terms of self-operated senior care communities, Ping An's premium senior care community project, Zhen Yi Nian, has been established in five cities across six projects. The Shanghai Yi Nian Cheng Jing'an No. 8 is already in operation, while Shenzhen Yi Nian Cheng Futian has entered trial operations.

More importantly, Ping An's self-developed AI-assisted diagnosis system enables AI doctors to accurately diagnose over 11,300 diseases with a diagnostic accuracy rate of 95.1%. The AI-MDT multi-disciplinary consultation and treatment plans for complex diseases have an accuracy rate of nearly 90%. This means that Ping An’s medical and elderly care services are not just supported by human doctors but also by AI doctors—digital physicians who can be online 24/7 without fatigue or breaks. This capability is difficult for traditional medical institutions to replicate.

04. Conclusion

The investment logic behind traditional insurance stocks essentially bets on interest rates, real estate, and agent cycles. However, Ping An is breaking free from this passive reliance on cyclical trends:

Core operations are driven by productivity rather than workforce size. Technology has transitioned from being a cost center to becoming a profit generator, contributing an independent growth pillar. The medical ecosystem transforms low-frequency insurance into high-frequency services, enhancing customer stickiness and revenue stability.

When a company’s growth no longer depends entirely on macroeconomic tailwinds but instead on internally generated momentum, it completes a genetic restructuring from a cyclical stock to a growth stock.

At this point, Ping An is no longer a pure insurance company.

It has three aspects:

The first aspect is being the leader in the life insurance industry;

The second aspect is being the AI-driven integrated finance leader;

The third aspect is being the operator of a healthcare and retirement ecosystem.

These three aspects together form Ping An's triple valuation logic. However, the current market only reflects the price of the first layer.

History always repeats itself because human nature remains unchanged. When the market is preoccupied with short-term fluctuations, Ping An uses its annual report to prove the long-term correctness of its strategy—it does not pursue explosive growth but instead builds a compounding model with higher barriers over time through deep customer engagement, technological empowerment, and ecosystem synergy.

When the market panics due to short-term noise, real opportunities often lie with companies that adhere to long-termism against conventional thinking.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment