Focus on the Google Cloud annual conference, how will it impact market trends?

Essential for US stock investors! A preview of major events in April, these dates that could impact rises and falls have been highlighted

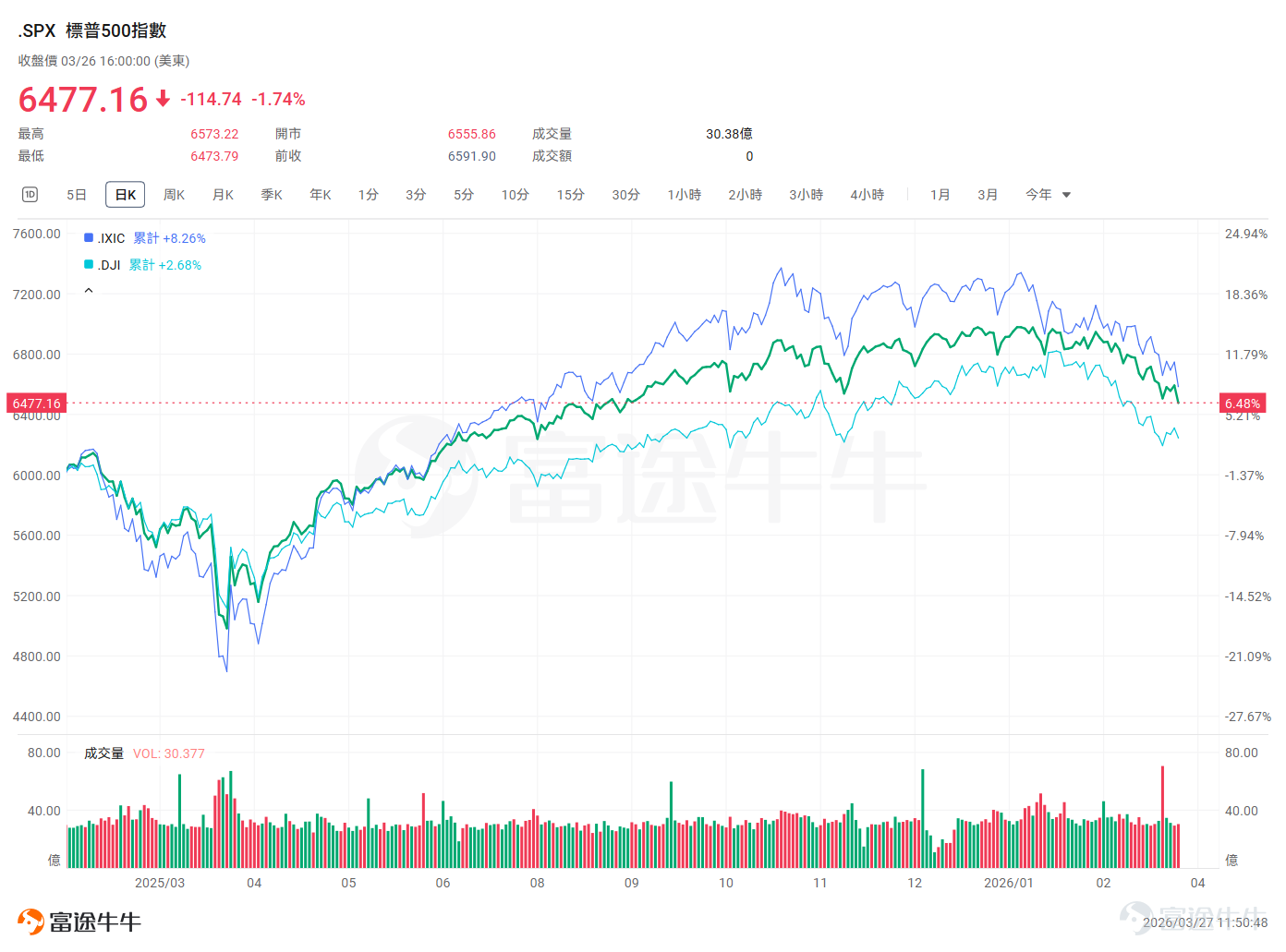

Before entering an April filled with suspense, let's first review the turbulent US stock market in March.

Throughout March, the US stock market did not continue its previous one-sided rise but instead exhibited a pattern of 'weak fluctuations under high volatility.' The persistent fermentation of Middle Eastern energy risks led to a significant surge in crude oil prices, with Brent crude oil and West Texas Intermediate (WTI) briefly reaching $119 per barrel. The spike in oil prices directly intensified market concerns about a rebound in inflation.

US stock indicesTechnical perspectiveUnder heavy pressure, the Nasdaq fell into consolidation, and$S&P 500 Index (.SPX.US)$the S&P 500 broke below the key support level of the 200-day moving average for the first time since May 2025. As of the close on March 26, the S&P 500 had fallen 5.38% year-to-date, $Nasdaq Composite Index (.IXIC.US)$ with a year-to-date decline of approximately 8%. Over 80% of the components in the technology, consumer discretionary, and communication services sectors were once in a downtrend, and the VIX $CBOE Volatility S&P 500 Index (.VIX.US)$ also showed a noticeable increase.

![Before diving into an April full of suspense, let's first review the turbulent March in the US stock market. Throughout March, the US stock market did not continue its previous one-sided rise but instead exhibited a pattern of 'weak fluctuations under high volatility.' The ongoing escalation of Middle Eastern energy risks led to a sharp increase in crude oil prices, with Brent crude and US oil briefly surpassing $119 per barrel. The surge in oil prices directly heightened concerns about a rebound in inflation. US stock indices[Share Link: Technical perspective]Under mounting pressure, the Nasdaq index fell into consolidation, and$S&P 500 Index (.SPX.US)$fell below the key support level of the 200-day moving average for the first time since May 2025. As of the close on March 26, the S&P 500 had cumulatively declined by 5.38% year-to-date, $Nasdaq Composite Index (.IXIC.US)$ with a decline of approximately 8% year-to-date. Over 80% of the constituent stocks in the technology, discretionary consumption, and communication services sectors were once in a downward trend, and the VIX $CBOE Volatility S&P 500 Index (.VIX.US)$ also showed a significant increase. US stocks are about to face a series of new significant tests and catalysts in April. Macro data changes triggered by the situation in the Middle East will keep the market on edge, with the Fed’s moves at the end of the month remaining the top focus. Whether the Fed’s interest rate expectations for this year will change due to macro data shifts deserves strong attention. In addition, regarding the timing of US President Trump's visit to China, White House spokespersons and Trump himself indicated via posts that it would be delayed until May 14 to 15...](https://nnqimage.futunn.com/sns_client_feed/900104/20260327/web-1774595712466-UYXONVCpyB.png/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

The US stock market is about to face a series of new major tests and catalysts in April. Macro data changes triggered by the situation in the Middle East will affect market sentiment, and the Federal Reserve’s moves at the end of the month remain the focal point. Whether the Fed’s interest rate expectations for this year change due to macro data movements deserves strong attention.

In addition, regarding the timing of US President Trump's visit to China, White House spokespersons and Trump himself announced that it would be delayed until May 14-15, rather than late March or early April as previously planned. The Chinese Foreign Ministry stated that both sides are maintaining communication regarding President Trump’s visit to China.

To help fellow investors better grasp the main market trends and investment opportunities, Futubull has carefully compiled a list of must-know US stock financial events for April. It is recommended to bookmark it for future reference!

![Before diving into an April full of suspense, let's first review the turbulent March in the US stock market. Throughout March, the US stock market did not continue its previous one-sided rise but instead exhibited a pattern of 'weak fluctuations under high volatility.' The ongoing escalation of Middle Eastern energy risks led to a sharp increase in crude oil prices, with Brent crude and US oil briefly surpassing $119 per barrel. The surge in oil prices directly heightened concerns about a rebound in inflation. US stock indices[Share Link: Technical perspective]Under mounting pressure, the Nasdaq index fell into consolidation, and$S&P 500 Index (.SPX.US)$fell below the key support level of the 200-day moving average for the first time since May 2025. As of the close on March 26, the S&P 500 had cumulatively declined by 5.38% year-to-date, $Nasdaq Composite Index (.IXIC.US)$ with a decline of approximately 8% year-to-date. Over 80% of the constituent stocks in the technology, discretionary consumption, and communication services sectors were once in a downward trend, and the VIX $CBOE Volatility S&P 500 Index (.VIX.US)$ also showed a significant increase. US stocks are about to face a series of new significant tests and catalysts in April. Macro data changes triggered by the situation in the Middle East will keep the market on edge, with the Fed’s moves at the end of the month remaining the top focus. Whether the Fed’s interest rate expectations for this year will change due to macro data shifts deserves strong attention. In addition, regarding the timing of US President Trump's visit to China, White House spokespersons and Trump himself indicated via posts that it would be delayed until May 14 to 15...](https://nnqimage.futunn.com/sns_client_feed/900104/20260327/web-1774595716528-NlfQYQiHLT.png/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

1. Intensive macro data bombardment, with non-farm payroll and inflation data moving market sentiment.

At the beginning of the month, employment data will set the tone for the market. On April 1st, the US ADP employment numbers for March and the ISM manufacturing PMI will be released successively; then on April 3rd (Friday) at 20:30, the crucial US non-farm payroll data and unemployment rate for March will be announced, which is essential for assessing the current state of the US labor market.

Regarding inflation, several core indicators will take center stage. On April 9th, the US PCE price index for February and the final Q4 real GDP annualized quarterly rate will be released, delayed due to the previous shutdown of the US federal government. Subsequently, the most critical US CPI data for March will arrive on April 10th at 20:30, followed by the release of the US PPI data for March on April 14th.These inflation indicators will directly affect the market’s pricing of the Fed's subsequent policies.

Amid renewed entanglement between the Middle East situation and inflation outlook, two Federal Reserve governors spoke on Thursday, March 26th Eastern Time. Governor Cook stated that the balance of risks has now shifted, with inflation risks being higher than employment risks. She believes that inflation risks 'may last longer than expected.'

Milan estimated that under the existing operational framework, if the demand for bank reserves could be reduced, the Fed's asset size could potentially decrease by 1 to 2 trillion US dollars. He emphasized that the process of reducing the balance sheet must be 'very gradual' to allow financial markets time to adapt, and must be coordinated with interest rate policy to avoid market disruptions.

2. A new earnings season for US stocks kicks off, with Wall Street giants leading the way.

The bugle call for the earnings season has sounded again! From April 13th to 14th, a new earnings season for US stocks officially begins. $Goldman Sachs (GS.US)$ 、 $Citigroup (C.US)$ and $JPMorgan (JPM.US)$ Financial giants such as [omitted] will be among the first to announce their results. As a 'barometer' of the macroeconomy, the performance of these major banks and their forward-looking guidance will set the tone for the entire earnings season.

Analysts, amid ongoing tensions in the Middle East, continue to raise earnings expectations. Data from Bloomberg Intelligence shows that analysts expect S&P 500 component companies to see an 11.9% year-on-year increase in earnings for the first quarter of this year, up from the previous expectation of 10.9% before the Iran conflict erupted.

Data compiled by strategist Wendy Soong also shows that earnings and revenue expectations for the next three quarters have been raised by 1.9% and 1.5%, respectively, partly due to the continued fading impact of tariff shocks.

3. Tech giants gear up for another major event, keep an eye on Google Cloud Next 2026

In the technology sector, from April 22 to 24, $Alphabet-C (GOOG.US)$ the Google Cloud Next 2026 conference will be held in grand fashion. Against the backdrop of the ongoing AI wave sweeping across industries, focus on Google's latest technological breakthroughs and strategic layout in artificial intelligence and cloud computing.

The core theme of the conference is entering the 'Intelligent Agent' era, with a focus on showcasing how to build, deploy, and manage AI agents capable of reasoning and independently completing tasks. It will delve into the deep integration of the Gemini model with the Google Cloud ecosystem (such as Google Workspace, Vertex AI), highlighting real-world cases that demonstrate improvements in enterprise productivity.

Additionally, the market expects Google to present deployment data for its seventh-generation TPU and its self-developed ARM-based CPU Axion.

4. The Federal Reserve takes center stage, focusing on the Fed's FOMC interest rate decision

This month, the Federal Reserve remains the focal point. At 2:00 AM on April 9, the Fed will release the minutes of its March monetary policy meeting.

The real 'climax' will arrive at the end of the month. At 2:00 AM on April 30, the Federal Reserve's FOMC will announce its interest rate decision and summary of economic projections. Following that, at 2:30 AM, Federal Reserve Chair Powell will hold a press conference on monetary policy. On the same evening at 8:30 PM, the US March PCE price index will also be released. These back-to-back high-impact events are expected to trigger significant volatility in the US stock market and even global markets.

5. Special Reminder: Market Holidays

April 3 (Friday) is Good Friday, and the US stock market will be closed for the day. Fellow investors, please arrange your trading funds in advance.

Stay ahead with key financial events and discover investment opportunities early! Open Futubull > Market > US Stocks >Economic Calendar/Selected macroeconomic data, seize the investment opportunity!

Stay ahead with key financial events and discover investment opportunities early! Open Futubull > Market > US Stocks >Economic Calendar/Selected macroeconomic data, seize the investment opportunity!![Before diving into an April full of suspense, let's first review the turbulent March in the US stock market. Throughout March, the US stock market did not continue its previous one-sided rise but instead exhibited a pattern of 'weak fluctuations under high volatility.' The ongoing escalation of Middle Eastern energy risks led to a sharp increase in crude oil prices, with Brent crude and US oil briefly surpassing $119 per barrel. The surge in oil prices directly heightened concerns about a rebound in inflation. US stock indices[Share Link: Technical perspective]Under mounting pressure, the Nasdaq index fell into consolidation, and$S&P 500 Index (.SPX.US)$fell below the key support level of the 200-day moving average for the first time since May 2025. As of the close on March 26, the S&P 500 had cumulatively declined by 5.38% year-to-date, $Nasdaq Composite Index (.IXIC.US)$ with a decline of approximately 8% year-to-date. Over 80% of the constituent stocks in the technology, discretionary consumption, and communication services sectors were once in a downward trend, and the VIX $CBOE Volatility S&P 500 Index (.VIX.US)$ also showed a significant increase. US stocks are about to face a series of new significant tests and catalysts in April. Macro data changes triggered by the situation in the Middle East will keep the market on edge, with the Fed’s moves at the end of the month remaining the top focus. Whether the Fed’s interest rate expectations for this year will change due to macro data shifts deserves strong attention. In addition, regarding the timing of US President Trump's visit to China, White House spokespersons and Trump himself indicated via posts that it would be delayed until May 14 to 15...](https://nnqimage.futunn.com/sns_client_feed/900104/20260327/web-1774595712376-qcCrqysGJn.webp/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

Editor/Rocky

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

9

4