"AI Bottleneck Trade" Ignites Upstream Sector—Who’s Raking in the Profits?

The era of AI computing power 'inflation' has arrived! Unveiling how to capture the price hike transmission across the entire industry chain and investment opportunities.

An 'inflation' across the entire industry chain triggered by AI is intensifying.

Since 2026, the AI industry chain has been experiencing a strong structural price hike. Key components such as MLCCs (multi-layer ceramic chip capacitors), specialty PCBs, optical fibers, GPUs, CPUs, analog chips, power semiconductors, and cloud services have all entered an upward pricing trajectory.

It is worth noting that this is not a traditional general price increase,but rather a profound 'AI structural inflation.'With the rapid advancement of AI computing infrastructure, high-end components are facing intense 'demand suction.' Global capacity is concentrating in high value-added areas, ultimately triggering a wave of supply-demand mismatches and value restructuring across the entire industry chain.

So, what is the rhythm of this round of inflation? Why has this inflation sweeping through the AI industry chain occurred? What are the paths of price transmission and the investment logic? This article will explain these aspects one by one for fellow investors.

What is the rhythm of this round of inflation?

Starting from the middle of last year, $Alphabet-C (GOOG.US)$ 、 $Microsoft (MSFT.US)$ Driven by the exponential increase in Token consumption by overseas giants, the market has ushered in the first wave of activity centered around computing power. As GPU computing power directly determines the upper limit of Token supply, GPUs and their core supporting components (such as optical modules, PCBs, etc.) have taken off first.

Subsequently, the price hike effect spread deeper along the industrial chain. In January this year, with the surge in demand for ultra-long context memory from AI agents (Agent), segments such as HBM (High Bandwidth Memory) tightened in supply and officially entered a price hike phase; at the same time, expectations of price increases for CPUs also emerged. This cost pressure further passed down to downstream sectors, triggering collective price adjustments for cloud services. Led by Amazon AWS, six major cloud giants including Microsoft, Google, and domestic 'BAT' (Baidu, Alibaba, Tencent) successively announced price hikes.

Overall, this wave of 'computing power inflation' was initially triggered by upstream GPUs, gradually transmitted to memory and CPUs, then spread to cloud services, and is expected to eventually reach IDCs (Internet Data Centers), showing a clear pattern of spillover from upstream core hardware to downstream infrastructure.

Why has this inflation sweeping through the AI industrial chain occurred? What is the transmission path of the price hikes?

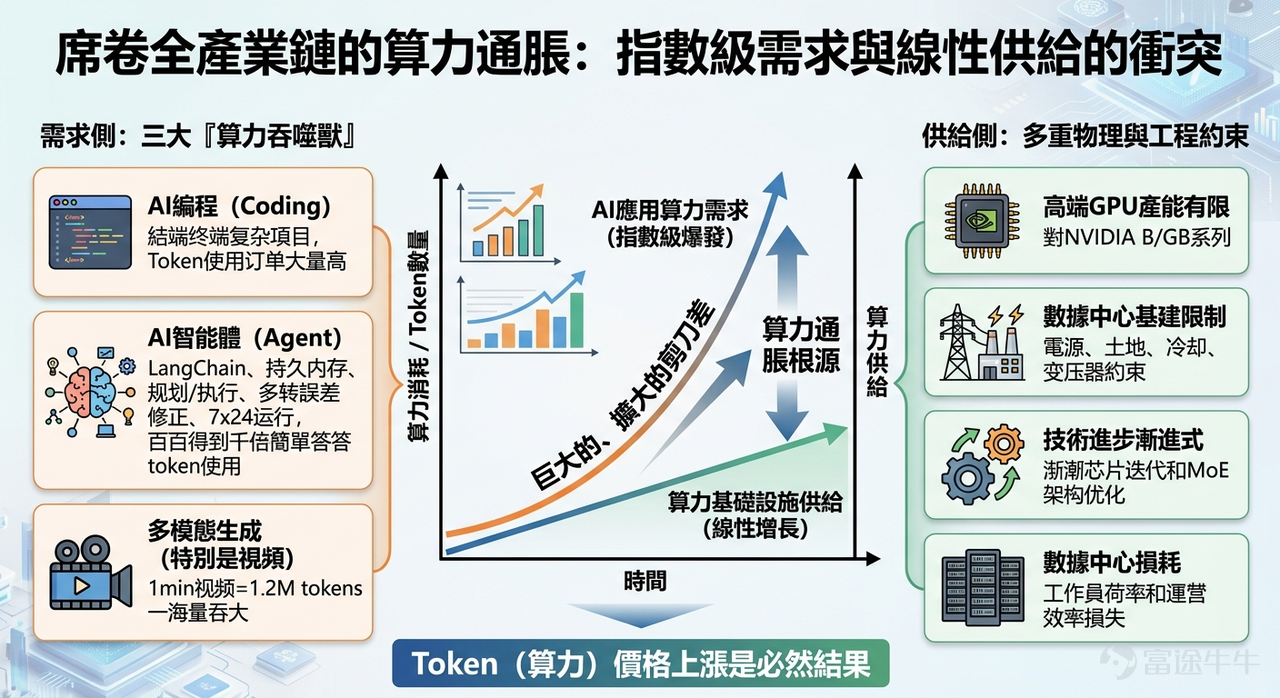

Exploring the underlying logic of this 'computing power inflation,' the core lies in an ever-expandingSupply-demand scissors gap: Exponential growth in demand on the AI application side, while the supply of computing power infrastructure can only maintain linear growth.

– Exponential leap on the demand side: The main consumers of computing power have fully upgraded.AI CodingAchieved end-to-end project delivery;AI agents need to run 24/7 with ultra-long context memory; and multimodal large models represented by video generation, require over 1.2 million tokens per minute for generation. These three major trends have led to an exponential increase in computational power consumption.

– Linear bottleneck on the supply side: Despite overseas cloud providers expecting a surge of 70-80% in capital expenditure, high-end GPUs (such as NVIDIA's B series, GB series) are facing production bottlenecks. At the same time, advanced packaging capacity, power supply, cooling systems (e.g., liquid cooling facilities), transformers, and other infrastructure deficiencies have become physical and engineering constraints for expanding computing power.

This significant supply-demand gap is the fundamental driver behind the recent surge in token and cloud service prices.

Overall, the linear growth trajectory of computing power supply is far from matching the exponential demand slope on the application side. This enormous supply-demand gap is the key reason for the recent price hikes in tokens and cloud services.

By clarifying the underlying logic of the supply-demand contradiction, the cost transmission path and investment focus of the AI industry chain become clear. This 'computing power inflation' strictly follows the rule of gradually spilling over from upstream to downstream of the industry chain. The core factors determining the pace of transmission lie in the competitive landscape and scarcity of each link, as shown in the figure below:

First is the most upstream segment (such as GPUs, HBM memory, advanced packaging).This field has extremely high technical barriers, showing a significant oligopolistic monopoly pattern, and its capacity expansion is most restricted by physical and process limitations. During surges in demand, its scarcity becomes most prominent, holding absolute pricing power, thus becoming the segment that experiences the first price increases and captures core benefits.

Next is the midstream infrastructure (such as cloud services, IDCs).This segment has more participants, leading to a more intense competitive environment (especially in the domestic market). Despite facing significant cost pressures, companies often delay price increases until leading firms take the initiative. This creates lag in the price transmission process, making investment certainty relatively weaker compared to upstream sectors.

Finally, we come to the downstream application side.With the comprehensive increase in underlying computing power resources and cloud service costs, some of the cost pressure will inevitably be passed on to end users.

What investment logic should investors adopt in response to AI-driven inflation?

In light of current supply-demand contradictions and price transmission pathways, the short- to medium-term investment logic can be clearly outlined as follows:

First, the short-term trading rhythm:Capital flows towards marginal opportunities. Currently, cloud services have just entered a price hike phase, quickly becoming a focal point for short-term capital inflows. Following this chain, the next 'expectation-driven speculation point' in the market will inevitably focus on midstream infrastructure like IDCs. This is essentially a right-side trading logic following the wave of price hikes moving downstream, profiting from the time lag in price transmission.

Next, the core of medium- to long-term allocation:The closer to the source, the stronger the logic. Over an extended investment horizon, asset certainty largely depends on its 'scarcity.' In this AI infrastructure boom, the most upstream sectors (chips, HBM storage, advanced packaging) face the strictest dual barriers of technology and physical production capacity. The strongest position means they have the greatest control over pricing and the highest likelihood of profit realization. Therefore, in portfolio construction, emphasis must shift upstream, heavily weighting these sectors to secure higher odds of success, while downstream sectors serve as satellite positions for speculative gains.

Lastly, the cyclical nature of market trends:The continuous reevaluation of total supply logic. Computational power inflation is not a one-time event but rather an upward spiral. While the market is still focused on the current computational bottlenecks, once the next wave of strong applications (such as world models or physics simulations) explodes, Token consumption will see a new exponential surge. This qualitative change on the 'demand side' will directly force the market to reassess the 'total supply logic' across the entire industry and will likely trigger another round of valuation restructuring across the whole industry chain, starting from core sectors like GPUs.

In summary,The further upstream the computational power chain (chips, memory, GPUs),,the greater the physical constraints and the more advantageous the industrial landscape,the stronger and longer-lasting the certainty of price increases.;The further downstream,(cloud services, IDCs), the more vendors there are and the fiercer the competition,the weaker the certainty of price increases.

Based on this, fellow investor Niuniu has compiled a related chart for investors' reference:

The first wave: The absolutely scarce 'core computing engines' and 'contract manufacturing/packaging'

Since GPU computing power directly determines the upper limit of Token supply,Core computing engine - chipsExploded first.

Computing brain:Dominating here are oligarchs with absolute pricing power, such as $NVIDIA (NVDA.US)$、 $Advanced Micro Devices (AMD.US)$、 $Broadcom (AVGO.US)$ 。

Capacity lifeline:Once a chip is designed, it must rely on“Wafer fabrication” and “advanced packaging and testing”. Taiwan Semiconductoroccupies a core position here, while companies like $SMIC (00981.HK)$ 、 $ASE Technology (ASX.US)$ 、 $Amkor Technology (AMKR.US)$and $ASMPT (00522.HK)$ are also experiencing a revaluation due to tight capacity.

The second wave: Expansion extends into 'storage' and 'communication networks'

As the demand for AI agents with ultra-long context memory surges, price hikes are spreading rapidly.

Storage price hikes: It's a foregone conclusion that storage chip prices will rise in 2026. DRAM is expected to increase by 60%-88% for the year, while NAND could see increases of 38%-74%. Related companies such as $CSOP Samsung Electronics Daily (2x) Leveraged Product (07747.HK)$、 $CSOP SK Hynix Daily (2x) Leveraged Product (07709.HK)$、 $Micron Technology (MU.US)$、 $SanDisk (SNDK.US)$have seen astonishing gains this year.

Optical communication infrastructure: The larger the computing cluster, the higher the communication requirements between nodes. This has spurred a massive 'optical communication network'sector rally. From silicon photonics manufacturers $Marvell Technology (MRVL.US)$ 、 $Fabrinet (FN.US)$, to optical module leaders $Lumentum (LITE.US)$ 、 $Coherent (COHR.US)$, to fiber-optic segment players $Corning (GLW.US)$and$YOFC (06869.HK)$ , indium phosphide $AXT Inc (AXTI.US)$ The entire supply chain is benefiting from the spillover of demand.

Notably, Prices for mainstream fiber optic varieties, particularly bulk fiber, continue to rise,especially for high-end bend-insensitive fiber G.657A2, with high-priced orders surpassing 250 yuan/core kilometer, and order volumes remaining consistently strong. Regular varieties such as G.652D also maintain a robust upward trend, reflecting an industry pattern of 'rising volume and price.'

Additionally, compared to prices at the beginning of 2025,the price of indium phosphide substrates has recently increased,with domestic market increases of around 15%, while international markets have seen rises of about 60%.

Third wave: Spreading to surrounding 'infrastructure' and 'cloud/model' sectors

The enormous computational power beast requires massive energy and extreme cooling to sustain operations.

Energy and Cooling:Infrastructure and key componentsand intermediarypower management and analog chipsare beginning to gain momentum. $Texas Instruments (TXN.US)$、 $Monolithic Power Systems (MPWR.US)$Analog chip and power management giants, as well as those specializing in liquid cooling solutions, $Vertiv Holdings (VRT.US)$are becoming the "water carriers" of the market. Meanwhile, underlying materials like CCL copper-clad laminates (e.g., $KINGBOARD HLDG (00148.HK)$ ) and MLCCs (e.g., $Vishay Intertechnology (VSH.US)$ ) are experiencing both volume and price increases due to a surge in high-end demand.

Cost pass-through: Ultimately, cost pressures will be passed on tomodel providers/cloud service providers.。 $Amazon (AMZN.US)$、 $Alphabet-C (GOOG.US)$、 $TENCENT (00700.HK)$As major players, and $Z.AI (02513.HK)$、 $MINIMAX-W (00100.HK)$ have gradually started raising prices, passing inflation down to end users.

Summary

Overall, this 'AI computing power inflation' sweeping across the entire industry chain is essentially a value restructuring of the global tech landscape. The supply-demand imbalance in computing power will remain a core driver of market pricing for a long time to come.

For investors, the best strategy to deal with this inflation has already been clearly laid out in the blueprint:

1. Core holdings focus on 'scarcity': Closely monitor leading companies in chips, wafer fabrication, and advanced packaging at the core of the blueprint. The higher the physical barriers and stronger the oligopolistic effects, the better they can lock in long-term success rates for us.

2. Satellite positions follow 'transmission gaps': Flexibly deploy in optical communication, liquid cooling, and power management on both sides of the blueprint. Align with the rhythm of capital spillover to peripheral infrastructure after cloud giants raise prices, and speculate on medium- and short-term odds.

3. Always watch for 'demand leaps': Stay sharp on model applications. Any groundbreaking application will herald the next round of valuation reassessment across the entire industry chain.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

72

159