The era of AI-powered payments has arrived. Circle (CRCL.US) is making a strong bet on it—what does the future hold? | In-depth Analysis | Research Report | Growth Stocks | Stablecoins

The year 2026 has been defined by the industry as the first year of AI agent commerce. AI agent payment, as the core closed loop in the AI economy transitioning from 'decision-making' to 'execution,' is reaching a critical inflection point moving from concept to scaled commercial application. It is expected to drive annual transaction volumes exceeding tens of billions of dollars within 5-10 years. $Circle (CRCL.US)$ As the issuer of USDC, the global compliant stablecoin, Circle is leveraging its three core advantages—technology, compliance, and ecosystem—to fully invest in this emerging growth track that has yet to fully explode. Since 2025, $Circle (CRCL.US)$ the company’s performance has achieved rapid growth, with cumulative stock price increases of over 58.93% since the beginning of 2026. The key drivers have been better-than-expected fundamentals, regulatory tailwinds, global geopolitical dynamics, and valuation system restructuring driven by the narrative of AI agent payments. In the medium to long term, as the number of AI agents grows exponentially, AI-driven transaction volumes are expected to surpass human transaction volumes, $Circle (CRCL.US)$ evolving from being the leading stablecoin provider into a core financial infrastructure operator for the next generation of internet economies, continuously expanding long-term growth potential.

The large-scale implementation of AI agents is driving a fundamental transformation in the payment system from 'human-led' to 'machine-native.' The AI agent payment sector has entered the explosive tipping point from 0 to 1. As the issuer of USDC, the world's second-largest compliant stablecoin, $Circle (CRCL.US)$ Circle is making an all-in bet on this track through full ecosystem deployment, positioning AI agent payments as the core growth engine for the next phase of stablecoins. Bloomberg reports indicate that $Circle (CRCL.US)$ internet groups are developing a payment infrastructure for a future-oriented world. In this new era of transactions, autonomous AI agents will become the main transaction drivers, capable of completing millions of transactions per day. Stablecoins, rather than the currently dominant credit card payment methods, will serve as the settlement tool supporting these massive volumes of transactions.

Service interactions and consumption scenarios between AI agents are expected to see widespread adoption. Typical application scenarios include AI agents with legal service capabilities that can handle service requests initiated by external agents representing business operations; or agents responsible for data extraction and basic information queries where each service fee may only be a few cents. Traditional bank card payment models, which use fixed fees plus percentage-based charges, are commercially unfeasible for such small transactions. Addressing this industry pain point, $Circle (CRCL.US)$ Circle launched Arc, a new blockchain specifically designed for stablecoin payment scenarios, and recently began testing a new feature called 'Agent Pay.' This feature allows autonomous AI agents to hold account balances and execute cross-network payments at transaction costs as low as a fraction of a cent, enabling the commercial viability of machine-to-machine microtransactions—a capability fundamentally unmatched by traditional bank card fee structures. March 11, 2026,MasterCard officially announced the launch of its Crypto Partner Program, bringing together over 85 global crypto, blockchain, and financial institutions to build a compliant crypto payment ecosystem alliance covering the entire industry chain. This is not a one-off concept trial but a deep acceptance and strategic integration of blockchain technology by traditional payment networks.

Contrary to the early crypto industry narrative of 'decentralization against regulation,' the current implementation of stablecoins and AI agent payments is proceeding entirely along a compliance-oriented path. The core premise of MasterCard's crypto partner program is to unify compliance standards, anti-money laundering rules, and cross-border operational norms, addressing the biggest obstacle to integrating digital assets into everyday commercial activities. $Circle (CRCL.US)$ The deep involvement of institutions like Circle has also made compliant stablecoins the core medium connecting on-chain and off-chain financial systems.As countries around the world gradually implement regulatory frameworks for stablecoins, stablecoins are transitioning from a 'regulatory gray area' to becoming regulated global financial infrastructure. Their application scenarios will expand from niche crypto circles to mainstream financial use cases such as international trade, cross-border remittances, and corporate treasury management.

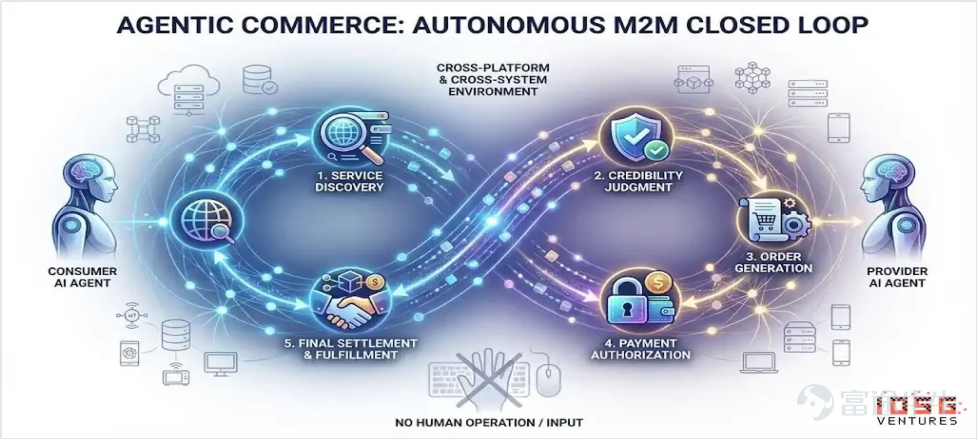

Figure 1: AI Agent Commerce - A Seamless Loop of Fully Automated Transactions and Payments

Data Source: Wind, IOSG VENTURES

– Dual Drivers of AI Payments and Stablecoins: Unleashing a New Era of Transformation in the Financial Payment System

Two seemingly parallel tracks—AI Agents and stablecoins—are forming strong synergies, reshaping the future structure of the global financial system. For a long time, financial transactions have faced significant friction costs, including lengthy settlement cycles, high fees, and cumbersome manual approval processes, severely limiting improvements in transaction efficiency. The core value of stablecoins lies in eliminating these transaction frictions at the foundational level; meanwhile, the scaled application of AI Agents is pushing this 'frictionless' transaction model into an unprecedented era of high-frequency trading. When real-time fund movement and intelligent decision-making achieve ultimate synergy, the underlying architecture of the global financial system will face fundamental transformation needs.

The core of AI Agent payments represents a fundamental shift in the payment entity from 'human' to 'machine,' referred to as the fifth evolution of the payment industry. Its key transaction characteristics include ultra-high frequency micro-transactions, autonomous decision-making, machine-to-machine (M2M) interaction, programmability, second-level settlement, low-cost cross-border transactions, perfectly catering to scenarios that traditional payment systems cannot cover, such as API calls, computing power procurement, content copyright payments, and cross-border micro-settlements. These form the core infrastructure enabling the commercial loop of the AI Agent economy. Currently, stablecoins have already built an efficient underlying channel for cross-border payments, while the widespread adoption of AI Agents will fully unlock the transaction potential of this channel. In the future, every market participant may own multiple dedicated AI Agents for automating various business and daily tasks, generating continuous, massive-scale payment demands. Such demands cannot be met through traditional payment channels and can only be supported by stablecoins capable of instant settlement at this scale and frequency. This industrial trend has drawn attention from global mainstream regulators: last year, the Federal Reserve listed 'AI and Payment Innovation' and 'Stablecoin Application Practices' as core topics in payment innovation conferences, marking the formal entry of these two directions into mainstream policy focus. Fundamentally, AI and stablecoins possess natural compatibility. AI Agents operate without borders, simultaneously leveraging globally distributed computing power, purchasing digital goods and services across borders, and paying developers worldwide; whereas traditional banking systems inherently feature national and local currency attributes, making them unsuitable for the global operational needs of AI Agents.Through a unified global monetary standard, stablecoins enable low-cost, real-time cross-border settlements, providing a seamless payment experience akin to local transactions.

More critically, the operational model of AI Agents is naturally suited to high-frequency micropayments and condition-triggered transaction logic: a complete task can be broken down into hundreds of API calls, each requiring automated settlement and split-accounting. Traditional credit card payments and bank transfer models are entirely unsuitable for such high-frequency transaction scenarios; whereas the programmability and smart contract functionality of stablecoins can transform payment actions into embedded 'smart execution actions', enabling automatic payment upon task completion and automated settlement based on usage levels. From a deeper industrial logic perspective, payment actions in the AI ecosystem serve not only as carriers of fund flow but also as critical entry points for core information flow. Traditional payment records retain only basic information such as transaction amounts and times, lacking full business context; whereas blockchain-based stablecoin transactions inherently possess traceable and instantly readable data attributes, making their payment data itself a core asset for AI Agent training iterations and strategy optimization. This means thatStablecoins not only address the payment execution challenges of the AI era but also unlock intelligent growth potential that traditional financial systems cannot support.

Figure 2: Comparison dimensions between traditional fiat payments and compliant stablecoin payments

Data source: Company financial reports

*AI Agent payment track offers vast space with a clear competitive landscape in the industry

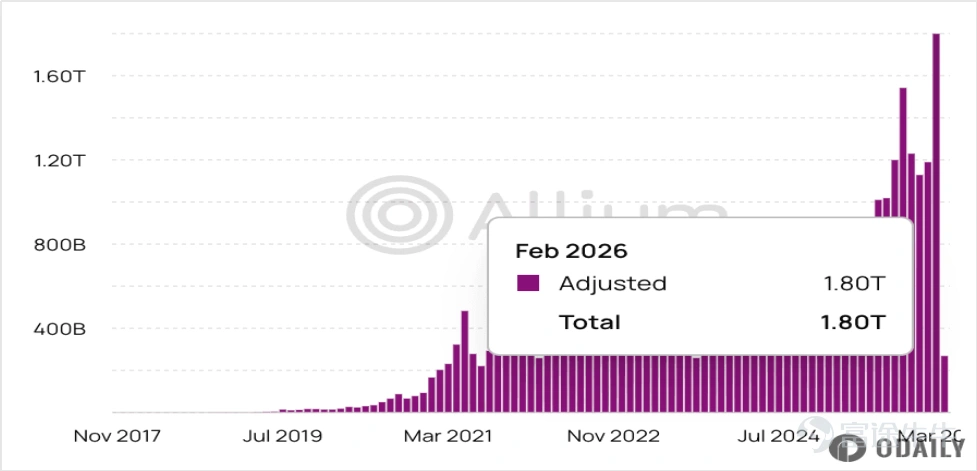

Currently, the AI Agent payment track remains in the critical phase transitioning from early commercial validation to scaled implementation. Although the absolute transaction scale is still relatively small, growth momentum is strong, infrastructure is rapidly taking shape, and transaction structures and market patterns have already presented clear industry characteristics. According to $Circle (CRCL.US)$the latest disclosed official data, during the nine-month period from July 2025 to March 2026,globally, AI Agents completed a cumulative total of 140 million payment transactions with a cumulative transaction value of approximately $43 million, showing low penetration within the $1.8 trillion monthly stablecoin trading volume, indicating significant market growth potential.

Figure 3: Number of stablecoin transactions per month over recent years

Data source: Allium

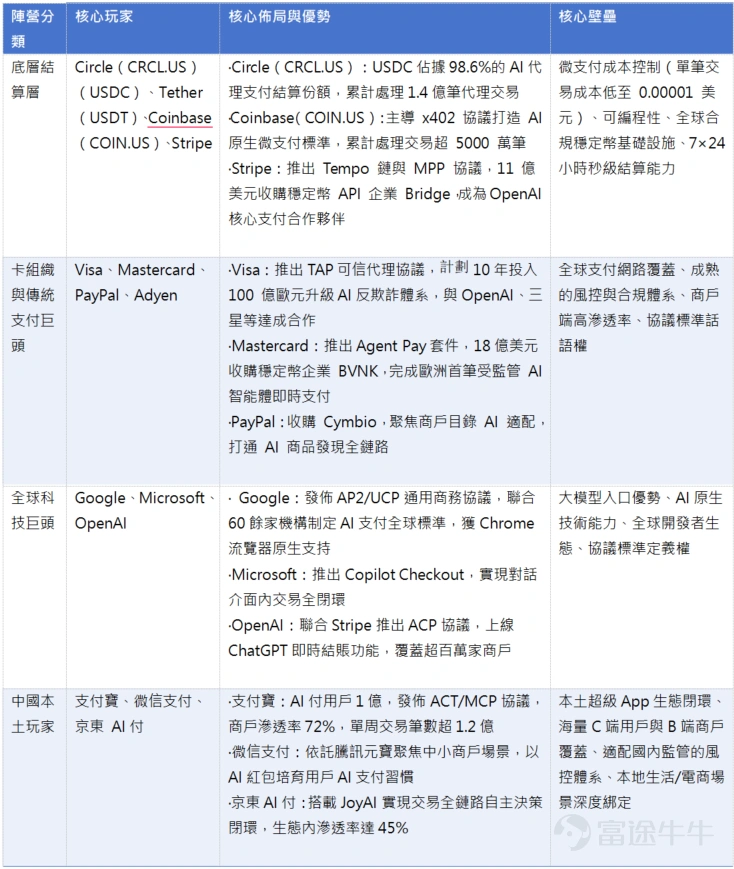

In terms of the competitive landscape, a clear echelon-based competitive pattern has formed in the global arena. Players on this track are divided into four core competitive camps based on their core competencies and strategic directions. The first group consists of players operating at the underlying settlement layer, represented by $Circle (CRCL.US)$ , Tether, $Coinbase (COIN.US)$ , and Stripe. These players leverage the programmability of stablecoins and ultra-low-cost micro-settlement capabilities to dominate the majority of global AI agent payment settlements. They lead the foundational protocols and technical standards for AI-native micropayments, forming the core infrastructure for large-scale transactions overseas. The second group includes card organizations and traditional payment giants like Visa, Mastercard, PayPal, and Adyen. Relying on mature global payment networks, high merchant penetration, and robust compliance risk control systems, they quickly launched specialized payment suites tailored for AI agents. Through acquisitions, they have also supplemented their stablecoin and blockchain technological capabilities, competing for industry influence as traditional payment systems transition into the AI era. The third group comprises global tech giants such as Google, Microsoft, and OpenAI, who hold the advantage of controlling access to large language models and a vast developer ecosystem. Focused on establishing universal commerce protocols and AI-native payment standards, they achieve transaction closures within conversational interfaces through deep integration with native large models, making them pivotal forces in shaping the foundational rules of the industry. The fourth group is composed of China-based players, primarily Alipay and WeChat Pay, which rely on massive C-end user bases from their super apps, B-end merchant resources, and well-established e-commerce and local life scenarios to rapidly scale AI payment products, firmly securing dominance in the domestic market.

Figure 4: Competitive Landscape of AI Agent Payments

Data Source: Financial reports from the above companies

*Addressing the core drawbacks of micropayments, USDC aims to become the foundational payment layer for AI agents

The monthly trading volume of stablecoins reaching $1.8 trillion confirms that stablecoins have gained widespread acceptance in the global market; meanwhile, the completion of 140 million AI agent payment orders marks the official start of the 'Agent Finance' era. Over the past nine months, more than 400,000 AI agents with autonomous purchasing capabilities have demonstrated exceptionally high payment activity, with 98.6% of transactions conducted via USDC. USDC has emerged as the dominant standard in the AI agent payment sector. Its near-monopoly market penetration stems from its precise resolution of the fundamental pain points underlying the Agent economy. $Circle (CRCL.US)$ Data disclosed by Peter Schroeder, Global Head of Markets, shows that the average transaction amount per AI agent payment is just $0.31, directly highlighting the core bottleneck of the Agent economy — the cost challenges of high-frequency micropayments.

During task execution, AI agents must continuously pay fragmented costs such as API calls, computational power rentals, and data collection. In traditional banking and credit card payment systems, transferring $0.31 often incurs fees exceeding the principal itself. This high-cost structure renders traditional payment channels unsuitable for AI agent payment needs. While cost advantages represent surface-level competitiveness, the true driver behind AI agents choosing USDC lies in $Circle (CRCL.US)$ the comprehensive technical components and ecosystem adaptability provided by the platform. $Circle (CRCL.US)$ The programmable payment suite launched supports developers in directly embedding wallet management logic into AI code. Relying on the Model Context Protocol (MCP) server, developers can enable mainstream AI tools such as Claude, Cursor, and Windsurf to directly generate USDC payment invocation scripts, offering extreme ease of development that has made USDC the default option for Agent payments. The Cross-Chain Transfer Protocol (CCTP) completes the final link for practical implementation. AI Agents mostly operate on low-cost, high-concurrency Layer 2 networks and high-performance public chains like Base and Solana, where the single transaction fee for USDC is less than one cent and settlement can be achieved within seconds. At the same time, CCTP enables seamless liquidity migration between different blockchains, perfectly accommodating the core requirement of frequent cross-chain resource calls by AI Agents.

Currently,$Circle (CRCL.US)$ is experiencing its own 'golden cross': First, the continuous strengthening of its fundamentals has raised the valuation center. $Circle (CRCL.US)$ The company's Q4 financial results for the fiscal year 2025 comprehensively exceeded market expectations: On the profitability side, it achieved earnings per share of $0.56 in a single quarter, significantly higher than the analysts' consensus expectation of $0.17; on the revenue side, quarterly sales reached $7.7 billion, surpassing the analysts' consensus expectation of $7.4 billion, representing a substantial year-over-year increase of 76.92% from last year’s $4.3 billion revenue. In terms of core business data, by the end of 2025, the circulation scale of USDC reached $75.3 billion, up 72% year-over-year; in Q4 2025 alone, the on-chain transaction volume of USDC reached $11.9 trillion, achieving an explosive growth of 247% year-over-year. Additionally, at the macro level, escalating geopolitical conflicts in the Middle East have dampened market expectations for Federal Reserve rate cuts, with interest rates likely to remain high, directly boosting interest income from the company's reserve assets, reinforcing its core profit logic.Meanwhile, geopolitical conflicts have disrupted traditional cross-border financial channels, driving up demand for stablecoins both as a safe haven and for cross-border payments, with the circulation of USDC continuously reaching new historical highs, further expanding the growth space for performance.

In the emerging AI payment track, the narrative of AI agent payments brings about a revaluation of the valuation system, opening up $Circle (CRCL.US)$ long-term growth potential. $Circle (CRCL.US)$ The advantageous positioning within the ecosystem has driven long-term growth expectations, while breakthroughs in the AI Agent payment track have opened up a completely new blue ocean market. $Circle (CRCL.US)$ The disclosed financial report shows that the current transaction scale of the AI agent payment track is limited in absolute terms, but the transaction structure presents highly valuable industry-referential characteristics. According to $Circle (CRCL.US)$ official data released by the Global Head of Payments in March, over the past nine months, AI agents have cumulatively completed 140 million payment transactions, with a total transaction size of $43 million; 98.6% of these transactions were settled via USDC, with an average transaction amount of $0.31 per transaction, and the number of AI agents currently possessing autonomous purchasing power has surpassed 400,000. Overall, although the dollar scale of transactions in this track remains relatively low at present, its explosive growth trend cannot be ignored. In an uncertain industry cycle, AI agent payment is the most value-creating business model with long-term potential, poised to become the foundational infrastructure defining industry certainty. $Circle (CRCL.US)$stands at the intersection of global settlement network hegemony and Agent monetary sovereignty, building a compliant payment infrastructure for the impending era of AI civilization, and its embryonic form as the 'central bank of the digital economy era' has begun to emerge.

As of March 20, 2026, $Circle (CRCL.US)$ the closing price was $126.03, with a cumulative increase of 58.93% year-to-date in 2026, and a rise exceeding 51.04% over the past month, reaching an all-time high since its listing. In summary,this round of strong stock price growth is the result of the resonance of four major factors: fundamental business performance, macro-regulation, valuation restructuring, and trading dynamics. Among them, the long-term narrative of AI agent payment is the core logic driving the shift in valuation.

Source: Wind

Overall, the short-term high-interest-rate environment will continue to be maintained, and USDC’s circulation and market share are expected to keep rising. $Circle (CRCL.US)$ The company’s core earnings are expected to continue surpassing market expectations, and its profitability stability will further strengthen. Meanwhile, the commercialization process of AI agent payments is accelerating, providing continuous valuation catalysts for the company. In the medium to long term, the explosion of the AI agent economy is a certainty, and AI agent payments will become a core growth point in the next generation of the payment industry, with vast market potential. $Circle (CRCL.US)$ With a full-stack technology layout, an absolute first-mover advantage, an irreplaceable compliance barrier, and a robust ecosystem network, Circle (CRCL.US) has firmly established itself as the dominant player in the AI agent payment sector, and USDC is expected to become the mainstream currency in the AI agent payment world. From a competitive landscape perspective, no players can shake Circle’s (CRCL.US) monopoly position in the AI agent payment track in the short term. Traditional payment giants’ core architectural weaknesses will be difficult to resolve in the near future, blockchain-native competitors cannot overcome their compliance shortcomings, and emerging players can only achieve minimal breakthroughs in niche scenarios.With the exponential growth in the number of AI agents, transaction volumes between AI agents are expected to far exceed human transaction scales. Circle (CRCL.US), currently the leading stablecoin provider, will evolve into a core financial infrastructure operator for the next-generation internet economy, gradually unlocking significant long-term growth potential.

Disclaimer: Any information provided in this report regarding or related to any investment or potential transaction is subject to the applicable laws and regulatory requirements of your jurisdiction, and you are solely responsible for ensuring compliance with such laws and regulations. The content of this report is for reference purposes only and does not constitute investment advice. Our company has made every effort to ensure the accuracy of the financial information provided, but we assume no responsibility or provide any form of guarantee regarding the accuracy, completeness, or effectiveness of all or any part of the content. We will not be held liable for any errors or omissions. Please also note that securities and virtual asset prices can fluctuate, particularly with very high risks associated with virtual assets, and investors should exercise caution and bear investment risks on their own.

———————————————————————

About the author:

Victory Securities - Hong Kong's Leading Virtual Asset Broker

Victory Securities (08540.HK), with over 50 years of history in Hong Kong, is a comprehensive full-service licensed brokerage offering four main business services to retail investors, institutional investors, high-net-worth clients, and enterprises: wealth management, asset management, virtual assets, and capital markets. It has received numerous accolades and essential qualifications in the Asia-Pacific region. In 2023, Victory Securities became the first licensed brokerage in Hong Kong to hold licenses issued by the Securities and Futures Commission for virtual asset trading, advisory, and asset management services. It was also approved by the SFC to provide virtual asset trading and advisory services to retail investors, offering one-stop compliant and legal Bitcoin and Ethereum trading, exchange, and deposit/withdrawal services.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comment (1)

to post a comment

5