Industry Leader Reports Results: China Hongqiao's 22.6 Billion Net Profit Signals the Start of Genuine Value Reassessment

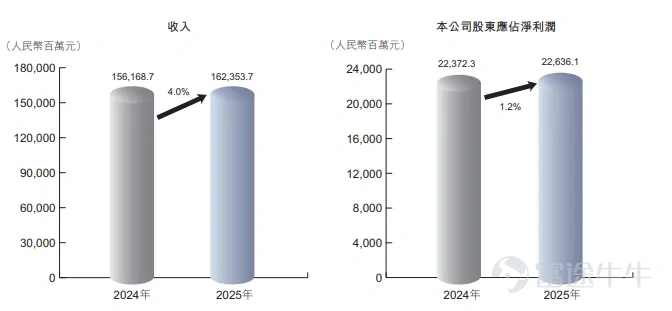

On March 20, China Hongqiao (01378.HK)$CHINAHONGQIAO (01378.HK)$ released its full-year 2025 performance: revenue of 162.354 billion yuan, up 4.0% year-on-year; net profit attributable to shareholders of 22.636 billion yuan, up 1.2% year-on-year; basic earnings per share of 2.3842 yuan.

An "unremarkable" annual report hides an underestimated fact.

At first glance, the profit only rose by 1.2%, which seems uneventful. However, when you break down the numbers, the value of this report card is much higher than it appears.

The average price for electrolytic aluminum in 2025 was just 18,216 yuan per ton, only about 3.8% higher than in 2024—many incorrectly project the spike in aluminum prices to 24,000 yuan in Q1 of this year onto last year. Meanwhile, the average price for alumina plummeted 15.2% to 2,899 yuan per ton. Between one increase and one decrease, the gross profit per ton of the company’s core product, electrolytic aluminum, surged from 4,313 yuan to 5,183 yuan, marking a year-on-year increase of 20.1%.

In other words, despite aluminum prices not rising significantly, profits continued to grow, which is not due to luck but rather the hard strength of cost control.

Full industry chain moat: The 'stabilizing force' amidst aluminum price fluctuations

China Hongqiao's core competitiveness can be summarized in six words: integration of upstream and downstream operations.

Looking upstream, the group's early-year investments in overseas bauxite resources, with stable supply from Guinea's mines, have ensured controllable raw material costs. The midstream alumina production capacity is sufficient, with external sales reaching 13.397 million tons by 2025, most of which is used internally to lock in internal costs. On the energy front, self-generated power in Shandong combined with hydropower in Yunnan has led to a continuous increase in the proportion of green electricity. The annual production of 250,000 tons of high-precision aluminum alloy ingots at Hongyan in Yunnan has officially commenced, further solidifying the framework for the green aluminum strategy.

This complete chain from ore to end products gives Hongqiao a cost buffer in aluminum price fluctuation cycles that peers find hard to replicate. The decrease in bauxite prices and savings in hydropower costs in 2025 effectively offset profit erosion caused by falling alumina prices.

The numbers speak volumes: net operating cash flow amounted to 42.658 billion yuan, up 8.3% year-on-year; cash reserves reached 51.187 billion yuan, an increase of 14.3% year-on-year; and the debt-to-asset ratio dropped to 42.2%, down six percentage points from the previous year. A heavy-asset manufacturing enterprise earning 22.6 billion yuan annually, holding 51.2 billion yuan in cash, with a debt ratio just over 40%, ranks among the top performers across the entire Hong Kong stock market.

Generous dividend payouts: 65% payout ratio, nearly 5% dividend yield

Hongqiao’s shareholder returns have always been a topic of keen interest in the market.

The final 2025 dividend was HKD 1.65 per share, with an annual payout ratio of approximately 65%, corresponding to a dividend yield of nearly 5% based on recent share prices. Additionally, the company spent HKD 5.58 billion during the year to repurchase and cancel 306 million shares, creating value for shareholders with tangible actions.

High dividends plus significant buybacks set a benchmark in the Hong Kong resource sector. For long-term funds seeking stable cash returns, this itself constitutes an attractive 'safety cushion.'

Profit elasticity for 2026: a simple arithmetic problem

If 2025 performance can be described as 'stable,' what truly excites for 2026 is the 'elasticity.'

The key variable lies in aluminum prices. The average electrolytic aluminum price in 2025 was about 18,216 yuan per ton (excluding VAT), while the average price in the first quarter of 2026 had already surged to approximately 24,000 yuan.

Based on the production capacity of 5.82 million tons, if the average annual price remains around 24,000 yuan, there will be an additional marginal profit of over 3,000 yuan per ton. After deducting approximately 27% in marginal tax, this means that for electrolytic aluminum alone, after-tax profits could see a significant increase.

This does not yet account for cost savings from Yunnan's hydropower operating year-round, reductions in new energy project costs, and favorable impacts from falling bauxite prices. Although partially offset by rising coal prices, the overall trend is clear — the profit potential for 2026 could far exceed current market pricing.

The 'asymmetry' of aluminum prices: Why aluminum may represent the clearest upward logic at present

Looking at the industry level, the supply-demand dynamics of aluminum are undergoing structural changes.

Supply-side is highly rigid. China’s electrolytic aluminum production cap is about 45 million tons, with 2025 output projected at 44.23 million tons, meaning capacity utilization is approaching 99%, leaving extremely limited room for growth. Globally, high electricity prices in Europe are suppressing restarts, while Indonesia's new projects are underperforming expectations, leading to continued tightness in overseas supply.

Geopolitical risks amplify supply vulnerability. The Middle East produces about 6.8 million tons of aluminum, accounting for roughly 7% of global supply, or 18% excluding China. Recent tensions between the US and Iran have been escalating, and any disruption to logistics in the Strait of Hormuz would leave Middle Eastern aluminum plants with only about one month of alumina inventory to operate at full capacity.

Once electrolytic aluminum reduces its load, it takes 4-6 months to recover. Analysts from Yangtze Securities’ metals team pointed out,In either a stagflation or recovery scenario, electrolytic aluminum stands to benefit.The market could first lose 400,000 to 500,000 tons of effective supply monthly, and demand would need to drop GDP forecasts by over 3% to fully offset this gap — a shock magnitude already considered extreme. On the demand side, structural improvements are evident. In 2025, China’s electrolytic aluminum consumption is expected to reach 46.34 million tons, up 2.6% year-on-year, with aluminum products and alloy exports making up 25% of the consumption structure. Continued growth drivers include transportation (lightweighting), electronics and power (new energy), and packaging containers. The AI-driven wave of global power infrastructure investment is creating new demand growth opportunities for aluminum. Goldman Sachs has put it more bluntly: aluminum represents the cleanest upward expression today.

Goldman Sachs recently stated that if the Middle East experiences a full month of production halts, aluminum prices will stage a temporary rise to3,600 US dollars per ton;As the market anticipates an extended period of supply disruptions, forecast values have been further revised upwards. Another US investment bank, Citi, has raised its aluminum price forecast for the next three months to3,600 US dollars per ton,and pointed out that in anoptimistic scenario,aluminum prices could climb to4,000 US dollars per ton.

(Top headlines from overseas media, screenshot source: Argus Media)

A vote of confidence from the capital markets: A 'milestone' on the financing front

In 2025, Hongqiao is also making frequent moves in the capital markets.

The company issued a total of 12.6 billion yuan in short-term financing, medium-term notes, and corporate bonds domestically; overseas, it completed two US dollar bond issuances totaling 600 million US dollars (including 330 million US dollars in senior notes that were over 10 times oversubscribed, setting a record for the lowest coupon rate among similar bonds issued by non-urban investment Chinese enterprises since February 2022); it issued 300 million US dollars in convertible bonds with simultaneous buybacks, becoming the first composite financing case of 'convertible bonds + buyback' in Hong Kong stocks; it also completed a 1.5 billion US dollars placement of existing shares followed by new shares issuance, which was 7 times oversubscribed with participation from several global top-tier long-term funds.

Upgrades in domestic and international credit ratings and continuous optimization of financing costs—these are votes of confidence cast by the capital markets with real money.

Conclusion: An undervalued leader across the entire industrial chain awaits repricing.

Taking a broader view, the investment landscape of China Hongqiao is becoming increasingly clear: cost advantages across the entire industrial chain form a deep moat, a low debt ratio of 42.2% and cash reserves of 51.2 billion yuan provide ample safety margins, a dividend payout ratio of 65% and a dividend yield of nearly 5% offer stable returns to holders, while profit elasticity driven by rising aluminum prices in 2026 has yet to be fully priced in by the market.

Coupled with the tight balance in global aluminum supply and demand and catalyzed by geopolitical risks, this world’s second-largest aluminum company stands at the starting point of an accelerated profit release phase.

Peter Lynch often said, 'When buying stocks, look at future earnings, not past financial statements.' The 2025 report card demonstrates Hongqiao's ability to navigate through cycles, but the story of 2026 might just be the truly anticipated chapter.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

1

5