Raising 'lobsters' drives up computing power demand! Where are the investment opportunities?

Why invest in Asian semiconductors at the current juncture?

1. Four major regional barriers with deep foundations, each with its own strengths

1) Mainland China: Anchoring the core position of domestic substitution, focusing on key industry leaders

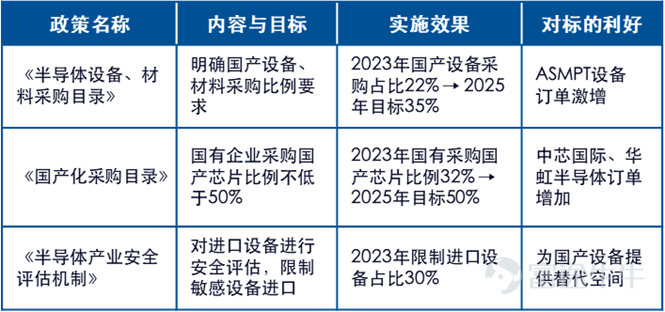

China's semiconductor industry is currently in a critical window period for 'domestic substitution,' coupled with strong support from 'protective policies,' forming an irreversible upward cycle for the industry. According to data from the 'China Semiconductor Industry White Paper 2025,' China's semiconductor self-sufficiency rate increased from 15% in 2019 to 28% in 2024, but still relies on imports for 72%, leaving significant room for domestic substitution. On the other hand, policy protection continues to tilt, with ongoing capital injections from the National Integrated Circuit Fund and local governments at all levels, primarily directed towards equipment and materials sectors, aiming to establish a complete industrial chain. In key infrastructure areas (such as power grids, communications, and government affairs), the procurement priority for domestic chips has significantly increased, providing local companies with a solid revenue base and new orders.

As the core position of domestic semiconductor industrialization, Hong Kong-listed entities cover key links such as semiconductor wafer foundries, advanced packaging and testing equipment, AI computing chips design, and specialized chips, representing benchmark enterprises for domestic substitution: Huahong Semiconductor$HUA HONG GRACE (01347.HK)$is the domestic leader in memory chip foundry services, focusing on expanding production in mature process technologies, while SMIC$SMIC (00981.HK)$ Achieving mass production of 5nm-class N+3 process, ASMPT $ASMPT (00522.HK)$ is a core supplier of global advanced packaging and testing equipment, forming a complete domestic industrial chain from chip manufacturing to equipment support.

Figure: Procurement support policies promote the demand for domestic substitution.

Data as of October 2025

2) South Korea: Core beneficiary of AI memory dividends, with monopolistic leadership in its field.

SK Hynix is a core player in the global AI memory sector. In the HBM (High Bandwidth Memory) domain, it has established a dual monopoly in technology and market: holding a 62% share of the HBM shipment volume in 2025 and accounting for 57% of revenue. It is one of the few global suppliers capable of consistently delivering HBM3E and the next-generation HBM4, fully benefiting from the explosive demand for AI computing memory.

Figure: Global HBM Market Share.

Data Source: CICC Research,Visible Alpha, February 2026.

Data source: Huatai Securities Research, Visible Alpha, February 2026

3) Japan: Invisible champions in equipment and materials, with technological barriers difficult to overcome.

Japan controls the core supply of high-end semiconductor equipment and materials globally, with Tokyo Electron$Tokyo Electron Device (2760.JP)$As a leader in front-end equipment (etching, thin-film), it consistently ranks among the top in global market share. Its market share for photoresist coating and developing equipment reaches as high as 92%, leveraging high technological barriers to become a 'critical link' in the global semiconductor industry chain.

Figure: Tokyo Electron Equipment Revenue and Global Market Share Situation (FY25)

Data source: Tokyo Electron official website, financial reports; Huatai Research Institute, February 2026

4) Taiwan, China: The core gateway for global advanced process technology, an absolute leader in wafer foundry and packaging testing

Taiwan, China is the core gateway for global advanced process technology, with Taiwan Semiconductor$Taiwan Semiconductor (TSM.US)$being the absolute leader in the wafer foundry field. NVIDIA$NVIDIA (NVDA.US)$ , AMD $Advanced Micro Devices (AMD.US)$, Google, and other global tech giants’ AI chips are all manufactured by Taiwan Semiconductor. Its industrial position is unshakable. Taiwan Semiconductor’s 3nm production capacity is booked until 2027, with 2nm process technology entering mass production by the end of 2025, leading Samsung and Intel by at least three years.$Intel (INTC.US)$From 2026 to 2029, it plans consecutive annual price increases, demonstrating strong cost-pass-through capabilities. Coupled with the world's largest cluster of EUV lithography machines, it forms a virtuous cycle of 'R&D - Mass Production - Customer Feedback,' ensuring strong customer stickiness.

2. The demand side will be the core catalyst for Asia's semiconductor industry in the future.

1) Explosive demand for AI computing power

From 2022 to 2024, the market's confidence in the development of the global artificial intelligence industry mainly came from the investment of cloud computing companies in AI. Their annual investments at the hundreds of billions level supported the development of the AI industry chain, making upstream AI chip manufacturers who received direct orders the biggest beneficiaries. However, since 2025, as the performance of AI models has gradually improved, downstream application scenarios for AI models have emerged, driving extensive downstream applications and completing the last piece of the positive cycle puzzle for the AI industry. The positive cycle brought by this commercial closed loop has become a new source of confidence for the AI industry.

Against this backdrop, both overseas and Chinese artificial intelligence industries are currently in a user expansion phase. Based on the monthly active users (MAU) of various AI apps in Q4 2025, Chinese AI apps have generally maintained a quarter-on-quarter user expansion, with DouBao and YuanBao showing particularly noticeable growth. Undoubtedly, the continuous growth of users implies an ongoing increase in demand for AI computing power.

The daily average token usage of leading domestic large-scale AI models has seen significant growth since 2025, primarily due to increases in the number of basic users and model capabilities. As AI functionalities evolve from chatbots to multi-modal tasks such as image/video/voice generation, the computational power required per task is expected to continue rising.

Figure: Daily average token usage of DouBao's large model (trillions)

Data source: Volcano Engine, December 2025

Globally, the trend of increasing demand for AI-generated content is similar: Looking at the token consumption of Google’s AI large models and their applications, there has been rapid quarter-on-quarter growth since 2025. Google's token processing volume reached 1,300 trillion in September, up from 980 trillion in July 2025, reflecting that we are currently at an inflection point where global AI application terminal demand is rapidly increasing, leading to a surge in demand for computing power and semiconductors.

Figure: Monthly token processing volume of Google’s AI large model and applications (trillions)

Data source: interconnects.ai, company earnings call, September 2025

2) High growth in cloud vendors' capital expenditures benefits upstream semiconductors

The current funding source for the AI industry is mainly the capital expenditure of cloud vendors. Since the advent of ChatGPT, tech giants have significantly increased their capital expenditures to build AI hardware. Year-over-year growth in capital expenditure has remained high at 60%-70% since 2025, instilling confidence in industrial investment and development, while also driving demand growth in the upstream semiconductor industry.

According to CICC forecasts and earnings calls of various tech giants, these substantial capital expenditures are expected to continue flowing into the upstream semiconductor sector, with the Asian semiconductor industry cluster set to benefit continuously.

Figure: FY2026 Global Key Cloud Vendors Capital Expenditure and Investment Expectations

Data source: Bloomberg, Nomura, CICC, company websites and earnings calls; data as of February 2026

Looking back, every technological revolution has relied on the underlying support of semiconductors. Looking ahead, the booming AI industry will continue to drive sustained growth in semiconductor demand. Leveraging complementary advantages across China, Japan, South Korea, and Taiwan, the Asian semiconductor industry cluster has formed the world's most complete semiconductor ecosystem, occupying irreplaceable strategic positions in core areas such as AI computing chips, advanced processes, memory, equipment, and materials.

The Solactive Asia Semiconductor Select Index precisely gathers regional industry leaders, covering core segments like wafer foundry, memory, equipment, and packaging and testing, demonstrating strong long-term performance elasticity.

E Fund (Hong Kong) Solactive Asia Semiconductor Select Index ETF (3486) $EFund A SEMICON ETF (03486.HK)$Tracks the Solactive Asia Semiconductor Select Index, focusing precisely on the 'golden semiconductor supply chain' comprising 'Japan in materials and equipment, South Korea in memory, Taiwan in contract manufacturing and advanced packaging, and mainland China in packaging, testing, and manufacturing.' The index includes 30 leading companies from China, Japan, South Korea, and Taiwan such as Taiwan Semiconductor, SK Hynix, SMIC, and Tokyo Electron. The top ten weighted stocks are highly concentrated, comprehensively covering core sectors such as AI computing chips, high-bandwidth memory (HBM), advanced processes, and equipment. Against the backdrop of explosive demand for AI computing power and significant increases in capital spending by global tech giants, this ETF provides investors with a core tool to seize high-growth opportunities in Asia's semiconductor supply chain.

This content is issued by E Fund Management (Hong Kong) Co., Ltd. This content does not constitute an invitation or recommendation to invest in fund units. Investment involves risks, and fund prices can rise or fall. Before investing, investors should carefully read the fund prospectus (including the "Risk Factors" section) for information on investment risks related to the fund. This content has not been reviewed by the SFC. For detailed important notices and disclaimers regarding the above fund, please visit E Fund Management (Hong Kong) Co., Ltd.

E Fund (Hong Kong) Solactive Asia Semiconductor Select Index ETF(3486):https://www.efunds.com.hk/tc/products/53/important/

$ASMPT (00522.HK)$$INNOSCIENCE (02577.HK)$$SHANGHAI FUDAN (01385.HK)$$GIGADEVICE (03986.HK)$$INNOSCIENCE (02577.HK)$$Tokyo Electron (8035.JP)$$Advantest (6857.JP)$$SENSETIME-W (00020.HK)$ $ZTE (00763.HK)$$XIAOMI-W (01810.HK)$$LENOVO GROUP (00992.HK)$$BLACK SESAME (02533.HK)$$MONTAGE TECH (06809.HK)$$ASE Technology (ASX.US)$

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (4)

to post a comment

7

21