Dividend Income Cheat Sheet: June Dividend Season Is Here—Earn Up to HK$1,596 Per Lot!

Le Comfy (2698.HK) continues to benefit from the demographic dividend in emerging markets, with annual net profit surging 27%. Three growth drivers reinforce its leadership value.

Currently, the global disposable hygiene products industry shows a clear divergence. Growth in mature markets like Europe and the US is gradually slowing, while emerging markets centered around Africa and Latin America have become a stable and continuously growing blue ocean in the global hygiene products sector, driven by ongoing demographic dividends, rising public hygiene awareness, and steadily improving consumer spending power.

For example, data from Frost & Sullivan shows that the African absorbent hygiene products market reached $3.8 billion in 2024, and is expected to maintain a compound annual growth rate of 7.9% from 2025 to 2029. However, the penetration rates for infant diapers and sanitary napkins in this region are only 20% and 30%, respectively, far below the average of over 80% in mature markets such as Europe and America, leaving ample room for growth.

On March 20, Lekeshi, the first Hong Kong-listed stock in the African consumer goods manufacturing sector, released its first full-year earnings report since going public. The company achieved comprehensive growth in both financial data and business results, providing a key reference for understanding investment logic in emerging consumer sectors.

Core performance indicators accelerated further, demonstrating hard-core quality through multi-dimensional improvements.

Looking directly at the financial data, Lekeshi achieved comprehensive optimization in revenue, profit, profitability, and financial structure in 2025.

More importantly, the growth rate of its core performance indicators accelerated further compared to the same period in 2024, completely dispelling market doubts about sluggish growth among emerging market enterprises, showcasing the steady operating capabilities and explosive earning potential of a leading company.

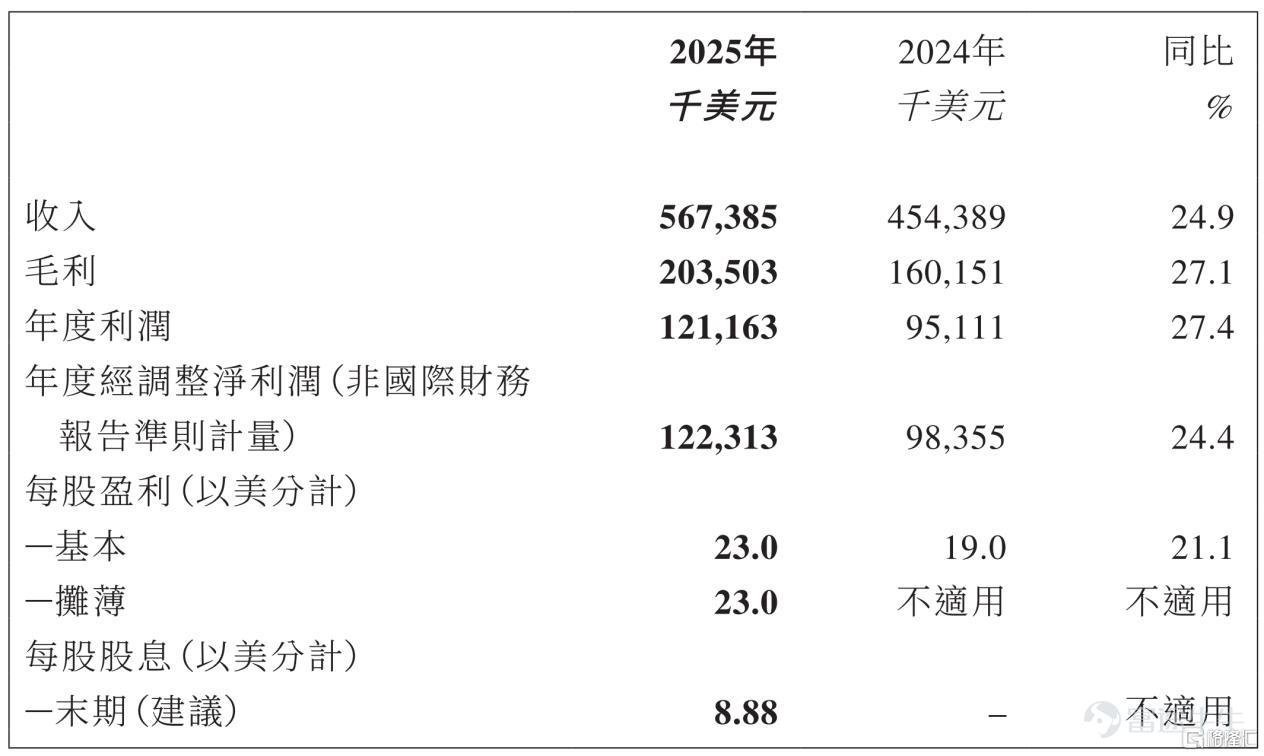

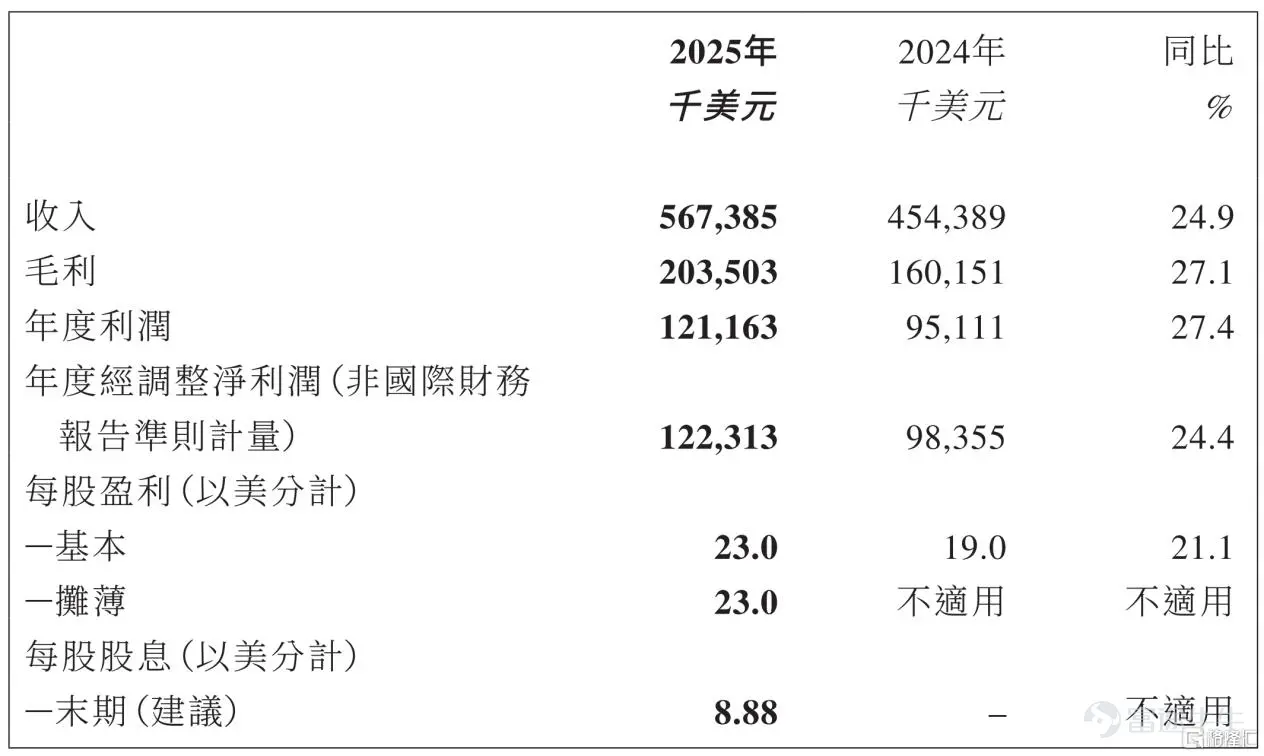

The financial report shows that the company achieved annual revenue of $567 million, representing a year-over-year increase of 24.9%. Despite the continuously rising base in emerging markets, it maintained a steady pace of revenue expansion, solidifying its economies of scale.

In terms of profitability, Lekeshi reported gross profits of $204 million, a year-over-year increase of 27.1%; annual profits reached $121 million, growing by 27.4% year-over-year, achieving dual growth in scale and efficiency. Basic earnings per share were 23 cents, an increase of 21.1% year-over-year, with shareholder return capacity consistently being realized. The company announced a final dividend of 8.88 cents per share for the fiscal year ending December 31, 2025, totaling approximately $55 million.

Compared to the revenue and profit growth rates for the first four months of 2025 (revenue growth of 16%, profit growth of 12%), Lekeshi's full-year revenue and profit growth rates significantly improved, with strong momentum continuing to build.

In addition, Lekeshi made substantial improvements in its financial health in 2025.

According to the company’s earnings announcement, supported by the continuous optimization of its capital structure post-IPO, its current ratio increased from 1.6 in 2024 to 5.7 in 2025, enhancing short-term debt liquidity. Meanwhile, its debt-to-equity ratio dropped from 44.9% to 16.4% during the same period, making its financial leverage more stable and greatly improving its risk resistance.

A three-dimensional growth logic loop, anchoring long-term growth certainty

At its core, the acceleration of LeShuShi's performance growth can be attributed to three growth logics.

First, deep cultivation of core products in existing markets, with channel digitalization enabling scaled replication.

Focusing on the traditional African core market, LeShuShi leverages the demographic dividend continuously released by emerging markets. Through refined and digital transformation of channels, it achieves scaled replication of core products.

Due to the dispersed geography of the African market and the complex hierarchy of traditional channels, the industry has long faced challenges such as insufficient terminal coverage and low distribution efficiency.

In 2025, LeShuShi will fully advance its channel digitalization transformation strategy, focusing on pilot operations in key markets such as Ghana and Kenya to completely reconstruct the original distribution system. This extends from previously covering only upper-level distributors and wholesalers to deeply penetrating downward, achieving direct control and refined operation of terminal stores, and bridging the last mile from brand to terminal.

Following the channel digitalization transformation, the number of terminal stores managed by distributors has significantly increased, and channel distribution efficiency, product rollout speed, and market responsiveness have all achieved qualitative leaps.

Going forward, the company will further expand the geographical reach of its channel digitalization transformation, broaden the coverage of terminal stores, and leverage upgraded channel capabilities to enhance multi-brand and multi-category channel penetration, continuously amplifying the growth potential of existing markets.

Second, accelerate the development of new regional markets, targeting Latin America to create a second growth curve.

While consolidating its base in Africa, LeShuShi simultaneously adopts a new regional expansion strategy to create a second growth curve, with a focus on breaking into emerging markets such as Latin America to achieve diversified regional optimization.

Using the Peruvian market as a core breakthrough, the company is actively promoting the diversification and upgrading of its channel structure, with a focus on expanding the presence in modern channels such as supermarkets and pharmacies to quickly address gaps in its distribution network.

According to the earnings announcement, in 2025, the company's channel coverage density and quality in the Peruvian market increased simultaneously, directly driving local sales up by 85.8% year-over-year to $17.279 million.

In terms of overall regional contributions, revenue from the Latin American market surged from 0.1% in 2022 to 3.9% in 2025. In addition to maintaining steady growth in its 'core' African market, the company has been accelerating its expansion into the 'growth' Latin American market, nurturing new growth trajectories.

Thirdly, transitioning from cost-performance expansion to brand fortification, the company’s marketing system upgrade aims to build long-term competitive advantages.

If the first two growth curves focused on external expansion through market size and regional positioning, the third growth curve represents an internal push by Leshushi to build core barriers.

Currently, supported by its mature production, supply, and sales systems, the company is officially transitioning from early cost-performance-driven scale expansion to high-quality, sustainable growth driven by brand moats.

Through multi-dimensional efforts including digital marketing and a multi-brand portfolio, Leshushi continues to build brand equity and user loyalty, breaking free from industry challenges that rely solely on price competition, enabling both brand strength and financial performance to mutually reinforce each other.

This strategic shift from 'cost-performance scaling' to 'brand building' has closed the loop on Leshushi’s three growth curves. Early growth was driven by cost-performance and channel expansion, while later phases rely on brand barriers to defend market share and enhance profitability for long-term sustainable growth.

Conclusion

From an investment perspective, Leshushi's growth value has already received positive evaluations from professional brokerage firms, who believe its current valuation offers strong investment potential.

For instance, Huatai Securities initiated coverage with a 'Buy' rating, setting a target price of HKD 42, which is 40% higher than the closing price of HKD 29.80 on March 21. The rationale is based on the company’s long-term growth certainty. Huatai Securities believes that, considering the developmental tailwinds enjoyed by emerging markets where Leshushi operates — such as high population growth rates and significant penetration potential — the company, as the leading hygiene product provider in Africa, will benefit from established advantages in capacity deployment and channel development. Therefore, it deserves a target PE ratio of 26x, above the industry average of 19x, corresponding to net profit growth below 20% for both 2025 and 2026.

Currently, as the company's performance continues to grow throughout the year, Leshushi still has significant room for valuation recovery.

In addition to the recovery logic at the valuation level, the continuous realization of positive developments in Leshushi’s capital market is also expected to further boost the value reevaluation process.

In March this year, the company was officially included in the Shanghai-Hong Kong Stock Connect, which will effectively enhance stock liquidity and market attention, attract more mid-to-long-term value-oriented institutional funds for investment, continuously optimize the shareholder structure, and inject new momentum into valuation growth.

It is not difficult to predict that after the release of significantly accelerated revenue and profit growth figures for 2025, Leshushi, with its clear and sustainable growth logic, combined with a low valuation and the dual support of the Shanghai-Hong Kong Stock Connect, is entering a critical window period for accelerating value release.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

1