Aiming to be the 'NVIDIA alternative', is Horizonrobot in trouble?

(The author of this article is Dolphin Research, published by Titanium Media with authorization)

By Dolphin Research

HorizonrobotReleased its second-half 2025 earnings report after the Hong Kong stock market closed on March 19, 2026, Beijing time. The performance of this earnings report fell short of expectations, specifically:

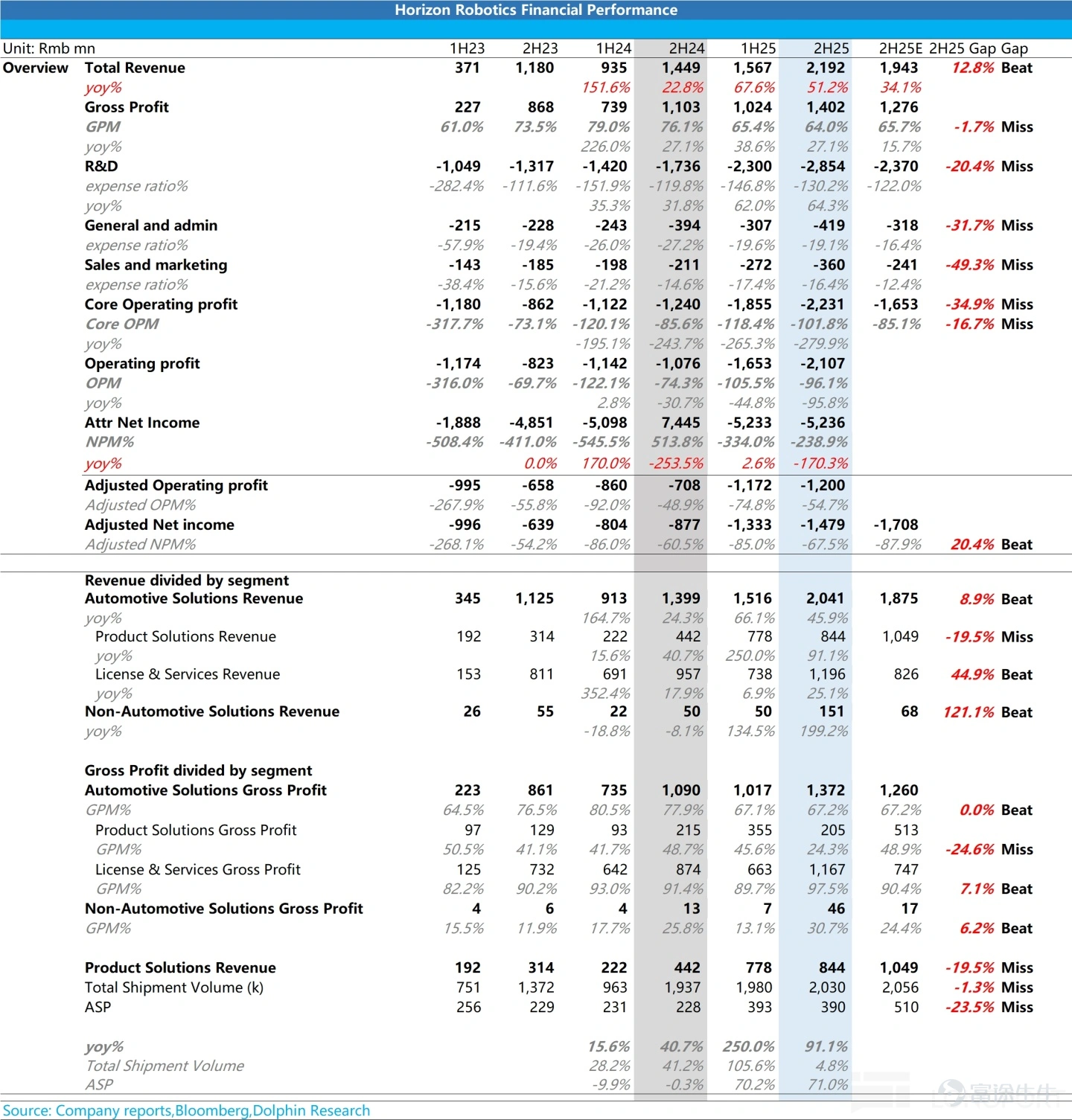

1) Revenue exceeded expectations, but core chip business revenue was below expectations:Horizonrobot's total revenue in the second half of 2025 was 2.19 billion yuan, with a year-over-year growth rate of 51.2%, surpassing the market expectation of 1.94 billion yuan.

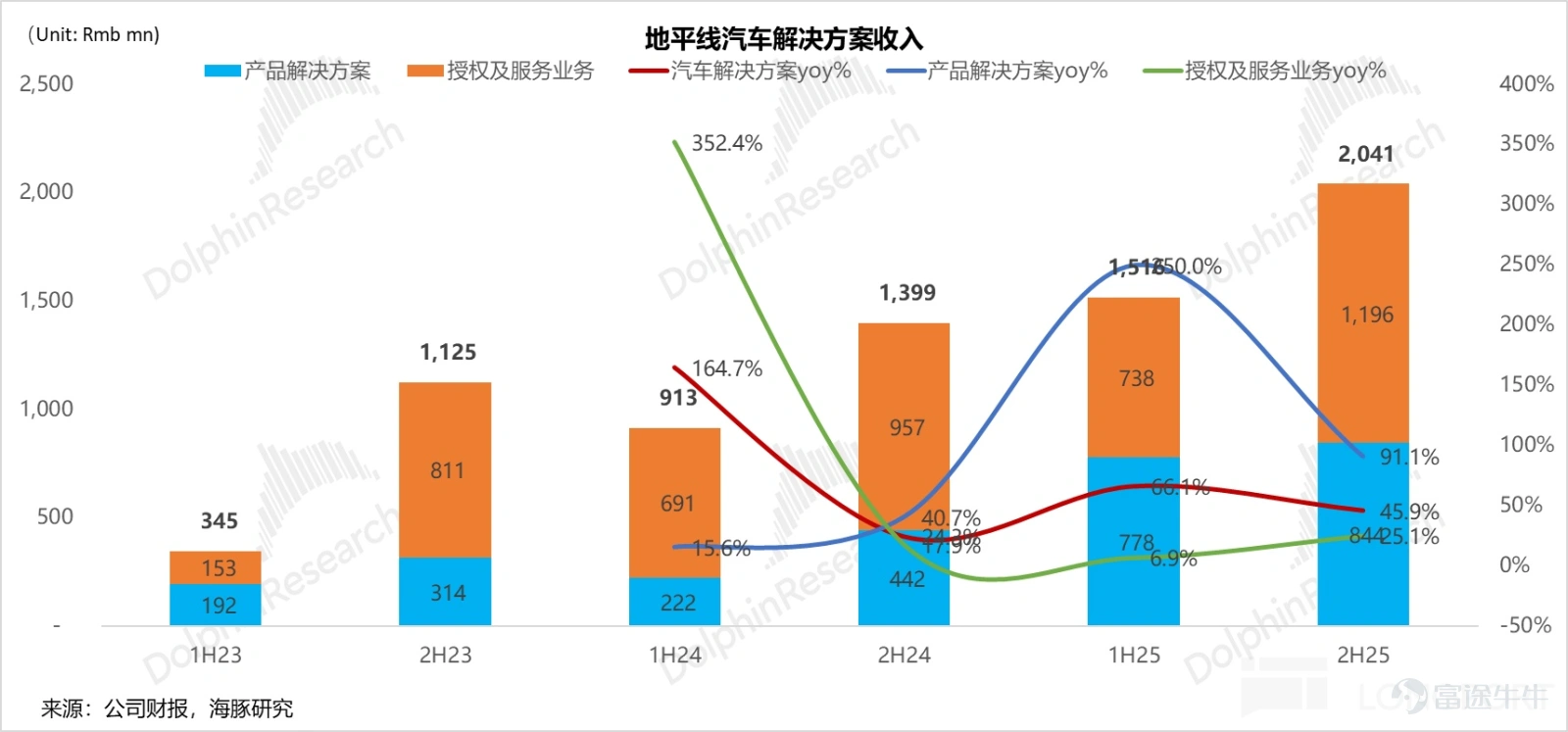

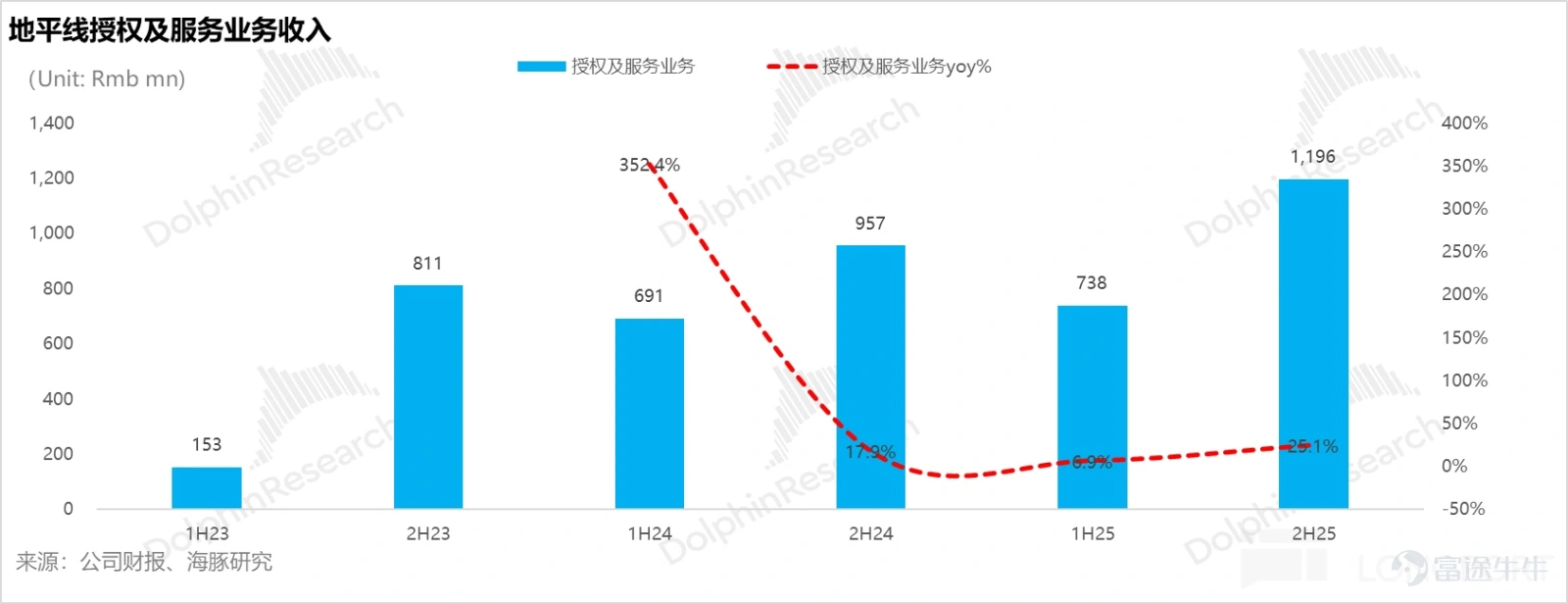

However, the core driver of this outperformance was not chip hardware, but licensing and service business (achieving 1.17 billion yuan in the second half of 2025 vs. an expectation of 750 million yuan). In addition to contributions from its existing major client CoreTech (a joint venture with Volkswagen), the company added a top-tier global Tier 1 Japanese client (expected to be Denso), which immediately became one of the top five clients in 2025.

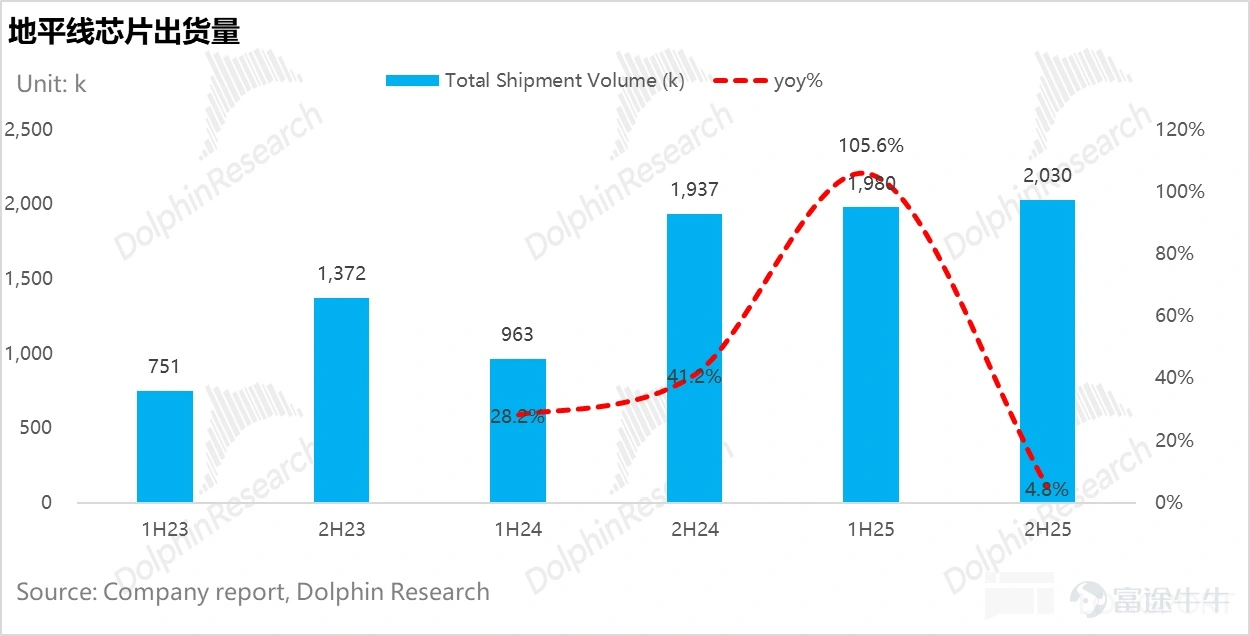

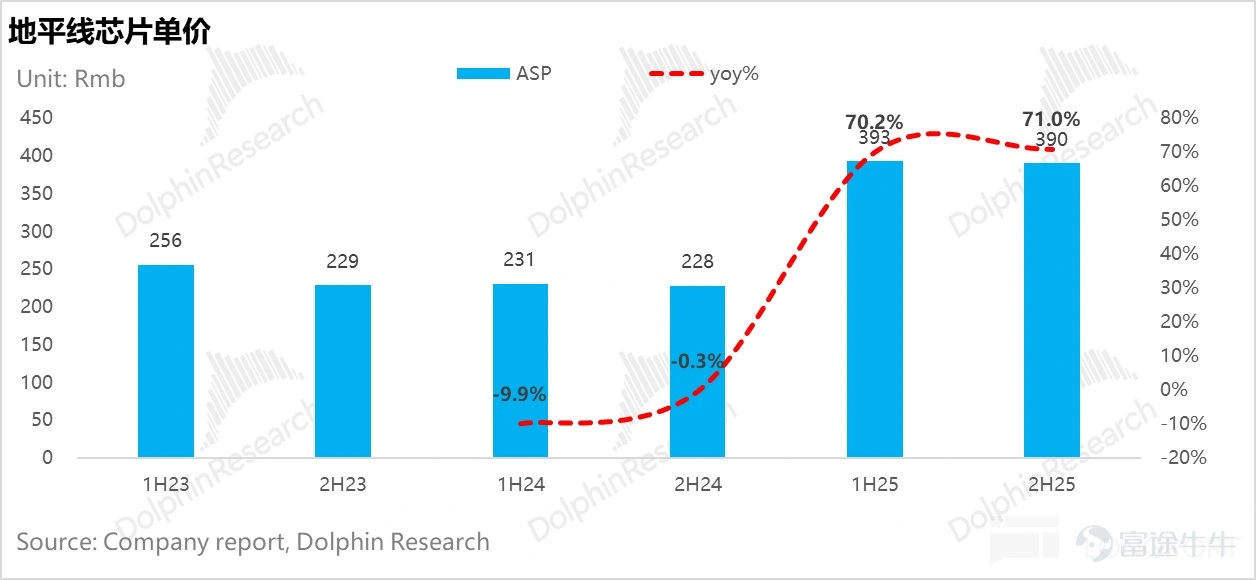

2) The logic of simultaneous increases in volume and price for the core chip business has been hindered, and the pace of premiumization has slowed down:Revenue from the product solutions business (core chip hardware business), which represents future scale and core competitiveness, was only 840 million yuan in the second half of 2025, significantly below market expectations of 1.05 billion yuan. Analyzing volume and price separately, the anticipated logic of 'increased shipments of mid-to-high-end chips leading to ASP improvement' did not materialize:

Slight increase in shipment volume: The shipment volume in the second half of 2025 was 2.03 million units, increasing by only 5% year-over-year, slightly below the expected 2.06 million units.

The average selling price (ASP) stagnated: The chip unit price in the second half of 2025 was approximately 390 yuan, flat compared to the first half of 2025, and significantly lower than the expected 510 yuan.

Dolphin Research believes that there are mainly two reasons for the chip unit price failing to meet expectations:

a. Downgrade in shipment mix: The shipment volume of high-end intelligent driving chips (>80 TOPS) fell from 990,000 units in the first half of 2025 to 830,000 units, with their share dropping from 50% to 40%. This is primarily due to J6P not seeing substantial volume growth, and J6M underperforming at key clients such as BYD, Geely, and Li Auto (for instance, fluctuations in the sales of Li Auto’s L series and electric models not adopting Horizonrobot).

b. Proactive price cuts to boost sales: To respond to competition, the company reduced prices for its existing older chip product lines in the second half of the year.

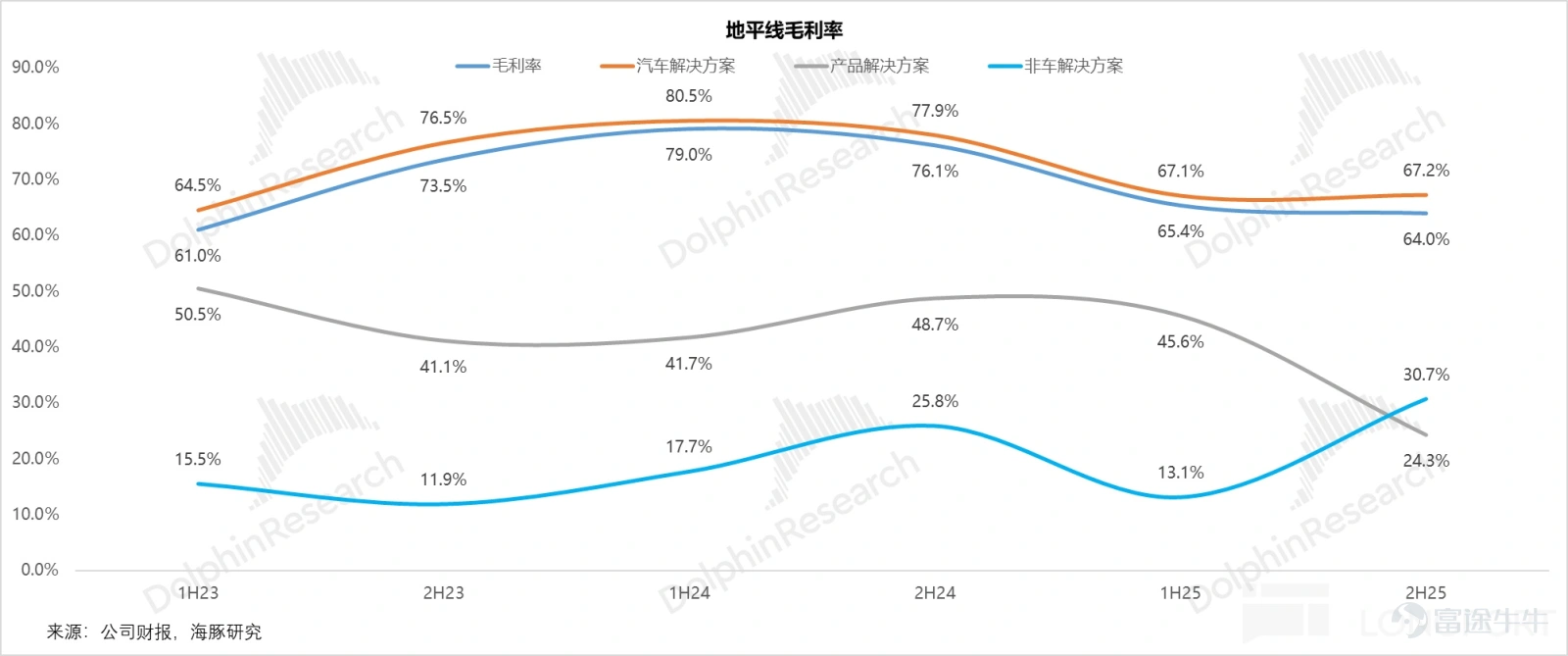

3) Sharp decline in gross margin: Strategic 'system-level delivery' unable to mask competitive pressures:The overall gross margin in the second half of 2025 was 64%, down 1.4 percentage points from the previous half, and lower than the expected 65.7%. Although the proportion of high-margin (97.5%) licensing business increased, the gross margin of the product solutions business plummeted from 45.6% in the first half of 2025 to 24.3%, severely dragging down the overall performance. Dolphin Research believes that the sharp drop in gross margin is mainly due to two factors:

a. "System-level delivery" lowers apparent gross margin: To accelerate the mass production and adoption of high-end HSD, Horizonrobot provided some clients with a "system-level delivery" solution that includes domain controllers and other hardware. For non-self-developed external hardware, only a nominal markup over cost was applied, which can be understood as a strategic investment to trade profit for time or market share.

b. After excluding this impact, pressure from proactive price cuts remains evident: After removing the influence of "system-level delivery," the gross margin of the core autonomous driving chip business still fell by approximately 6 percentage points quarter-over-quarter to 39.6% (with full-year 2025 at 42.5%). Facing sluggish volume growth in mid-to-high-end chips, pricing competition from domestic peers like Black Sesame, and pressure from automakers' self-developed chips, Horizonrobot was forced to adopt a strategy of "trading price for volume," indicating that the competitive environment remains challenging.

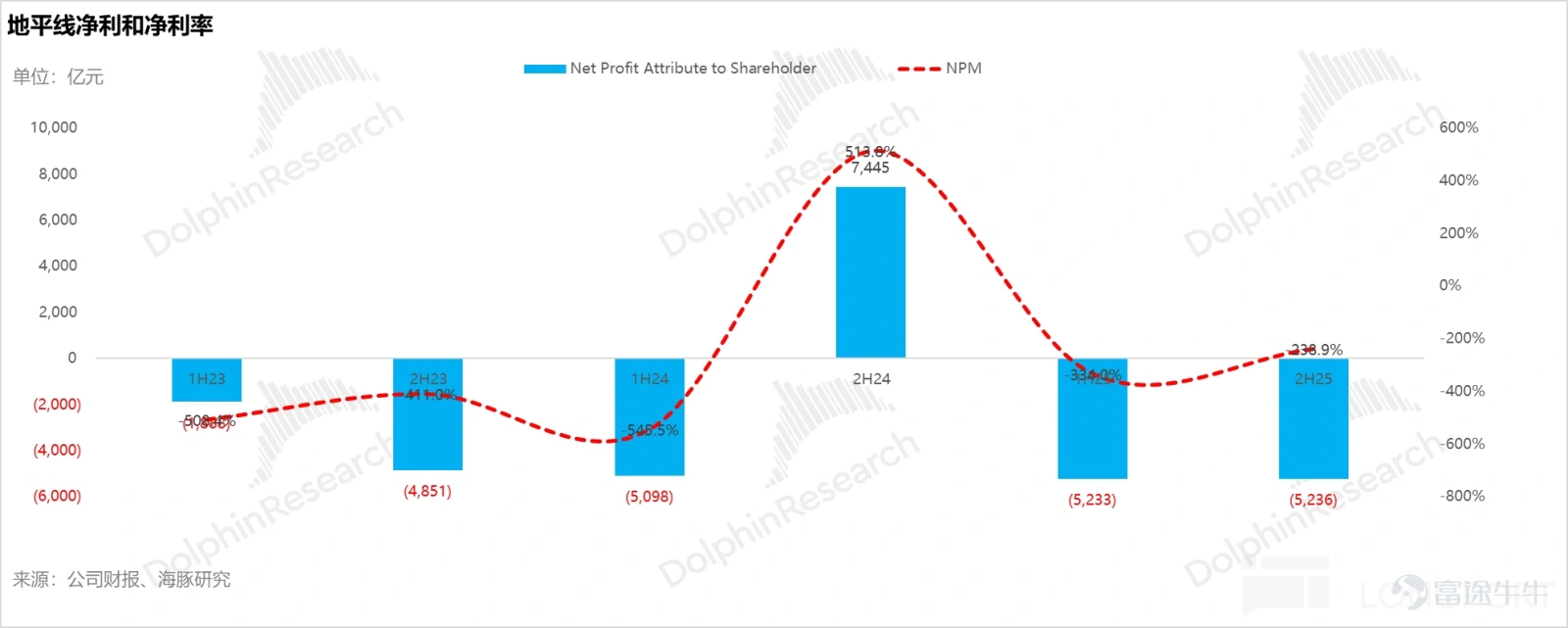

4) Continued high R&D intensity leads to further expansion of operating losses:R&D expenditure in 2H25 reached 2.85 billion yuan (up 550 million yuan quarter-over-quarter, significantly exceeding the expected 2.37 billion yuan), primarily allocated to large model training cloud service fees for HSD and tape-out costs for next-generation high-end chips.

Under the dual pressures of high R&D spending and low gross margins, core operating profit (gross profit minus core three expenses) recorded a loss of 2.2 billion yuan (worse than the anticipated loss of 1.65 billion yuan), while adjusted net profit stood at -1.48 billion yuan (an additional loss of 150 million yuan quarter-over-quarter).

Dolphin's Perspective:

Overall, this is a somewhat "lean" report card.

Behind the seemingly robust revenue growth, there is heavy reliance on licensing businesses whose sustainability is questionable, while the hardware chip business, acting as the cornerstone, is losing momentum.

The market’s most anticipated increase in mid-to-high-end chip volumes, which would drive a "volume and price" growth narrative, did not materialize this quarter. Instead, sales of mid-to-high-end chips declined quarter-over-quarter, compounded by price reductions, leading to stagnation in chip unit prices and slower-than-expected progress in product mix upgrades.

The decline in gross margin, the surge in R&D investment, and the continuously widening losses are all testing the 'patience' of the capital market in the face of its high valuation. Fortunately, the company has ample cash reserves (approximately USD 29 billion), which can buy precious time for breaking through in the premium segment.

The core focus of the market has now completely shifted to 2026, especially regarding the ramp-up pace of J6P (chip computing power at 560 TOPS). This high-end autonomous driving chip, which carries the hope of domestic substitution, will determine whether Horizonrobot 'digests its valuation' or faces a 'valuation cut.' Strong confidence was expressed in the management's guidance for 2026 during the earnings call:

Revenue side: Automotive business revenue growth is expected to accelerate to 60% in 2026 (from 54% in 2025), driven by both volume and price increases.

Shipment volume: It is projected that shipments will grow by approximately 35% to 5.4 million units in 2026 (a slight adjustment from the previous guidance of 5.5 million units). The structure shows a clear trend of 'contraction at the low end, explosive growth in the mid-to-high end':

Low-end ADAS (J6B/J2/J3): Falling below 2 million units.

Mid-tier ADAS (J6E/M): Exceeding 3 million units. Management expects BYD and Geely to each contribute approximately 1 million units in sales, and Horizonrobot will integrate into BYD’s 'Tian Shen Zhi Yan B' autonomous driving system by 2026.

High-end HSD solution: Expected to reach between 300,000 and 400,000 units, with primary demand coming from models such as Chery Fengyun, iCAR, and V27.

b.Average Selling Price (ASP): Implies an extremely high growth threshold

Based on the guidance of '60% increase in automotive revenue, 35% increase in shipments, and flat licensing service revenue,' a reverse calculation showsProduct solutions revenue for 2026 needs to surge 132% year-over-year to 3.76 billion, implying that the core chip unit price also needs to soar 73.4% year-over-year to approximately 694 yuan。

Management attributes this to the increase in the proportion of mid-to-high-end chips (guidance jumps from 45% in 2025 to over 65% in 2026). The core of this jump lies in high computing power (560 TOPS) and high-valueJ6P chip volume expansion(Unit price as high as 500 USD, nearly 10 times the average ASP of 56 USD in 2025)

Management believes that the core reason supporting the continued rapid growth of mid-to-high-end chip sales is that although 2025 is the first year of widespread adoption of autonomous driving, most automakers will only start integrating highway NOA and above functionalities into models in the second half of the year or even Q4, with mass production starting in 2026

The implied HSD structure in the chip unit price guidance is expected to be entirely contributed by the J6P solution

Regarding the HSD solution (expected to ship about 400,000 units in 2026), official定点 progress is proceeding smoothly (already secured 20 mass production定点 agreements), covering the highest-selling automaker in China (BYD). Horizonrobot states it is actively negotiating HSD collaborations with leading automakers, making good progress, and expects HSD定点 numbers to reach record highs in 2026

However, there are three shipping methods for the HSD solution:

J6P Solution: Total ASP of $700 (J6P chip $500 + software $200), targeting models priced around 150,000 yuan.

Dual J6M Solution: Total ASP of $400 (chip $200 + software $200), targeting models priced between 120,000 and 130,000 yuan.

Single J6M Solution: Price under negotiation, targeting models priced around 100,000 yuan.

Management previously indicated that more than half of HSD sales would be contributed by the 'HSD+J6P' solution (mainly Chery's nine models), with the rest contributed by the J6M solution. However, based on the 73.4% high-growth ASP guidance, Dolphin Intelligence calculated that J6P must dominate 'almost all shares' of the HSD solution to accelerate the increase in chip unit price. Of course, this also means significant volume pressure for J6P.

② Gross margin: Guidance remains above 60%.

Facing competition and cost pressures from memory components, management is still confident in maintaining a gross margin above 60% under an average revenue growth rate of 60% over the next few years, mainly due to:

a. Returning to a high-margin business model: Domain controller delivery is only a transitional phase during the early stages of HSD mass production. By 2026, hardware will be handed back to Tier 1 suppliers, refocusing on the core high-margin model of 'SoC + software licensing (nearly 100% gross margin)'.

b. Hedging against supply chain volatility: Memory supply prices have been locked in until the end of 2025, avoiding cost fluctuations. It is expected that memory price volatility this year will not further impact gross margin levels.

c. Replacing 'price wars' with 'architectural innovation': An integrated cockpit-driving solution (combining two into one memory system) will soon be launched, saving several thousand yuan per vehicle in costs (including wiring harnesses, cooling, PCBs, etc.). Technological innovation reduces costs for automakers rather than solely relying on cutting SoC unit prices.

Therefore, Dolphin Intelligence believes that it is undeniable that Horizonrobot remains a rare 'domestic alternative' in the intelligent driving chip (software + hardware) track. With J6P, Dolphin Intelligence sees hope for it to become a true 'NVIDIA alternative'.

However, the current stock price implies relatively high expectations: even based on the management's aggressive revenue guidance (Dolphin calculates total revenue to approach RMB 5.9 billion by 2026), Horizonrobot's forward P/S ratio for 2026 remains close to 16x.

This valuation level is close to domestic AI chip companies in a high-growth phase with strong certainty (around 10-20x, with a midpoint of 15x), but higher than NVIDIA, which has extremely stable profitability (13-14x). However, Horizonrobot's current growth certainty and competitive barriers do not demonstrate a significant premium advantage.

Moreover, in the 'cost-performance range' for high-end intelligent driving chips, Horizonrobot will face fierce competition from Momenta's self-developed chips and algorithm solutions starting in the second half of 2026.

Thus, before the substantial emergence of the 'embodied intelligence/robotics' second growth curve and tangible large-scale financial reflection of J6P in earnings reports, the upside potential for excess returns remains limited.

Earnings report-related charts:

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

1

2