Focus on GTC 2026! What signals did Jensen Huang's speech send?

Targeting the foundational cornerstone of AI industry trends! The E Fund Asia Semiconductor ETF opens for subscription on March 20th.

From the PC Internet to the mobile Internet, and now to the era of artificial intelligence, semiconductors have been the cornerstone of every industrial revolution. Currently, the penetration rate of artificial intelligence is still at the eve of an explosion, comparable to the Internet around 1987 or the mobile Internet around 2008, indicating vast potential.

Asia is irreplaceable in the global industrial chain, producing over 75% of the world's chips, forming a 'golden combination' of 'Japanese materials and equipment + Korean memory + ** foundry + Chinese mainland packaging, testing, and mature process'., holding an irreplaceable position in the global industrial chain, will fully benefit from this round of AI computing power demand explosion.

Therefore, E Fund Hong Kong accurately grasps the industry trend and launches $EFund A SEMICON ETF (03486.HK)$ providing investors with a tool to deploy core leading assets of Asian semiconductors with one click.E Fund Asia Semiconductor ETF starts subscription from March 20 to 24, and officially lists on March 26.

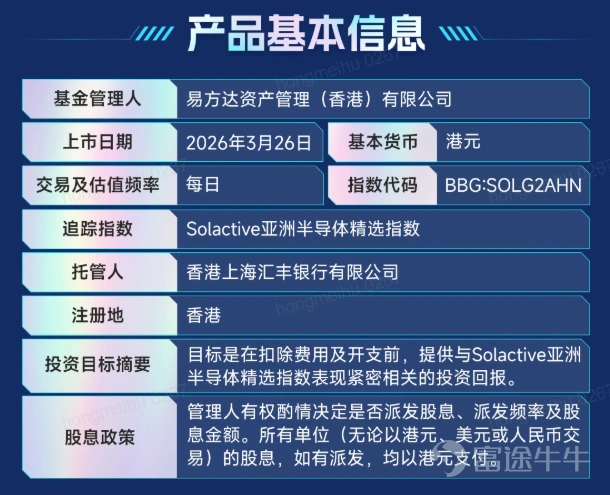

1. Basic product information

II. Investment Highlights

2.1 Cross-regional full industry chain layout, diversifying single-market risks

E Fund Asia Semiconductor ETF closely tracks the Asian Semiconductor Index, aiming to replicate the index performance as its investment objective, precisely covering leading enterprises across the entire Asian semiconductor industry chain.

The index adopts a cross-regional layout, which can effectively diversify the risk of a single market. The constituent stocks include 15 Hong Kong stocks, accounting for 48.5%; 10 Japanese stocks, accounting for 18%; 2 Korean stocks, accounting for 20%; and 3 US stocks, accounting for 13.5%.

The Asian Semiconductor Index is a typical large-cap style index, primarily composed of leading large-cap stocks with a median market capitalization of 100.5 billion yuan. Companies with market capitalizations below 100 billion yuan account for only 24.33% of the index weight, includingSK Hynix, Huahong Semiconductor, Taiwan Semiconductor, SMIC, Advantest, and other industry-leading enterprises. The top ten weighted stocks account for 76.65% of the index.

2.2 Impressive index performance with strong profitability and growth potential

Since its base date on March 20, 2020, the Asian Semiconductor Index has achieved a cumulative increase of 426%, with an annualized return rate of 29.68%. It has shown excellent short-term volatility, with returns of 72% over the past year and 185% over the past two years.

Compared to similar indices, the Asian Semiconductor Index demonstrates significant excess return advantages, with a cumulative increase of 402% from March 2020 to February 2026, significantly outperforming FactSet's Asian Semiconductor Index at 306%, the China-Korea Semiconductor Index at 237%, and the STAR Market Chip Index at 155%.

This indicates that the index has strong profitability and growth potential over the long term, making it a typical high-volatility, high-elasticity index.

2.3 Long-term positive industry prospects with multiple ongoing benefits

Currently, the global semiconductor industry is in an upward cycle, primarily driven by the surge in demand following the formation of a closed-loop business model in the AI industry.

From 2022 to 2024, the development of the AI industry mainly relied on hundreds of billions of dollars invested by cloud computing companies, with upstream AI chips being the first to benefit. Entering 2025, with improvements in AI model performance and the continuous emergence of downstream application scenarios, the final piece of the AI positive cycle will be completed, forming a positive flywheel between end-user demand, model companies, cloud computing firms, and upstream hardware.

In the AI era, demand for computing power continues to grow. Tech giants have significantly increased their capital expenditures, with Meta, Google, Microsoft, Amazon, Alibaba, Tencent, and others raising their 2026 capital expenditure forecasts, primarily investing in AI computing power, cloud services, and chip sectors, directly driving demand for semiconductor products such as GPUs, HBM, and DRAM.

Meanwhile, as semiconductors are a core strategic fulcrum in the contest between major powers and the peak of technological competition, China's semiconductor self-sufficiency rate has increased from 15% in 2019 to 28% in 2024, leaving vast room for domestic substitution. The National Integrated Circuit Industry Investment Fund will continue to inject capital, with strong policy support.

Against this backdrop, the global semiconductor upturn cycle continues, with memory chip price increases expected throughout 2026, leading to sustained improvement in industry profitability. As a core pillar of the global supply chain, Asian semiconductors will continue to benefit from three key drivers: the AI industry boom, domestic substitution, and an upward industry cycle, offering long-term growth prospects.

III. Risk Warning

Important Notes:

1. The E Fund (Hong Kong) Solactive Asia Semiconductor Select Index ETF ('Sub-fund') is a sub-fund under the E Fund ETF Trust, established as an umbrella unit trust under Hong Kong law. The Sub-fund is classified as a passively managed ETF under Chapter 8.6 of the Securities and Futures Commission’s ('SFC') Code on Unit Trusts and Mutual Funds. Its units are traded on the Hong Kong Stock Exchange ('HKEX') like stocks, aiming to provide investment returns closely tracking the performance of the Solactive Asia Semiconductor Select Index ('Index') before fees and expenses. 2. Investing involves risks. The Sub-fund faces: a) investment risk, b) stock market risk, c) new index risk, d) geographic concentration risk, e) political, economic, and social risks related to Mainland China, f) concentration risk in the semiconductor sector, g) risks associated with small- and mid-cap companies, h) securities lending transaction risk, i) differing trading hours risk, j) passive investment risk, k) trading risk, l) tracking error risk, m) currency risk, n) risks of distributions being paid from capital or effectively from capital, o) reliance on market makers risk, p) termination risk. The value of the Sub-fund can rise and fall, potentially significantly. Investors may incur losses. 3. To the extent permitted by the Code on Unit Trusts and Mutual Funds, the Sub-fund may invest in derivatives for hedging or investment purposes, which could fail or lead to significant losses under adverse conditions. 4. Distributions from the Sub-fund may be paid out of capital. Investors should note that such distributions are equivalent to returning or withdrawing part of their original investment or any capital gains generated, reducing the net asset value of the units immediately. 5. The Sub-fund is traded on the exchange at market prices, which may differ from its net asset value. The offering documents for the Sub-fund can be accessed here: https://www.efunds.com.hk/products/. 6. The Index is a new index with a very short operating history, making it impossible for investors to assess past performance. There is no guarantee regarding the Index’s performance. Compared to ETFs tracking indices with longer histories and larger scale, the Sub-fund may involve higher risks. 7. Given the Sub-fund’s focus on securities of companies primarily involved in the semiconductor sector in Hong Kong and East Asia, it may be particularly affected by certain specific factors, thus exposing it to industry and geographic concentration risks. Consequently, its net asset value may experience greater volatility than more diversified funds. 8. Unless the intermediary selling the Sub-fund to you has confirmed its suitability based on your financial situation, investment experience, and goals, you should not invest in the Sub-fund. 9. Investors should not make investment decisions based solely on this document. Before making any investment decision, investors should carefully read the Sub-fund’s offering documents (including risk factors).

Index Provider Disclaimer

Solactive AG ('Solactive') is the licensor of the Solactive Asia Semiconductor Select Index ('Index'). Solactive does not in any way maintain, endorse, promote, or sell financial instruments based on the Index, and Solactive makes no express or implied representations, warranties, or guarantees regarding: (a) the suitability of investing in such financial instruments; (b) the quality, accuracy, and/or completeness of the Index; and/or (c) the results obtained or to be obtained by any individual or entity using the Index. Solactive does not guarantee the accuracy and/or completeness of the Index and assumes no liability for any errors or omissions related to it. Despite obligations to its licensees, Solactive reserves the right to change the calculation or publication methodology of the Index and assumes no responsibility for incorrect calculations or any inaccurate, delayed, or interrupted releases. Solactive shall not be liable for any damages, including but not limited to lost profits or business, or any special, incidental, punitive, indirect, or consequential damages arising from the use (or inability to use) the Index.

E Fund Hong Kong Disclaimer

1. E Fund Asset Management (Hong Kong) Limited is the issuer of this document. This document is neither an offer nor an invitation to purchase fund units. Applications for fund units must be made using the application form provided in the accompanying fund prospectus. Investing involves risks. The value of the fund can go up or down. Past performance is not indicative of future results. Investors should carefully read the fund prospectus (including risk factors) before investing to understand the risks associated with the fund investment.

2. This document may be subject to distribution restrictions in certain jurisdictions. This document does not constitute the distribution of any information or an offer or invitation in any jurisdiction where such distribution, offer, or invitation would be unlawful. This document has not been reviewed by the Hong Kong Securities and Futures Commission.

3. SFC recognition does not constitute a recommendation or endorsement of the scheme, nor does it guarantee its commercial viability or performance. It does not imply that the scheme is suitable for all investors, nor does it represent an endorsement of its suitability for any particular investor or category of investors.

$EFund Biophar ETF (03186.HK)$ $EFUND GOLD MI ETF (02824.HK)$ $E FUND (HK) MSCI Asia Pacific Select High Dividend Index ETF (03483.HK)$ $E Fund (HK) CSI Liquor Index ETF (03189.HK)$ $E Fund (HK) HSI ESG Enhanced Index ETF (03039.HK)$ $E Fund (HK) FTSE AI Select Index ETF (03489.HK)$ $EFUND DIGITAL ETF (03434.HK)$ $E Fund (HK) MSCI China A50 Connect ETF (03111.HK)$

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (6)

to post a comment

7

31