Tongcheng New Materials IPO: Four hurdles in the Hong Kong stock market, why rush for secondary financing after cashing out nearly 1 billion?

IPO Information

Author:Baker Street Detective

When a company listed on the A-share market experiences continuous share reductions by shareholders and executives while initiating an IPO in the Hong Kong stock market, a direct question often arises in the market: Why are shareholders retreating before attempting to list on the Hong Kong Stock Exchange? This is the core controversy sparked by Tongcheng New Materials' recent attempt to enter the Hong Kong market.

On the surface, this is a typical 'A+H capital layout'; but if we look at the combination of industrial transformation, shareholder reduction, and the capital market window period, it becomes clear that this is more like a capital game where industrial expansion and capital realization are happening simultaneously.

01 The Eager New Materials 'Top Performer'

Tongcheng New Materials initially had a simple label: the leader in tire rubber additives, and a leading domestic supplier of specialty rubber additives and electronic chemical materials, with products widely used in tires, new energy vehicles, semiconductor materials, and other fields.

The company's main products are phenolic resins, bonding resins, and other rubber materials, serving clients such as Michelin, Bridgestone, and Goodyear, global tire giants. In the niche track of tire materials, the company has long maintained a leading position domestically.

However, the problem is also evident: tire materials belong to a typical mature industrial track with a clear industry ceiling and limited valuation space. Thus, over the past few years, Tongcheng New Materials began telling a new story — semiconductor materials.

Through investments and acquisitions, Tongcheng New Materials gradually entered the supply chain for photolithography gel support materials, electronic chemicals, and semiconductor materials, hoping to upgrade from a 'tire material company' to an 'advanced materials platform.'

This transformation step is crucial for the capital market because, in terms of valuation logic, the valuation systems for chemical materials companies and semiconductor materials companies are almost two different worlds. According to Tongcheng New Materials' 2025 interim report, most of the company’s ongoing construction projects are related to chip semiconductors.

Perhaps under the background of this industrial narrative upgrade, Tongcheng New Materials became increasingly eager to push forward its Hong Kong stock listing.

From the perspective of the enterprise, this step is not difficult to understand. The electronic chemicals industry has one common characteristic: long R&D cycles, high technical barriers, and massive capital investments. Especially in the field of semiconductor materials, moving from R&D to production capacity building often requires continuous funding.

A Hong Kong listing can bring overseas financing channels, foreign currency funds, and international institutional investors, which serve as very practical capital tools for a materials company looking to enter the global semiconductor supply chain. Additionally, the narrative system in the Hong Kong market differs as well.

In the A-share market, Tongcheng New Materials is more easily seen as a chemical materials company; but in the Hong Kong stock market, it can be redefined as a semiconductor materials platform company. One thing capital markets are best at is using different narratives to assign different valuations to the same company.

Continuous reductions - how large exactly is the funding gap, and where are the proceeds going?

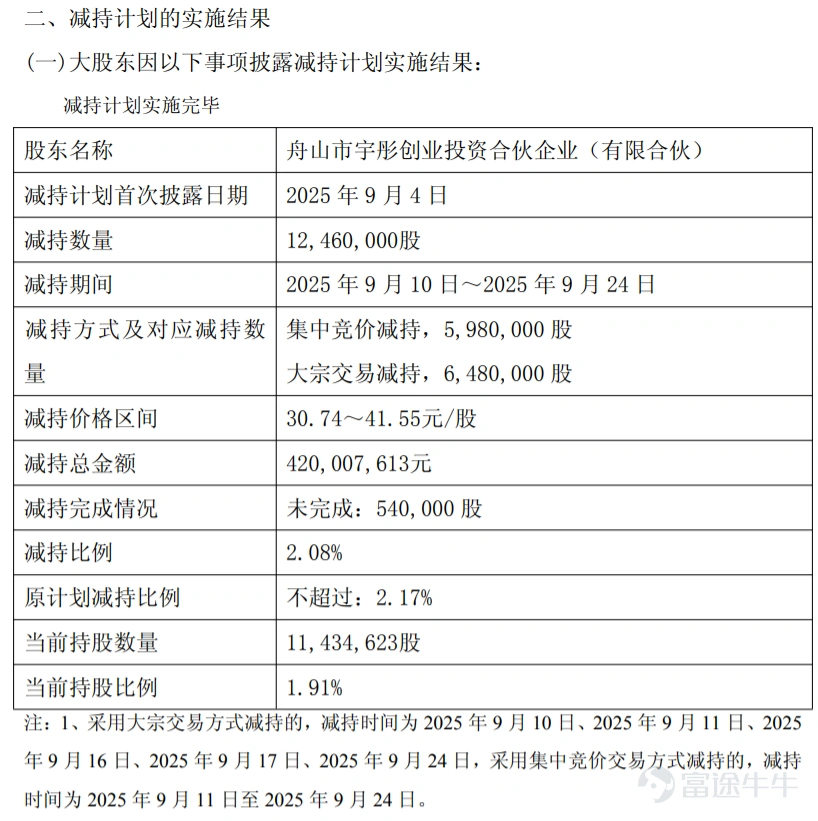

But just as the company was preparing to tell its 'global advanced materials story,' another event also caught the market's attention - shareholders were continuously reducing their holdings. A search on Juchao revealed no fewer than 25 announcements of share reductions by Tongcheng New Materials, with the most notable case being early investor Yu Tong Investment.

Public information shows that Yu Tong Investment held about 10% of Tongcheng New Materials' shares shortly after its IPO, then continued to reduce holdings over the following years through block trades and centralized bidding. From 2021 to 2024, it cumulatively reduced its stake by about 5%; in 2025, it initiated a new reduction plan, selling approximately 3.33%. Based on publicly available data, these reductions have resulted in cash-outs totaling approximately 659 million yuan.

After completing the reductions, its stake has dropped to about 1.91%, including an incomplete reduction of 540,000 shares, almost nearing a complete exit. More subtly, during the process of reduction, this institution was also subject to regulatory warnings due to issues with information disclosure. In other words, early-stage capital is gradually withdrawing.

Meanwhile, related shareholders are also synchronously reducing holdings. Virgin Holdings Limited, a company related to the controlling shareholder’s family, reduced its stake by approximately 1.65% between July 2023 and January 2024, cashing out around 314 million yuan, with the price range per share between 27.74 yuan and 38.40 yuan. If we combine all these transactions, the total amount of capital cashed out is close to 1 billion yuan.

This raises a classic question in the market: if future growth certainty is strong, why are some investors choosing to realize profits at this stage?

Of course, from the perspective of corporate governance, Tongcheng New Materials' control remains very stable. Company Chairman Zhang Ning holds more than 60% of shares through multiple platforms, meaning there will be no change in control, and management remains highly aligned with the company. However, what the capital market really cares about is not 'why the reduction,' but why the reduction is happening during the IPO window period.

Because in the psychological logic of the capital market, if a company’s future growth certainty is extremely high, internal capital tends to prefer long-term holding rather than realizing gains prematurely.

From a broader perspective, Tongcheng New Materials’ Hong Kong IPO actually reflects an increasingly evident trend: A-share companies are upgrading their valuation and financing systems through Hong Kong stocks. When enterprises transition from traditional manufacturing to technological materials, a single capital market often struggles to simultaneously meet financing needs and valuation narratives.

Thus, companies maintain their industrial financing base in the A-share market while seeking international capital and new valuation logic in the Hong Kong stock market. Over the past two years, from new energy to AI, and then to advanced materials, an increasing number of companies are following this 'A+H' path.

The key issue lies in this: a capital narrative can change the valuation logic but cannot alter fundamentals. The real test for Rongcheng New Materials is not the IPO itself, but whether it can complete the transformation from a tire materials company to a semiconductor materials platform. If the semiconductor materials business achieves a real breakthrough, the company’s valuation system may be completely restructured; however, if progress in related businesses falls short of expectations, the capital market will also swiftly adjust its forecasts.

Against the backdrop of simultaneous capital exits and industrial expansion, the future of this company will likely depend on a simple question: Can the new story truly turn into new profits?

03 Who is the new story being told to

The core narrative behind Rongcheng New Materials’ push into the Hong Kong stock market boils down to one sentence: Upgrading from a tire materials company to a semiconductor materials platform. However, what the capital market truly cares about is not the story but the results: Can the new story translate into new profits?

This is because, in the semiconductor materials sector, there is significant room for storytelling, but commercialization is equally challenging. For Rongcheng New Materials, at least four practical hurdles must be overcome.

The first challenge is the technical barrier and certification timeline. Semiconductor materials are not ordinary chemical products; their defining feature is 'extreme stability.' Products such as photoresist support materials, electronic resins, and electronic chemicals must operate stably over long periods in ultra-clean environments, as even the slightest impurity can affect chip yield rates.

Therefore, wafer fabs impose extremely rigorous certifications on material suppliers. The process from sample submission to mass production adoption often takes two to three years or even longer. This means that even if a company already possesses the technical capability, it may not quickly generate revenue. For Rongcheng New Materials, which is accelerating its transformation, there could be a lengthy time gap between technological breakthroughs and commercial implementation.

The second hurdle is the inertia of the global supply chain. The semiconductor materials industry has long been dominated by international giants like JSR, Tokyo Ohka Kogyo, and Shin-Etsu Chemical, which have been deeply entrenched in the photoresist and related materials fields for decades. These companies are not only technologically advanced but, more importantly, have become deeply embedded in the global wafer fab supply chain.

For new entrants, the biggest challenge is not whether they can produce a product but whether they can replace existing suppliers. In the semiconductor industry, once a certain material is running stably, wafer fabs typically do not easily switch suppliers, as doing so would mean re-validating yield and reliability risks. In other words, the market is not entirely open competition but rather a highly locked-in supply chain system.

The third issue is capital consumption and the return cycle. Semiconductor materials are a typical 'slow return industry.' Long-term investment is required for R&D, high-standard equipment is needed for production, and customer certification takes many years, leading to companies often having to invest continuously over a long period without being able to achieve scale profits immediately. For traditional material companies, this model differs significantly from their existing businesses. The rubber additive industry usually has stable orders and mature customer structures, whereas semiconductor materials are more like long-term technological investments. This is also why many companies that venture into semiconductor materials often do not see significant profit contributions in the short term. For Tongcheng New Materials, Hong Kong stock financing can address short-term capital needs but cannot shorten the industrial cycle itself.

The fourth practical challenge is competition within the supply chain. In the semiconductor material system, technological barriers vary greatly across different segments. Photoresist is the segment with the highest barrier, while supporting resins and electronic materials, though equally important, have more competitors and relatively lower entry thresholds.

This means that even if Tongcheng New Materials achieves breakthroughs in certain material segments, it does not necessarily mean they can achieve high-profit margins like photoresist companies. Many semiconductor material companies will ultimately face a reality where their products enter the supply chain but offer limited profit margins.

These issues do not mean that Tongcheng New Materials’ transformation will inevitably fail. On the contrary, the trend towards localization of China's semiconductor materials indeed provides historical opportunities for new entrants. However, opportunities and difficulties often coexist. For the capital market, the key question is actually not 'whether one can enter the semiconductor materials industry,' but whether one can generate real profitability in this sector.

If Tongcheng New Materials can complete customer certifications, expand wafer factory orders, and gradually establish a stable supply chain in the coming years, then today's capital narrative may evolve into genuine profit growth. However, if technology adoption is slow, customer validation cycles are prolonged, or products remain at marginal material stages, then the semiconductor business could remain a 'strategic investment' for quite some time, making it difficult to become a profit pillar.

Considering the aforementioned points, according to Tongcheng New Materials’ 2025 interim report, most of its ongoing projects are semiconductor-related, and uncertainties exist regarding capacity ramp-up. Whether Tongcheng New Materials’ transformation succeeds still requires time to provide an answer.

© THE END

All materials sourced from official public information

This article does not constitute any investment advice.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment