Earnings reports from Chinese giants raise concerns! Is it a good time to buy on dips?

Tencent's earnings report blew up, but AI has never been a good thing for big tech companies

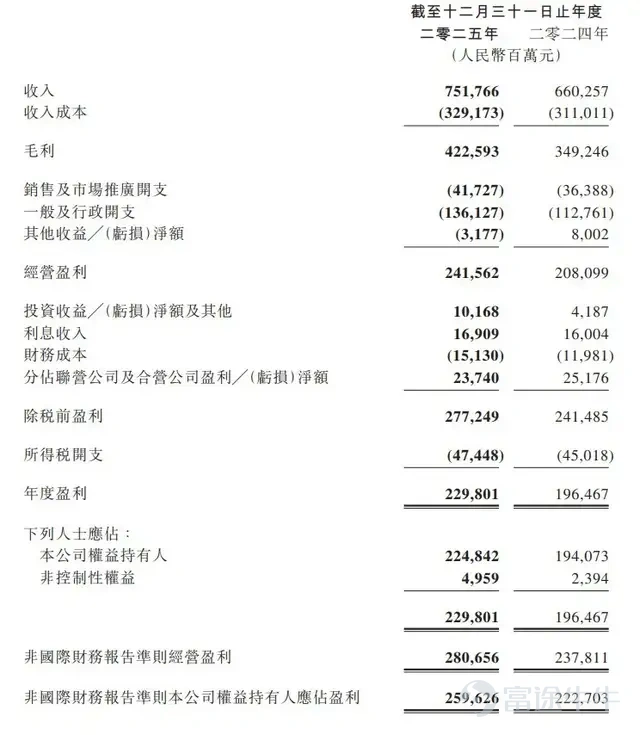

On March 18, Tencent released its Q4 and full-year financial report for 2025.The financial report showed that in Q4 of 2025, Tencent's total revenue was RMB 194.371 billion, a year-on-year increase of 13%; gross profit was RMB 108.289 billion, up 19% year-on-year; operating profit under non-IFRS standards was RMB 69.518 billion, increasing by 17% year-on-year. Revenue and net profit exceeded market expectations.

Tencent’s management stated that the company's core business meets multiple resilience criteria, demonstrating high defensiveness.

On one hand, the performance surpassed expectations, while on the other hand, there is a potential threat from AI. The day before Tencent released its financial report, Tencent Music posted decent earnings but saw its stock price plunge.

Recently, Tencent’s stock price has been hovering at a low level. The rapid development of AI technology is not good news for all major companies.The development of AI has disrupted all stable expectations. Below is the transcript of last night’s earnings call Q&A session.

Q&A

Q: What are the impacts of AI investments on profits and profit margins in 2026, and how will resource prioritization be handled under GPU and AI talent constraints?

A: In 2026, revenue growth may outpace profit growth due to increased investment in new AI products. Management expressed comfort with this outcome, believing that AI products can expand user coverage and create new value, with some products already showing good product-market fit. Regarding AI talent, we have assembled a top-tier global and domestic team for the HunYuan project through competitive compensation, culture, and leadership attraction, stabilizing the team, and selective recruitment will continue. Regarding GPU constraints, computing power is gradually increasing through leasing, purchasing high-end imported GPUs (as supply recovers), and domestic GPUs, with supply expected to accelerate in the second half of 2026. Resource priorities focus on the HunYuan large model and new AI products, with core products able to access computing power from local devices or multiple cloud platforms, ensuring flexibility in sourcing compute resources.

Q: How do you evaluate the ROI of AI investments, the timeline for returns, and the choice between self-building vs. leasing? What are the priorities across different layers of the AI stack?

A: Existing businesses applying AI have already achieved good ROI. Excluding investments in new AI products, operational leverage is evident. New AI products are currently investment-heavy with limited revenue (due to insufficient consumer subscription demand in China and high-cost coding agent requirements on the enterprise side) but are expected to generate revenue and deliver attractive returns over the long term, similar to Tencent Cloud’s path from losses to profitability. For self-building vs. leasing, given a strong balance sheet, purchasing is prioritized to avoid leasing premiums, but leasing will be considered under supply chain and regulatory constraints. Investment is required across all layers of the AI stack (models, orchestration layer, application layer, etc.), and it is difficult to prioritize due to dynamic market conditions. Tencent has the resources and teams to cover all layers, with each layer offering different advantages (e.g., the application layer benefits from products, orchestration capabilities, and ecosystem).

Q: After the launch of Yuanbao and Skill Hub, how does Tencent's positioning and differentiation in various parts (such as models) compare to Android’s open ecosystem in terms of Agent AI?

A: Agent AI is evolving into a decentralized landscape, similar to how the internet transitioned from centralized entry points like browsers/search engines to a multi-application ecosystem. The current AI landscape isn't monopolized by a single AGI but consists of multiple models (specialized in different fields) and open-source models coexisting. In the future, more companies will introduce agents, competing based on unique value propositions. Tencent's advantage lies in its cross-platform capabilities spanning PC, mobile, and cloud, covering both applications and webpages. It owns centralized applications as well as decentralized ecosystems (like mini-programs). Decentralized experiences such as mini-programs can be upgraded with agent capabilities. Regarding models, the HunYuan team continues to improve, becoming better and faster in the future. Usage will increase, but no monopoly will form. Different models occupy various positions on the cost-performance curve, and Tencent aims to be one of them, not the only one.

Q: What is the demand outlook for PC AI (such as the 3B model) in enterprise productivity scenarios, and what are Tencent’s capabilities and competitive advantages?

A: AI will complement and enhance productivity tools like CAD, playing an important role in industrial design, architecture, and gaming (especially 3D graphical assets). Due to its gaming business, Tencent possesses abundant data on 3D graphical assets, giving it a unique advantage in training 3D tool models. However, this area remains a niche market rather than the largest opportunity.

Q: How does AI impact game quality and costs, Tencent’s response, the changing importance of publishing versus development, and whether there will be an increase in game studio supply?

A: AI currently focuses on enhancing existing game content and accelerating content creation but cannot create games from scratch yet. Tencent’s Interactive Entertainment team showcased at GDC how AI is applied to game graphics, gameplay, and user engagement, placing them at the industry forefront. The gaming industry already suffers from oversupply (with 200,000 new mobile games annually and 18,000 on Steam), and while AI lowers barriers to entry, it won’t significantly alter the supply-demand balance. The key remains in creating evergreen games, which require top talent and technology. The value balance between development and publishing remains unchanged, benefiting leading developers. AI benefits the gaming industry as its proliferation increases users' free time and boosts gaming demand. Tool accessibility favors teams with resources and user bases (like Tencent), accelerating content production and iterative innovation, turning games into platforms.

Q: With strong AI compute demand but rising costs for AI servers (DRAM, HBM), what is Tencent Cloud's pricing power and value capture strategy?

A: AI demand drives up requirements across all compute categories, including GPUs, CPUs, RAM, and SSDs. Due to historically low margins among cloud service providers and current supply constraints (requiring months/quarters of pre-ordering, prioritizing hyperscale vendors), the industry has no choice but to raise prices; price hikes have already appeared in China’s cloud market. The value capture strategy involves enhancing value through premium services: Bare metal rentals yield low margins, virtualization offers higher-priced compute tokens, and packaging into PaaS/SaaS provides the best margins. Tencent Cloud has transformed from significant losses four years ago to achieving substantial profitability last year and will continue shifting towards high-value services.

Q: Will Tencent fall behind in the AI field (compute, models, applications) due to a late start?

A: AI is a multi-track competition rather than a single race, with new opportunities continually emerging (e.g., from Chatbots to coding, multimodal, agents). The market is still in its early stages, and more AI forms (models, products, agents) and upgrades to existing services’ agent capabilities will appear. Tencent possesses cross-PC/mobile application layer capabilities (WeChat, Video Accounts) and ecosystems (communication, cloud, payment infrastructure), allowing it to integrate these strengths into AI competition. The key lies in rapid innovation; the HunYuan team restructuring and product team innovations are already underway, so we are not concerned about starting late but focus more on innovation speed.

Q: What is the impact of Apple's reduction in App Store commission rates on Tencent Games' profits, will it be shared with partners, and what are the subsequent trends?

A: The reduction in Apple's commission rate (from 30% to 25%, and from 15% to 12%) directly benefits Tencent, as most game distribution revenue shares are based on gross revenue (before deducting Apple's commission), meaning the incremental profit will flow to Tencent; if corporate income tax is involved, it depends on whether the incremental profit will be reinvested in AI products. More importantly, Apple announced that Chinese developers will enjoy the same low commission rate as global developers, indicating that the App Store commission rate will be reduced globally going forward. This is a positive first step, with further optimizations expected.

Q: What is Tencent's priority regarding AI chips (self-developed)?

A: Currently, self-developed chips are not a core priority: training chip design and manufacturing present significant challenges, requiring access to the most advanced training chips to train optimal models; the inference chip market is highly competitive (many suppliers in China, low gross margins), making costs manageable. Tencent is currently focused on using the best training chips to iterate its models (HunYuan 3.0 will significantly outperform 1.0) while leveraging its product development and connectivity capabilities to build AI products. Future considerations will involve reducing inference costs.

(Note: The author holds Tencent shares. This article is purely for information sharing and does not constitute any investment advice.)

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment