Putailai's IPO: After distributing $2.2 billion in dividends, the company seeks financing in Hong Kong stocks, but what Putailai wants is more than just money

IPO Information

Author:Baker Street Detective

In the capital narrative of the new energy vehicle industry chain,Shanghai Putailai New Energy Technology Co., Ltd.has always been a somewhat unique presence. Now, this slightly special new energy technology company is preparing to make a push for a Hong Kong listing.

It does not attract as much attention as battery manufacturers or directly determine industrial costs like lithium mines, but almost every leading battery company’s supply chain cannot bypass Putailai. From anode materials and separator coatings to PVDF binders and lithium battery equipment, this company has covered nearly all the most crucial segments in the battery materials industry chain.

Precisely because of this, when Putailai began planning its Hong Kong IPO and attempting to build an 'A+H' capital structure, the market’s first concern was not whether the company needed money, but why a new energy materials company that has been profitable for many consecutive years and distributed over 20 billion yuan in dividends still needs additional financing?

01 Dividends of 22 billion, yet still seeking financing

In terms of financial performance, Putailai doesn’t fit the typical profile of a 'financing-driven company.' Since going public, the company has consistently paid dividends, distributing more than 1.1 billion yuan in the past three years, with a dividend payout ratio consistently maintained at around 50%, making it quite generous among new energy material enterprises.

From an industry perspective, Putailai’s performance has been stable. Many companies in the same sector are still in the phase of expanding production and burning cash, whereas Putailai has already established a stable profit structure. Meanwhile, there has been no significant reduction in shares by founders or core executives to cash out, and the equity structure remains relatively stable. Even during periods of substantial volatility in the new energy sector, reports of large-scale internal capital withdrawal from Putailai have been rare.

In other words, this is not a typical 'shareholder exit type IPO.' However, if you shift the focus away from the financial statements and back to the reality of the new energy vehicle industry chain, another question arises: 'In such a volatile industry, where will the funds for the next round of expansion come from behind these stable large dividends?'

Putailai's push for a Hong Kong listing provides an answer to the market. According to the company’s prospectus, Putailai plans to build a new production facility in Malaysia with an annual planned capacity of 50,000 tons of anode materials. This expansion is expected to enhance Putailai’s overseas production layout and improve its ability to serve international clients.

At the same time, a new base film production facility will be built in Sichuan. This expansion is expected to increase Putailai's self-sufficiency rate for base film in its coated separator business and further enhance Putailai's market share in the base film and coating processing industries.

02 The new energy industry is unpredictable

The new energy industry chain has undergone significant changes over the past three years. The most profitable segments have always been upstream resources and battery manufacturing, while material companies are often squeezed in the middle layer of profits. Once battery manufacturers begin large-scale capacity expansions, material companies must expand in tandem; otherwise, they risk losing clients. However, capacity expansion itself is an extremely costly endeavor.

Production lines for anode materials, coating equipment, chemical material plants—every link in the chain requires massive capital investment. Many material companies may appear to have decent profits, but once a new round of capacity cycles begins, their cash reserves are quickly consumed by capital expenditures.

For Putailai, the issue isn't a current lack of funds, but rather that it will likely require even more money in the coming years because there is an often overlooked rule in the new energy materials industry: as soon as downstream battery manufacturers go global, material companies must follow suit.

This is the real background behind Putailai's listing in Hong Kong. In recent years, Chinese battery companies have started expanding production to Europe, Southeast Asia, and North America, and if material suppliers remain solely in China, they will quickly be replaced.

To continue binding core customers, material companies must also expand overseas. Building factories abroad means higher costs, longer return cycles, and more complex capital structures. Raising funds on the A-share market can certainly address some issues, but if a company hopes to engage with international investors and build a global capital platform, the Hong Kong stock market is almost the only option.

Over the past two years, an increasing number of A-share companies have opted for an 'A+H' structure, essentially preparing capital ammunition for global operations. For Putailai, the Hong Kong listing is more like a strategic reserve than a short-term financing move.

From the perspective of the capital markets, such companies are hard to categorize simply. On one hand, unlike many tech companies that rely on storytelling for financing, Putailai’s profitability has already been proven; on the other hand, it is not yet in a stable dividend cycle like traditional manufacturing firms, as the new energy industry chain is still in a phase of rapid expansion.

Companies are paying dividends to shareholders while simultaneously needing to continuously raise funds for capacity expansion. This contradictory structure is a typical characteristic of the new energy materials industry. Capital markets enjoy talking about 'high-growth stories,' but what material companies truly face is another reality: as long as the industry continues to expand, they will perpetually be in an investment cycle.

Of course, the future of Putailai is not without risks. The new energy materials industry has already started to experience significant capacity expansion pressures, with increased price volatility in anode materials and even signs of oversupply in some segments. Once the industry enters a cyclical downturn, profit margins are likely to compress rapidly.

Importantly, within the new energy supply chain, material companies' pricing power is consistently weaker than that of battery manufacturers and vehicle makers. This means that when industry profits begin to shrink, material companies are often the first to be squeezed. The reason why the capital market is paying attention to Putailai's Hong Kong listing is not because the company has operational issues, but because everyone is pondering the same question: Can new energy material companies sustain their current profit levels in the long term?

Taking a longer-term view, Putailai’s Hong Kong IPO actually represents a shift being experienced by a class of Chinese manufacturing companies. Over the past decade, China's new energy industry has relied on domestic capital markets to achieve rapid expansion, but as companies begin to go global, they must enter more complex international capital systems.

The A-share market addresses financing needs during the growth stage, while the Hong Kong market plays a larger role in global financing. From this perspective, Putailai’s Hong Kong listing is not just a routine capital move, but rather preparation for the next phase of global competition for leading new energy materials companies.

For investors, what might really be worth watching is not whether this company needs financing, but a more practical question: When the new energy supply chain enters the next cycle, will material companies still be able to earn as much as they do today?

03 The Unchangeable 80/20 Split: Only a Few Companies Will Make Money

From an industrial structure perspective, the profitability of material companies depends on three variables: demand growth rate, industry capacity, and bargaining power within the supply chain. In recent years, these three factors have tilted in a favorable direction simultaneously, causing material companies' profits to surge quickly, but such a combination may not reoccur in the future.

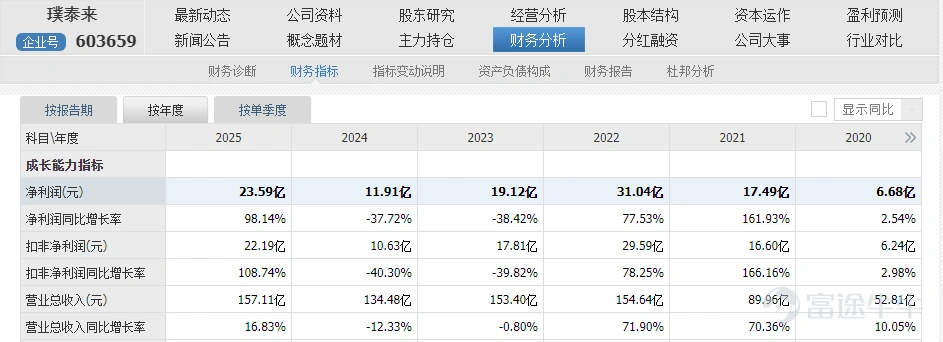

Putailai’s profitability has been significantly affected by industry cycles. Performance declined between 2023-2024, with a rebound in 2025, though it still couldn’t match 2022 levels. The main reason was the noticeable drop in anode material prices, which led to reduced profitability. For instance, in 2023, the company reported net profits of approximately 1.9 billion yuan, a year-on-year decrease of about 38%, primarily due to falling anode material prices and rising inventory pressure.

From an industry perspective, this profit contraction is not a problem unique to Putailai but rather a cyclical feature of the entire lithium battery materials industry. In previous years, explosive demand for new energy vehicles drove aggressive capacity expansions among material companies. But as demand growth slows, prices can fall rapidly. In 2023, anode materials saw a clear price decline, with average selling prices decreasing by approximately 25% year-on-year, and gross margins dropping from nearly 30% to around 15%.

However, what sets Putailai apart from many material companies is that it is not just a single-material enterprise but a platform company encompassing “lithium battery materials + equipment + processes.” Besides anode materials, it also has multiple business segments such as separator coatings, PVDF binders, and lithium battery equipment. Its market share in separator coatings exceeds 40%, placing it among the global leaders. This means that when prices in one segment fall, other segments can still provide profit support.

More importantly, the customer structure includes several of the world's leading battery companies, such as CATL, LG Energy Solution, and Samsung SDI. In the battery industry chain, once a company enters the supply system of a top-tier battery manufacturer, orders tend to have strong stability. If a materials company can maintain long-term partnerships with these clients, its profit fluctuations are typically smaller than the industry average.

Therefore, looking at the medium to long term, Putailai’s profitability may present three potential trends: first, the central level of profit margins will decline; second, concentration among leading players will increase; third, the profit structure will shift from single-material to 'materials + services'.

In addition, Putailai not only sells materials but also equipment, processes, and technical solutions, making its model more akin to an 'industry chain platform.' As battery companies expand globally, such firms often generate additional profits through equipment and engineering services.

Overall, Putailai’s future profitability is likely to follow a typical path for leading new energy materials companies. After the peak boom period for the industry passes, the company’s profits will no longer surge as they did during the height of the market. However, by leveraging scale, technology, and client-binding capabilities, it should still maintain stable earnings.

To put it more bluntly, Putailai may no longer earn the 'windfall profits' seen during the peak of the new energy boom. The market needs to focus on whether Putailai can become the most stable supplier in the lithium battery materials industry after it matures. This will test whether the company can make every major decision without error or quickly rectify mistakes when they occur. No one can predict the answers to these questions, and the final outcome of this HKEX IPO will require time to reveal itself.

Thus, from an industry perspective, new energy materials companies will still be profitable in the future, but it will be difficult for them to universally achieve the 'windfall profits' seen in previous cycles. The industry will shift from 'boom-driven profits' to 'competition-driven profits.' In this environment, differentiation among companies will become increasingly pronounced: leading companies will sustain profitability through technology and scale, while less competitive firms may be eliminated in the next cycle.

In other words, the next phase of the new energy supply chain will no longer be an era where all materials companies make money together, but rather an era where only a few companies can consistently profit.

© THE END

All materials sourced from official public information

This article does not constitute any investment advice.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment