Following the failed launch of the ASTS satellite, where do space-related stocks go from here?

Not just about lobsters or space exploration! Jensen Huang officially set the tone for the "Token Factory" at GTC—what sectors could see investment opportunities?

March 16, 2026$NVIDIA (NVDA.US)$The GTC 2026 conference officially opened, with Jensen Huang delivering the keynote speech.

At this conference, regarded as the 'annual AI industry pilgrimage,' Jensen Huang outlined NVIDIA’s transformation from a 'chip company' into an 'AI infrastructure and factory company.'

1. Trillion-dollar order guidance: Dispelling concerns about 'peaking capital expenditures'

In his keynote speech, Jensen Huang introduced a core concept:‘Token Factory Economics’ – every data center in the future will become a ‘factory’ for producing tokens.He predicts that by the end of 2027,NVIDIA's flagship chips alone will generate at least $1 trillion in revenue,driven by the underlying logic of global enterprises' insatiable demand for token generation capabilities.

Jensen Huang’s trillion-dollar forecast once pushed NVIDIA's stock price up by over 4.3%, but the subsequent pullback was also understandable. When investors cooled down and compared this eye-catching figure with Wall Street’s pre-existing models, the sense of surprise quickly diminished.

According to Bloomberg consensus estimates, NVIDIA's total data center revenue for fiscal years 2026 to 2028 had already been projected at approximately $969.6 billion. The difference between this number and the newly announced $1 trillion is only about $30.4 billion, translating to roughly a 3% increase.

However, Goldman Sachs pointed out that this strong growth outlook is not only highly consistent with the bank's own estimates but far exceeds market expectations. This move provided investors with reassurance, effectively alleviating widespread concerns about a potential 'peak in capital expenditures' by 2026.

Notably, behind this $1 trillion in demand lies a fundamental shift in business logic.

Currently, 60% of NVIDIA’s business is supported by the top five hyperscale cloud service providers (CSPs) such as AWS, Azure, and Google Cloud, while the remaining 40% is rapidly penetrating into diversified fields like sovereign clouds, enterprise applications, industrial robots, and edge computing. This also signals to investors that NVIDIA’s growth trajectory no longer solely relies on chip iteration but is deeply tied to the global AI industrialization process.

Related stocks:NVIDIA and its core cloud service providers $Microsoft (MSFT.US)$ 、 $Alphabet-C (GOOG.US)$ 、 $Amazon (AMZN.US)$ 、 $Meta Platforms (META.US)$ 、 $Oracle (ORCL.US)$ 、 $CoreWeave (CRWV.US)$ 。

II. Foundation of the Industrial Chain: Breaking the Limits of Computing Power and Physics

At the forefront of the AI industrial chain, NVIDIA has demonstrated an overwhelming dominance with its 'one update per year' strategy.

1. Chips and Memory: The Surge in Inference and Computing Power

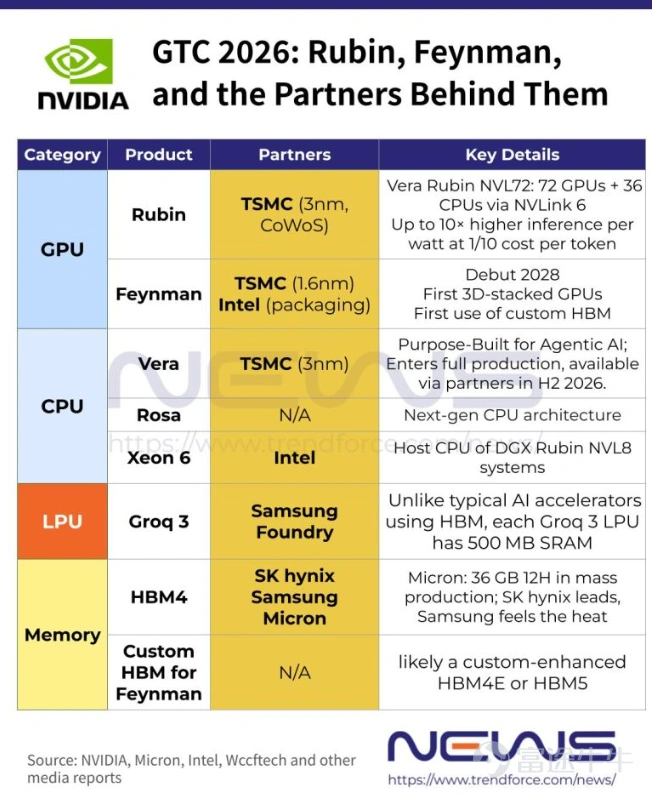

The launch of the Vera Rubin computing platform marks NVIDIA's complete transition from selling single chips to offering rack-level system solutions. Vera CPU debuted as an independent business, directly targeting the core markets of traditional giants. In the field of ultra-high-speed inference, NVIDIA officially launched the LPU (Inference Accelerator), incorporating Groq’s technology, filling a market gap and achieving a 35x increase in throughput. Jensen Huang publicly confirmed for the first time that Groq 3 LPU is manufactured by Samsung; Micron announced HBM4 entered mass production in Q1 2026.

2. Competitive Ecosystem: Intel’s Pragmatic Positioning

Within the computing power ecosystem, Intel exhibits a subtle ‘coopetition’ logic. On one hand, Vera CPU poses a challenge, but on the other, Intel solidified its cooperation at the conference, confirming that its Xeon 6 processor will provide computational support for the DGX Rubin NVL8 system, ensuring backward compatibility for enterprise-level systems. Looking ahead, Intel is expected to participate in the packaging of the next-generation Feynman GPU as a foundry partner.

3. Physical Infrastructure: Copper and Optics Together, PCB Advancements, and Liquid Cooling as Standard

To break through capacity limitations, NVIDIA introduced a new generation of MGX racks—the NVIDIA Kyber. This rack doubles the NVLink domain capacity, accommodating up to 144 GPUs. Jensen Huang clearly stated: 'Copper remains important, optics are used for expansion across different dimensions, both are essential capabilities.'

The exponential leap in computing density directly triggered three core increments in physical infrastructure:

Integration of Optics and Copper: In the short term, CPO (co-packaged optics) will be prioritized in scale-out networks to alleviate power consumption and bandwidth pressures, while scale-up expansions within Kyber and Rubin architectures will still largely depend on advanced copper interconnects.

Major PCB Upgrade: Renowned Apple supply chain analyst Ming-Chi Kuo pointed out that the scaled mass production of LPU/LPX racks will have a profound impact on the PCB supply chain. The high-frequency data exchange among 144 GPUs is driving the evolution of HDI boards towards higher layer counts (24-30 layers or more), leading to a surge in demand for ultra-low loss materials (such as M8-grade copper-clad laminates). Relevant manufacturers are experiencing both volume and price increases.

Liquid cooling has become essential: Vera Rubin is now 100% liquid-cooled,Installation time has been reduced from two days to just two hours, utilizing 45°C hot water cooling, which significantly reduces data center cooling pressure.

Core beneficiary companies of infrastructure:

Contract manufacturing and testing: $Taiwan Semiconductor (TSM.US)$ 、 $Intel (INTC.US)$ 、 $ASE Technology (ASX.US)$ 、 $Amkor Technology (AMKR.US)$ 。

Optical and copper interconnects: $Coherent (COHR.US)$ 、 $Lumentum (LITE.US)$ 、 $Ciena (CIEN.US)$ 、 $Amphenol (APH.US)$ 、 $Credo Technology (CRDO.US)$ 。

Software and Agent ecosystem: Defining the 'Intelligent Agent Era', traditional SaaS is undergoing significant changes.

In addition to hardware barriers, Jensen Huang devoted a significant portion of his discussion to the revolution in AI software and ecosystems, particularly the explosion of Agents.

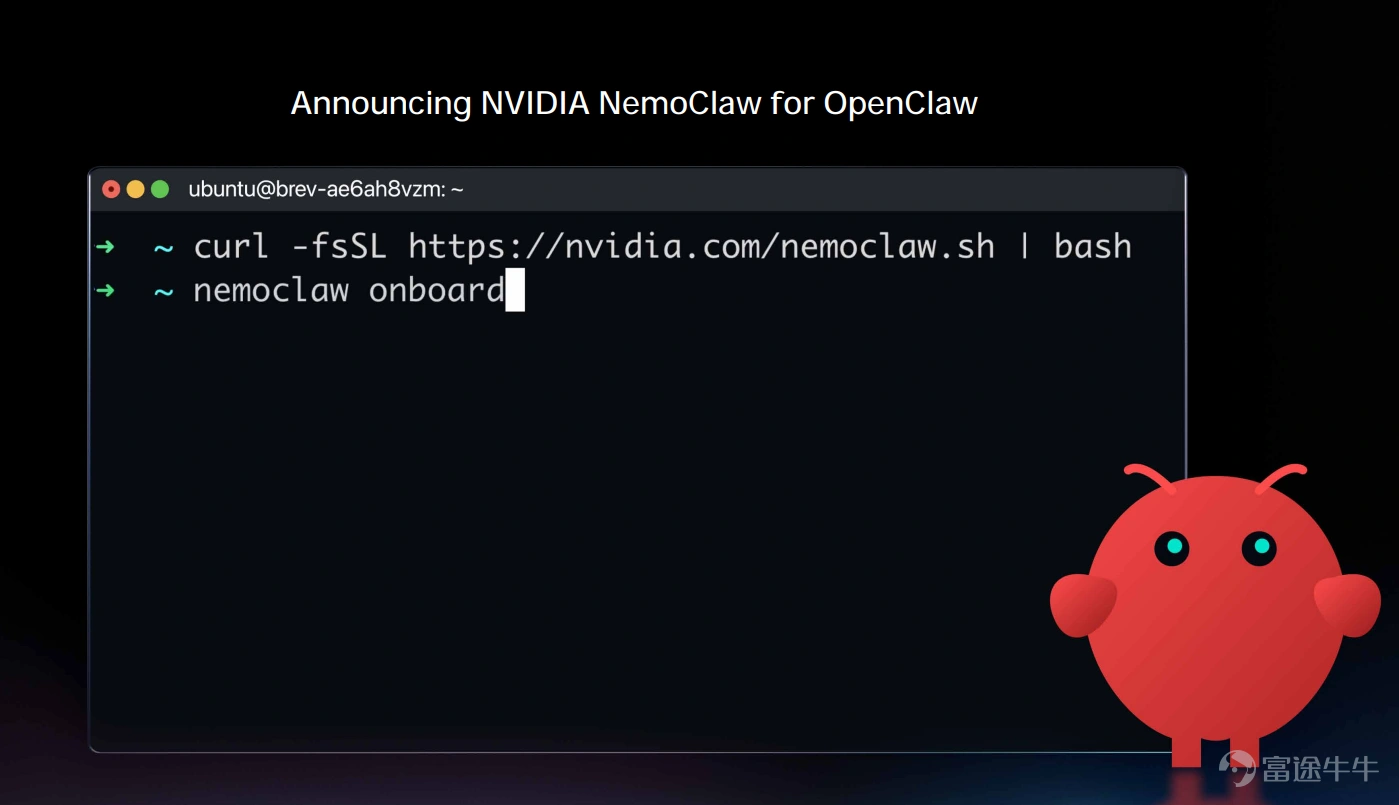

He described the open-source project OpenClaw as 'the most popular open-source project in human history' and asserted:Every SaaS (Software-as-a-Service) company will become an AaaS (Agent-as-a-Service) company.

There is no doubt that in order to safely implement these agents, which have the ability to access sensitive data and execute code,NVIDIA has launched the enterprise-grade NeMo Claw reference design, adding a policy engine and privacy router.

Compared to open-source systems, Nemo Claw establishes extremely high security barriers for enterprise applications. As software giants like Adobe and Salesforce prominently join the Nemotron ecosystem alliance, AI is accelerating its transformation from a 'passive dialogue tool' to an 'active task-executing digital employee.'

Third, industry boundary expansion: venturing into the vast universe of embodied intelligence and space computing.

NVIDIA’s ambitions have moved beyond traditional data centers to venture into a much broader universe.

In the embodied intelligence (Physical AI) sector,NVIDIA not only released a full-stack robotics software platform but also showcased its collaboration with $Disney (DIS.US)$ The Olaf robot, jointly developed.

In addition, the company officially announced a deep partnership with $BYD COMPANY (01211.HK)$ 、 $Nissan Motor (7201.JP)$ and other automakers, and has partnered with Uber Technologies to target a global Robotaxi (self-driving taxi) network by 2027.

Even more impressive is its grand vision of 'space computing.' NVIDIA is secretly developing 'Vera Rubin Space-1'with the aim of delivering powerful AI computing power directly into low Earth orbit. This move will completely revolutionize the existing model of spatial data analysis by enabling real-time inference in orbit, reducing bandwidth consumption for satellite-to-ground data transmission by 90%.

Relevant companies:

Autonomous Driving and Mobility: $Uber Technologies (UBER.US)$ 、 $Pony AI (PONY.US)$ 、 $WeRide (WRD.US)$ 。

Commercial Aerospace: $Rocket Lab (RKLB.US)$ 、 $AST SpaceMobile (ASTS.US)$ 、 $EchoStar (ECHO.US)$ 、 $Iridium Communications (IRDM.US)$ , among others.

Summary

The core logic of this conference lies in: NVIDIA has transformed from being a single hardware supplier into an 'AI Infrastructure and Factory System' The transformation of the entire debt platform. Its investment value is no longer limited to GPU iteration but is deeply tied to the global AI industrialization, physical infrastructure innovation, and the Agent ecosystem.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (7)

to post a comment

116

319