Global Weekly Insights | US Economic Growth Slows, China's Price, Trade, and Financial Data Impress

On the macroeconomic front

United States: Economic growth slows, inflation resilience stands out, manufacturing recovery hits roadblocks

Last week, the US focused on delayed key economic data and manufacturing-related indicators. Economic momentum cooled significantly, with stubborn inflation putting the Federal Reserve in a policy dilemma.In terms of GDP, the annualized quarterly growth rate of real GDP in Q4 2025 was revised down sharply to 0.7%,far below the preliminary estimate and Q3 growth rate. The full-year growth rate was revised down to 2.1%, with government spending and exports as significant drags. On consumption and inflation, January saw a pattern of 'strong income, weak consumption,' with personal disposable income rising 0.9% month-on-month while real PCE grew only 0.1%, and the savings rate rebounded. Core PCE rose to 3.1% year-on-year (the highest since March 2024),with inflation cooling less than expected and geopolitical tensions pushing up oil prices, expectations for Fed rate cuts continued to decline.In manufacturing, durable goods orders were flat in January, far below market expectations. The core capital expenditure indicator slowed, with transportation equipment orders being a major drag. Although shipments and backlogs provided short-term support, ongoing inventory accumulation added pressure for future destocking, hindering the manufacturing recovery.

China: Prices, trade, and financial data perform strongly, PMI affected by seasonal factors

China's price, financial, trade, and PMI data showed an overall positive trend, with some indicators affected by seasonal factors. Regarding prices, February saw both month-on-month and year-on-year increases in CPI, with core CPI rising 1.8% year-on-year,mainly driven by concentrated Spring Festival demand, with significant service price increases.PPI increased month-on-month for five consecutive months, while year-on-year declines narrowed for three straight months, benefiting from rising international commodity prices and effective domestic policies. Emerging industries showed positive price performance. In finance, new aggregate financing and RMB loan increments for January-February exceeded expectations, with M2 growing 9% year-on-year at the end of February, M1 growth rebounding, and the gap between M1 and M2 further narrowing, indicating ample liquidity. In trade, total import and export value in the first two months rose 18.3% year-on-year.Both exports and imports achieved double-digit growth, with private enterprises as the main growth driver.Trade growth with ASEAN and countries participating in the Belt and Road Initiative was notable, while trade with the US declined year-on-year. Regarding PMI, the manufacturing PMI continued to contract in February, while the non-manufacturing sector showed slight improvement.This was mainly due to the impact of the Spring Festival holiday. A seasonal rebound in the manufacturing PMI is expected in March.

In terms of the equity market

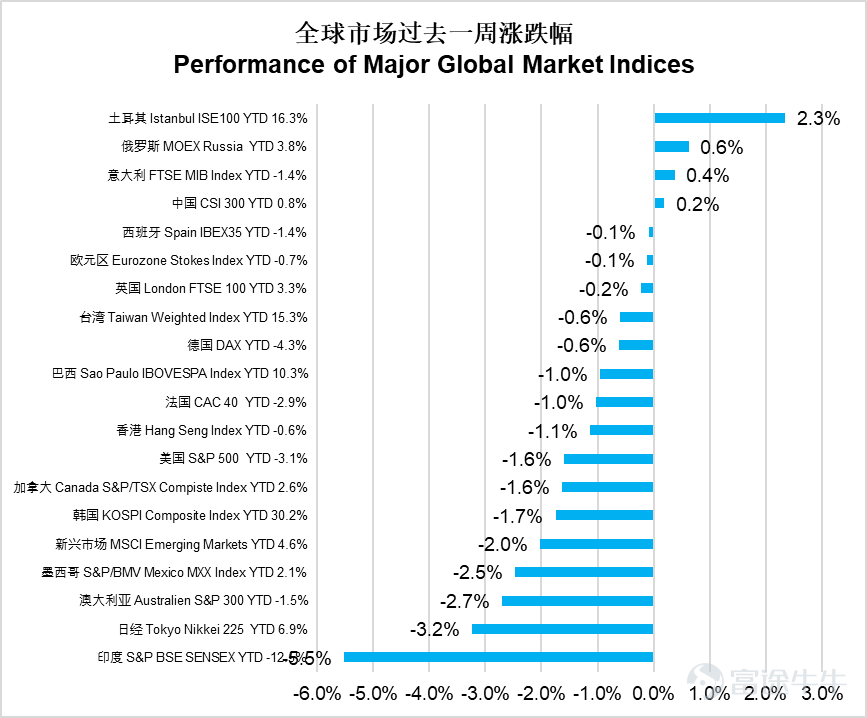

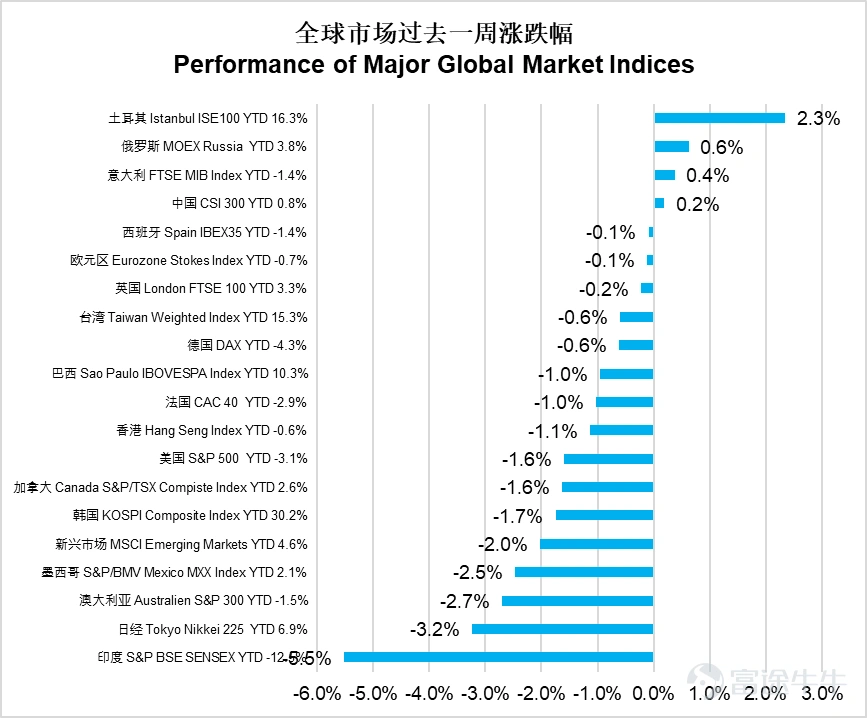

Last week, global markets generally fell, with India's Sensex Index plummeting 5.5%, leading the declines worldwide.The Nikkei 225 dropped 3.2%, and Australia’s S&P 300 fell 2.7%. Emerging markets overall declined by 2.0%, with Mexico’s MXX down 2.5% and the Hang Seng Index falling 1.1%. Turkey’s ISE100 rose 2.3%, showing the best performance, while Russia’s MOEX increased by 0.6%, and Italy’s FTSE MIB climbed 0.4%. The US S&P 500 fell 1.6%, while China’s CSI 300 edged up 0.2%.Overall, some European markets demonstrated relatively resilient performances, while Asian emerging markets faced significant pressure.

The US energy sector stood out with a 2.1% rise, performing exceptionally well.The utilities sector rose by 0.4%, becoming one of the few sectors that gained. Information technology fell 0.8%, and consumer staples dropped 0.2%, with relatively smaller declines. However, the financial sector plummeted 3.4%, industrials fell 3.2%, and consumer discretionary dropped 3.0%. Healthcare declined 2.0%, while materials and real estate fell 1.6% and 1.5%, respectively.Communication services fell 1.2%. The market exhibited a pattern of energy rising alone while finance and industrials led the declines.

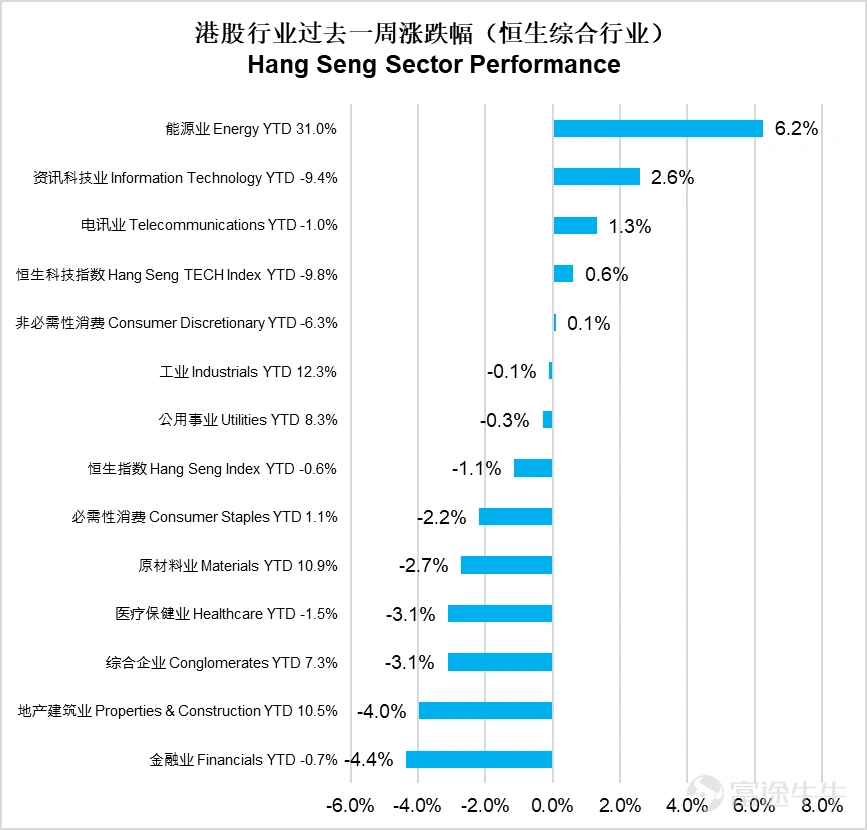

Hong Kong’s energy sector surged 6.2%, showing the best performance, while the information technology industry rose 2.6%.The telecommunications sector rose by 1.3%. The Hang Seng Tech Index increased by 0.6%, while non-essential consumption edged up by 0.1%. However, the financial sector plummeted by 4.4%, real estate and construction fell by 4.0%, healthcare and conglomerates both declined by 3.1%. The raw materials sector dropped by 2.7%, and essential consumption decreased by 2.2%.The industrial sector slightly fell by 0.1%, and utilities declined by 0.3%. The market displayed a divergence with energy and technology leading gains, while finance and real estate led losses.

In the bond market,

Global bond markets slightly retreated overall in the past week,The Global Aggregate Index fell by 1.23%, the US Aggregate Index declined by 0.92%, US investment-grade corporate bonds dropped by 1.44%, and US high-yield corporate bonds fell by 0.77%. The Emerging Markets USD Bond Aggregate Index decreased by 0.83%.The China USD Credit Bond Index declined by 0.49%.

In terms of interest rates, US Treasury yields rose overall,The 2-year US Treasury yield rose by 16 basis points to 3.72%, and the 10-year US Treasury yield climbed by 14 basis points to 4.28%.

Market Outlook

– Market expectations for interest rate cuts by the Federal Reserve this year may be less than one time, and inflation could pick up again.

The Middle East geopolitical conflict remains the core issue in the market. Although the US stated that most strategic targets have been destroyed,the Strait of Hormuz remains closed, and oil prices surged past $100 from last week's $90. The release of strategic reserves by G7 countries fundamentally cannot address the supply-demand gap caused by the closure of the strait. If the situation persists, high oil prices will significantly impact global inflation.US consumer gasoline prices have risen, and recent inflation data showed that prior to the Middle East conflict, US inflation was on a downward trajectory as expected by the Fed.However, if the strait cannot resume passage in the short term, we may see inflation picking up as early as in the March US CPI data.Amid rising oil prices, the market's expectation for the Fed's rate cuts this year has further declined from last week's one to two times down to less than one time.If oil prices rise further, the market may shift its expectations for this year’s Federal Reserve interest rates towards no rate cuts or even a rate hike. The S&P 500 has pulled back nearly 5% from its January peak.As analysts have not yet revised down their full-year corporate earnings forecasts, apparent valuations have receded somewhat.However, the overall valuation level still exceeds 20 times the forward price-to-earnings ratio, remaining relatively high by historical standards. From the perspective of market sentiment indicators,there has been no sign of panic selling so far.If tensions escalate or the duration extends, it is possible that markets could see further declines.

Key economic data and events this week

China will release February’s retail sales, industrial production above designated size, unemployment rate, and corporate profits data on Monday.

The US will announce the March FOMC interest rate decision on Thursday.

All rights reserved © 2026. E Fund Management (Hong Kong) Co., Limited.The issuer of this report is E Fund Asset Management (Hong Kong) Co., Ltd. This report does not constitute an invitation or recommendation to invest in fund units. Fund unit subscriptions can only be made using application forms accompanied by the fund prospectus. Investment involves risks; fund prices may go up or down, and past performance is not indicative of future results. Before investing, investors should carefully read the investment risks related to the fund in the fund prospectus (including the 'Risk Factors' section). This report may only be distributed within certain jurisdictions. In any jurisdiction where distribution of such information or making any invitation or recommendation is prohibited, or if distributing this report or making an invitation or recommendation to any person constitutes a violation of the law, this report does not constitute such distribution or invitation or recommendation. This document is exempt from prior review and approval by the Hong Kong Securities and Futures Commission (SFC) and has not been reviewed by the SFC. SFC recognition does not imply a recommendation or endorsement of the scheme, nor does it guarantee the commercial merits or performance of the scheme, nor does it represent that the scheme is suitable for all investors, or endorse its suitability for any individual investor or class of investors.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

1

1