Pop Mart plans to launch new products! Can the IP giant capitalize on this opportunity?

Market Forecaster Weekly Call | 2026 Consumer Trends: Pop Mart Revaluation & Sporting Goods Take the Lead

Consumer Track Special Topic: In-depth Sharing of the Sporting Goods Industry (Joe Yu):

1. Opening: Quick Overview of Market Weekly Views US Stocks: High Volatility, Weak Index, Strong Structure

Index level is constrained by high oil prices and delayed rate cuts, leading to a decline in risk appetite; growth stocks are not optimistic in the short term, but should not be overly pessimistic in the medium term.

High oil prices weaken the 'soft landing' narrative and promote stagflation trades; delayed rate cuts have pressured the discount rates for growth stocks.

Allocation preference: prioritize defense-related assets, energy, and defensive assets; selectively invest in leading tech stocks (e.g., NVIDIA), with one each in hardware and AI.

Hong Kong Stocks: Short-term outlook leans positive, with potential for valuation recovery

The Hang Seng Index/Hang Seng Tech dynamic P/E ratios are approximately 11x/17x respectively; expectations of earnings downgrades have been largely priced in, indicating room for future valuation recovery.

The impact of high oil prices on Hong Kong stocks is mainly indirect (global risk sentiment + USD liquidity transmission); however, it supports high-dividend central state-owned enterprises in sectors such as oil, gas, coal, and electricity, which can act as 'framework assets' within portfolios.

II. Assessment of the Macroeconomic Consumption Environment in 2026

Core Tone: Low Growth but Stable, Not a Full Reversal

In 2026, consumption will exhibit characteristics of "stabilizing total volume, improving structure, and continuing stratified spending," more likely reflecting low but stable growth rather than significant re-acceleration. Households remain constrained by weak employment and wages, deleveraging, and the drag from real estate. Precautionary savings and low consumer confidence remain key suppressive factors. Nominal year-on-year retail sales growth is forecasted to rise from 3.9% in 2025.5.5%Goods consumption is expected to pick up pace.

Investment Insights

Avoid the assumption of a "pure macro-driven broad-based rally"—If the investment thesis is solely based on a full recovery in household purchasing power, sector elasticity is easily overstated.

Focus on alpha opportunities—Sub-sectors with more restrained supply, healthier pricing systems, and demand driven by professionalism or sentiment.

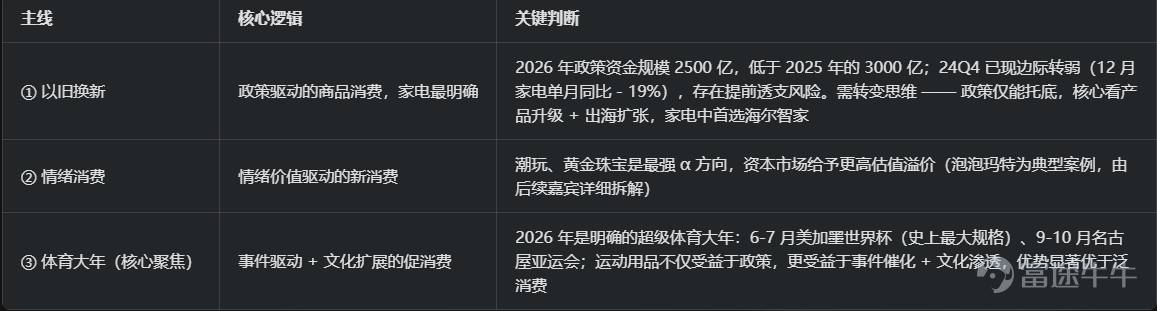

III. Three major investment themes in consumption for 2026

IV. Why is sporting goods the clearest consumer direction for 2026? — Three core advantages

Advantage one: Low penetration rate and per capita spending, with huge long-term growth potential

Per capita spending on sports shoes and apparel in China is only45 USD, less than half of Japan (90 USD), one-third of South Korea (166 USD), and one-third of Germany (150 USD). The penetration rate of sports shoes and apparel in China is just15%The United States is at 37-40%, Japan at 22%, with clear and optimistic room for improvement.

Advantage two: Demand shifting from general sports to vertical specialization, with high-growth niche segments significantly outpacing the industry

The overall annual growth rate of sports shoes and apparel is about 5%, butthe predicted CAGR for the outdoor segment between 2025-2027 is 16%, significantly higher than the overall industry. Outdoor, running, and tennis are the core growth engines, with significant alpha opportunities existing in vertically segmented fields.

Advantage Three: Product innovation-driven, local brands regain pricing power

By the end of 2025 to early 2026, local brands will release a flurry of new professional running shoes: the Xtep 2000 km series, 361 Degrees' Fei Ran series, etc., building product barriers through new technology, new scenarios, and new brand matrices.

Core conclusion: Sporting goods possess four key elements—long-term penetration logic, short-term event catalysts, concentrated brand share, and product innovation support—making it the clearest investment direction in the 2026 consumption theme.

Five: Dissection of the global sports brand landscape

(1) Domestic brands: Shifting from mass-market sports to professional running, outdoor activities, and high cost-effectiveness

Anta Sports – Platform leader, the top choice for portfolio allocation.Core strengths: It is not a single-brand explosion but rathermulti-brand, multi-price range, multi-scenarioplatform-based coverage.Operating DataIn 2025, the main brand is expected to grow at a low single-digit rate, FILA at a mid-single-digit rate, and other brand portfolios (Descente, KOLON, etc.) are projected to grow over 45% year-over-year; group-wide annual sales flow will grow at a double-digit rate; in Q4 2025, Descente +25-30%, KOLON approximately +55%.Market concernsSlight decline in the main brand’s sales flow, and whether FILA can maintain mid-to-high single-digit growth.ValuationForward P/E ratio for one year is approximately 15x, and forward P/E ratio for two years is around 14x, which is within an acceptable range.Outstanding cash flow advantageFree cash flow reached 15.7 billion yuan in 2024, with nearly 11 billion yuan net cash inflow in H1 2025 and 7.5 billion yuan free cash flow. Anta Sports does not rely on store expansion or financing for growth but instead drives brand expansion and acquisitions through operating cash flow—this high-quality cash flow ensures its investments in advertising, R&D, and acquisitions won’t be pressured by capital expenditures during industry fluctuations.Investment positioningMost suitable for institutional and allocation-oriented clients asLong-term Core Holdings。

361 Degrees – The best value-for-moneyDomestic brand with the highest upside potential.Operating Data: Main brand offline +10% in Q4 2025, children's wear offline +10%, e-commerce revenue growth in the high double digits; inventory ratio maintained at around 4.5x, excellent operational health.Valuation: TTM PE is only about9 times, offering extremely high safety margins compared to double-digit revenue growth, healthy inventory, and strong e-commerce expansion.E-commerce performance: E-commerce performed the best in the sales mix.Investment positioning: If event-driven catalysts in 2026 lead to sector recovery, 361 Degrees is theeasiest target to experience both valuation expansion and profit realization,with the highest upside potential.

Li Ning - High elasticity in recovery but with the lowest certainty. Fundamental changes: In Q3, institutions quietly upgraded their ratings; in Q4, full-channel sales declined by a low single-digit percentage (an improvement from before), e-commerce remained flat, and inventory returned to a normal level of 4-5 months ——The worst moment may have passed, but the earnings inflection point has not yet been fully established.。Key highlights for 2026: Not purely a fundamental recovery, but rathernew product categories, new store formats, and the introduction of Olympic/Asian Games resources.Continuing as the sports apparel partner of the Chinese Olympic Committee, covering events such as the Milan Winter Olympics and the Nagoya Asian Games.Valuation: TTM PE is approximately 18x, against the backdrop of weak fundamentals,it cannot be considered cheap,and will require betting on whether an earnings reversal or event catalysts can change market perceptions.Investment positioning: Suitable forEvent-driven allocation, not suitable as a long-term base holding. Summary of the three major domestic brands

Xtep International - a typical undervalued professional running shoe stock, with expected net profit growth of 11-19% by 2025, and further mid-teens improvement anticipated for 2026, with the core variable being the running shoe market. Among the three Hong Kong-listed companies: Anta Sports shows the most balanced growth quality, Xtep demonstrates the strongest structural elasticity (outperforming Li Ning as a high-elasticity stock), while Li Ning has the lowest certainty.

(ii) Overseas Brands:

Adidas exhibits the strongest fundamentals and catalysts, while Nike is still in the recovery phase

Adidas – the top overseas choice and the most direct beneficiary of the World Cup. Management views the 2026 World Cup asa commercial opportunity exceeding 1 billion euros。Revenue realization timeline: Q4 2025 has already contributed approximately 200 million euros, with expectations to contribute around 800 million euros in H1 2026. Fundamentals and event catalysts are formingthe strongest resonance, making it the most certain choice among overseas stocks.

Nike - In the process of recovery, with the Chinese market still being the main drag. Management acknowledged a decline in foot traffic at Chinese stores, disappointing product sales for the quarter, and inventory overhang; inventory reduction plans have been implemented at stores in Beijing, Shanghai, and other locations. Still in therecovery expectationphase, positioned as a thematic trading opportunity/distressed turnaround play, no rush to establish positions.

(III) US Sports Brands: Select growth track

(IV) Global Valuation-Growth Matrix Overview

Deep Value Zone(Growth + Cheap Valuation): Anta Sports, 361 Degrees, and Xtep - Stable growth but PE ratios still in the single digits to 15x.

Growth + Bubble Coexistence Zone(High Growth + High Valuation): Deckers, On Running - Emerging brands enjoying high growth premium, with both risks and opportunities present.

Low Attractiveness Zone: Nike - Valuation is not cheap and net profit growth remains weak.

PEG framework conclusion: Anta Sports and Xtep's growth-to-valuation alignment is better than Li Ning and Nike; Deckers and On Running's growth trajectory justifies their high valuations.

6. Event catalysts and entry timing in 2026

Connection of two major events: World Cup (June-July) → Asian Games (September-October), with August-September formingcontinued media support and peak market sentiment。

Entry rhythm: Q1-Q2 early positioning in World Cup beneficiaries → Q2-Q3 tracking World Cup sales data → Q3-Q4 increasing positions in domestic brands before the Asian Games.

7. Final investment rating and allocation recommendations

Three-level classification of underlying assets

Summary of market allocation strategy

In-depth analysis of Pop Mart by Lu Huiyu, Analyst at Hua’an Hexin

Part One: The foundational basis for IP consumption

What is IP consumption?

The essence of IP consumption isthe pricing and commercialization of cultural products, a form of 'meaning consumption.' Its development benefits from two favorable conditions:

Economic prosperity: After achieving material abundance, consumers show greater respect for original copyrights;Turbulent environment: The higher the uncertainty, the more people need meaningful consumption to achieve spiritual compensation.

Historical validation: The world's most valuable IPs were concentrated in two periods — the Great Depression in the United States and Japan’s lost two to three decades.

II. The Triple-Demand Model of Meaningful Consumption

The demand for meaningful consumption has existed since ancient times, transcending time and culture, with long-term sustainability. Specifically, it can be broken down into three categories:

III. The macro environment for Pop Mart's growth

1. China: IP consumption is just beginning

Per capita GDP has just surpassed $10,000, with a target to double again by 2035; the economic foundation is still on an upward trajectory;Prominent structural issues: Over the next decade, three major demographic trends are clear — an increase in retirees, a decrease in women of childbearing age, and a rise in graduates; young people are facingDownward pressure on income expectations and upward pressure on spending expectationsDouble squeeze → choosing to forgo big-ticket consumption (not buying homes, not having children) → released purchasing power shifts towardEmotional or self-indulgent spending that brings joy; This forms the foundational environment for Pop Mart's rapid growth domestically and represents a significant market.

2. Global: Resonating demand

The rapid development of AI is replacing entry-level positions (i.e., job opportunities for young people); fluctuations in geopolitical risks are intensifying; globally, young people generally need meaningful consumption as emotional compensation and comfort ——Global demand resonance。

3. China’s infrastructure advantage in consumer goods exports

China not only leads in traditional infrastructure but also has extremely high efficiency in spreading informational infrastructure (e.g., short videos, web series); it possessesThe ability to compete globally with overwhelming superiority, optimistic about the continued overseas expansion of Chinese consumer goods.

Fourth, how large is the IP consumption market?

Core viewpoint: There's no need to look at the ceiling because the ceiling is extremely high.IP can collaborate with anything, with unlimited forms of expression. Greater attention should be given to the company's product innovation capabilities and the extensibility of IP consumption.

The business logic of the industry boils down to two key capabilities:Communication + Retail。

Part Two: Analysis of Pop Mart's retail capabilities

First, the origins from agency to proprietary IP

In its early days, Pop Mart was an IP agent. After the IPs they represented became popular, the IP owners reclaimed them for self-operation at higher prices. Wang Ning solicited IPs via Weibo, and Molly received the highest votes. Subsequently, they signed Molly in Hong Kong as a proprietary IP. In its early days, Molly once accounted for more than 40%.

Second, the issue of IP lifecycle and countermeasures

Issue: The natural instability of IP growth — The Monsters (Labubu series) saw declining sales in 2022-2023 after 2021, which reflects the lifecycle challenges naturally faced by IPs.

Solution: New categories + Family-oriented extensions.

Taking Molly as an example:In 2023, only one blind box for Molly was released throughout the entire year, indicating a significant decline in innovation frequency seven years after its launch.Solution: Introducing family-oriented extensions such as Baby Molly and Angry Molly, along with launching the new Mega category in 2021; Outcome: By 2024, Molly restored its update frequency to 3-4 times per year.

The rise of plush products:The success of plush was not an overnight achievement. Starting from 2021, Pop Mart had extensively experimented with various new categories. Plush becamethe result of a competitive mechanism.; However, caution is needed: Multi-format experimentation can lead to 'diversification deterioration' and inventory risks from outdated IPs, demanding high organizational management skills and close coordination between channels and supply chains. Third, channel capability: The core advantage of a fully direct-operated model.

4. The rapid evolution of the supply chain

5. The strategic value of retail capabilities

After the popularity of Labubu overseas, Pop Mart can leverage this retail system (direct stores + rapid supply chain iteration)to capitalize on the buzz, convert it into revenue, and retain users;

Overseas revenue achieves leapfrog growth: from only 200 million yuan in H1 2022 → to 5.6 billion yuan in H1 2025, growing over 27 times in three years, becoming the core driver of performance growth.

6. Organizational structure: The management DNA of flexible iteration

Two major organizational restructuring events in history: First: Adjusting the product department → leading to the success of plush categories; Second: Adapting to global expansion.

Wang Ning himself: A self-made entrepreneur from a grassroots background, part of the younger generation of business leaders, with strong charisma (many current executives are his classmates), making flexible decisions.

Part Three: Breaking down Pop Mart's communication capabilities

1. How did Labubu become popular?

The SparkLisa (from BLACKPINK) is a self-driven promoter of Labubu, personally liking it and making it popular in Thailand;

Expansion PathThailand explosion → Western fashion circles → Sports circle → Mass following to form a trend;

Core logicFor just 99 yuan (overseas one or two hundred yuan), you can own the 'same model as celebrities'—a perfect 'class eraser' product.

2. Will Labubu only be a passing fad? — The Halfway Theory

The complete consumer journey: unawareness → recognition through various opportunities → obsession (blind box gambling nature, scarcity, premium pricing) → retention as 'true fans' through continuous operation → or disengagement and departure

Definition of True Fans: They no longer purchase every month but will keep an eye on new releases and buy one or two if they fit their aesthetic — this is sufficient for Pop Mart. True fans are Pop Mart's most core asset.

Labubu naturally has excellent potential for family expansion (referencing Molly’s family experience); logically, it has the potential for sustained growth. Comparable reference: Hello Kitty

Core assessment: Labubu is still at the halfway point with very low penetration rates.

Third, Pop Mart ≠ Labubu, Labubu ≠ Pop Mart

Pop Mart is an IP platform

At the time of its IPO in 2020, it had 28 artists under its wing, now streamlined to six, who are mostly associated withbillion-dollar IPsand have an increasingly matureIP selection and elimination mechanism, with Labubu being a successful result of this competitive process; artists come from diverse backgrounds: the company organized one of the earliest large-scale trendy toy exhibitions domestically, signing many artists at these events—to a certain extent defining the industry。

with strong influence over artists

A halo effect: successful experiences feed back into other IPs

Star People (Other characters from The Monsters): Their approach is very similar to Labubu. Before 2024, they signed with another company in the same industry (Super Meta Factory) but did not gain much popularity; after signing with Pop Mart in 2024, they became hugely popular domestically within a year; attracting top designers strongly – their individual strengths can be better amplified on Pop Mart’s platform;

Some even argue that Pop Marthas nearly monopolized the best pool of domestic designer resources(though somewhat exaggerated, its leading position is confirmed).

Part Four: Sustainability of IP Operations – Core Controversies and Framework

1. Must a good IP necessarily originate from long-form content? Answer: Not necessarily.The current communication environment is highly fragmented, the information infrastructure has completely changed, and the forms of content creation are bound to differ;Disney itself is also evolving: In 2021, it launched the LinaBell family, a pure character-based IP without any content background. Although its popularity has declined now, sales continue to grow annually—The true fans have settled in; but longer content is definitely better - it can support the IP's longevity and extend its lifespan.

Second, where does good content come from? - Three pathways

Pop Mart's current situation:

Language system: initially established

Interactive gameplay: initially established

Worldview construction:Yet to prove itself, requiring a long time for validation -This is the most controversial core reason for Pop Mart currently

Third, IP operation = Good content + IP maintenance + Unified retail operations

IP maintenance (legal capability)

Disney and Nintendo have extremely strong legal departments; Pop Mart is also enhancing its capabilities:

After Labubu went viral last year, the official team cooperated with customs to crack down on piracy; this year, there was a litigation dispute with Top Bamboo (3D printing);

Analyst's viewpoint: There is no fundamental conflict between Pop Mart and Top Bamboo’s business models. Cooperation may offer greater potential, but we need to keep observing Pop Mart’s progress in IP maintenance.

Retail capabilities must keep up with the hype

IP operations must be aligned with unified retail efforts—when popularity rises but the supply chain cannot keep up, it harms the business model; Miniso offers a cautionary tale: despite collaborating on many popular IP projects, their franchise model caused mismatches in product distribution, leading to lower-than-expected sales turnover.

Part Five: Financial Quality and Shareholder Returns

Part Six: Q&A Highlights

Q1: Will Labubu's revenue growth significantly slow down or even retreat as it did in 2022-2023?

Answer:The decline in 2022-2023 was influenced bymacro pandemic disruptionsand at that time, Labubu's product form (gashapon blind boxes) did not fully showcase its appeal—Labubu is naturally more suitable for plush products, where the attributes are less noticeable in blind box form.Penetration remains very low,with new people discovering Labubu every day. A decline in Google search data reflects the passing of the 'first discovery' peak but does not indicate a weakening of purchasing behavior.Latest data validation:The first-day sellout volume of Labubu × Sanrio collaboration plush was comparable to the previous 'Heartthrob' series, with continuous stockouts across overseas channels.Growth forecastA relatively conservative estimate predicts20-30% growth.——Labubu is already a brand with a scale of approximately 10 billion, and while continuous doubling is unrealistic, maintaining growth of 20-30% as a global brand is reasonably expected.

Q2: The number of suppliers is increasing rapidly; how do you view the management risks?

Answer:Reason for the surge in suppliers: High demand热度 requires capacity expansion, and the majority of upstream factories are small, leading to an apparent increase in supplier numbers.This was indeed a key concern previously.: After the increase in the number of suppliers, management difficulty rises exponentially, and quality control issues did emerge in the second half of last year.Positive signals: Timely response to quality control issues; new product process iteration has not stopped (new processes such as flocking and ceramics continue to be introduced with noticeable improvements).Conclusion: Management difficulty is indeed a risk, but the company's preliminary response indicates good iteration capabilities, and errors made are within the range the company can manage, which is acceptable.

Q3: How do you view the competitive threat from smaller companies and new entrants?

Answer: Competitive threats are currently not significant for four reasons: ① The long-tail market is large enough that it does not pose direct competition.Emotional demands are extremely complex, inevitably leading to a large number of niche long-tail markets; small and beautiful companies serving specific customer groups are entirely feasible but do not form zero-sum competition with Pop Mart. Characteristics of spiritual consumption: it's not 'if you buy from one brand, you won't buy from another,' consumers can purchase multiple brands simultaneously.Pop Mart has an extremely strong platform leverage effectThe same IP (such as Dimoo), which could only generate tens of millions in revenue annually at its previous company (Super Genki Factory), has now reached several billion to 20 billion yuan at Pop Mart; even if Pop Mart only gives artists a three percent share, the absolute income far exceeds what they would earn by taking fifteen percent on other platforms; outstanding designers will inevitably consider this factor when choosing a platform.Extremely high channel barriersAccess to prime properties such as China Resources MixC, SKP, and Deji requires proof of historical performance; it is extremely difficult to roll out 100 stores nationwide at once – even Ye Guofu (founder of Miniso) with his resources and capabilities couldn’t achieve that.High cost of resetting supply chain and delivery systemsPop Mart has a very thick delivery manual (learning from Japanese manufacturers); building this system takes time and trial-and-error costs; even with AI accelerating learning, it would take at least half a year or more.A typical negative case – WAKUKU: Starting at the same time as Dimoo, imitating Pop Mart’s strategy with celebrity endorsements and drama promotions, but due to the lack of its own direct sales channels and conflicts of interest caused by the separation of IP licensors and channels, it has now basically become dormant – It takes about six months to a year to prove that incubating IPs isn’t that easy.。⑤ The catch-up efforts of Miniso (Top Toy) validate the high barriers to entryAfter realizing the shortcomings of the franchise model, Miniso started learning from Pop Mart's approach: incubating its own IPs (such as YOYO), signing designers, and developing direct sales channels —This essentially represents a disruption of its own business model; from starting to learn last year until now, they plan to invest hundreds of millions or even billions; how much capital and time should new entrepreneurs prepare for this?The reset cost is not low。

Summary: Pop Mart’s investment framework

Key Conclusions

Pop Mart is a company with great potential, but it is difficult to confidently predict exactly what its future will be.

Wang Ning’s summary is the most precise:

"Initially, we aimed to do A (IP agency), ended up succeeding in B (Molly), later found success in C (Labubu), and perhaps in the near future, this company will achieve greatness in D."

Reasons to be bullish

The underlying consumer base for IP is solid (resonance between demand in China and globally);

Retail capabilities (fully direct operation + supply chain) are far ahead in the industry; the screening and elimination mechanism of the IP platform is becoming increasingly mature, with a noticeable siphon effect emerging;

Labubu is still at the halfway point, with very low penetration, and the ceiling—referencing Hello Kitty—is far from being reached;

The balance sheet and cash flow are extremely strong, supported by an asset-light model;

High reset costs for competitive barriers (platform leverage + channels + supply chain + designer influence);

Core risks and questions to be validated

Will Labubu’s GMV trend follow an A-shape (spike then fall) or stabilize after climbing?

World-building capability has yet to be proven – this is the biggest current controversy;

Quality control and management risks brought on by rapid supplier expansion;

Reflexivity of explosive popularity: public opinion backlash, factory incidents, offline order issues, all scrutinized under a microscope.

Whether diversified expansion (new business models such as jewelry stores) will lead to the deterioration of diversification;

Long-term risks of technological disruption from AI and 3D printing.

Investment advice framework

Weigh Pop Mart's current valuation against its associated risks and immense potential upside (potential returns) to make your own investment decision.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

4

1