Micron, the dominant player in US memory stocks, faces a major test: What is Wall Street really focused on?

Author | Eric

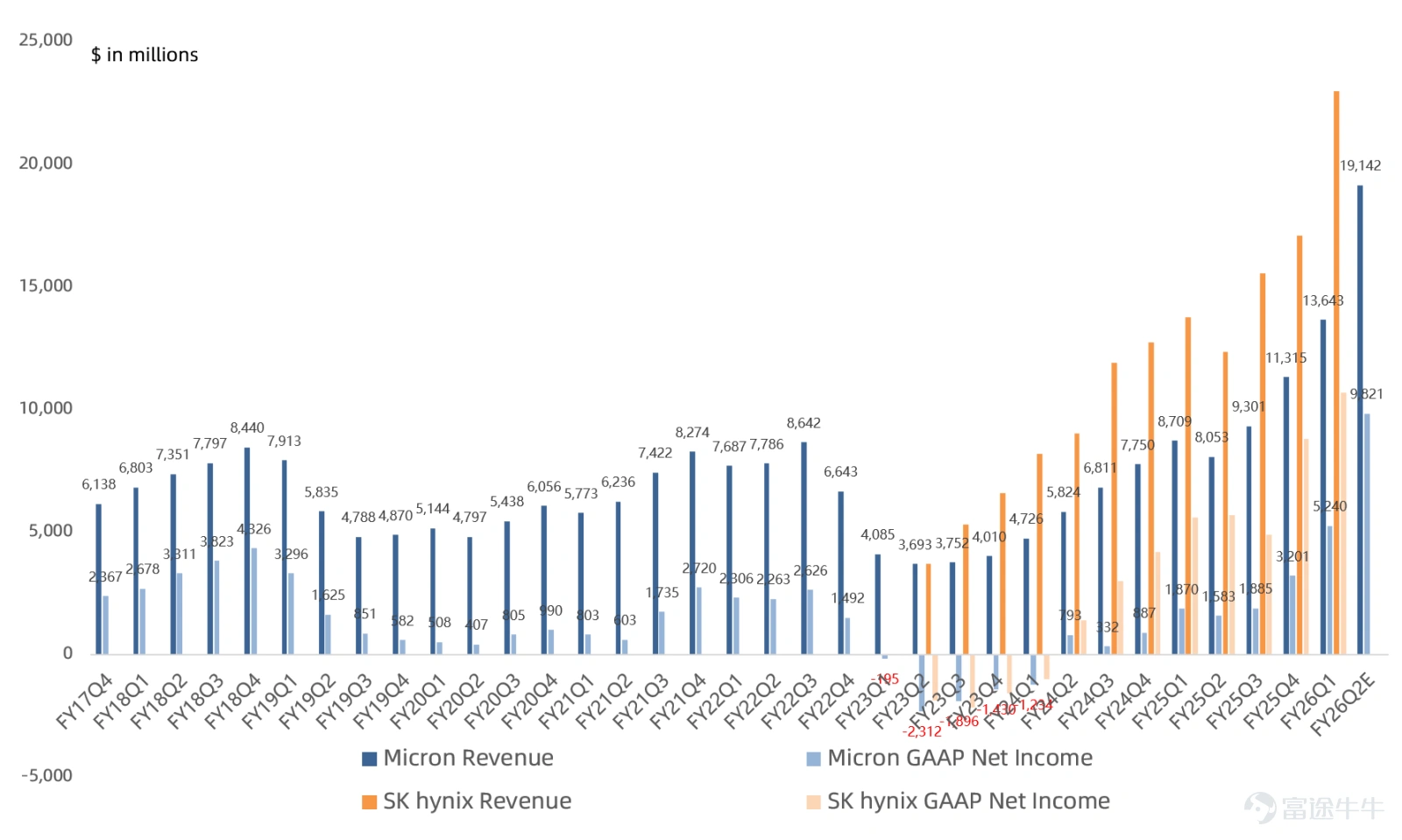

The leading American memory manufacturer, the world's third-largest DRAM and fourth-largest NAND provider, $Micron Technology (MU.US)$ is set to release its FY26Q2 earnings report after the market closes on March 18 in the Eastern Time Zone. The market is focused on whether this Micron earnings report can provide a turning point for the sentiment of the geopolitically impacted tech sector.

Consensus forecast for core financial metrics in FY26Q2:

- Consensus revenue forecastUSD 19.14 billion, growing by138%, representing a 40% quarter-over-quarter increase, with the company's guidance at USD 18.7 billion.

- GAAP gross margin consensus forecast67.9%, up 31.1 percentage points year-over-year and 11.9 percentage points quarter-over-quarter, with the company guiding at 67%. Non-GAAP gross margin consensus forecast is68.4%, up 30.5 percentage points year-over-year and 11.6 percentage points quarter-over-quarter, with the company guiding at 68%.

- Consensus GAAP net profit is expected to beUSD 9.82 billion, growing by520%, reflecting an 87% quarter-over-quarter increase, with the company's guidance at USD 9.34 billion. Non-GAAP net profit consensus forecast isUSD 9.79 billion, growing by449%, up 79% from the previous quarter, with the company's guidance at USD 9.68 billion.

Key highlights of this earnings report:

1. How did the management respond to market rumors that Micron’s HBM4 share fell short of expectations?

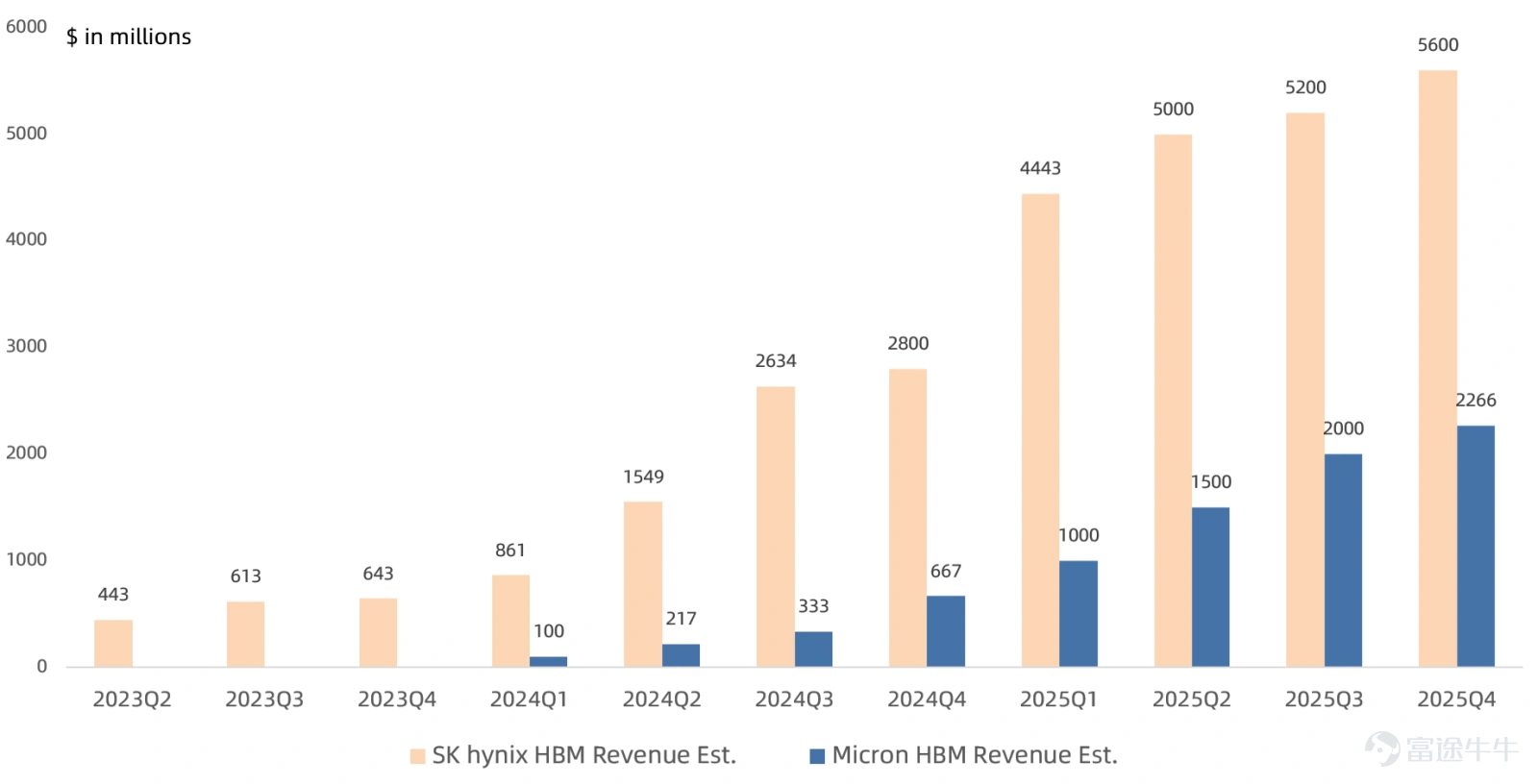

Last quarter, Micron's management stated that its HBM4 product is expected to start ramping this quarter,with all HBM capacity for 2026 already sold out.. Management forecasts HBM TAM to exceed USD 35 billionin 2025, growing to USD US$100 billion(CAGR 40%+), reaching the USD 100 billion milestone two years ahead of schedule. By 2028, the HBM TAM will surpass the entire DRAM TAM of 2024.

However, Korean media frequently reported that $NVIDIA (NVDA.US)$ the main orders for HBM4 are in the hands of SK Hynix and Samsung,Claimed that Micron's HBM4 has been delayed due to non-compliance with specifications, which would lead to a loss of market share. However, management later responded thatHBM4 is expected to have already started mass production in the first quarter of this year, one quarter earlier than the timeline provided in the previous earnings report. Pay attention to management’s response to market rumors in this earnings report.

2. How sustainable is the price increase for non-data center products?

The biggest difference in this cycle is that HBM is consuming advanced DRAM capacity, leading to a passive contraction in traditional DRAM supply, making it easier for prices to rise. In the NAND market, major storage manufacturers are more willing to expand DRAM production rather than NAND, resulting in a passive contraction in NAND supply as well.

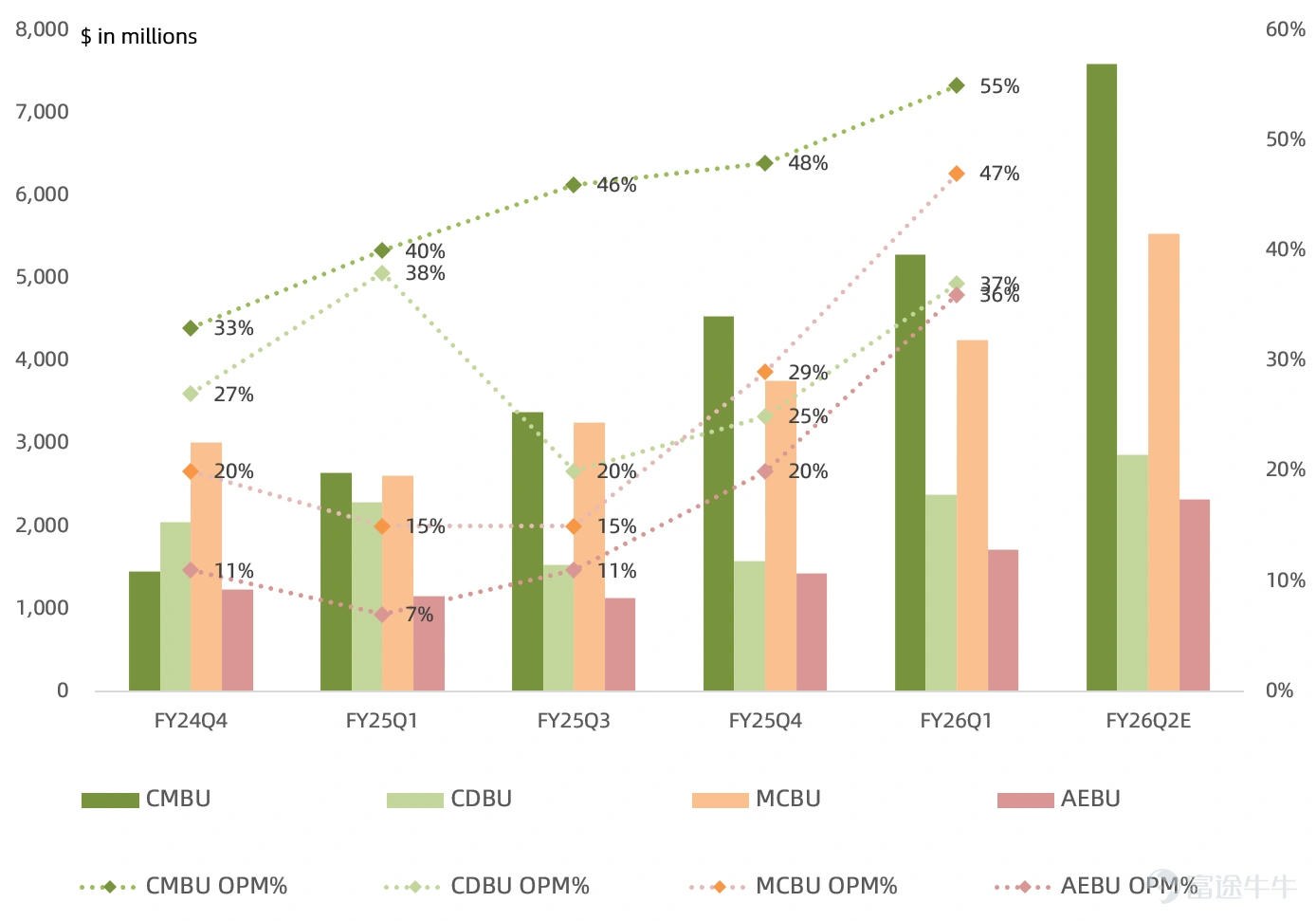

The biggest beneficiaries of this round of the super memory price surge turn out to be the previously sluggish non-data center businesses.Last quarter, the operating profit margin of the CMBU business, which is mainly focused on data centers,55%, increased year-over-year by15 percentage points, but the operating profit margin of the MCBU business, which is mainly mobile-focused, reached47%, increasing year-over-year by32 percentage points, and the operating profit margin of the AEBU business, which is mainly industrial-focused, reached36%, increasing year-over-year by29 percentage points, with growth far exceeding that of the data center business.

The market is most concerned about whether the demand for these non-data center businesses, which rely entirely on price increases, can be sustained. In the previous quarter's earnings report, management forecasted that supply and demand for DRAM and NAND will remain tight untilbeyond 2026, primarily constrained by cleanroom capacity. Let’s see how management views the supply-demand outlook for 2027 in this earnings report.

3. Non-HBM products drove overall gross margin to a new high; future guidance on gross margin trends warrants attention.

Before the current price hike cycle, Micron's gross margin was mainly driven by its HBM business growth.60%+Last quarter, the gross margin rose to56%. Looking back at Micron's FY2018 super price hike cycle, without the HBM business, price increases alone were sufficient to drive traditional DRAM and NAND products, supporting the company’s overall gross margin to reach a record high. Attention should be paid to management's guidance on subsequent gross margin trends in this earnings report.

Summary

Overall, geopolitical conflicts have caused the previously strong memory chip uptrend to start losing momentum, with the market expecting Micron’s earnings report to shift focus back to fundamentals. Returning to Micron’s earnings report itself, this quarter’s figures are no longer crucial; the market is more focused on the sustainability of future performance, which requires management to provide a longer-term outlook.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (8)

to post a comment

11

47