The US-Iran peace talks present conflicting narratives! What’s next for oil prices?

Options Sir on Macro | Trump Pulls Another TACO, Is It Time to Bottom-Fish?

On March 9, Trump told CBS in an interview that the war with Iran was 'already very complete, almost over,' and indicated progress was much faster than his original timetable of four to five weeks.

The market immediately repriced based on a 'shortened duration of conflict': US stocks reversed from early losses to close higher, $Dow Jones Industrial Average (.DJI.US)$ up 0.5%, $S&P 500 Index (.SPX.US)$ up 0.83%, $Nasdaq Composite Index (.IXIC.US)$ up 1.38%;

however, Iran's Revolutionary Guard subsequently made clear that the decision of when the war ends 'is up to Iran' and stated that as long as attacks by the US and Israel do not stop, they will not allow 'a drop of oil' to leave the Middle East region.

1. Can yesterday’s market rebound be defined as a comprehensive 'buying opportunity signal'?

If we break down the fluctuations of the past few days, the geopolitical escalation itself is not scary; what is concerning is that it has pushed oil prices to a level that could hurt growth while also raising inflation.

The US has low dependence on Middle Eastern crude oil (domestic production accounts for 67%), resulting in minimal cost impact. The main transmission channel is through oil prices driving inflation → affecting Fed policy.For every 10% increase in oil prices, it is estimated to push up US CPI by approximately 0.2-0.3 percentage points.Therefore, Trump’s remark yesterday of 'ending soon' was essentially compressing the expectation of 'how long high oil prices will last,' rather than proving that the supply shock has ended.

Can this rebound be defined as a comprehensive 'buying opportunity signal'?The macroeconomic backdrop was already unstable, and this conflict simply disrupted an already fragile balance.

On March 6, data showed that the US non-farm payrolls for February declined by 92,000, with the unemployment rate rising to 4.4%. Over the past three months, average new job creation was only 6,000, significantly weaker than the previous trend. Meanwhile, average hourly earnings still grew 3.8% year-over-year. This set of data is troubling: growth is weakening, but wage stickiness remains.This suggests that even before the oil price shock arrived, the US economy was already showing signs of a prelude to stagflation — slower growth combined with stubbornly persistent inflation.

More importantly, although oil prices have fallen sharply from yesterday's highs, they have not returned to safe levels. On the morning of March 10, Brent crude briefly dropped to $88.05 per barrel before rebounding to $94.79, continuing to oscillate. Spot benchmarks in the Middle East, such as Murban and Dubai, remain clearly above $100, indicating that while the 'paper panic premium' has receded, 'ground-level supply tightness' has not entirely disappeared.

In other words, the market has merely adjusted the 'worst-case scenario' from total loss of control to 'it might not drag on too long,' without entering a state where risks have dissipated.What has been bought back are 'rate-sensitive, longer-duration' risk assets, not a full return to pro-cyclical positioning. This appears more like sentiment repair and risk discount recovery rather than the complete elimination of macro uncertainty.

Second, how will the midterm elections affect the Middle East conflict?

Trump's statement that 'the war will end soon' is aimed at reassuring both the markets and voters; while the midterm elections won't automatically bring peace, they will significantly raise the political threshold for the US to engage in a prolonged Middle East war.

First,Oil prices and gasoline pricesGasoline prices hold particular political sensitivity in the US, with voters considering the cost of living as one of their top pressures ahead of the November midterms; the latest Reuters/Ipsos poll shows that 67% of Americans expect gas prices to rise in the coming months, while only 29% support this war. For Trump, any spike in oil prices due to Middle East tensions would quickly translate into political costs reflected in voter turnout.

Second,MAGA voters favor 'strikes,' not 'getting bogged down'Interviews by Reuters with Trump supporters indicate that while they broadly accept airstrikes and naval bombardments, they generally oppose large-scale ground troop deployments, long-term military presence, and 'nation-building.'

Even among Republican voters, 42% said they would be less supportive of this operation if the war results in US military casualties in the Middle East, and 34% of Republicans said they would also be less supportive if US oil prices increase. In other words, Trump’s base doesn’t oppose 'showing strength,' but strongly resents turning 'America First' into 'America stuck in the Middle East again.'

Third,The Republican Party's own midterm election prospects are far from secureThe Republicans currently hold a narrow 218-to-214 advantage in the House of Representatives, and Democrats need to flip only a few seats to regain control of the House; moreover, the ruling party typically loses more seats during midterm elections. Meanwhile, Reuters also reports that Democrats are currently leading in fundraising in key House districts compared to Republican challengers. This means that if the war drags on, oil prices remain high, and casualties increase, the already slim midterm election prospects for Republicans will be further squeezed.

So,Trump's current stance is related to the midterm elections, but it's not 'he will definitely stop the war for the sake of the election'; rather, 'for the election, he prefers quick strikes followed by quick withdrawal, controlling oil prices, and avoiding deep entanglement of American troops.'。This is also why he simultaneously says the war may end soon while warning that if Iran blocks the Strait of Hormuz, the US will respond with greater force. This is not contradictory but a typical election-year strategy: maintaining external deterrence while avoiding giving the market and voters the impression that the US is entering a prolonged war of attrition.

3. Is it worth intervening now?

Yesterday's rebound addressed the issue of 'excessive panic pricing' but did not resolve the problem of 'ongoing macro constraints.' US labor data has already shown weakness.The February CPI will be released on March 11, PCE on March 13, and the Federal Reserve's interest rate decision meeting will take place on March 17-18. The market still expects the Fed to hold steady in March, with the first rate cut being pushed back to around July.In other words, if oil prices rise again, the market may no longer be able to count on immediate monetary policy support.

Going forward, the market will most likely evolve along three paths.

- First scenario, baseline case: The conflict does not end immediately but does not spiral further out of control.

The conflict does not end immediately but also does not escalate to an uncontrollable level. In terms of asset prices, oil remains range-bound between $90 and $100, with equities entering a volatile recovery phase but unlikely to return to the previous trend of smooth upward movement.

- Second scenario, risk case: The war drags on, and energy disruptions persist.

Iran continues to strengthen its blockade rhetoric, while US-Israeli actions escalate, pushing oil prices back above $100 and keeping them elevated. In that case, yesterday’s rebound would likely prove to be merely a sentiment-driven correction, after which the market shifts back into 'stagflation trading' – bonds under pressure, stocks under pressure, and gold and energy regaining favor.

– The third scenario, the optimistic case: a softening of political rhetoric and an acceleration in supply substitution, but it's too early to bet on this just yet.

Trump’s soothing rhetoric may eventually translate into policy execution, such as further easing of crude oil-related sanctions, coordinating strategic reserves, and promoting supply substitution, making the market believe that 'oil will eventually be transported.' There are indeed signs pointing in this direction currently, with the US assessing the release of emergency crude oil reserves, and the G7 indicating readiness to take necessary actions if oil prices spike.

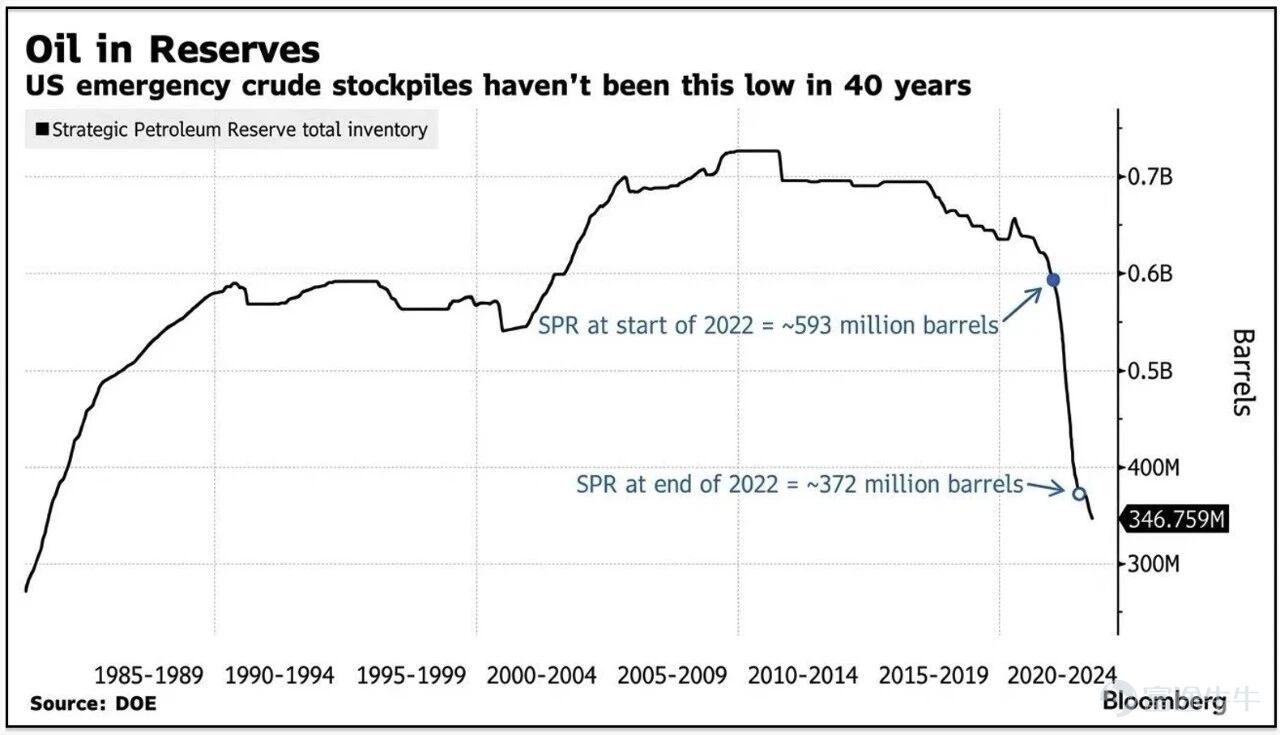

However, these measures are still at the 'expectation management' stage, far from truly altering the supply-demand landscape. After the Russia-Ukraine conflict in 2022 and the release of oil reserves, the reserves dropped to a low of about 350 million barrels, marking the most depleted period since the early 1980s.According to the US Department of Energy, at least 70% of the reserve infrastructure and equipment has 'exceeded its service life,' meaning the time required could far exceed expectations.

For traders, the most crucial indicator to watch now is not the stock index itself, but oil prices. It may be worth adjusting positions from being overly defensive to neutral-bullish, but confirmation of a new major uptrend still needs to wait.

If there is a softening of Iran's stance and CPI/PCE does not significantly exceed expectations, this rebound has the potential to upgrade from 'valuation recovery' to 'trend recovery.'The market focus might return to its original trajectory, with the Optical Module Conference and GTC conference approaching, and many positive catalysts for the technology sector, where momentum remains strong in these leading sectors.

Avoid sectors most vulnerable to profit compression due to high oil prices, such as airlines, at least for now. Even if these sectors see short-term rebounds, they are more likely to be trading opportunities and should not be considered the main focus of this event-driven rally.

1. If clients are currently fully or lightly positioned and want to participate in the rebound,

You may considerBull call spread strategyIn terms of approach, for example, $SPDR S&P 500 ETF (SPY.US)$ / $Invesco QQQ Trust (QQQ.US)$ , buy an at-the-money or slightly in-the-money call, while simultaneously selling a call with a higher strike price above, to reduce the cost.

The reason is firstly, the essence of this rebound istail risk unwinding, not a sudden upward revision in profit expectations; secondly, $CBOE Volatility S&P 500 Index (.VIX.US)$ although it has retreated from 25.5 to 23, the absolute level is still not low, and directly buying naked calls can easily incur time value decay; thirdly, if oil prices continue to fall subsequently, growth stocks will remain elastic, but if there are further fluctuations in the Middle East, the drawdown of the spread structure will be more controllable.

(The design images displayed on screen are for illustrative purposes only and do not constitute any investment advice or guarantees; market conditions fluctuate frequently, and the option prices shown do not represent real-world values.)

2. If the client already holds a heavy long position in US stocks, especially in large-cap or technology stocks,

consider applying a collar to the current long position by purchasing protective puts below and selling covered calls above.

The reason is simple: yesterday's market has already demonstrated that as long as the expectation of 'war duration' is revised downward, equities will immediately recover. However, it is also a reminder that risks have not completely dissipated, considering Iran's strong response, the risks in the Strait of Hormuz, and the secondary impact of high oil prices on financial conditions.For profitable long positions, the optimal solution now is not to continue running naked, but to stay in the game in a way that controls drawdowns.

Take $NVIDIA (NVDA.US)$ For example, NVDA was one of the main forces driving yesterday's rebound. Looking ahead, there is potential event-driven momentum from the GTC conference.

(The design images displayed on screen are for illustrative purposes only and do not constitute any investment advice or guarantees; market conditions fluctuate frequently, and the option prices shown do not represent real-world values.)

3. If clients have previously bet correctly on energy, oil and gas, or gold, they should now see significant unrealized gains in their accounts.

Energy positions should now be the top priority for handling. Yesterday’s market reversal essentially pulled back the pricing narrative that 'oil prices are permanently stepping up.' This kind of positioning focuses more onlocking in profits.The core variable mirroring yesterday's market reversal was oil prices: On Monday, Brent approached $119.50 during trading, but by Tuesday it had been driven back down to the $91-93 range. This kind of volatility indicates that the odds for energy long positions have shifted from 'crowded crisis trades' to 'headline trades that can easily be hit by a single statement.'

From a practical standpoint, there are two useful strategies: First, sell covered calls on spot or stock long positions, voluntarily giving up some upside potential in exchange for certainty. Second, buy protective puts to lock in sudden drawdowns beforehand, with $United States Oil Fund LP (USO.US)$ as an example:

(The design images displayed on screen are for illustrative purposes only and do not constitute any investment advice or guarantees; market conditions fluctuate frequently, and the option prices shown do not represent real-world values.)

Finally, here's a small perk for fellow investors—welcome to claim it!Options Beginner Pack

This event is exclusively for invited HK users, click to learn moreDetailed event rules >>

Futu's simulated trading challenge is now open for registration! Zero cost, zero risk, and you could win stock cash vouchers!

Disclaimer

This content does not constitute any offer, solicitation, recommendation, opinion, or guarantee of any securities, financial products, or tools. The risk of loss in buying and selling options can be substantial. In some cases, your losses may exceed the initial margin amount deposited. Even if you set contingent orders, such as 'stop-loss' or 'limit' orders, these may not necessarily prevent losses. Market conditions may make these orders unexecutable. You might be required to deposit additional margin within a short period. If you fail to provide the required amount within the specified time, your open positions may be liquidated. However, you will still be responsible for any account deficit arising from this. Therefore, before trading, you should study and understand options and carefully consider whether such trading suits you based on your financial situation and investment objectives. If you trade options, you should be familiar with the procedures upon exercising options and at expiration, as well as your rights and obligations when exercising options and at expiration.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (9)

to post a comment

49

45