Focus on March 10! The US will host a roundtable meeting for robotics manufacturers. How should investors seize the investment opportunity?

According to Semafor,The U.S. Department of Commerce will hold a roundtable meeting for American robotics manufacturers on March 10,with the theme of 'Identifying key supply chain and policy challenges impacting U.S. robotics manufacturing and deployment.'

The market views this as essentially the last hearing before the introduction of the 'Robotics version of the CHIPS Act,' with the core objective being to promote the return of the robotics supply chain to the U.S. through subsidies and standard-setting, focusing on key areas such asactuators and rare earth permanent magnet motorssuch as core components, rebuilding the hardware's underlying dominance.

So, how should we seize the investment opportunities amid this upcoming industrial chain reshaping?The investment logic running through the entire robotics industry can be framed using a highly penetrating framework:“Components as the core, complete machines as the carrier, and embodied intelligence as the long-term barrier.”。Using this as an anchor, this policy shift will profoundly affect the following three key sectors.

1. Components as the Core: Seeking ‘water carriers’ in underlying hardware and strategic resources.

The U.S. has clear advantages in software algorithms and foundational computing power, but its domestic production capacity is relatively weak in the high cost-performance manufacturing of precision components. This meeting signals that future policy subsidies will precisely support domestic hardware manufacturing and upstream key materials sectors.

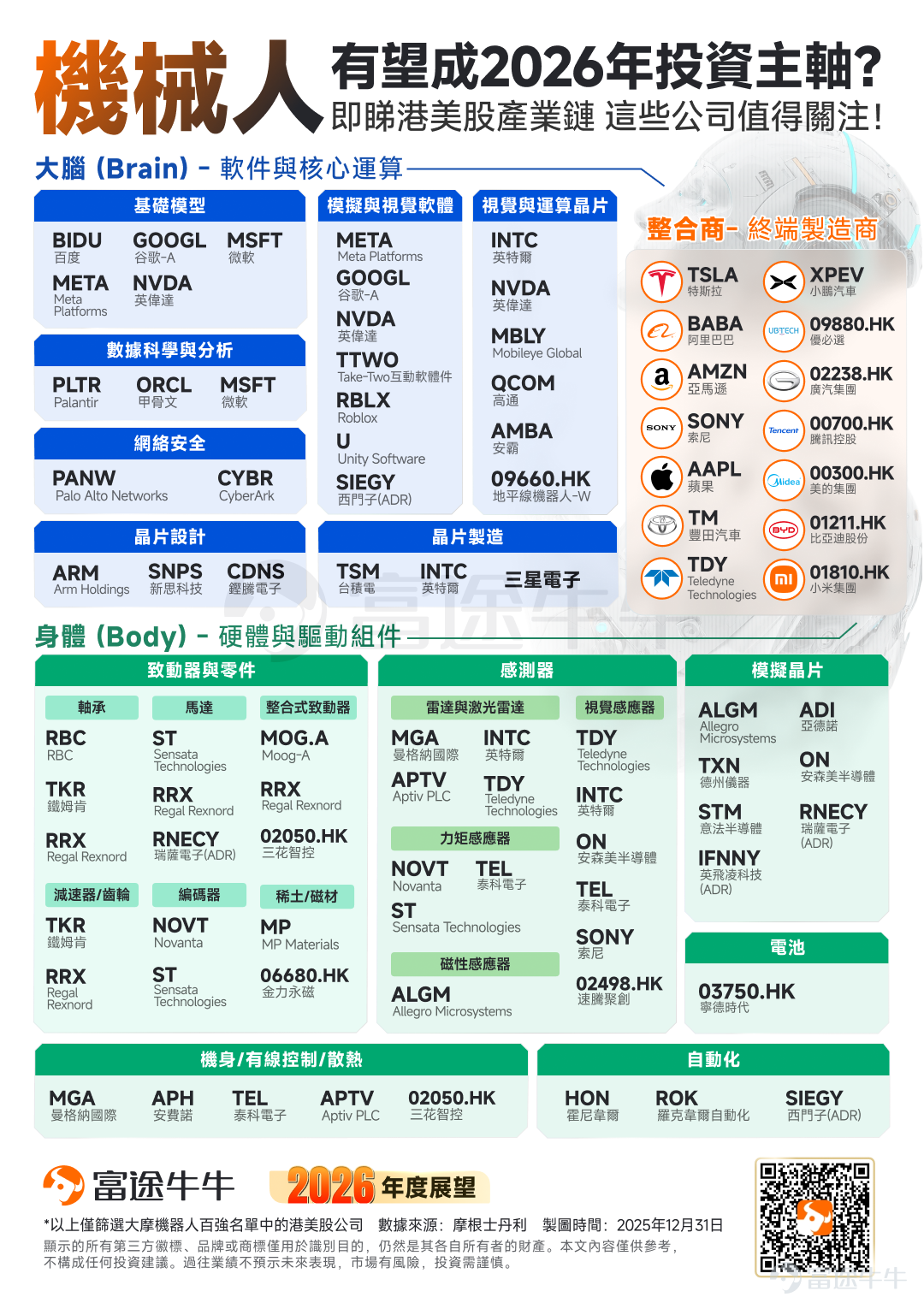

At the beginning of the year,The article '2026 Outlook | US-China Rivalry Enters New Arena! Robotics Industry May Face 'Commercialization Test'; Which Core Companies Did Morgan Stanley Highlight?'As previously noted in an article, Morgan Stanley pointed out that as the industry approaches mass production, value creation and investment timing across all segments are being reassessed. Currently, value creation is highly concentrated in upstream core components, with relevant supply chains mapped out as follows:

![According to Semafor reports,The US Department of Commerce will convene a roundtable meeting for American robotics manufacturers on March 10,with the theme of 'Identifying key supply chain and policy challenges impacting US robotics manufacturing and deployment.' The market views this as essentially the last hearing before the introduction of the 'Robotics version of the CHIPS Act,' with the core objective being to promote the reshoring of the robotics supply chain through subsidies and standard-setting, focusing on overcomingactuators, rare earth permanent magnet motorsand other core component bottlenecks, to reshape control over the hardware foundation. So, in the face of this upcoming industrial chain reshaping, how should we grasp the investment opportunities within?Spanning the entire robotics industry's investment logic, we can apply a highly penetrating framework:"Core components, complete machines as carriers, and embodied intelligence as long-term barriers"。Using this as the anchor point, this policy shift will profoundly impact the following three major sectors. 1. Core Components: Seeking the 'water sellers' of underlying hardware and strategic resources The United States has a clear advantage in software algorithms and underlying computing power, but its domestic production capacity for high cost-performance precision components is relatively weak. This meeting signifies that future policy subsidies will be precisely directed towards local hardware manufacturing and upstream key materials fields. At the beginning of the year,[Share Link: The article '2026 Outlook | US-China Rivalry Enters New Arena! Robotics Industry May Face 'Commercialization Test'; Which Core Companies Did Morgan Stanley Highlight?']As mentioned in a previous article, Morgan Stanley believes that as the industry approaches mass production, each stage...](https://nnqimage.futunn.com/sns_client_feed/900080/20260306/web-1772789396729-kjqv6oonBk.png/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

From the perspective of the supply chain structure, we can focus on the following three major directions:

1. Rare earths andMagnetic materials (the heart of motors and the foundation of strategic resources):High-performance servo motors are the power source for robot joints, while rare earth permanent magnet materials such as neodymium-iron-boron are at the core of these motors. In an AI-driven era with surging electricity demands and physical robots acting as dual catalysts in a supercycle, resource attributes are especially critical.

Local cornerstone: $MP Materials (MP.US)$ As the largest rare earth producer in the U.S., it is an indispensable foundational asset in rebuilding a secure and controllable North American motor supply chain.

Global perspective: Although policies promote localization, within global production capacity, $JLMAG (06680.HK)$ remains one of the most competitive magnetic material suppliers listed on the Hong Kong Stock Exchange.

2. Actuators and core components (local hardware pioneers bridging the cost gap):Actuators serve as the 'muscles' of robots and represent one of the highest cost components in the BOM (Bill of Materials). Policy support can potentially help established U.S. hardware companies achieve significant cost reductions through scaled production.

Integrated actuators and motors: $Moog-A (MOG.A.US)$ is a traditional American aerospace-grade actuator giant with extremely high technological barriers; $Regal Rexnord (RRX.US)$ and $Sensata Technologies (ST.US)$ plays a key role in the integration of motors and actuators. The market currently heavily relies on companies like $SANHUA (02050.HK)$ This is precisely the area where U.S. policy is eager to support domestic alternatives.

Reducers, gears, and bearings:responsible for precise transmission. $The Timken (TKR.US)$ and $RBC Bearings (RBC.US)$ has deep expertise in high-precision bearings and gears.

Encoders:responsible for accurately measuring position and speed, $Novanta (NOVT.US)$ a core U.S. stock in the precision field.

3. Sensors and analog chips (the 'neural network' through which robots perceive the world):Robots require sharp tactile and visual capabilities to adapt to complex environments.

Multi-dimensional sensor arrays: Traditional automotive Tier 1 suppliers such as $Aptiv PLC (APTV.US)$ 、 $Magna International (MGA.US)$ have a strong presence in radar deployment; $Teledyne Technologies (TDY.US)$ specialize in vision sensors, and $Novanta (NOVT.US)$ occupy a key niche in torque sensors.

Analog chip giant: $Texas Instruments (TXN.US)$ 、 $Analog Devices (ADI.US)$ 、 $ON Semiconductor (ON.US)$and$STMicroelectronics (STM.US)$ will directly benefit from the explosive growth in the number of robot sensors.

II. Whole machine as a carrier: Automation deployment and subsidies to address labor shortages

If relevant legislation is passed, the policy goals aim not only at 'manufacturability' but also at 'wide adoption.' To alleviate long-term labor shortages in U.S. manufacturing and logistics industries, companies purchasing domestic robots for production line automation are expected to receive substantial equipment investment subsidies.

As early as December of last yearTrump Administration 'Targets' Robotics Sector! Related Stocks Rally Collectively, Here's the Hong Kong and US Stock List to KeepAn article mentioned that the U.S. Commerce Secretary Lutnick has recently been frequently meeting with CEOs in the robotics industry, showing ‘full support’ (All in) for accelerating the development of this sector. It was also noted that the Trump administration is considering issuing an executive order on robotics by 2026. Niuniu also compiled a list of robotics-related stocks across various fields, detailed below:

![According to Semafor reports,The US Department of Commerce will convene a roundtable meeting for American robotics manufacturers on March 10,with the theme of 'Identifying key supply chain and policy challenges impacting US robotics manufacturing and deployment.' The market views this as essentially the last hearing before the introduction of the 'Robotics version of the CHIPS Act,' with the core objective being to promote the reshoring of the robotics supply chain through subsidies and standard-setting, focusing on overcomingactuators, rare earth permanent magnet motorsand other core component bottlenecks, to reshape control over the hardware foundation. So, in the face of this upcoming industrial chain reshaping, how should we grasp the investment opportunities within?Spanning the entire robotics industry's investment logic, we can apply a highly penetrating framework:"Core components, complete machines as carriers, and embodied intelligence as long-term barriers"。Using this as the anchor point, this policy shift will profoundly impact the following three major sectors. 1. Core Components: Seeking the 'water sellers' of underlying hardware and strategic resources The United States has a clear advantage in software algorithms and underlying computing power, but its domestic production capacity for high cost-performance precision components is relatively weak. This meeting signifies that future policy subsidies will be precisely directed towards local hardware manufacturing and upstream key materials fields. At the beginning of the year,[Share Link: The article '2026 Outlook | US-China Rivalry Enters New Arena! Robotics Industry May Face 'Commercialization Test'; Which Core Companies Did Morgan Stanley Highlight?']As mentioned in a previous article, Morgan Stanley believes that as the industry approaches mass production, each stage...](https://nnqimage.futunn.com/sns_client_feed/900080/20260306/web-1772789397486-E2R2f5e5A9.png/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

From the perspective of industrial application end-use scenarios, investment opportunities will fully emerge in the following sectors:

1. Integrators and Industrial Robots (the 'Super Foreman' of Local Manufacturing):

Pioneers in the commercialization of humanoid robots: $Tesla (TSLA.US)$ Not only a new energy vehicle giant but also a highly representative terminal manufacturer and leader in industrial robotics. With policy subsidies, it would greatly alleviate the cost pressures during the early mass production phase of Optimus.

Industrial hardware giant: $Honeywell (HON.US)$ Has deep involvement in industrial robots and underlying automation control; its subsidiary Universal Robots $Teradyne (TER.US)$ is also a hardcore target not to be overlooked.

2. Robotics Automation ('Infrastructure Enthusiast' Empowering Traditional Production Lines):

Absolute Leader in Automation: $Rockwell Automation (ROK.US)$ Spanning both automation and robotics automation fields, it will directly benefit from the enormous demand for production line upgrades in North America.

Machine Vision and Data Acquisition: $Cognex (CGNX.US)$ and $Zebra Technologies (ZBRA.US)$ Will play a key role in quality control and logistics tracking within automated production lines.

3. Logistics Robots (A Powerful Tool to Address U.S. Supply Chain Bottlenecks):

Driving Force Behind E-commerce Giants: $Amazon (AMZN.US)$ As a top-tier end-to-end integrator, its massive logistics system serves as the largest application testing ground for logistics robots.

Rising Star in Warehouse Automation: $Symbotic (SYM.US)$ Specializing in last-mile delivery $Serve Robotics (SERV.US)$ , its business model perfectly aligns with the policy goal of 'addressing supply chain logistics challenges'.

4. Defense and Medical Robotics (High Value-Added and Policy-Certainty Sectors):

National Defense Security: Gathers $Lockheed Martin (LMT.US)$ 、 $AeroVironment (AVAV.US)$as well as spanning sensors and defense $Teledyne Technologies (TDY.US)$ and other military giants.

Precision Medicine:以$Intuitive Surgical (ISRG.US)$ 、 $Medtronic (MDT.US)$ a sector represented by companies with extremely high gross margins and long-term inelastic demand.

III. Embodied Intelligence as a Long-Term Barrier: Strengthening the 'Brain' Moat, Controlling Ecosystem Definition Rights

If hardware reshoring is aimed at addressing the 'urgent needs' of U.S. manufacturing, ensuring dominance over the integrated hardware-software ecosystem represents the strategic core for the U.S. to maintain long-term technological hegemony. In the 'brain (software and core computing)' domain of robotics, U.S. companies currently hold a dominant position, which also constitutes the deepest and hardest-to-surpass long-term barrier in the era of embodied intelligence.

Combining the above industry chain map, we can see that investment opportunities in the 'brain' of robots mainly focus on three major computing and software infrastructures:

1. Vision and computing chips: The cornerstone for embodied AI's computational power and design For a robot to understand the three-dimensional world and make decisions, it relies heavily on powerful edge and cloud computing capabilities.

The dominant forces in computing power and vision: $NVIDIA (NVDA.US)$ Undoubtedly at the core, providing not only powerful computing chips but also dominating the field of visual computing. Meanwhile, $Qualcomm (QCOM.US)$ 、 $Intel (INTC.US)$ and companies focused on edge vision $Mobileye Global (MBLY.US)$ and $Ambarella (AMBA.US)$ together build a rich ecosystem for edge computing power.

The 'enablers' in chip design and manufacturing: The birth of these top-tier computing chips is entirely dependent on $Arm Holdings (ARM.US)$ architecture licensing, $Synopsys (SNPS.US)$ and $Cadence Design Systems (CDNS.US)$ EDA design software, as well as $Taiwan Semiconductor (TSM.US)$ advanced manufacturing processes. These are the most fundamental 'enablers' supporting the explosion of computing power in robotics.

2. Simulation and Visual Software: The 'Virtual Training Ground' for Robotic Evolution Embodied intelligence cannot evolve solely through trial and error in the real world; highly realistic physics simulations and virtual training environments are key to accelerating algorithm iteration.

Underlying foundational models from tech giants: $Microsoft (MSFT.US)$ 、 $Alphabet-C (GOOG.US)$ and $Meta Platforms (META.US)$ They not only excel in data analysis but also serve as the core force driving multimodal visual software and foundational models for robotics.

Dimensionality reduction impact of physics engines and interactive software: Unity、Robloxand Take-Two These companies, traditionally known for gaming and interactive software, have quietly become essential infrastructure for training robots, thanks to their deep expertise in building hyper-realistic 3D physics worlds, collision testing, and synthetic data generation.

3. Data Science and Cybersecurity: The Invisible Defense Line in Scalable Deployments As thousands of robots enter factories, logistics centers, and even homes, they will become extremely dense mobile data collection endpoints.

Data Analysis: How to efficiently process and apply these massive amounts of real-world data $Palantir (PLTR.US)$ and $Oracle (ORCL.US)$ Data science giants like [company names] will see new business growth opportunities.

Security and Compliance Baseline: The consequences of robots being hacked or data breaches are unimaginable. Therefore, as policies promote localized deployments, $Palo Alto Networks (PANW.US)$ Leading cybersecurity companies will inevitably become the standard configuration for ensuring the security of robotic networks and endpoints.

Summary

Overall, for investors, rather than blindly guessing which complete machine brand will eventually dominate the market in the early stages of the industry, it is better to focus on 'Core components, complete machines as carriers, and embodied intelligence as a long-term competitive barrier.'Common knowledge in the industry.

In the short term, potential policy subsidies are expected to directly improve the income statements of local hardware alternatives and upstream resource suppliers; in the long term, companies that control core computing power and software training ecosystems remain the most certain segment in the entire industrial chain.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

54

106