The United States and Iran are sticking to their respective positions—can peace talks proceed smooth

Escalation of US-Iran tensions and its impact

I. Event Development

Starting February 28, 2026, the United States and Israel launched large-scale airstrikes against Iran, targeting military installations, missile bases, and regime targets, directly resulting in the death of Iran's Supreme Leader Khamenei. Two days prior, US-Iran delegations held their third round of nuclear negotiations in Switzerland, but Iran refused to make concessions on key issues such as limiting regional proxy armed groups, prompting dissatisfaction from Trump, who deemed the talks unsuccessful. Iran retaliated by targeting US Air Force bases in the Middle East and Israel, among other locations, with the conflict continuing into its third day. Trump stated that the operation might last 4-5 weeks, aiming to push for regime change in Iran, and warned there could be additional American casualties. This situation appears to exceed previous limited strikes (e.g., the 12-day war in June 2025) and has evolved into a direct attempt at regime change, significantly raising regional risks, including potential disruptions to shipping through the Strait of Hormuz.

On March 1, Gulf nations partially closed their airspace and canceled flights, slowing traffic through the Strait of Hormuz. Some tankers paused operations or rerouted, but traffic was not completely halted. Houthi forces resumed attacks in the Red Sea, increasing multi-front proxy risks. The OPEC+ meeting concluded on Sunday, with the group agreeing in principle to increase production in April. They will add 206,000 barrels per day, reducing OPEC's total spare capacity to below 4 million barrels per day.

II. Market Reaction (as of writing)

Crude Oil: The increase in Brent crude oil and WTI crude oil futures narrowed to within 4.5%, after jumping 13% earlier in the trading session. Market statistics show that in previous military strikes, the average one-day rise in crude oil remained flat, with an average drop of about 2% in one month and an average gain of around 3% in three months. During the conflict period, Iran’s exports will be restricted, and depending on the actions of Iran's leadership (export restrictions similar to those seen in Venezuela could occur), these restrictions may last longer. Whether the spike in oil prices can be sustained and how high it can go will depend on the actual and anticipated impact on global oil supply. The longer-term fundamental impact will hinge on several factors, including Iran's new leader and the choices made by the rest of the leadership in the coming days.

US Stock Market:S&P 500 and Nasdaq 100 index futures trimmed losses to less than 0.5%, after falling more than 1% earlier. Market statistics indicate that in previous military strikes, the S&P 500's average one-day change was flat, with an average rise of about 4% in one month and an average gain of around 6% in three months.

Cryptocurrencies:Bitcoin staged a V-shaped reversal over the weekend, rebounding above $68,000, with a gain of 2.21%.

Gold:Risk aversion sentiment drove gold higher, with spot gold rising 2% to $5,353.90 per ounce at one point.

Interest rate:Risk premium increased, leading to curve steepening, with the US 10-year Treasury yield rising by 4 basis points.

Forex:The US dollar opened 0.42% higher at 98.1 but later pared gains, falling back below 98. Escalating tensions with Iran have provided fresh tailwinds for the recent movements in the US dollar by pushing up energy prices (for every 10% increase in oil prices, the dollar gains a corresponding boost of 0.5-1%) and intensifying haven demand. Prior to this geopolitical conflict, strong data starting from the January nonfarm payrolls report and the Federal Reserve’s hawkish January meeting minutes had already helped the dollar rebound from its lows. The US Supreme Court’s ruling on the International Emergency Economic Powers Act (IEEPA) can also be seen as evidence of the functioning of the US system of checks and balances, which might lower the risk premium on the dollar, although authorities' responses and fiscal impacts are also worth monitoring. Apart from developments in the Middle East, key macroeconomic data to watch this week include the ISM survey, January retail sales figures, and the latest jobs report released on Friday.

III. Impact on the Macroeconomy

1. On Gulf countries

Oil price dynamics remain a core factor influencing the economic outlook of the Gulf Cooperation Council (GCC), not only due to their contribution to GDP but also because of their crucial role in fiscal and balance of payments for each country. The sensitivity to price shocks is significant: every $10 increase in crude oil prices typically improves fiscal balances and current account balances by more than 2% and 3% of GDP, respectively. However, if production facilities are damaged or crude oil cannot be freely traded via the Strait of Hormuz, conventional sensitivity analysis will no longer apply.

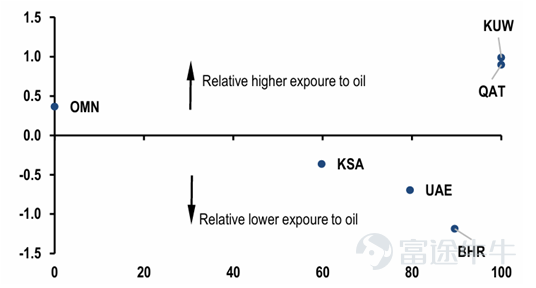

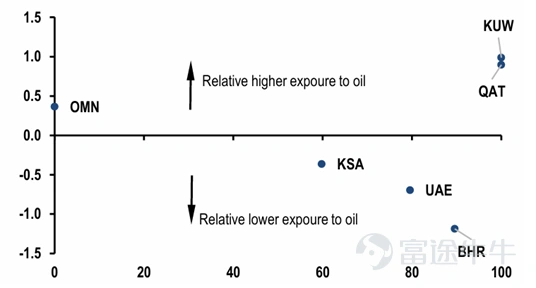

The vertical axis represents the Z-value*, and the horizontal axis indicates the percentage dependence on oil and gas trade through the Strait of Hormuz

Notably, Oman is the only Gulf country that would not be directly affected by a blockade of the Strait of Hormuz, as all its export terminals are located on the eastern side of the strait. In contrast, Bahrain, Kuwait, and Qatar rely entirely on this strait for their oil and gas exports and have no alternative routes (except for Bahrain's exports to Saudi Arabia). Saudi Arabia and the UAE can divert some oil and gas transportation through pipelines: Saudi Arabia transports via the East-West pipeline to the Red Sea, while the UAE uses pipelines to its east coast—but spare capacity is limited, so a blockade of the strait would still cause significant disruptions. It is also worth noting that Iran’s oil fields and export terminals are located on the western side of the strait, meaning its crude oil exports also depend on this passage.

The impact on liquefied natural gas (LNG) will be even more severe: Qatar and the UAE have no alternative routes for their exports, while Oman can continue trading. A disruption in non-oil and gas trade will further affect the UAE and Bahrain: as a critical global logistics hub, the UAE’s re-exports account for about 37% of GDP; Bahrain’s key export revenue-generating industries, primarily aluminum-based, would also suffer significantly.

In the short term, non-oil activities face significant downside risks, stemming from potential prolonged business interruptions and weak business and consumer confidence. Non-oil growth in the Gulf region has been strong in recent years; we estimate a growth rate of 4.3% for 2025, led by the UAE (over 5%), followed closely by Saudi Arabia (over 4%). Our baseline forecast for 2026 was 3.5%, with the UAE remaining robust, but growing concerns in Saudi Arabia due to ongoing fiscal consolidation. Reported attacks in Dubai and Abu Dhabi could weigh on economic activity and may lead to a decline in tourism, one of the region’s key growth engines. The real estate market could also be affected, with reduced inflows of expatriates and asset valuations adjusted if the market demands higher risk premiums for regional stability.

2. Regarding Asia

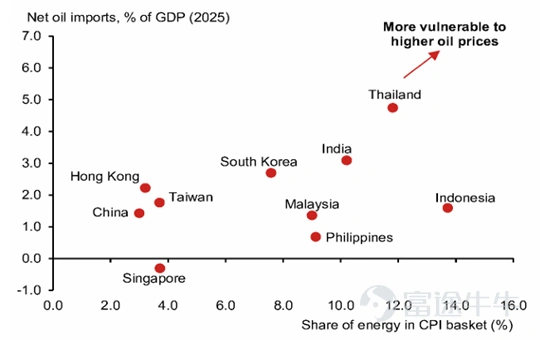

The impact on Asia’s trade balance is negative, but local fuel prices are often regulated, keeping growth and inflation impacts manageable. The main effect is an increase in import bills, followed by rising fiscal burdens. Thailand, India, South Korea, and the Philippines are highly dependent on oil imports, while Malaysia, as a net energy exporter, benefits relatively. Asian governments will use fiscal measures as the first line of defense, employing price controls, increased subsidies, fuel consumption tax cuts, and reductions in crude oil and refined product import tariffs to protect consumers. Rising oil prices strengthen the case for central banks to stay on hold, but short-term supply shocks are insufficient to trigger rate hikes, as underlying inflation remains mild. If oil prices continue to rise, the impact on Asian stock markets would be negative; however, if the conflict ends quickly, the negative effects may be short-lived.

Percentage of net oil price imports and energy in CPI among Asian countries

IV. The Impact on Credit

1. Gulf countries

The developments over the last weekend may put pressure on the GCC credit market. During previous periods of heightened tensions in the Middle East, regional assets were minimally affected as markets anticipated that conflicts would remain contained. However, the current situation is different—this is the first time in years that missiles and drones have directly struck the territory of a GCC member state. For instance, DP World has suspended operations at the Jebel Ali Port, with some hotel facilities and airports also damaged in the attacks. These events pose a substantial shock to a region long regarded as stable and insulated from global volatility. Previously, GCC credits benefited from strong sovereign balance sheets, high investment-grade ratings, and steady demand from Asian markets—supported by tightening supply in the Asian credit market. This attack is shaking the region's longstanding status as a safe haven, which had never been truly challenged during prior escalations.

Within the GCC region, UAE credit may face greater pressure. Intensive media coverage of local attacks has amplified investor concerns. Technical pressures should not be overlooked: JPMorgan’s decision in late February 2026 to remove the UAE from the EMBI index could lead to similar dynamics as observed when Qatar was excluded in 2025, resulting in benchmark investors being forced to reduce holdings and widen spreads. The current conflict will likely amplify this effect. Some investors may choose to reduce GCC exposure to lock in year-to-date gains—from this perspective, Qatar (+1.7%) and Saudi Arabia (+1.3%) are outperforming other member states. We also note that sovereign bonds may underperform corporate bonds in the short term, mainly due to liquidity considerations (investors tend to sell bonds that are easier to repurchase after volatility subsides), except for entities directly impacted by the attacks. Additionally, given that investors will continue to seek investment-grade credit, some capital may rotate into the Asian market.

The coming weeks will test whether GCC credit can regain its resilience. If not, this event could trigger a lasting repricing of regional risk.

2. Asia

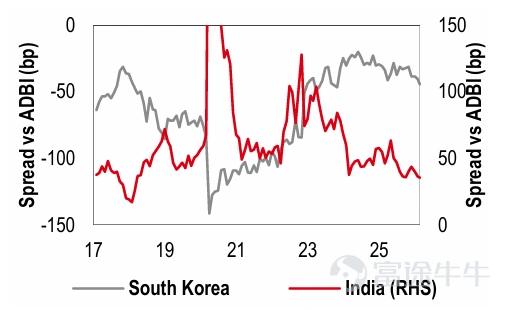

In the Asian credit market, the three major markets of India, China, and South Korea heavily rely on crude oil imports from the Middle East and are thus vulnerable to potential supply shocks. However, the impact on their dollar-denominated bonds varies. On one hand, Indian credit trades at relatively high levels compared to historical standards, leaving little spread buffer to protect investors from risks. In contrast, China and South Korea benefit from lower beta and wider spreads relative to broader Asian credit.

The spread buffer for Indian credit bonds is smaller than that for Korean credit bonds

Moreover, growing concerns about growth prospects naturally favor defensive sectors such as telecommunications, utilities, and non-cyclical consumer goods, especially when there is little spread premium for initially taking on cyclical risk. Fundamentally, banks should remain relatively insulated from shocks as long as loan losses do not rise significantly. However, since bank bonds are typically more liquid than non-financial corporate bonds, they are more likely to be sold during portfolio de-risking, potentially causing the sector to lag in the short term.

Lagging performers may include travel and leisure companies such as airlines, as well as discretionary consumer goods firms. Rising oil prices will squeeze these companies' profit margins in two ways: directly increasing costs or indirectly weakening consumer purchasing power. The wider the spread widens, the greater the appeal of directly increasing beta (via cash bonds or CDS indices) rather than focusing on relative value across curves, sectors, or issuers. Even so, the speed of spread retracement will depend on how quickly oil supplies can be restored and whether the market demands a structural risk premium to offset lingering geopolitical and credit risks.

V. Subsequent Scenario Analysis

Barclays provides three scenario analyses.

1. Larger-scale action without ground invasion: Military operations are broader than those in the summer of 2025 but stop short of ground incursions. Fighting is mainly confined to Iran (and Israel), with Iran opting for measured retaliation aimed at limiting civilian casualties among neighboring countries. Tehran also increases pressure on the Strait of Hormuz through harassment and disruptions rather than an official closure. Tensions persist for several weeks before a negotiated cessation of hostilities allows both sides to claim partial strategic success. Under this scenario, the risk premium in financial markets and energy prices is likely to persist longer than it did after the summer of 2025.

2. Quick de-escalation and return to negotiations: This scenario roughly echoes the pattern of summer 2025, but given the scale and momentum observed in the first two days of fighting, it is the least likely of the three. Military actions focus on nuclear facilities, senior regime figures, and key security assets. After several days of high tension, Iran seeks de-escalation through mediation by China, Europe, or Gulf Cooperation Council countries, and returns to the negotiating table. If both sides judge that further escalation would incur severe economic costs with limited military benefits, a relatively rapid normalization may follow.

3. Further escalation with regional spillover: Iran receives stronger support from countries like China and Russia and expands the conflict by targeting nations hosting US military assets. Tehran takes concrete steps to effectively close the Strait of Hormuz using mines, drones, and anti-ship missiles. Although Iran's conventional capabilities have weakened in recent years, several regionally embedded proxies, including Hezbollah, the Houthis, and pro-Iran Iraqi militias, remain active. Their involvement would significantly expand the conflict and substantially increase the risk of broader confrontation across the Middle East.

VI. Main Focus

Duration of the conflict, shipping through the Strait of Hormuz, and oil supply conditions.

Data source: Franklin Templeton, sell-side reports

Disclaimer

China Life Franklin Asset Management Co., Ltd. (hereinafter referred to as "the Company") is licensed by the Hong Kong Securities and Futures Commission (hereinafter referred to as "SFC") under Section 116 of the Securities and Futures Ordinance to engage in Type 1, Type 4, and Type 9 regulated activities.

Persons residing in jurisdictions where applicable laws or regulations do not permit the distribution or issuance of this document are not the intended recipients. If you are not the intended recipient, please do not continue reading this document and should destroy it immediately.

This document is for reference only and does not constitute an offer or solicitation to buy or sell any securities or invest in other investment products in any jurisdiction. It must be kept strictly confidential and delivered solely to the recipient. Unless with prior written consent from our company, this document shall not be used, reprinted, copied, or distributed in whole or in part. This document has not been approved by the Securities and Futures Commission. If this document is distributed by a third party outside our company, our company shall not be responsible for any actions taken by the recipient or such third party.

None of the contents of this document constitutes investment, legal, or other advice, and investors should not rely on it when making investment or other decisions. Prospective investors should seek independent advice regarding the suitability or other aspects of individual investments based on their own investment objectives and personal financial situations. Our company, its directors, officers, employees, or other clients may from time to time hold long or short positions in the securities or other financial instruments mentioned in this document, buy or sell such securities, or invest in such other financial instruments, and our company, its directors, officers, employees, or other clients may have conflicts of interest concerning the securities or other financial instruments mentioned herein. Our company shall not be liable for any loss and/or damage arising from the use of this document and any investment decision made by investors based on such materials. The opinions expressed in this document reflect our company's views at the time of publication and may be changed without notice.

Our company will make every effort to provide accurate and timely information. Nevertheless, our company does not guarantee the accuracy, timeliness, completeness, usefulness, or any other aspect of the information contained in this document, nor shall it assume responsibility for any such content. The value of investments can go up as well as down and may be affected by market fluctuations. Past performance or any estimates or forecasts are not indicative of future results. There is no guarantee that the use of any strategy described in this document will lead to the achievement of the specified objectives. Although the information in this document is obtained from sources believed to be reliable, our company, its directors, officers, and employees do not warrant the accuracy or completeness of such information. All charts and results (if any) are for illustrative purposes only and do not represent actual or future performance of any investment. While the account fund manager will make reasonable efforts to minimize investment risks, the value of investments may fluctuate, potentially resulting in losses, and in the worst-case scenario, the entire investment amount could be lost. Investment returns not denominated in Hong Kong dollars or not benchmarked in Hong Kong dollars may be subject to risks due to exchange rate fluctuations. Before making any investment, the recipient should refer to the relevant offering documents (if any) and financial reports (if any) for further details.

Our company reserves the right to take legal action.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

1

4