Mediators have proposed a 10-day ceasefire—will the U.S. and Iran enter a 'cooling-off period'?

Options Sir Macro View | Escalation of risks in the Strait of Hormuz, what’s next and what to do now?

1. After a sharp drop in US stocks last night, they rebounded again. Is this a real stabilization?

On March 3, the three major US stock indexes plunged across the board at one point, causing a sharp rise in market panic. $CBOE Volatility S&P 500 Index (.VIX.US)$ Intraday surge exceeded 30% at one point.

However, it rebounded later and eventually $Dow Jones Industrial Average (.DJI.US)$ Finally closed down 0.83%; $Nasdaq Composite Index (.IXIC.US)$ Dropped 1.02%; $S&P 500 Index (.SPX.US)$ Fell 0.94%. The main reason was that Trump's announcement of strong measures by the US to ensure the safety of energy transportation in the Middle East calmed the market, and after the statement was released, international oil prices fell accordingly.

1) Tail risk becomes 'tradable'

The intensity of this conflict far exceeded market expectations, leading the market to worry that the conflict might escalate into a long-term war of attrition rather than a short-term limited strike.

The joint US-Israeli action directly targeted the core of the Iranian regime. The attacks that killed Khamenei and several senior executives caused the situation to rapidly shift from a 'controllable conflict' towards an 'uncontrollable retaliation' path dependence; Iran’s de facto blockade of the Strait of Hormuz effectively placed the world’s most sensitive energy channel on the table.

How it will affect asset performance and capital flows has no direct historical script that can be simply copied.Key factors include how long the conflict lasts, the scope of strikes and counterstrikes, the extent of the 'blockade,' and its impact on oil prices.

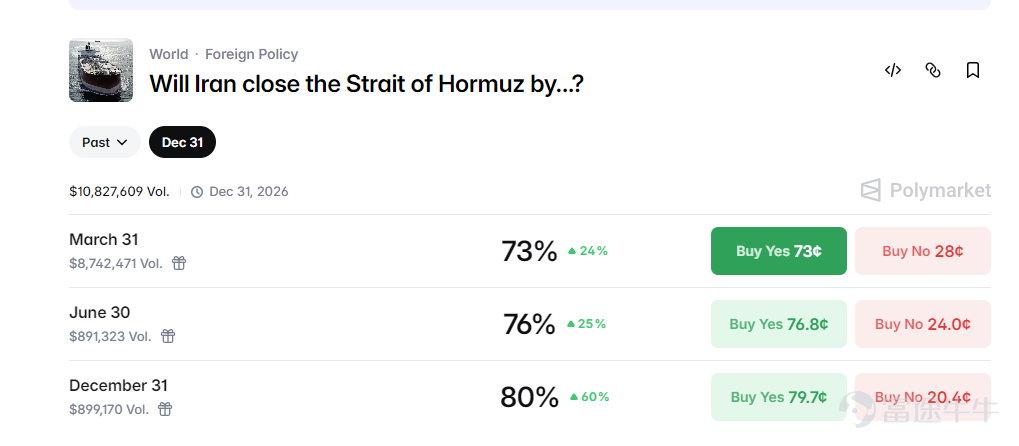

Currently, on the Poly market, the bet on the blockade of the Strait of Hormuz before December 31 has reached 80%.The probability of a blockade in 3, 6, and 12 months is increasing.

Trump's escort statement last night was a typical event-driven policy intervention. Its effect was more akin to injecting 'strong damping' into a highly volatile market rather than fundamentally reversing the situation.

Constraints of military capabilityare the primary issue. Several shipowners expressed uncertainty about whether the US military has enough vessels.Time lag and limitations in the transmission of insurance mechanismsThis should not be overlooked either. It can be said that as long as the conflict continues, Trump's plan may not be sufficient to fully reassure the shipping industry.

This uncertainty has led to a large-scale withdrawal of funds from risky assets.

2) Rising oil price expectations → resurgence in inflation/interest rate trajectory, directly hitting interest-rate-sensitive assets

Once the market begins to seriously price in a sustained premium for crude oil and freight costs, the logical chain will quickly become:

Higher oil price expectations → stickier inflation expectations → reduced room for rate cut speculation/actual interest rate rise → compressed valuation multiples.

The chart below shows Goldman Sachs' assessment of the transmission effects of rising oil prices on inflation indicators,Every sustained 10% increase in oil prices will add 4 basis points to the US core Consumer Price Index (CPI) and 28 basis points to the overall CPI.

Traders' expectations for the Fed's second interest rate cut this year have plummeted from nearly 100% last Friday to around 50%,Minneapolis Fed President Kashkari stated that a war in the Middle East could create a situation supporting a longer pause in rate cuts.

This is also why it’s common to see:The Nasdaq/high-valuation growth stocks experience sharper declines。

3) Liquidity and deleveraging amplify the drop

In the event of sudden incidents, a rise in volatility triggers systematic funds to reduce risk (volatility control, risk parity, some CTAs). Combined with the negative gamma effect from options market makers' passive hedging, this creates short-term distortions where 'the more it falls, the more selling occurs'—a typical characteristic of such declines isFast speed, strong structural nature, and weak intraday rebounds。

II. Trend outlook: Beware of reflexivity in the market; prioritize risk management over trading

The current market is in a typical 'headline-driven' mode,Volatility (VIX) remains highly sensitive to any news from the Middle East. Trump's comments only temporarily suppressed the VIX but did not ease market concerns.

At the same time, beware of reflexivity in the market; consensus equals risk,Any ceasefire signal could trigger a stampede-like pullback.

For ordinary investors, before the situation becomes clearit is more appropriate to adopt a strategy that prioritizes risk control and treats trading as secondary.Reducing overall positions and increasing cash holdings remains a prudent move.

Scenario A: Deterrence-focused, with limited actual operations

Blockades remain mostly symbolic or involve sporadic harassment, leading to a short-term but manageable increase in shipping and insurance costs. Typically, the market first completes a round of 'sentiment + risk premium' pricing, followed by a restorative rebound and volatility. After one to two weeks of panic, the market begins to digest risks, with US stocks stabilizing at the bottom.

Scenario B: Periodic, recurring disruptions to shipping

If repeated vessel inspections, harassment, escalations in escort operations, and significant increases in insurance rates occur, energy prices and freight rates will sustain a persistent premium. Correspondingly, for the US stock market:Indices struggle to establish trends, and industry divergence widens.。

– Relatively benefiting / stronger defensive sectors include: upstream oil and gas along with oilfield services, certain refining chains, and defense-related military industries.

– Relatively under pressure: Aviation, transportation logistics, chemicals and high-energy manufacturing, discretionary consumption; high-valuation growth stocks sensitive to interest rates

Scenario C: Substantial lockdown or broader retaliation chain

This would pull the market towards the hardest-to-trade combination:Downward revision of growth + upward revision of inflation (quasi-stagflation shock)Inflation data picks up again, forcing the Fed to maintain high interest rates. Credit spreads and volatility may expand further, requiring equities to trade at a lower valuation center to absorb uncertainty.

Three, what should be done at this stage: Based on 'your current holdings + risk appetite'

During periods of event risk, the 'uncertainty premium' often persists longer than 'definitive conclusions.' For most portfolios, reducing high beta and crowded trade exposure, using options to cap drawdowns, and waiting for clearer turning-point signals from oil prices and credit/volatility before adding risk is more prudent.

Below we offer some reference option strategies tailored to different investors' holdings and risk preferences.

During periods of event-driven volatility, implied volatility tends to be elevated, making options premiums relatively expensive, prioritize usingSpread/Collar and other strategiesLower costs, define risks clearly; try to avoid selling options naked.

1) If you are 'long the index' and want to control drawdowns

– Low risk preference: Collar option strategy (Collar)

- Suitable for: Investors with large positions who prioritize drawdown control psychologically, holding spot/ETF without wanting to sell

- Logic: Taking $Invesco QQQ Trust (QQQ.US)$ as an example, while maintaining holdings, sell call options and use the premium collected to buy an equivalent number of out-of-the-money put options, giving up short-term index rebound gains in exchange for free protection against sharp declines. Suitable for guarding against the occurrence of a 'pessimistic scenario'.

(The design images displayed on screen are for illustrative purposes only and do not constitute any investment advice or guarantees; market conditions fluctuate frequently, and the option prices shown do not represent real-world values.)

2) If you believe that ongoing risk containment will continue to cause fluctuations, and you want to participate in benefiting industries but fear chasing highs

– Medium risk preference: Bull Call Spread

- Suitable for: Making 'thematic expressions' with small positions. Give yourself a clear maximum cost while retaining upside potential.

- Logic: Taking $United States Oil Fund LP (USO.US)$ For example, buy at-the-money call options (Call) and sell out-of-the-money call options (Call). Control the cost of going long while betting on the evolving logic of oil prices and military orders, while avoiding the risk of a dual hit to IV (implied volatility) caused by a sudden cooling of events.

(The design images displayed on screen are for illustrative purposes only and do not constitute any investment advice or guarantees; market conditions fluctuate frequently, and the option prices shown do not represent real-world values.)

3) You already hold energy stocks, optimistic about the upward trend but worried about a pullback after a surge

– Low-risk protective put options, or medium-risk covered call strategies

– Suitable for: Many who are reluctant to sell during an energy rally but can't withstand a pullback; a protective put is a cleaner way to 'lock in profits'

Alternatively, if focusing more on yield enhancement, one can partially write covered calls in a high-volatility environment. While holding stocks, sell out-of-the-money calls (call options) to take profits. However, be prepared for the possibility of being assigned and having to sell the stock, using the same example. $United States Oil Fund LP (USO.US)$ As an example:

(The design images displayed on screen are for illustrative purposes only and do not constitute any investment advice or guarantees; market conditions fluctuate frequently, and the option prices shown do not represent real-world values.)

4) You hold tech stocks or other affected sectors, want to hold them long-term, but are concerned about further declines in the near term

– Conservative approach: Protective put options

– Suitable for: Investors who believe in the company’s value, are willing to continue holding long-term, but are concerned about short-term volatility and pullbacks

Logic: Take the same example, while maintaining a position in the underlying stock, buy out-of-the-money put options to hedge against sharp declines in tech stocks due to upward revisions in interest rate expectations and risk aversion in an 'escalation scenario' at a controlled cost (premium). In a 'base scenario,' the rebound in spot prices should cover the premium loss. $NVIDIA (NVDA.US)$ Logic: Using the same example, while maintaining a position in the underlying stock, buy out-of-the-money put options to hedge against sharp declines in tech stocks due to upward revisions in interest rate expectations and risk aversion in an 'escalation scenario' at a controlled cost (premium). In a 'base scenario,' the rebound in spot prices should cover the premium loss.

(The design images displayed on screen are for illustrative purposes only and do not constitute any investment advice or guarantees; market conditions fluctuate frequently, and the option prices shown do not represent real-world values.)

Geopolitical conflicts often lead to sharp declines driven by sentiment, which is both a risk and a litmus test for portfolio resilience. Do not blindly sell stocks when the VIX peaks; instead, use option tools effectively to hedge tail risks

Finally, here's a small perk for fellow investors—welcome to claim it!Options Beginner Pack

This event is exclusively for invited HK users, click to learn moreDetailed event rules >>

Futu's simulated trading challenge is now open for registration! Zero cost, zero risk, and you can win stock cash vouchers!Click to learn more

Disclaimer

This content does not constitute any offer, solicitation, recommendation, opinion, or guarantee of any securities, financial products, or tools. The risk of loss in buying and selling options can be substantial. In some cases, your losses may exceed the initial margin amount deposited. Even if you set contingent orders, such as 'stop-loss' or 'limit' orders, these may not necessarily prevent losses. Market conditions may make these orders unexecutable. You might be required to deposit additional margin within a short period. If you fail to provide the required amount within the specified time, your open positions may be liquidated. However, you will still be responsible for any account deficit arising from this. Therefore, before trading, you should study and understand options and carefully consider whether such trading suits you based on your financial situation and investment objectives. If you trade options, you should be familiar with the procedures upon exercising options and at expiration, as well as your rights and obligations when exercising options and at expiration.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (8)

to post a comment

46

32