Fiber optic shortage triggers upstream supply crisis! Will fiber optic stocks keep soaring?

Marvell Earnings Preview: Can Three Key Highlights Fill the Performance Gap Until FY28?

Author | Eric

The global AI interconnection chip giant $Marvell Technology (MRVL.US)$ is set to announce its FY2026 Q4 earnings report after the market closes this Thursday Eastern Time. Last quarter, the company’s forecast that its XPU business would scale up in FY28 was accepted by the market, but performance before FY28 remains in a vacuum period; attention will be on whether management revises its guidance upward.

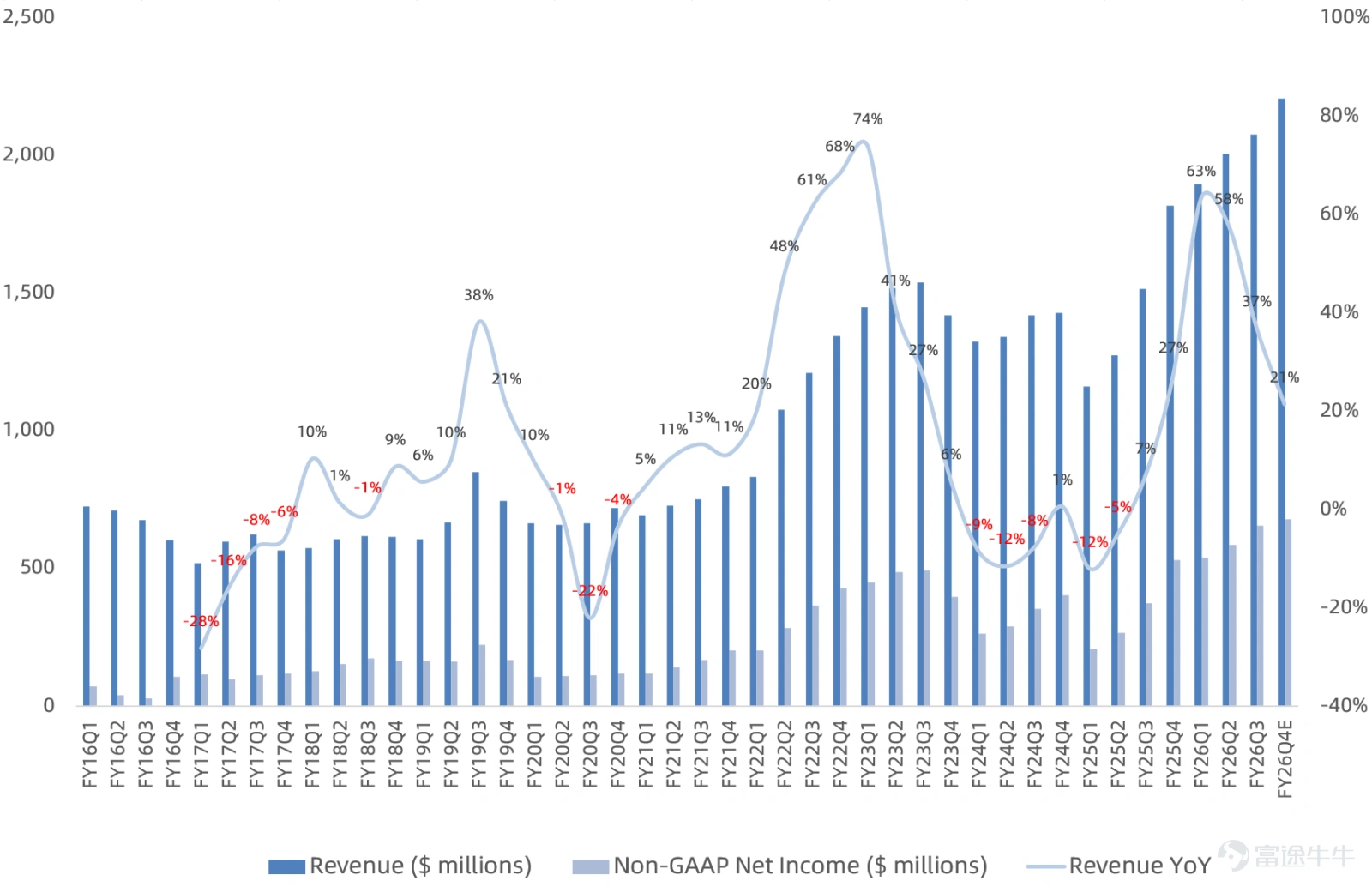

Consensus expectations for core financial metrics in Q4:

- Revenue consensus is$2.26 billion, growing by21%, representing a 6% increase quarter-over-quarter, while the previous company guidance was $2.2 billion.

- GAAP gross margin consensus is51.3%, increasing by 0.8 percentage points year-over-year but declining by 0.3 percentage points quarter-over-quarter, with the company's guidance ceiling at 52.1%. The consensus market expectation for Non-GAAP gross margin is59.1%, decreasing by 1 percentage point year-over-year and by 0.6 percentage points quarter-over-quarter, with the company’s guidance ceiling at 59.5%.

- Consensus GAAP net profit is expected to beUSD 297 million, growing by48%, previously the upper limit of the company’s guidance was USD 309 million. The market consensus for Non-GAAP net profit isUSD 678 million, growing by28%, while the previous upper limit of the company's guidance was USD 677 million.

Three key highlights of this earnings report:

1. Demand for AWS Trainium3 has been confirmed. Can it save the sluggish XPU business?

The market is most concerned about $Amazon (AMZN.US)$ AWS Trainium 3 orders. Last quarter, management stated they had secured all purchase orders for the next fiscal year’s current forecast for the next-generation XPU project (AWS Trainium 3). However, this does not seem to align well with the guidance of 20% growth in the custom data center business by FY27 and Amazon's projection of a significant increase in Trainium 3 production next year, possibly due to more Trainium 3 orders being taken by Alchip. In fact, the growth rate of the custom business for FY27 may be lower than that of the overall data center business.

Recently, Amazon has accelerated the deployment of AWS Trainium, securing a major 2GW order from OpenAI. Whether the company’s market share and unit value in Trainium 3 can reverse the long-term sluggishness of the XPU business still awaits clarification from management.

2. Can the storage business benefit from the industry’s supercycle boom?

Marvell's current storage product line includes HDD Controllers, SSD Controllers, SSD Converter Controllers, and Fibre Channel HBAs & Controllers. These products are used not only in data centers but also in consumer electronics.

Since FY22Q3, Marvell has ceased to separately disclose its storage business revenue.Prior to this, the scale of its storage business was approximately $12 billion on an annualized basis.If this segment can benefit from a super cycle of price increases in the storage industry going forward, it may significantly contribute incremental growth to Marvell’s overall performance.

In the previous quarter's earnings call, management did not mention any benefits to the storage business,only stating that data center storage business had seen double-digit growth quarter-over-quarter.We will observe whether this will constitute a major variable this quarter.

3. Will the long-term guidance for the optical interconnect business and XPU attach custom chips be raised?

Marvell’s full suite of optical interconnect products includes DSPs for Active Electrical Cables (AEC) and Active Optical Cables (AOC), Retimers for PCIe, Ethernet, and UA Link, as well as silicon photonics technology for near-packaged and co-packaged XPU optics.

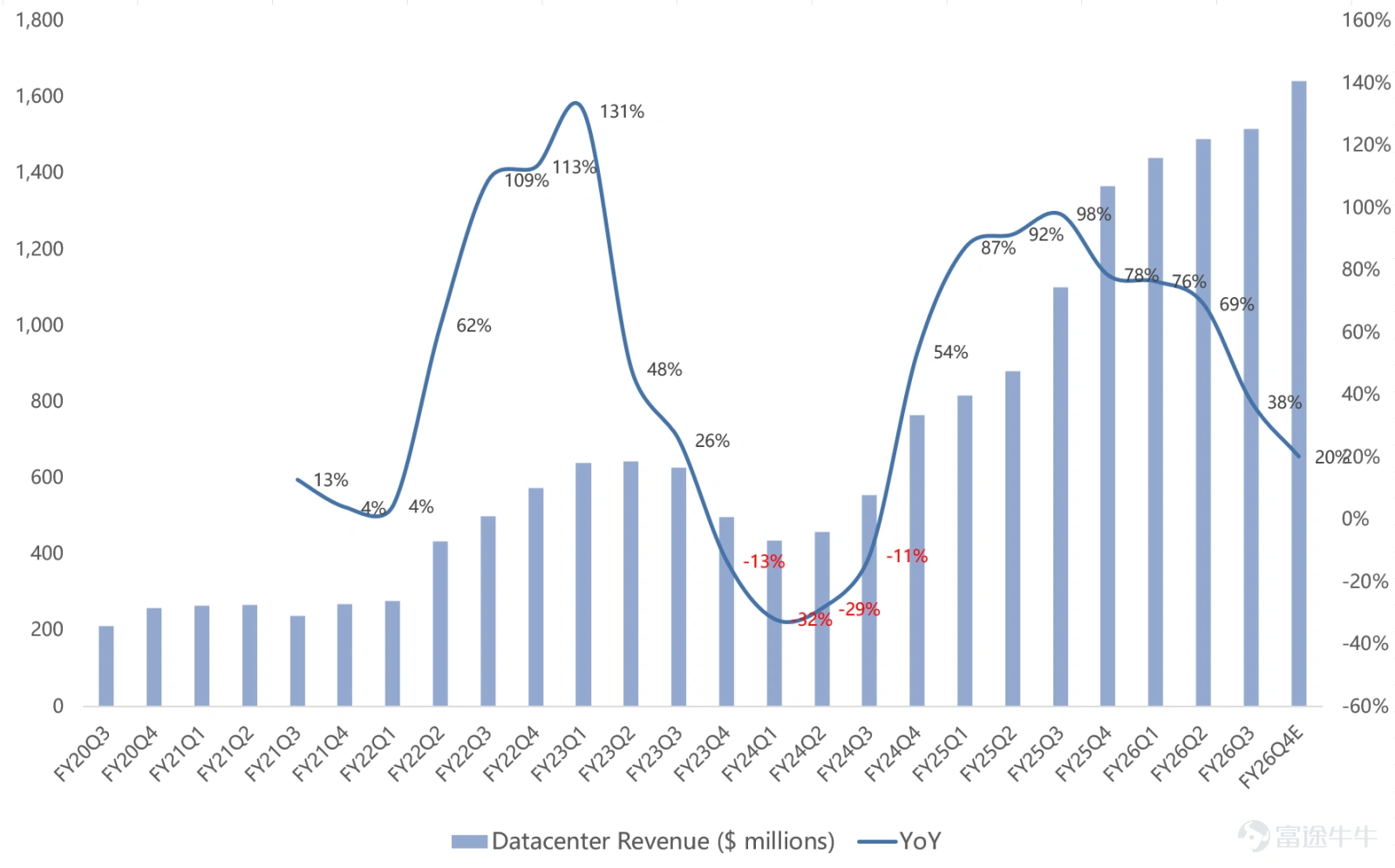

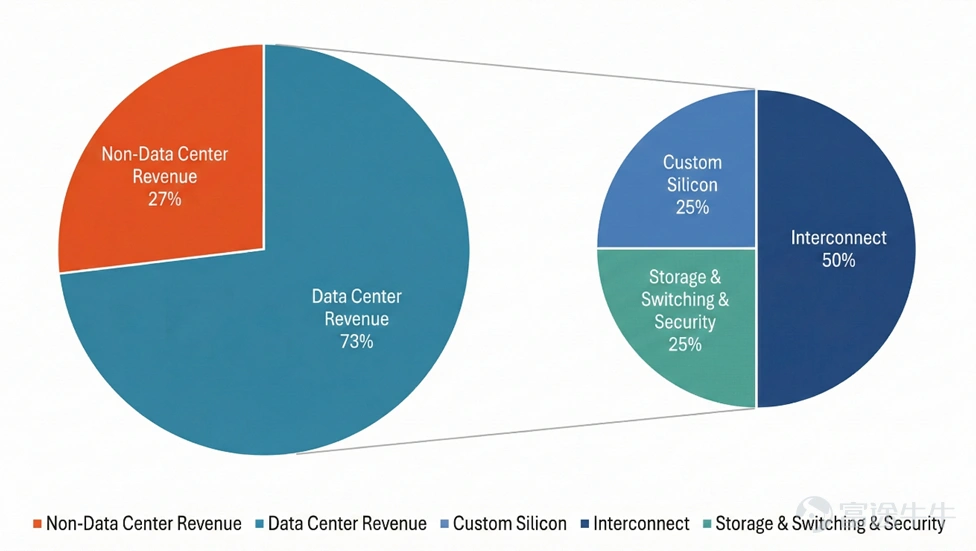

Currently, Marvell’s data center revenue growth is mainly driven by optical interconnect products.The company previously indicated that revenue from optical interconnect products accounts for a portion of data center revenue.50%, XPU (ASIC) accounts for25%. The remainder is composed of data center storage, switching, and security product portfolios. Data center switching business management anticipates a strong ramp-up by FY27, with revenue expected to exceed $500 million.AEC and Retimer become the company's new interconnect growth points, and the company’s market share is expected to continue growing,The combined revenue from AEC and Retimer in FY27 is expected to double.Management forecasts that the merchant scale-up switch market will have approximately $6 billion in opportunity by 2030. With optical interconnect attach on both the XPU and switch sides, the total addressable market for interconnects could exceed $10 billion.

Contrary to the previous market consensus that custom business primarily relies on XPU, management indicated there are now over15 XPU attach chip design wins, and based solely on design wins in NIC and CXL use cases, the company is expected to achieveover $2 billion in revenue by FY29.。

Summary

Overall, given the current stringent earnings report requirements for semiconductor companies in the US stock market,there are high expectations regarding gross margin trends, guidance upgrades, and the scale of backlog orders.This is especially true considering Marvell's long performance vacuum period before fiscal year 2028.

Reviewing the past eight quarters of earnings day stock price fluctuations, the stock price closed higher three times.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

1