NVIDIA publicly showcases CPO switches—could optical communication stocks be turning around?

Optical communication identified as the new bottleneck! Comprehensive comparison of dual leaders LITE and COHR

Author/Richard

NVIDIA splurged $40 billion yesterday to invest in two leading optical communication companies, aiming to secure key capacity for the next-generation AI computing architecture’s 'optical interconnect' era. Following the announcement, shares of both companies surged over 10% amid high trading, reflecting the market's repricing based on 'tight supply of upstream critical components + long-term volume commitments'.

Securing lasers, InP, and U.S.-based production capacity

What NVIDIA is betting on this time is not the currently largest but lower-barrier 'optical module' market, but rather more focused onthe upstream, more core parts of the optical communication chain with lower geopolitical risks—U.S.-based critical light source and component production capacity, with a focus on core areas like lasers and InP (Indium Phosphide).

– Correct $Coherent (COHR.US)$ : This funding 2 billion dollarswill be prioritized for capital expenditures, particularly expanding its Texas Sherman facility The factory's InP production capacity. Meanwhile, the 'multi-billion dollar' procurement commitment plan will commence in early 2027and continue until 2030。

– Correct $Lumentum (LITE.US)$ : The primary use of the funds is forconstructing a 'brand-new' wafer fabrication plant (new fab) in the United States. The company previously disclosed an anticipated 'several hundred million dollar' procurement order expected to be fulfilled in the first half of 2027; however, NVIDIA’s current procurement and investment leans more towards 'incremental variables,' with incremental revenue expected from the second half of 2027.

Comparison of two leading companies

Lumentum is currently a key supplier for NVIDIA in the CPO and pluggable optical module space,CW lasers, EML optical chips,and holds a leading position in the high-speed laser field, which represents its core competitive advantage. Its flagship products include 100G/channel EML (Electro-Absorption Modulated Lasers) used in 800G optical modules, with ongoing efforts to ramp up production of 200G/channel EMLs for 1.6Tb/s modules. Currently, Lumentum's InP laser chips are nearly sold out, and even with continuous capacity expansion, demand still significantly exceeds supply.

Coherent is also one of NVIDIA's suppliers,for CW lasers, ELSFP modules, and 800G/1.6T optical modules.Coherent was formed through the acquisition and merger of legacy optical communication company II-VI with Finisar and Coherent Inc., followed by a name change. Compared to Lumentum, Coherent has a broader business scope (lasers, devices, components, etc.), but the debt burden from acquisitions has kept its stock price range-bound for an extended period. As AI investment booms, Coherent's industrial capabilities and customer penetration in the optical communications field have become more evident.

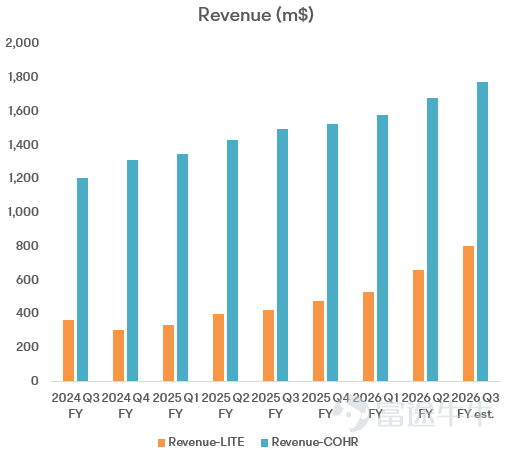

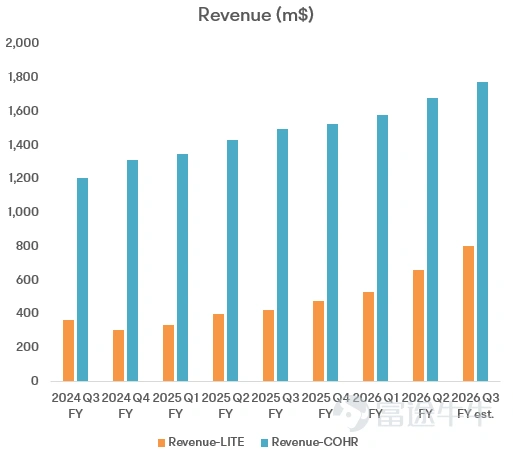

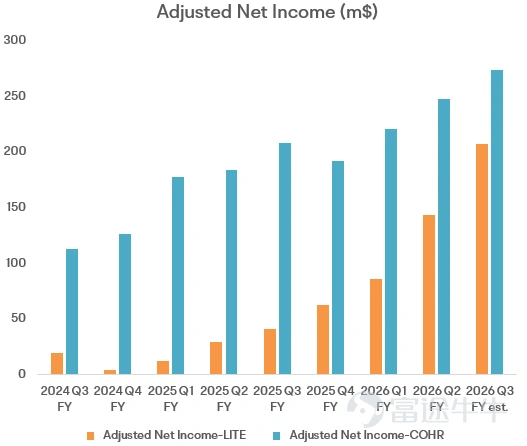

1. Financial Performance: Lumentum shows faster growth

In terms of scale, Coherent’s data communication business is significantly larger than Lumentum’s. For instance, in its recently disclosed FY26 Q2 results, Coherent reported quarterly revenue of approximately $1.6 billion, including about $1.2 billion related to data centers/communications and around $400–500 million from industrial applications. Meanwhile, Lumentum's total revenue for the quarter was approximately $630 million. On a comparable basis, Coherent’s optical network-related business is roughly twice the size of Lumentum’s.

However, in terms of profitability improvement, Lumentum exhibits a steeper trajectory: driven by products such as high-speed lasers, its gross margin has risen sharply over the past two years (Increased from 32% in FY25 Q2 to 42% in FY26 Q2), leading to a faster pace of net profit improvement; in comparison, Coherent's gross margin increased from38% in FY25 Q2to 39% in FY26 Q2, showing a slower rate of increase.

2. New TAM Technology Positioning: Lumentum Currently Holds an Advantage

Morgan Stanley noted in a report: Continued upward bandwidth growth in AI data centers and traditional technology nearing bottlenecks (copper transmission distance, single-channel/laser speed, I/O constraints, etc.) will force new technological evolutions in network architecture, thereby expanding the TAM: The optical-related market (fiber, scale-out, scale-across) is expected to reach approximately USD 300 billion by 2025, with a40% CAGR。

over the past four years driven by AI DC investments. As speeds increase and the 'reach of optics expands,' even though some solutions (especially on-board CPO) may squeeze the profit pool of traditional optical modules, the base case still sees growth in the optical communication space to about90 billionUSD level.

Morgan Stanley divided the 2028 TAM into Scale-Up / Scale-Out / Scale-Across three major scenarios, with TAMs of approximately9.4 billion USD, 64 billion USD, and 9.1 billion USD, totaling approximately82.5 billion USD。

(Scale-Up, Scale-Out, and Scale-Across refer to vertical, horizontal, and cross-regional expansion in data centers, respectively.)

Scale-Up / Scale-Out

Based on Morgan Stanley's scoring of the 'exposure intensity' of two leading companies in niche markets:

– LITEThe coverage is broader, and it is more proactive in directions related to the 'new architecture'.

– COHRIt leans more towards the 'core large-cap' of the currently largest optical module sector and stands out more in areas like 'fiber replacing copper interconnects' within racks; its scores in some CPO sub-sectors are relatively weaker.

However, it must be emphasized that this scoring might be relatively 'static', because in NVIDIA's recent investment and cooperation statement,both companieshave been explicitly included in the procurement/integration system related to CPO.More importantly, NVIDIA is unlikely to rely on a single optical component supplier for critical components; a dual or multiple supplier model aligns better with its supply chain risk management logic.

Manufacturing and Capacity: The Key Growth Foundation for the Future, Coherent Moves Faster

Indium phosphide (InP) is a III-V compound semiconductor, which hasa direct bandgap, high electron mobility, and low optical losswith excellent characteristics. The InP substrate serves as the core foundational material for optical devices, acting as the 'foundation' of photonic chips, upon which core structures such as lasers and detectors are later built using epitaxial growth technology.

Coherent boasts a larger manufacturing network with more aggressive capacity upgrades. By 2025, the company will complete a key transition: shifting InP laser production from traditional3-inch wafersto6-inch wafers. New 6-inch InP production lines have been commissioned at its Sherman, Texas plant and the Järfälla plant near Stockholm, Sweden. Management expects this to bring about a long-term reduction in die costs. A larger scale of production expansion and faster capacity ramp-up give it an edge in terms of 'deliverability' on the supply side.over 60%The cost per die decreases. Larger production scale and faster capacity ramp-up give it a relative advantage in terms of 'deliverable capability' on the supply side.

Lumentum is also expanding production, but at a slightly different pace and scale: its InP wafer capacity is primarily concentrated in San Jose, USA, where upgrades and renovations are underway; the company recently disclosed an investment of approximately $43 million aimed at increasing InP chip capacity by40%. NVIDIA's currentUSD 2 billioninvestment is more directly focused on 'building a brand-new InP wafer fab in the US,' creating room for imagination regarding its capacity curve.

Conclusion

NVIDIA's rare move to provide 'funding + long-term volume commitments' upstream in the supply chain essentially declaresOptical communication is becoming the next critical bottleneck in AI infrastructure and a differentiated technological segment competing with ASICs。

Against the backdrop of similar market capitalizations,Lumentum and Coherentwill both benefit from NVIDIA's deepened cooperation and the longer-term, broader trend towards co-packaged optics (CPO) transformation. For investors, the optimal strategy at present might be to opportunistically increase exposure to the 'optical interconnect' sector amid volatile market conditions, while closely monitoring the progress of customer adoption, product competitiveness, and gross margin changes for both companies, and dynamically adjusting expectations and allocations accordingly.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (2)

to post a comment

30

104